Small Business Succession Planning: Protecting Your Legacy with a Trust

Most small business owners build something valuable over decades, then leave its future to chance. Without a clear plan, your business could face years of legal battles, tax penalties, or even forced sale after you’re gone.

Small business succession planning isn’t just paperwork-it’s how you protect what you’ve built for your family. We at Law Offices of Roshni T. Desai help owners create strategies that keep their business intact and their heirs out of conflict.

Why Your Business Needs a Succession Plan

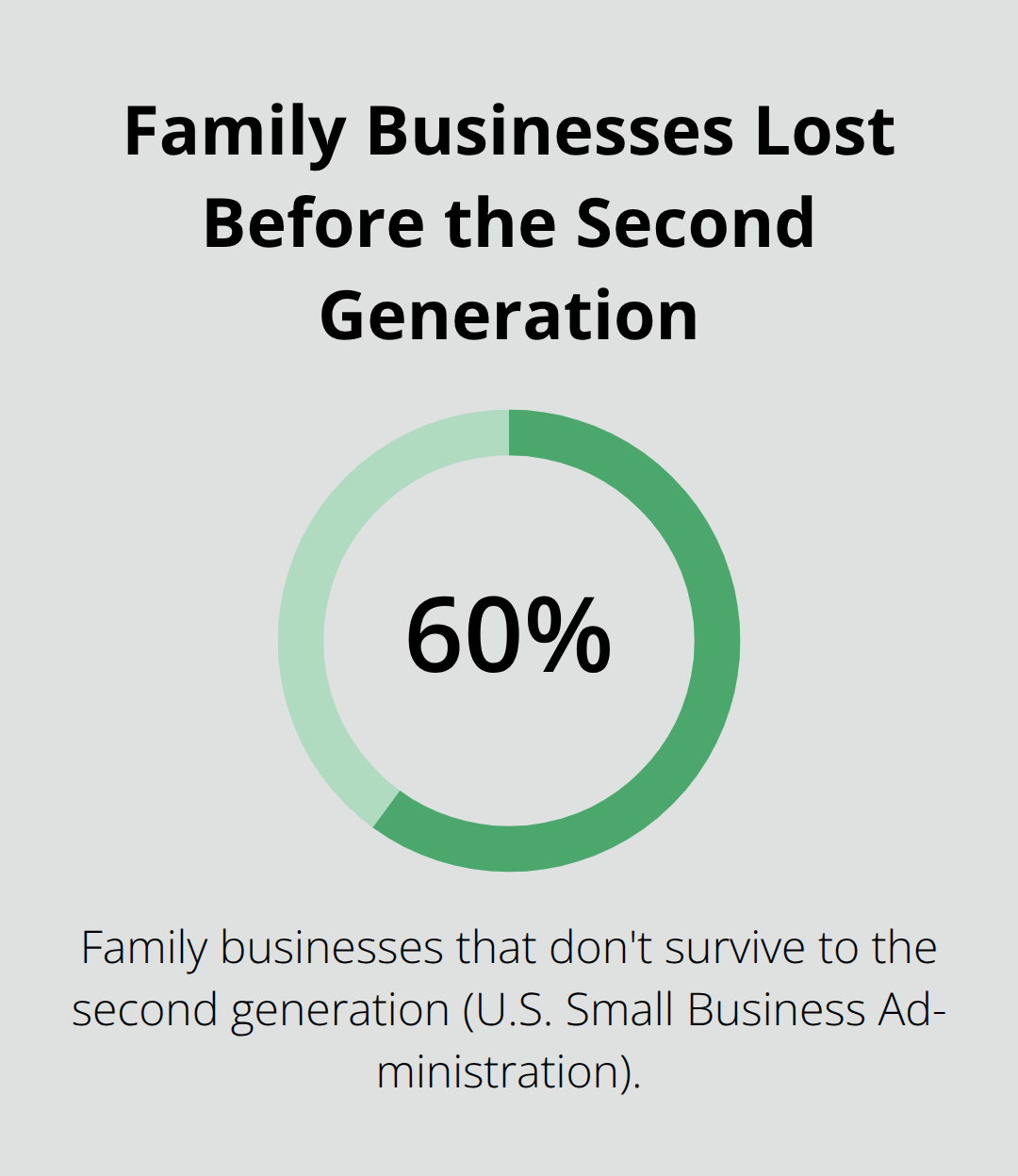

Without a succession plan, your business enters a danger zone the moment something happens to you. According to the U.S. Small Business Administration, about 60 percent of family businesses don’t survive to the second generation, and lack of planning is a primary reason.

When you die or become incapacitated without a documented plan, your heirs face immediate decisions under stress-often without knowing your wishes or having the skills to run operations. The business stalls for months while courts appoint a conservator, customers leave due to uncertainty, and key employees seek jobs elsewhere. Your family also faces a forced choice: sell the business quickly at a discount or scramble to learn how to run it while managing grief and financial pressure.

Probate Drains Your Estate’s Value

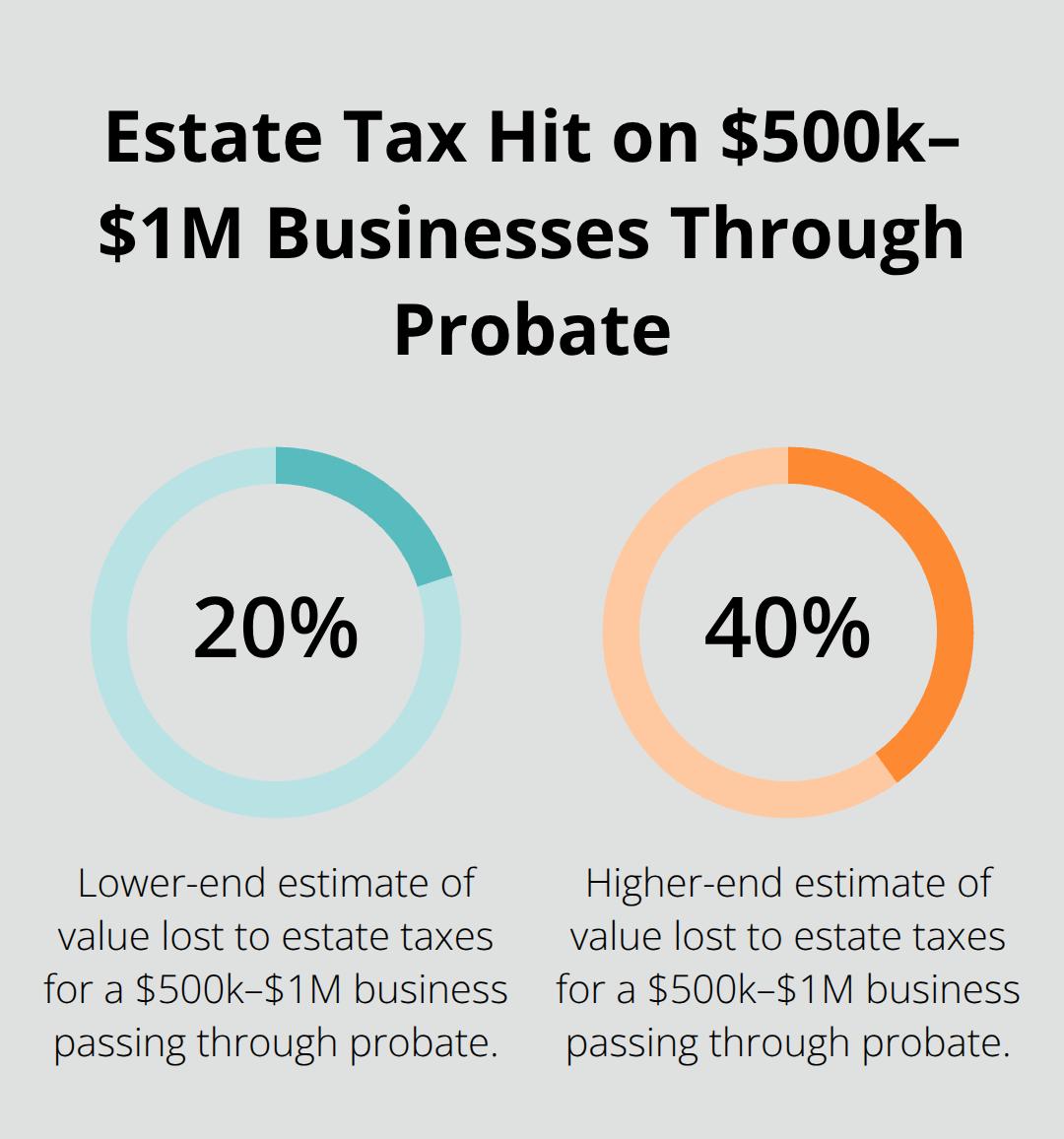

Probate is expensive and public. If your business passes through probate, your family pays court fees, attorney costs, and delays that stretch 12 to 18 months or longer depending on your state. During that time, the business sits in limbo while the court oversees every decision. Your estate may also owe federal and state taxes on the business’s full value at your death. For a business worth $500,000 to $1 million, estate taxes can consume 20 to 40 percent of the value before heirs receive anything.

A trust bypasses probate entirely, keeping your business operating smoothly and privately while reducing or eliminating those tax hits. A revocable living trust lets you maintain full control during your lifetime and names a successor trustee to take over without court involvement if you die or become unable to work.

Family Disputes Destroy Businesses and Relationships

Family disputes over business ownership happen more often than you think. When ownership intentions aren’t clear, siblings fight over control, compensation, and direction. One child wants to sell; another wants to grow it. A third feels left out and demands money. Without a documented plan, these disagreements turn into costly litigation that fractures family bonds permanently (and can cost tens of thousands in legal fees).

A well-drafted succession plan inside a trust makes your wishes binding and removes guesswork. It specifies who inherits the business, who manages it day-to-day, and how other heirs receive fair compensation. This clarity prevents resentment and keeps the business functioning while family members grieve together instead of fighting in court.

What Happens When You Become Incapacitated

Incapacity planning matters as much as planning for death. If you suffer a stroke, accident, or illness that leaves you unable to make decisions, your business needs someone to act immediately. Without a plan in place, your family may need to petition a court for a conservatorship-a public, expensive process that can take weeks or months. During that gap, vendors don’t get paid, contracts lapse, and clients wonder if the business will survive.

A revocable living trust with a named successor trustee eliminates this problem. Your chosen successor can step in right away to manage the business and make decisions without court involvement (or the delays and costs that come with it). This keeps operations running and protects your business value during a vulnerable time.

These risks make succession planning urgent. The next section shows how trusts become the foundation of a protection strategy that addresses all three threats at once.

How Trusts Keep Your Business Intact

Why a Revocable Living Trust Outperforms a Will

A revocable living trust is the single most effective tool for protecting a small business during succession. Unlike a will, which must go through probate, a trust takes effect immediately and transfers your business to your chosen successor without court involvement, public disclosure, or the months of delay that drain business value. When you place your business into a revocable living trust during your lifetime, you retain complete control and can modify or revoke it anytime. If you become incapacitated, your named successor trustee steps in right away to manage operations and make decisions without waiting for a court-appointed conservator. This continuity matters enormously.

The American Bar Association notes that probate delays alone cause key employees to leave, customers to seek competitors, and vendors to demand payment upfront due to uncertainty about the business’s stability. A trust eliminates that crisis window entirely.

Designating a Trustee With Industry Knowledge

You can use the trust language to designate a special trustee with industry knowledge to oversee the business-someone who understands your operations better than a family member might. This separation of roles keeps the business focused on serving clients while your family handles personal matters without interference. For S-corporations or partnerships, the trust structure must align with your governance documents, so amendments or careful drafting become necessary to avoid restrictions like rights of first refusal that might block transfers.

The Privacy Advantage Trusts Deliver

Privacy is another major advantage trusts deliver that wills cannot match. Probate is a public court proceeding, meaning anyone can walk into a courthouse and review your business valuation, asset distribution, and family details. A trust avoids this entirely-your business succession, valuations, and personal wishes remain completely private. No public record exists. This protects you from unwanted solicitation, competitor intelligence gathering, or family members outside the business learning details they shouldn’t know.

Tax Savings and Liquidity Planning

A properly funded revocable trust avoids federal estate taxes for many owners and reduces state-level exposure. If your business is valued at $500,000 to $1 million, the difference between probate and trust succession can mean your heirs receive an additional $50,000 to $200,000 depending on your state’s tax rates and the length of probate delays. Funding your trust with your business interests during your lifetime rather than naming the trust as a beneficiary after death gives you control over the timing and allows you to pair the transfer with life insurance or disability insurance to cover liquidity needs when a partner dies or becomes unable to work.

These protections set the foundation for your succession strategy, but they work best when paired with clear documentation of who will actually run the business and how ownership transfers happen. The next section addresses the mistakes that undermine even well-intentioned plans.

Common Succession Planning Mistakes Small Business Owners Make

Most small business owners who attempt succession planning make one critical error: they confuse having documents with having a real plan. A will or trust sitting in a drawer means nothing if it doesn’t reflect your actual business structure, your successor’s readiness, or the tax realities of your state. The three mistakes that destroy otherwise sound intentions happen because owners either rush the process, avoid difficult conversations, or fail to coordinate their business documents with their personal estate planning.

Conflicting Documents Create Litigation Instead of Clarity

Ownership intentions must be spelled out in writing within your operating agreement, partnership agreement, or corporate bylaws-not just in a trust or will. If your trust states your daughter inherits the business but your partnership agreement gives your partner a right of first refusal to buy it, those documents will conflict and create exactly the litigation you were trying to prevent. This coordination failure happens constantly because owners treat their trust as separate from their business governance documents, when in fact they must work together seamlessly. An attorney needs to review all documents side by side and identify conflicts before they surface after your death or incapacity.

Choosing a Successor Based on Family Loyalty Leads to Failure

Selecting a successor based on family loyalty rather than actual capability and willingness to lead the business is a recipe for failure. The National Federation of Independent Business found that family business succession succeeds at higher rates when the chosen successor has worked in the business for at least five years and has demonstrated specific operational skills-not just general management ability. If your son has no interest in running the company but you name him anyway because he’s the oldest, you set him up for stress and the business for decline. An honest conversation about readiness-or a trial management period-reveals whether your chosen successor can actually handle the role before documents lock in that decision.

Tax Laws and Timing Create Hidden Costs

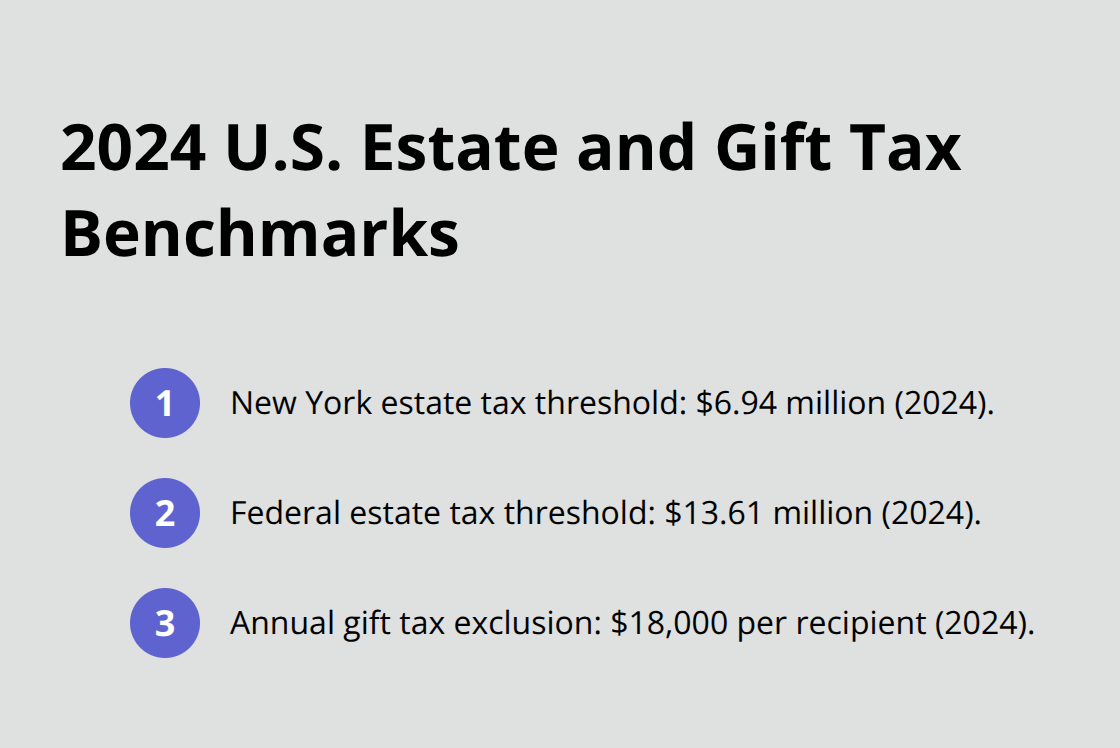

Ignoring state-specific tax laws and timing requirements costs owners thousands in unnecessary taxes and penalties. New York imposes a state estate tax on estates over $6.94 million as of 2024, while federal estate tax applies to estates exceeding $13.61 million.

Many owners fund their trusts incorrectly or transfer business interests at the wrong time, missing opportunities to use annual gift tax exclusions (currently $18,000 per recipient in 2024) to gradually shift ownership without triggering taxes. Additionally, S-corporation owners must verify that any trust holding business shares qualifies as a Qualified Subchapter S Trust or Electing Small Business Trust, or the business loses its tax status and faces unexpected tax bills.

Mistakes Compound When Discovered Too Late

These mistakes compound because heirs discover them only after an owner dies or becomes incapacitated, when they’re forced to unwind conflicting documents or pay penalties for tax violations. The solution requires three concrete actions: have an attorney coordinate your trust, operating documents, and tax strategy in writing; assess your chosen successor’s actual readiness through honest conversation and possibly a trial management period; and map out the timing of any business transfers to align with your state’s tax laws and your personal financial situation.

Final Thoughts

Small business succession planning protects what you’ve built by addressing three vulnerabilities at once: business continuity, family harmony, and tax efficiency. A revocable living trust funded with your business interests eliminates probate delays, keeps your succession private, and allows a named successor trustee to step in immediately if you die or become incapacitated. Coordinating that trust with your operating agreements, partnership documents, and tax strategy removes the conflicts that turn succession into litigation.

The cost of waiting far exceeds the cost of planning now. Every month you delay leaves your business exposed to the risks that destroy 40 percent of family businesses before the second generation takes over. If you become incapacitated tomorrow, your family faces court proceedings, operational paralysis, and decisions made under crisis conditions. If you die without a plan, your heirs may be forced to sell the business at a discount just to cover taxes and legal costs.

We at Law Offices of Roshni T. Desai help small business owners create succession strategies tailored to their specific structure, state tax laws, and family goals. Start with a free consultation to review your current situation and identify the gaps in your plan. Contact us today to secure your business future and give your family the clarity and protection they deserve.