Elder Law Planning Options for Southern California Families

Planning for your later years involves more than just thinking about retirement income. You need clear legal documents, strategies to protect your assets, and a plan that reflects your wishes for healthcare and end-of-life decisions.

At Law Offices of Roshni T. Desai, we help Southern California families navigate elder law planning options that address these critical areas. This guide covers the tools and strategies you need to protect yourself and your loved ones.

Who Should Make Your Healthcare and Financial Decisions?

A power of attorney document names someone to act on your behalf when you cannot. This matters more than most people realize. Without one in place, your family may face court proceedings to gain authority over your finances or medical decisions-a process that costs thousands of dollars and creates delays when time is critical.

California law recognizes two separate powers of attorney: one for financial matters and one for healthcare decisions. You need both.

Financial Power of Attorney

The financial power of attorney gives your chosen agent authority to manage bank accounts, pay bills, sell property, and handle investments. This person can act immediately if you become incapacitated, without waiting for court involvement.

Healthcare Power of Attorney

The healthcare power of attorney, also called a healthcare proxy or medical power of attorney, lets you appoint someone to make medical decisions if you cannot communicate your wishes. This agent speaks to doctors, approves treatments, and decides about life support.

Living Wills and Do-Not-Resuscitate Orders

Living wills and do-not-resuscitate orders take this further by spelling out exactly which medical interventions you want or refuse. A living will documents your preferences about feeding tubes, ventilators, and cardiopulmonary resuscitation. A do-not-resuscitate order tells paramedics and hospital staff not to perform CPR if your heart stops.

These documents must be signed, witnessed, and notarized to be valid in California. Two disinterested witnesses or a notary are required-notary fees typically run around fifteen dollars. Without these documents in writing, hospitals may default to aggressive treatment even if that contradicts your actual wishes.

Choosing Your Agent Wisely

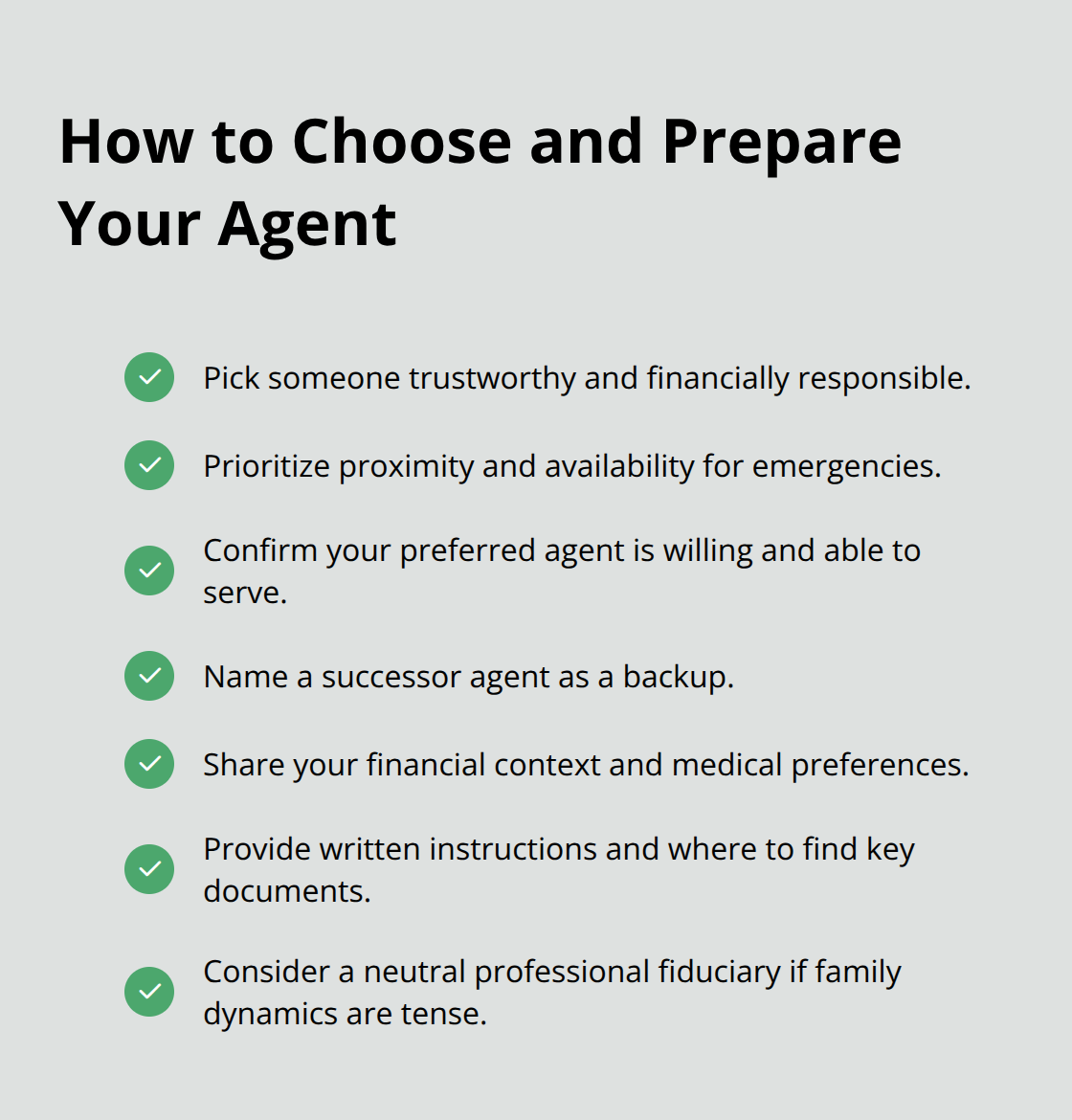

Choosing your agent is the most important decision in this process. This person will access your bank accounts, make irreversible medical choices, and potentially sell your home. Many families name an adult child out of habit, but that child may not live nearby, may lack financial knowledge, or may face conflicts of interest. Some families discover too late that their chosen agent is unwilling or unable to serve.

Name a successor agent as backup-someone who can step in if your first choice becomes unavailable. Have direct conversations with whoever you name, explaining your financial situation, your medical preferences, and where to find your documents. Many agents feel blindsided when they suddenly need to act.

Providing clear written instructions about your values and priorities reduces confusion and conflict.

If you have blended families or family dynamics that create tension, naming a neutral third party like a professional fiduciary may prevent disputes that drain your estate and damage relationships. With these documents and conversations in place, you establish clear authority over your finances and healthcare-setting the stage for the asset protection strategies that follow.

Protecting Your Assets During Long-Term Care

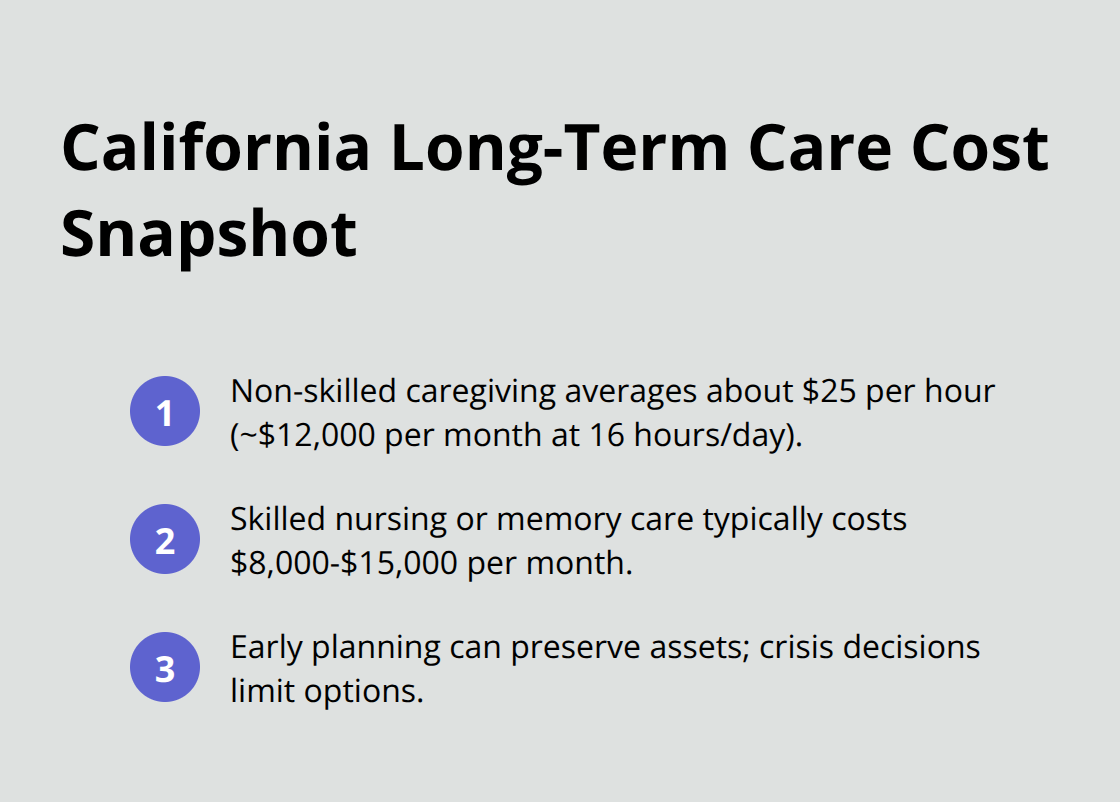

Long-term care costs in California are staggering. Basic non-skilled caregiving runs around twenty-five dollars per hour, which totals approximately twelve thousand dollars monthly for sixteen hours of daily support. Skilled nursing or memory care facilities charge between eight thousand and fifteen thousand dollars per month according to California pricing data.

These numbers matter because they determine whether your savings disappear within months or whether strategic planning preserves your assets for your family. Medi-Cal can cover these costs, but only if you structure your finances correctly beforehand. The window to plan closes quickly once care becomes necessary. If you wait until a health crisis forces immediate decisions, you lose the ability to protect assets through legal strategies. We recommend starting this conversation while parents remain healthy and capable of making their own choices.

Understanding Medi-Cal Eligibility and the Five-Year Lookback

Medi-Cal provides long-term care coverage, but the eligibility rules are strict and counterintuitive. Your home remains exempt from Medi-Cal asset limits when you or your spouse still lives there, which seems protective until you sell or transfer the property. Selling your home to pay for care can trigger immediate ineligibility because the sale proceeds become countable assets. The timing of any property transfer matters enormously. Medi-Cal includes a five-year lookback period, meaning transfers made within five years before applying may disqualify you. A parent who sells their home three years before needing care could face a penalty period where Medi-Cal refuses to pay, forcing the family to cover costs from savings. This is not a minor technicality-it can cost hundreds of thousands of dollars.

Waiver Programs and Trust-Based Asset Protection

Medi-Cal waiver programs exist in California and can ease qualification while preserving more assets than standard rules allow. These programs vary by county, so checking what’s available in your specific Southern California location is essential. Asset protection planning uses properly structured trusts to balance long-term care needs with preserving wealth. The goal is not to hide assets but to organize them legally so that your primary residence and some savings remain protected while Medi-Cal covers care expenses. A trust created and funded correctly (before any crisis) allows you to maintain control of your assets during your lifetime while positioning them to qualify for Medi-Cal when care becomes necessary.

Long-Term Care Insurance as a Strategic Alternative

Long-term care insurance offers a completely different approach. Rather than relying on Medi-Cal and spending down your assets, insurance policies cover care costs directly, allowing you to maintain your savings and home for your family’s inheritance. However, long-term care insurance premiums increase with age, and policies purchased in your seventies cost significantly more than those purchased in your fifties or sixties. Many Southern California families dismiss insurance as too expensive without comparing the actual cost of care. If you own a home worth eight hundred thousand dollars and face five years of skilled nursing care at twelve thousand dollars monthly, you need six hundred thousand dollars. Insurance might cost ten to fifteen thousand dollars annually, and over ten years that’s one hundred to one hundred fifty thousand dollars total. The math often favors insurance when you have substantial assets to protect. Conversely, if your assets are modest and you qualify for Medi-Cal anyway, insurance becomes unnecessary. The decision depends entirely on your specific financial picture and home value. High California home values create significant protection opportunities through insurance or trust-based strategies, but both require planning while you still have capacity to make decisions.

Coordinating Your Strategy With Professional Guidance

The choice between Medi-Cal planning, long-term care insurance, or a combination of both depends on your unique circumstances. Your home equity, liquid savings, family situation, and health status all factor into which approach makes sense. Some families benefit from insurance to protect substantial assets, while others structure trusts to maximize Medi-Cal eligibility. Still others use both strategies together. What matters most is that you make this decision proactively, not in crisis mode. Once you understand your asset protection options and have chosen a direction, the next step involves ensuring that your estate plan actually supports that strategy-which brings us to how your wills, trusts, and beneficiary designations must work together.

How Your Estate Plan Supports Your Asset Protection Strategy

Your wills, trusts, and beneficiary designations must align with the asset protection approach you’ve chosen. Many Southern California families create legal documents without considering how those documents interact with Medi-Cal planning or long-term care insurance. This disconnect creates problems later. If you’ve decided to use a revocable living trust for Medi-Cal planning, your will alone won’t accomplish that goal-the trust must actually hold your assets during your lifetime. If you’ve chosen long-term care insurance, your beneficiary designations on retirement accounts and life insurance need to work together so that inheritance doesn’t disrupt your spouse’s financial security.

Understanding Probate Thresholds and Trust Funding

The probate threshold in California matters significantly. According to California Probate Code Section 6240, assets exceeding $184,500 require probate unless they’re already in a trust or have payable-on-death designations. Probate typically takes around nine months minimum and costs thousands in attorney fees and court costs. A properly funded living trust bypasses probate entirely, which matters significantly when you’re coordinating Medi-Cal eligibility or protecting assets for your spouse.

Transfer on Death deeds allow you to pass real property to beneficiaries without probate and can be revoked anytime, making them useful for supplementing trust-based strategies. However, they don’t provide the control or tax benefits of a trust during your lifetime.

Addressing Blended Family Complications

Your situation likely differs based on whether you’re in a first marriage, a blended family, or managing business interests. Blended families create genuine complications that generic estate plans don’t address. If you have adult children from a previous relationship and a current spouse, a simple will creates conflict because it typically leaves everything to the surviving spouse, potentially disinheriting your adult children.

A revocable living trust can be structured to provide for your current spouse during their lifetime while preserving assets for your children after your spouse passes. This protects everyone’s interests. Similarly, if you own real estate or a business, you need clarity about succession and decision-making.

Keeping Documents Current With Life Changes

Updating your documents every three to five years keeps pace with changing tax law and family circumstances. California law changed multiple times in recent years regarding beneficiary designations and trust taxation, so documents created a decade ago may not reflect current advantages. Major life events warrant immediate reviews: retirement, home sale or purchase, relocation into or out of California, new diagnoses, or significant changes in your children’s circumstances.

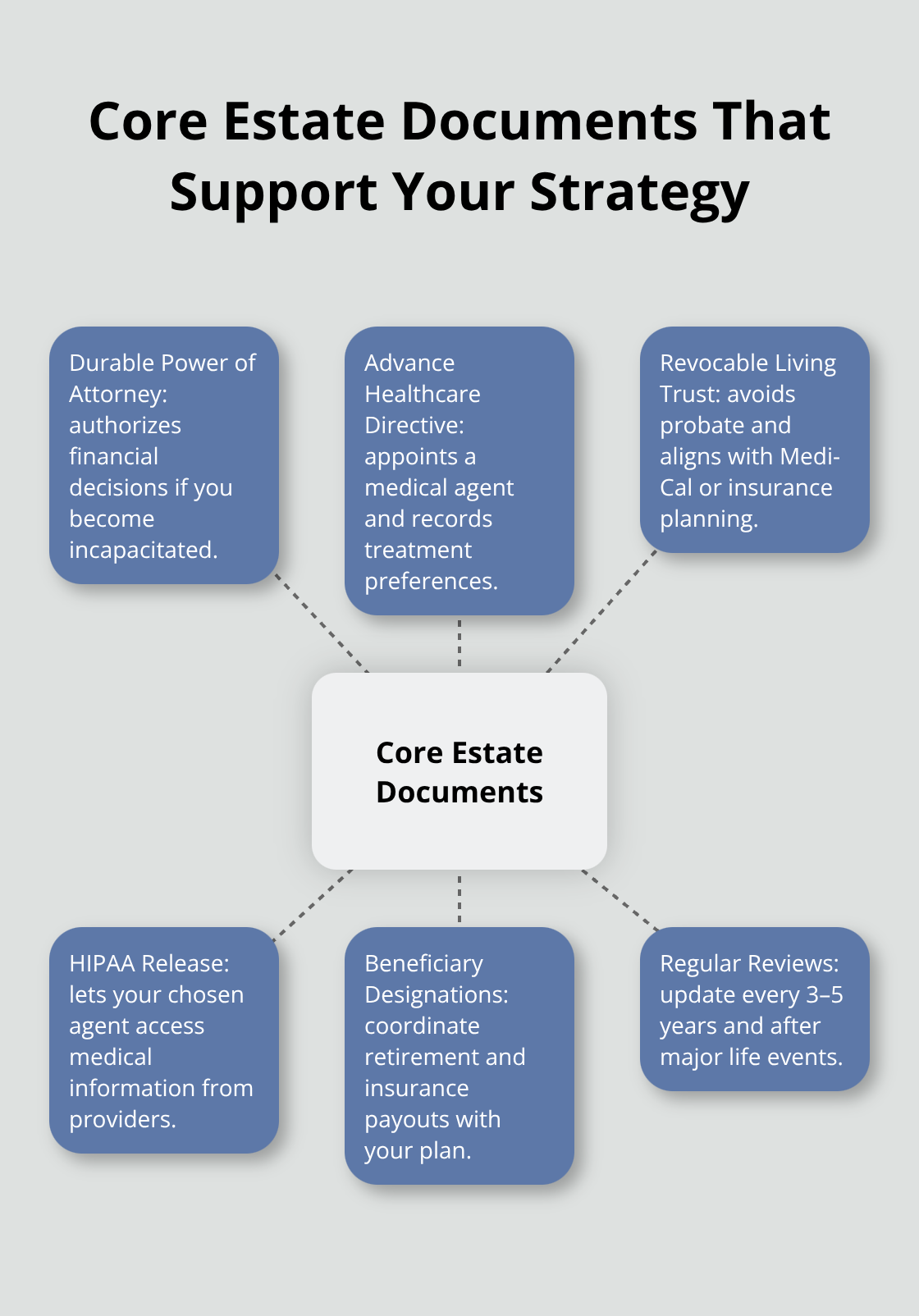

The cost of a review is minimal compared to the expense of fixing problems created by outdated documents. Your core documents should include a durable power of attorney, an advance healthcare directive, a revocable living trust with current beneficiaries, a HIPAA release authorizing your agent to discuss medical information with providers, and updated beneficiary designations across all retirement accounts and insurance policies.

These documents work together to create a coordinated plan that addresses both your immediate needs and your long-term care strategy.

Final Thoughts

Elder law planning options for Southern California families require you to make three interconnected decisions: who handles your healthcare and financial choices, how you protect assets from long-term care costs, and whether your estate documents support your chosen strategy. Without addressing all three areas, your family faces court proceedings, asset depletion, and conflict when clarity matters most. The documents you’ve learned about-powers of attorney, healthcare directives, living trusts, and updated beneficiary designations-form the foundation that prevents guardianship proceedings, probate delays, or Medi-Cal ineligibility.

Starting this planning while you remain healthy and capable gives you control over these decisions rather than forcing your family to make crisis choices under pressure. We at Law Offices of Roshni T. Desai understand that elder law planning feels overwhelming when you’re juggling multiple concerns simultaneously. That’s why we provide personalized guidance tailored to your specific situation, whether you need Medi-Cal coordination, long-term care insurance analysis, or trust restructuring for a blended family.

Contact Law Offices of Roshni T. Desai for a free consultation to discuss your family’s situation. We offer flexible home or office visits across Southern California, and our background in law and real estate streamlines property-related decisions that often complicate elder planning. Your family’s protection starts with one conversation about where you stand today and what matters most for your future.