Probate Attorney Elder Law: Integrating Elder Law Principles

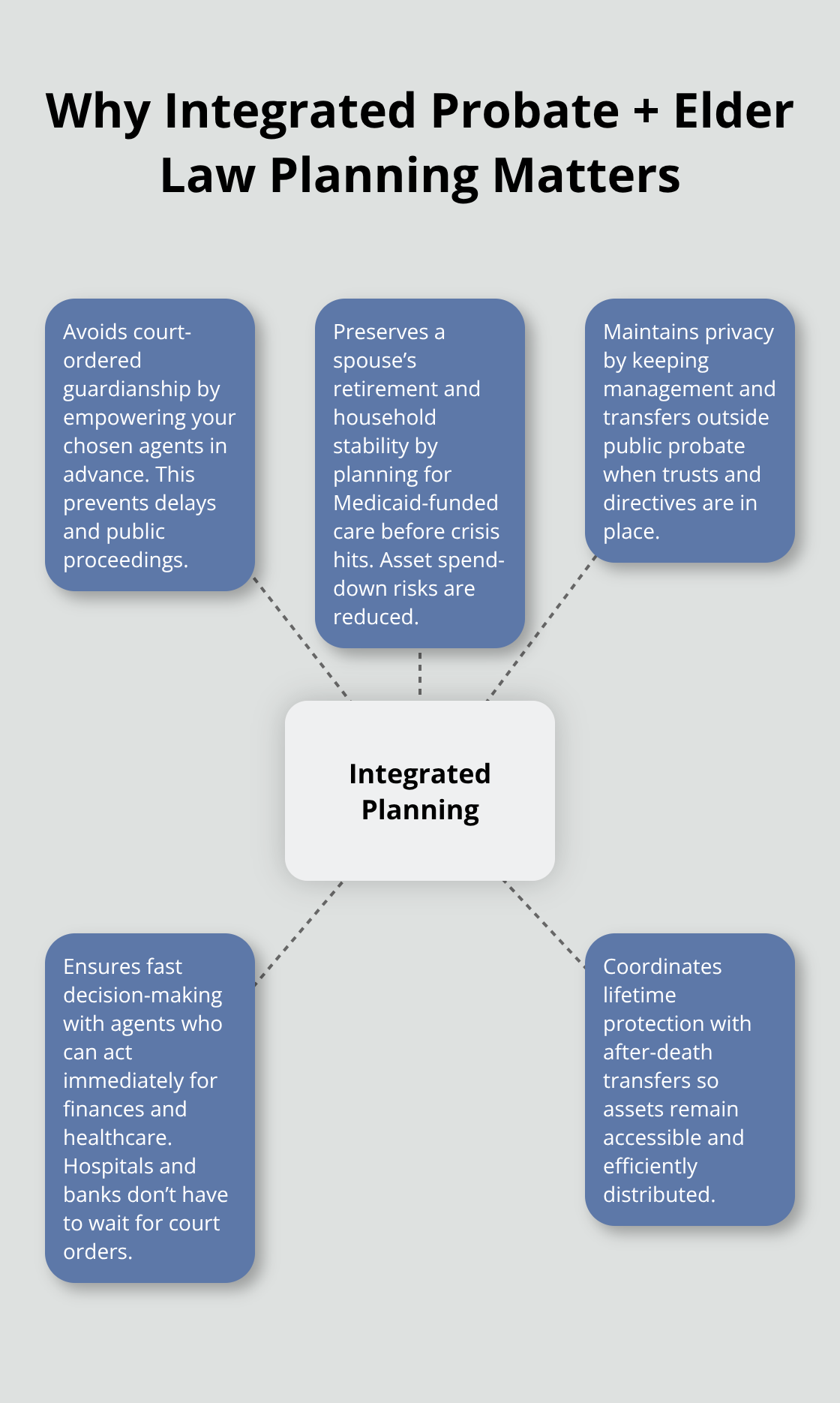

Most people think probate planning and elder law are separate concerns. They’re not. At Law Offices of Roshni T. Desai, we see how connecting these two areas prevents costly mistakes and family conflict.

When you plan for both lifetime protection and what happens after, your assets stay protected and your family avoids unnecessary delays and expenses. This integration matters whether you’re facing long-term care costs, incapacity, or eventual probate.

How Lifetime Planning Prevents Probate Disasters

Assets Deplete Rapidly Without Protective Structures

Assets disappear fast when you lack protective structures in place. The U.S. Department of Health and Human Services reports that over 70% of adults aged 65 and older will need some form of long-term care before death, yet more than half of Americans in that age group have not saved for these costs. A single extended nursing home stay consumes your entire estate within months without elder law tools integrated into your probate strategy. Durable powers of attorney, living trusts, and Medicaid planning prevent this asset depletion before it happens.

Durable Powers of Attorney Stop Costly Guardianship

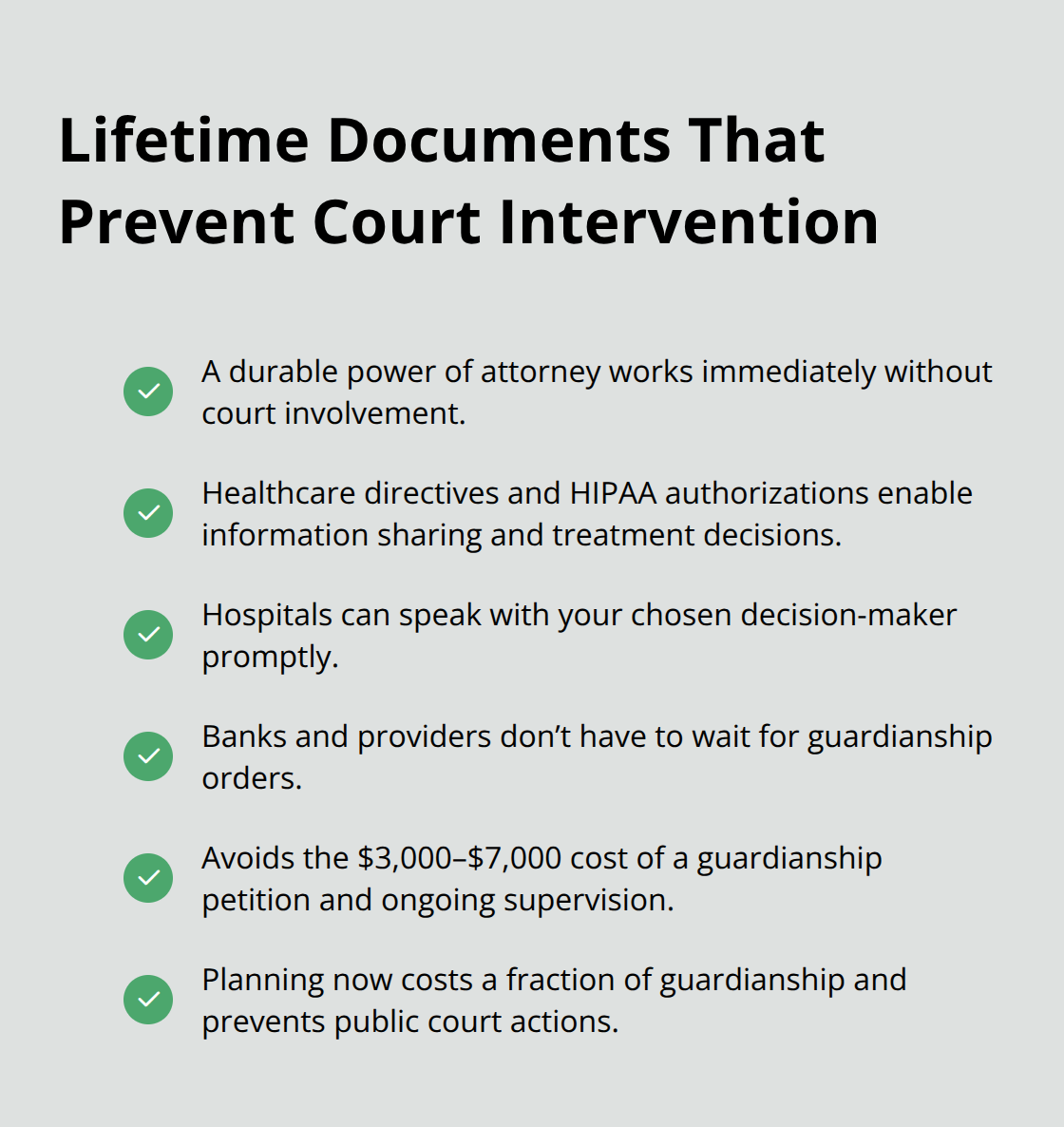

A durable power of attorney lets you appoint someone to handle finances before incapacity strikes, preventing court-ordered guardianship proceedings that cost thousands in legal fees and court costs. Without this document, a judge appoints a guardian to control your finances and healthcare decisions through public court actions that strip you of decision-making authority. Your chosen agent acts immediately when you become unable to manage your affairs, avoiding the delays and expenses of court intervention.

Living Trusts Protect Assets During Your Lifetime

Living trusts bypass probate entirely while protecting assets during your lifetime. If you become incapacitated, your successor trustee continues managing property without court intervention or public disclosure. This seamless transition keeps your family out of probate court and maintains privacy for your financial affairs.

Medicaid Planning Preserves Wealth for Your Family

Medicaid planning through irrevocable trusts and Medicaid Compliant Annuities preserves assets for your family while you fund extended care. An MCA converts excess countable resources into a non-cash income stream, allowing you to qualify for Medicaid benefits faster while protecting remaining wealth. Healthcare directives and HIPAA authorizations ensure medical professionals follow your wishes and share information with your chosen decision-maker, avoiding family disputes and unwanted interventions.

Incapacity Creates Greater Risk Than Death

Most people focus on what happens after they die and ignore what happens if they become unable to manage their affairs. Incapacity without proper documents triggers expensive guardianship court actions where a judge appoints someone to control your finances and healthcare decisions. A comprehensive durable power of attorney and healthcare proxy eliminate this risk entirely. When probate and elder law planning work together, your family avoids crisis decisions and maintains your autonomy.

Comprehensive planning also protects your family’s finances-if you need nursing care without Medicaid planning in place, your spouse’s retirement savings disappear paying for your care, leaving them vulnerable. These interconnected risks make integrated planning essential before incapacity or death occurs, which is why the next section examines the specific elder law tools that strengthen your probate strategy.

Tools That Protect Your Assets Before Probate

Powers of Attorney and Healthcare Directives Stop Court Intervention

Durable powers of attorney and healthcare directives form the foundation of protection during your lifetime. A durable power of attorney names someone you trust to handle finances, real estate, and tax matters the moment you become unable to manage them yourself. This document works immediately without court involvement, avoiding the guardianship process entirely. Healthcare directives and HIPAA authorizations let medical providers share information with your chosen decision-maker and follow your treatment preferences. Without these documents in place, hospitals and doctors cannot discuss your condition with family members, and no one has legal authority to make medical decisions on your behalf until a court appoints a guardian.

The cost difference is striking: a guardianship petition runs $3,000 to $7,000 in legal fees plus ongoing court supervision expenses, while creating a durable power of attorney costs a fraction of that amount and eliminates the need for any court action.

Living Trusts Manage Assets Without Probate or Court Permission

A revocable living trust holds your property during your lifetime and automatically transfers it to beneficiaries after death without probate delays. More importantly, if you become incapacitated, your successor trustee steps in immediately to manage the trust property without asking a court for permission. Your financial affairs remain private since trust administration happens outside the public probate process. This seamless transition protects your family from both delays and public disclosure of your financial details.

Medicaid Planning Preserves Wealth Through Strategic Structures

Medicaid planning through irrevocable trusts and Medicaid Compliant Annuities protects assets while you qualify for benefits to fund long-term care. An MCA converts excess countable resources into monthly income payments, accelerating Medicaid eligibility while preserving wealth for your spouse and children. A Medicaid Compliant Annuity must be irrevocable, non-assignable, and actuarially sound to satisfy Medicaid rules across states. Funeral Expense Trusts fund burial costs separately, removing those assets from Medicaid calculations entirely. These structures work because they address Medicaid’s resource limits, which typically allow institutionalized individuals to retain roughly $2,000 in countable assets while a community spouse can protect between $30,828 and $154,140 depending on your state. Without Medicaid planning integrated into your estate strategy, extended nursing care depletes your entire estate within months, leaving your surviving spouse with nothing.

The specific tools you need depend on your family situation, health status, and financial picture. The next section examines real-world scenarios where these protective structures prevent the exact problems families face when incapacity or long-term care strikes.

When Long-Term Care Strikes, Does Your Plan Actually Protect Your Family?

Long-Term Care Costs Destroy Unprotected Estates

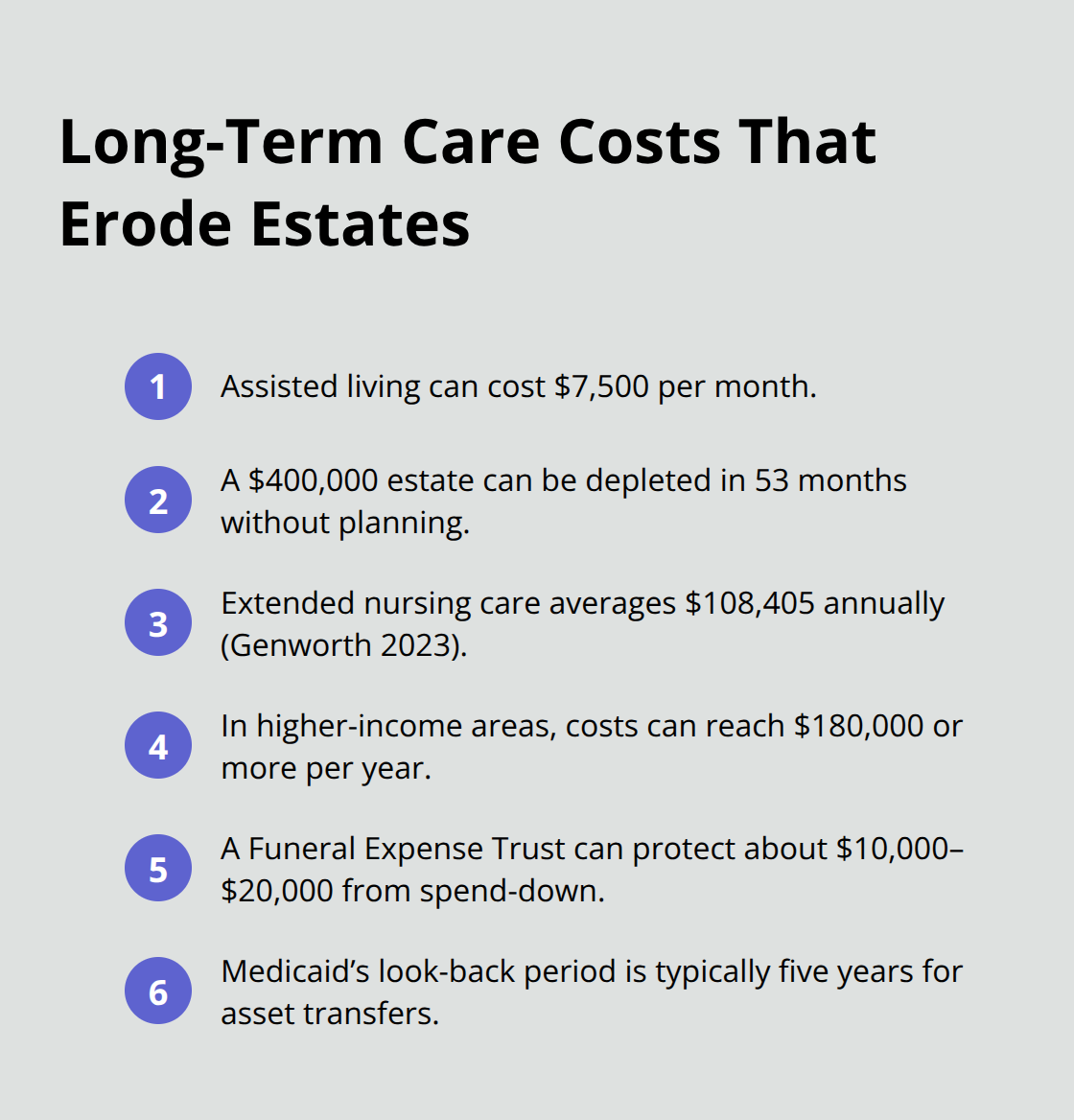

A 78-year-old woman enters assisted living after a stroke. Her monthly costs run $7,500. Without Medicaid planning, her $400,000 estate disappears in 53 months-leaving her spouse with nothing.

This scenario plays out constantly because families treat elder law and probate planning as separate decisions made years apart. The reality is harsher: a single health event forces immediate spending decisions that either preserve or destroy your family’s wealth, depending on whether protective structures exist before the crisis arrives. Extended nursing care averages $108,405 annually according to Genworth’s 2023 Cost of Care Survey, and costs in higher-income areas reach $180,000 or more per year. Without integrated planning, your spouse’s retirement security evaporates while you receive care.

The U.S. Department of Health and Human Services data showing 70% of seniors need long-term care means your family faces this risk whether or not you acknowledge it now. An MCA converts excess resources into income before Medicaid qualification, preserving tens of thousands for your family while you access benefits immediately. A Funeral Expense Trust removes burial costs from Medicaid asset calculations, protecting another $10,000 to $20,000 from spend-down requirements. These tools only work if established before incapacity or crisis spending begins-waiting until your diagnosis arrives means Medicaid’s look-back period (typically five years) captures all recent asset transfers, blocking protection strategies entirely.

Incapacity Without Documents Triggers Expensive Court Intervention

Incapacity without proper documentation creates a second disaster that most people overlook completely. When you cannot communicate your wishes, hospitals refuse to discuss your condition with family, banks freeze accounts until guardianship orders arrive, and your home sits unmanaged while bills accumulate. A 72-year-old suffered a severe fall with no healthcare directive in place; his daughter spent three months and $6,000 in legal fees obtaining guardianship before she could access his bank account to pay his mortgage.

His successor trustee could have transferred property through a living trust instantly, and his healthcare proxy could have authorized his daughter to receive medical information and make treatment decisions within hours. These delays disappear entirely when you execute a durable power of attorney naming your chosen agent, a healthcare directive naming your healthcare proxy, and HIPAA authorizations allowing medical providers to discuss your care with your family. The cost to create these documents runs $800 to $1,500 combined-a fraction of guardianship expenses.

Living Trusts Protect Assets Through Incapacity and Beyond

Revocable living trusts address both incapacity and probate by transferring property management to your successor trustee immediately upon your incapacity, without court intervention or public disclosure. Your financial affairs continue seamlessly while your family avoids the probate court entirely after death. Families who acted proactively through durable powers of attorney and living trusts maintain control over timing and structure, while those who delay face guardianship courts deciding asset disposition for them.

Special Needs Structures Protect Vulnerable Beneficiaries

Vulnerable family members-adult children with disabilities, spouses with substance abuse histories, or beneficiaries prone to poor financial decisions-require supplemental needs trusts or special needs structures that protect their inheritance while maintaining their Medicaid or SSI benefits. A standard will or basic trust leaves these beneficiaries ineligible for means-tested benefits, forcing them to spend down inheritances on basic living costs instead of enhancing their quality of life through carefully structured trusts. These integrated protections only function if established before crisis strikes, which is why comprehensive planning during healthy years determines whether your family maintains control or surrenders it to courts and guardians.

Final Thoughts

Integrated probate attorney elder law planning eliminates the delays, expenses, and family conflict that arise when you treat lifetime protection and estate planning as separate decisions. Guardianship proceedings cost $3,000 to $7,000 in legal fees plus ongoing court supervision, while comprehensive elder law documents cost a fraction of that amount and prevent court involvement entirely. Probate administration adds months of delays and public disclosure of your financial details, whereas a properly funded living trust transfers assets to beneficiaries within weeks while maintaining complete privacy.

Your chosen agent manages finances immediately upon incapacity instead of waiting months for guardianship orders, and your healthcare proxy authorizes medical decisions within hours instead of forcing hospitals to refuse family involvement. Medicaid planning through irrevocable trusts and MCAs preserves tens of thousands in family wealth that would otherwise disappear funding long-term care. Your successor trustee continues managing your property seamlessly instead of leaving your home and bills unattended while probate court processes paperwork.

We at Law Offices of Roshni T. Desai help families build these integrated plans before crisis strikes, combining estate planning, probate administration, and elder law into one coordinated strategy that protects your assets and preserves your family’s security. Contact us at Law Offices of Roshni T. Desai to start planning today.