Your Probate Asset Inventory Guide to a Smooth Estate Process

Most people don’t realize what happens to their assets when they pass away. Without a clear probate asset inventory guide, families face delays, missed assets, and unnecessary conflict.

We at Law Offices of Roshni T. Desai have seen firsthand how a well-organized inventory transforms the entire estate process. This guide walks you through exactly what to document and how to organize it.

What Goes Into Your Probate Asset Inventory

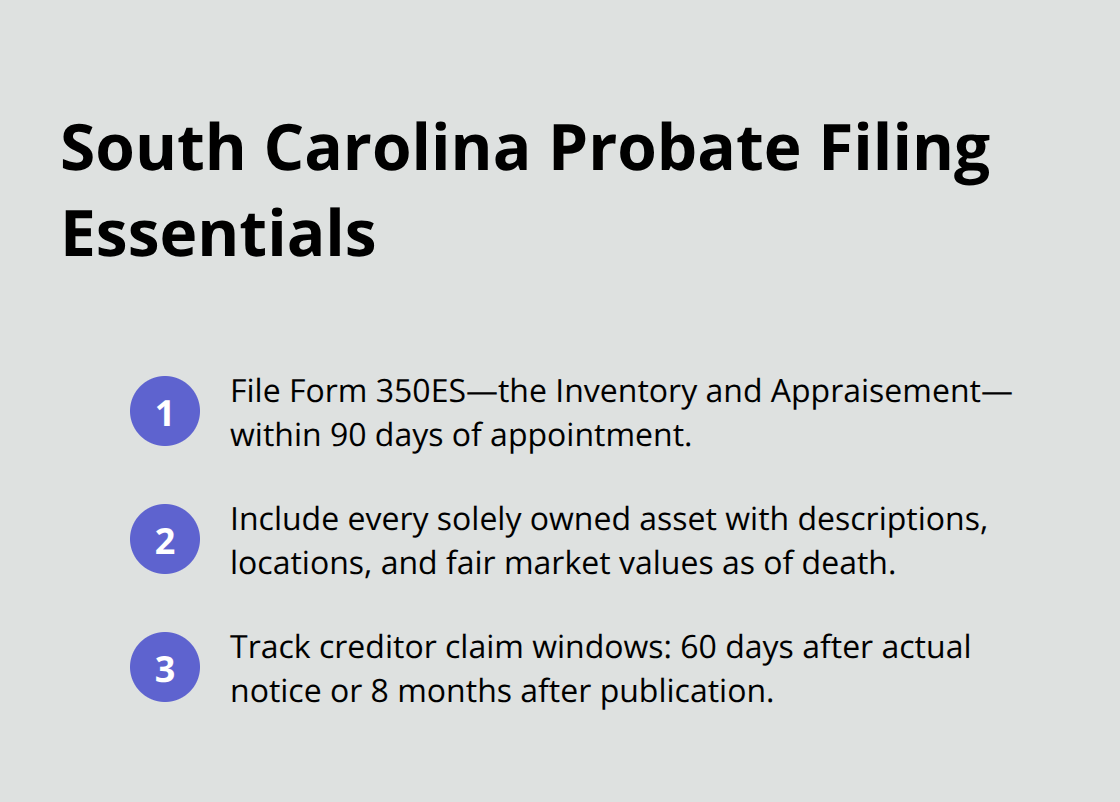

A probate asset inventory is far more than a casual list. In South Carolina, Personal Representatives must file Form 350ES-the Inventory and Appraisement-within 90 days of appointment, per S.C. Code Ann. § 62-3-706. Miss this deadline and you risk court penalties, delays, and creditor complications. The inventory must include every asset the decedent owned solely at death, with descriptions, locations, and fair market values as of the date of death. You cannot guess at values or leave items vague. Creditors have 60 days of actual notice or 8 months of published notice to file claims under S.C. Code Ann. § 62-3-803, so accuracy matters from day one.

Real Estate Demands Precise Documentation

Real estate trips up most families because the documentation requirements are strict. You need the legal description from the deed, the property address, and a current fair market value. If the property has a mortgage, document the remaining balance separately from the property value. For commercial real estate or properties with complex valuations, hire a professional appraiser rather than relying on online estimates. The court expects supporting documentation-deeds, recent appraisals, or statements from banks if the property is financed. Gather these now; you will submit copies to the court and provide them to interested parties upon request. If you discover additional real estate after filing, you must file an Amended Inventory to keep the record accurate.

Financial Accounts Need Exact Numbers

Bank accounts, investment accounts, retirement accounts, and cryptocurrency all belong in the inventory. For each account, note the institution, the account type, and the balance as of the date of death. Do not include accounts with named beneficiaries or payable-on-death designations-those bypass probate entirely. However, list them anyway for a complete accounting to heirs. Stocks and bonds are valued at the price on the date of death; check the investment manager or historical stock prices for that specific date. Bonds include any accrued interest owed at death. Life insurance policies you own on your own life go in the inventory at their cash surrender value, not the death benefit. If you own policies on someone else’s life, include those at cash value as well. Digital assets (cryptocurrency, domain names, social media accounts) also require listing with descriptions and any known values.

Personal Property Requires Honest Assessment

Jewelry, artwork, antiques, and collectibles need professional appraisals if their individual value exceeds a few thousand dollars. Auction houses and art museums provide valuations; the American Society of Appraisers can connect you with qualified professionals. For household furniture, electronics, and clothing, group items by room and assign reasonable estimated totals. Take photographs of high-value items and note serial numbers if available. Keep all supporting documentation-receipts, appraisals, insurance policies, certificates of authenticity. The court can request these at any time, and thorough documentation prevents disputes among heirs about whether items were actually owned or what they were worth.

Organize Information for Court Submission

Real estate requires the street address, a basic description, and an appraised or estimated fair market value. Financial accounts demand the institution name, account type, last digits of the account number, and the exact balance as of death. Vehicles need year, make, model, and value sourced from Kelley Blue Book or Edmunds-not what you think it’s worth. Personal property like jewelry, artwork, and collectibles must be individually listed with professional appraisals for high-value items, while lower-value household goods can be grouped by room with estimated totals. Debts are listed separately on the form. This structured approach helps the court review your filing efficiently and signals to interested parties that you have handled the estate with care.

Why a Complete Asset Inventory Protects Your Estate

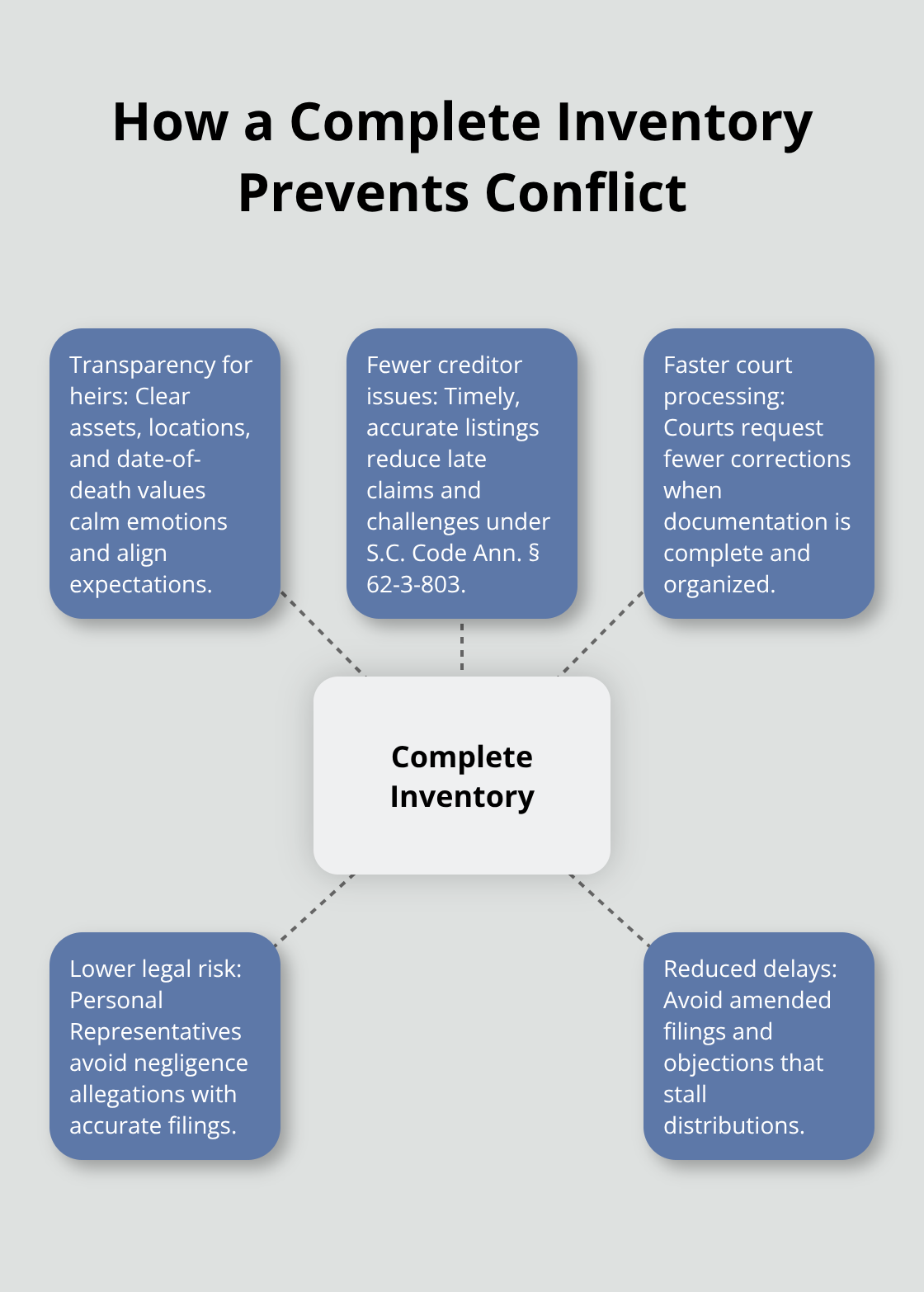

Incomplete asset documentation costs money, creates conflict, and extends probate by months. Families who skip proper inventory procedures face legal disputes, missed deadlines, and unnecessary expenses. The 90-day South Carolina filing deadline under S.C. Code Ann. § 62-3-706 doesn’t bend, and the consequences of incomplete inventories hit hard. When assets go missing from the initial filing, creditors file claims late, heirs argue over what was actually owned, and the Personal Representative faces potential liability for negligence. Missing even one account or failing to properly value a piece of real estate triggers court objections, requires amended filings, and delays distributions by additional months-sometimes years. Families already grieving the loss of a loved one end up spending thousands in legal fees to fix what should have been done correctly the first time.

An Organized Inventory Stops Disputes Before They Start

A detailed, complete inventory prevents arguments about hidden assets or unfair valuations. When heirs see exactly what existed, where it was located, and what it was worth on the date of death, disputes evaporate. Creditors under S.C. Code Ann. § 62-3-803 have 60 days of actual notice to file claims, and a thorough inventory signals that you take transparency seriously-they’re less likely to challenge the estate or file late claims.

Courts move faster when inventories are complete and well-documented; incomplete filings trigger requests for additional information, corrections, and resubmissions that add weeks to the timeline.

Start Early to Meet Your Deadline

Real estate appraisals, bank statements, and investment valuations all take time to gather. Starting immediately after appointment rather than rushing at day 85 means you meet the deadline without panic and without errors. The Personal Representative who files a comprehensive, accurate inventory on time demonstrates competence and care-judges take notice, interested parties trust the process, and the estate closes on schedule rather than languishing in probate limbo.

What Happens When You Get It Right

Proper documentation transforms how courts, creditors, and heirs view the estate administration. A well-organized inventory signals that you understand your responsibilities and take them seriously. The next step involves understanding exactly how to document each asset type and what supporting records the court expects from you.

Building Your Asset Inventory from the Ground Up

The moment you receive your appointment as Personal Representative, start collecting documents instead of waiting for the 90-day deadline to approach. Open a dedicated folder-physical or digital-and collect bank statements, property deeds, investment account statements, vehicle titles, insurance policies, and any documentation showing what the decedent owned. Contact each financial institution directly and request statements as of the date of death; online portals often show current balances, not historical values. For real estate, pull the deed from the county recorder’s office and request a preliminary appraisal from a real estate agent at no cost, or hire a licensed appraiser for properties exceeding $500,000 in value.

Create a Systematic Tracking System

Set up a spreadsheet with columns for asset description, location, institution or holder, account or reference number, date-of-death value, and supporting document file name. This structure forces systematic work and prevents gaps. Photograph high-value items like jewelry, artwork, and collectibles before appraisals arrive; these photos serve as proof of existence if disputes emerge later. For vehicles, pull the title and run a free valuation through Kelley Blue Book or Edmunds using the exact year, make, model, and mileage as of death. Digital assets demand special attention-search the decedent’s email for account confirmations, password managers, and transaction records. Cryptocurrency holdings hide in digital wallets; if the decedent used exchanges like Coinbase or Kraken, contact them with the death certificate to obtain account details and valuations as of the specific date.

Organize Assets by Category

Arrange assets by category rather than by value or timeline, because Form 350ES in South Carolina requires this structure. Real estate occupies one section with street addresses, legal descriptions from deeds, and fair market values. Financial accounts follow with institution names, account types, and exact balances. Personal property-jewelry, art, vehicles, household goods-occupies its own section with individual listings for items exceeding $5,000 and grouped estimates for lower-value categories. Debts and liabilities sit separately, never mixed with assets.

Protect Documents and Share Access

Store the original documents in a secure location-a safe deposit box at your bank or a home safe-and maintain digital copies on an encrypted cloud service or external hard drive kept in a different location. This redundancy protects against fire, theft, or loss. Share access credentials with co-Personal Representatives or successor representatives so they can step in if needed; include passwords, safe deposit box keys, and login information in a sealed envelope held by a trusted family member or attorney. South Carolina law requires Personal Representatives to provide a copy of the inventory to interested parties upon request under probate procedures, so clarity now prevents confusion later.

Meet the 90-Day Timeline

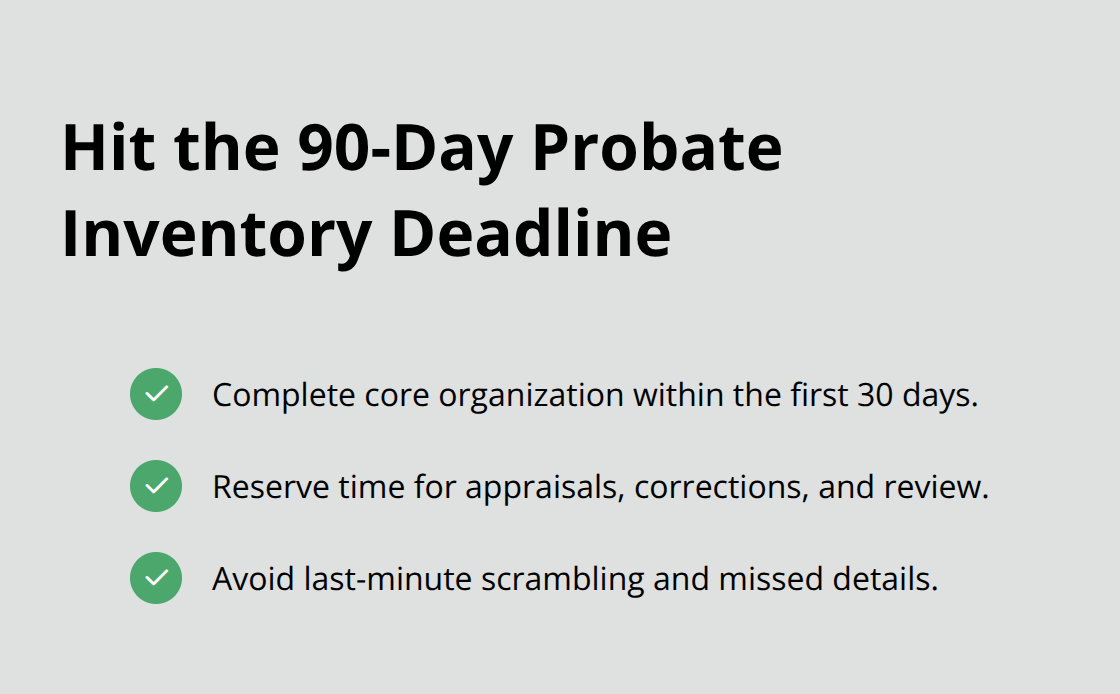

Complete this organizational work within the first 30 days of appointment-well before the 90-day filing deadline under S.C. Code Ann. § 62-3-706-to give yourself time for appraisals, corrections, and review without rushing. This early start separates Personal Representatives who file accurate inventories on time from those who scramble at the last moment and miss critical details.

Final Thoughts

A thorough probate asset inventory guide protects your family from months of delays, unnecessary legal fees, and preventable conflict. The work you complete now-documenting every asset, gathering supporting records, and organizing information systematically-determines whether your estate closes smoothly or gets tangled in disputes and court objections. South Carolina’s 90-day filing deadline under S.C. Code Ann. § 62-3-706 is real, and the consequences of incomplete or inaccurate inventories hit hard.

We at Law Offices of Roshni T. Desai understand the weight of this responsibility and have guided Personal Representatives through every step of probate administration for over 25 years. Ms. Desai’s dual licensure as an attorney and real estate professional means we handle estate-related property sales and transactions directly, reducing costs and the communication confusion that typically plagues probate. We offer free consultations with flexible home or office visits across Southern California, so you can discuss your situation without pressure.

Start your inventory planning today rather than waiting until the deadline looms. If you need guidance on valuation methods, deadline compliance, or how to structure your filing, contact Law Offices of Roshni T. Desai for a free consultation. The Personal Representative who acts early and seeks professional guidance closes the estate on time, protects family relationships, and honors the decedent’s wishes with competence and care.