Trust Administration for Heirs: What to Expect

When a loved one passes away, managing their trust can feel overwhelming. The process involves specific timelines, trustee responsibilities, and your rights as an heir-all of which we at Law Offices of Roshni T. Desai see families navigate regularly.

This guide walks you through trust administration for heirs, covering what to expect, how to protect your interests, and when to seek legal guidance.

What Happens When a Trust Goes Into Administration

The Timeline: From Death to Distribution

Trust administration begins the moment the grantor passes away, and the successor trustee takes control. The process typically unfolds over 4 to 18 months, depending on asset complexity and whether disputes arise. Simple estates with liquid assets and no real property wrap up in 4 to 6 months, while cases involving real estate, business interests, or multiple beneficiaries often stretch to 9 to 18 months.

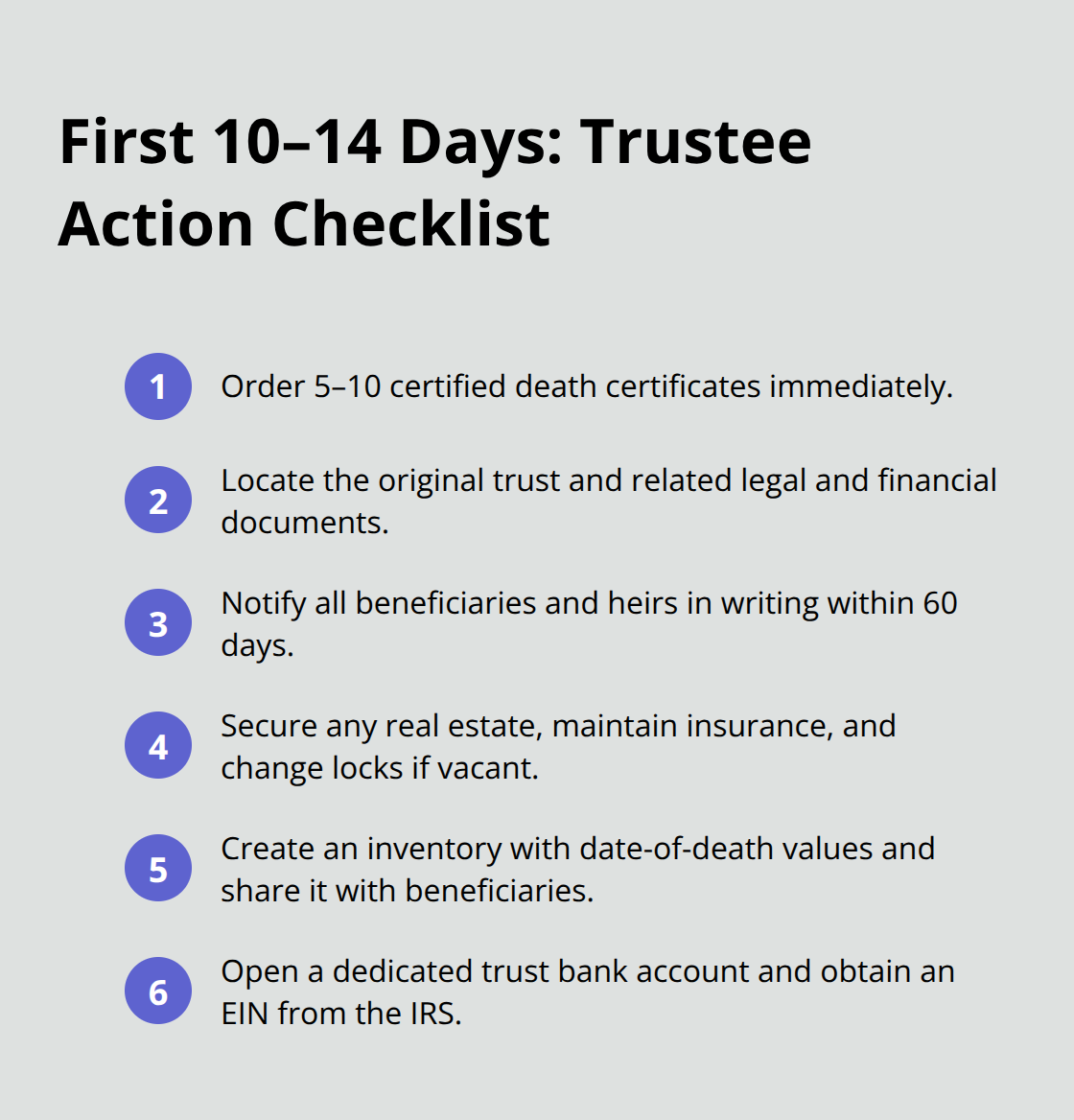

Immediate Actions: The First Days and Weeks

The trustee’s first move is obtaining 5 to 10 certified death certificates-a critical step because banks, insurance companies, and government agencies all demand proof of death before releasing funds or transferring assets. Waiting on death certificates costs time, so the trustee should order them immediately from the county vital records office to prevent bottlenecks later.

Next, the trustee locates the original trust document and related papers, including the Last Will and Testament, military discharge records, and financial statements. Within 60 days of the grantor’s death, California law requires the trustee to notify all beneficiaries and heirs in writing, disclosing the trust’s key terms and their inheritance rights. This 60-day window is non-negotiable-failing to meet it gives beneficiaries grounds to petition the court for enforcement, which creates legal costs and delays nobody wants.

Securing Assets and Managing Finances

The trustee then secures all trust assets to prevent loss or theft. If the trust owns real estate, the trustee changes the locks on uninhabited properties and maintains insurance coverage without lapse. The trustee creates a complete inventory of everything the trust owns as of the date of death, assigns values to each asset, and sends this inventory to beneficiaries.

Simultaneously, the trustee opens a dedicated trust bank account and obtains a federal Tax ID (EIN) from the IRS to keep trust finances separate from personal accounts-mixing them together exposes the trustee to personal liability and complicates tax filings. The trustee must also handle ongoing liabilities like mortgage payments, property taxes, and utility bills to prevent foreclosure or service disconnections. Canceling or updating subscriptions and credit cards stops unnecessary charges.

Creditor Notices and Professional Guidance

Within 90 days, the trustee publishes a Notice to Creditors in a local newspaper to start the claims period, which typically runs 120 days. This notice gives creditors a window to file claims against the estate; missing this deadline can extend administration indefinitely if unknown debts surface later.

Throughout these early months, the trustee works with professionals-a probate attorney, CPA, and financial adviser-to navigate tax filings, asset transfers, and distribution timing. Mistakes in these initial steps create cascading problems: missed deadlines trigger court involvement, improper asset management exposes the trustee to breach-of-fiduciary-duty claims, and poor communication fuels family conflict. Trustees who begin this process within days of the grantor’s death, not weeks, prevent most complications from taking root.

Understanding what the trustee must accomplish sets the stage for recognizing your rights as an heir and what you can expect during the months ahead.

Rights and Responsibilities of Heirs During Trust Administration

What You Inherit and When

As an heir, you hold concrete rights during trust administration, and understanding them prevents the trustee from sidelining you or moving forward without accountability. California Probate Code sections 16000-16015 define fiduciary duties that bind the trustee, including loyalty, impartiality, and a duty to account for all actions. The trust document itself determines what you inherit and when-some trusts distribute assets immediately after debts and taxes are paid, while others hold distributions in stages tied to milestones like reaching a certain age or completing education. A typical timeline places final distributions between 6 and 12 months after death for straightforward estates, though cases involving real estate or business interests commonly extend to 18 months.

Your Right to Information and Transparency

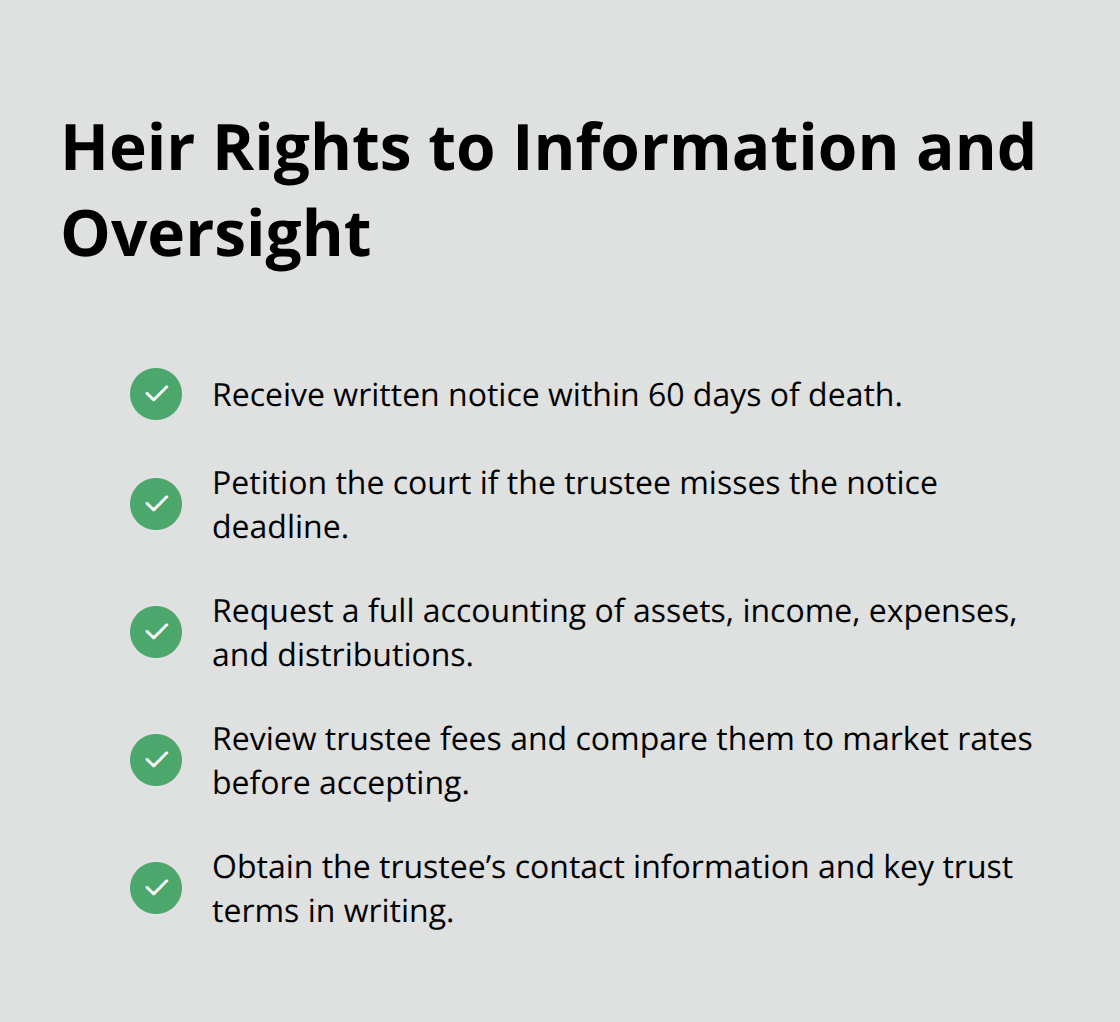

Within 60 days of the grantor’s death, the trustee must provide you with a written notice disclosing the trust’s key terms, your inheritance rights, and the trustee’s contact information. If the trustee misses this deadline, you can petition the court to compel disclosure, which forces the trustee to pay your attorney fees as a penalty.

You have the right to request an accounting of all trust assets, income, expenses, and distributions at any time; the trustee cannot withhold this information. You also have the right to know exactly how much the trustee charges for administration fees and whether those fees align with market rates-administrative costs typically range from 1 to 4 percent of the estate value, depending on complexity, so fees exceeding this band warrant scrutiny.

The trustee’s communication obligations extend far beyond the initial 60-day notice. You deserve regular updates on major actions, especially asset sales, tax filings, and creditor claim resolutions. A trustee who resists providing copies of trust documents, tax returns, or bank statements is hiding something and violating fiduciary law. If the trustee goes silent for months, that silence itself signals a breach.

Red Flags: When Distributions Stall or Fees Spiral

Distributions should never happen before debts, taxes, and administrative costs are settled, so if the trustee proposes early distributions while creditor claims remain unresolved, that’s a red flag signaling either incompetence or intentional misconduct. Disputes with the trustee typically emerge over three issues: unexplained delays in distribution, suspicious fees or expenses, or evidence that the trustee favors one beneficiary over another. If communication fails, send a written request for specific information and set a reasonable deadline-ten business days is standard. Keep copies of all correspondence.

Addressing Trustee Misconduct

If the trustee still refuses to provide information, you have grounds to petition the court to compel an accounting or even remove the trustee for breach of fiduciary duty. Trustee misconduct includes co-mingling trust funds with personal accounts, selling trust assets below market value without competitive bidding, making unauthorized loans to beneficiaries, or failing to file required tax returns. These violations expose the trustee to personal liability, meaning you can recover damages directly from the trustee’s personal assets. If you suspect misconduct, consult a probate attorney immediately-waiting months before taking action weakens your position because the statute of limitations for contesting a trustee’s conduct runs short.

Never accept a final accounting without reviewing it thoroughly or consulting a professional, because once you sign off, challenging the trustee’s actions becomes exponentially harder. When disputes arise or the trustee’s conduct raises questions, the next section covers how to identify whether legal intervention is necessary and what steps protect your inheritance.

Common Issues Heirs Face During Trust Administration

Delays in Asset Distribution

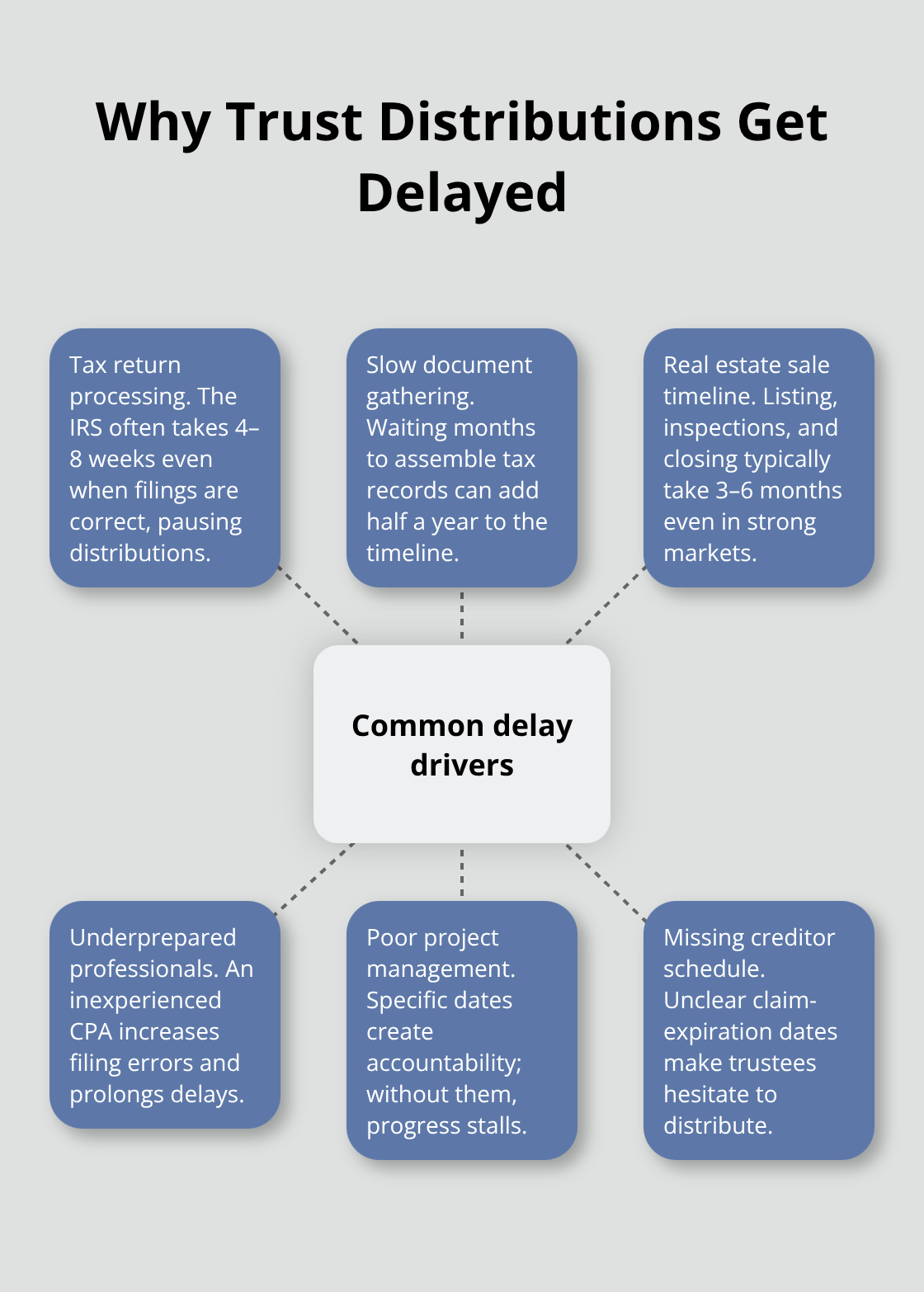

Delays in asset distribution frustrate heirs more than any other aspect of trust administration, and most delays stem from preventable mistakes rather than legitimate complications. The trustee’s failure to file tax returns on time creates cascading delays-federal Form 1041 for trust income and the decedent’s final personal return must both be filed before distributions can proceed, and the IRS takes 4 to 8 weeks to process returns even when filed correctly. If the trustee waits months to gather tax documents or hires an unprepared CPA, that delay alone stretches the timeline by half a year. Real estate sales compound the problem: properties require appraisals, listings, marketing, inspections, and closings, which typically take 3 to 6 months even in a strong market. Heirs often assume the trustee intentionally stalls when the real culprit is poor project management. Request a detailed timeline from the trustee showing when tax returns will be filed, when real estate will list, and when creditor claims expire-specific dates force accountability far better than vague promises.

Trustee Misconduct and Fiduciary Breaches

Trustee misconduct and breach of fiduciary duty expose heirs to direct financial loss, and the most common breach involves mixing trust funds with personal accounts. When a trustee deposits trust money into a personal checking account, the trustee loses the legal protection called trustee immunity and becomes personally liable for any shortfall or loss. A trustee who invests trust assets in speculative ventures without beneficiary knowledge or consent violates the duty of impartiality-conservative, diversified investments are the legal standard. Administrative fees spiraling beyond 2 to 3 percent of estate value signal either incompetence or self-dealing; compare the trustee’s proposed fees against market rates from local probate attorneys and CPAs before accepting them. If the trustee sells real estate owned by the trust without competitive bidding or accepts an offer 10 percent below appraised value, that constitutes a breach.

Tax Implications and Asset Management

Tax implications demand attention because improper asset management or delayed distributions can trigger unnecessary capital gains taxes. When real estate transfers, the tax basis resets to the property’s fair market value as of the grantor’s death, which means heirs avoid capital gains taxes on appreciation during the grantor’s lifetime. A trustee who delays distributions past the point when taxes are due forfeits this tax advantage and wastes estate assets. Improper handling of trust finances (such as failing to obtain a separate EIN or co-mingling funds) compounds tax problems and creates personal liability for the trustee that heirs can pursue.

Taking Action Against Misconduct

If you suspect misconduct, hire a probate attorney immediately to review the trustee’s actions; waiting six months weakens your legal position because statutes of limitation for challenging trustee conduct run short in most states. A probate attorney can examine whether the trustee filed required tax returns on time, whether fees align with market standards, and whether asset sales occurred at fair market value. Courts can remove trustees for cause and order them to repay damages directly to beneficiaries, so early intervention protects your inheritance and prevents further losses.

Final Thoughts

Trust administration for heirs demands that you act fast when the trustee misses deadlines, refuses to share information, or proposes distributions before taxes are settled. These red flags signal misconduct, and waiting months to respond weakens your legal position because statutes of limitation narrow your options. Consulting a probate attorney within weeks of discovering problems costs far less than fighting a trustee in court later when evidence has vanished and your ability to challenge conduct has expired.

We at Law Offices of Roshni T. Desai recognize that trust administration for heirs creates stress for families already grieving a loss. If you suspect trustee misconduct, need help reviewing an accounting, or want to recover damages from a trustee’s breach of fiduciary duty, contact us for a free consultation and let us protect your inheritance. Do not sign off on any final accounting without understanding every line item or consulting a professional, because once you approve it, challenging the trustee’s actions becomes nearly impossible.