Trust Administration in Orange County, California: From Setup to Settlement

A trust can provide peace of mind for your family’s future, but administering one requires careful attention to detail and strict adherence to California law. Trust administration in Orange County involves multiple steps, from inventorying assets to distributing funds to beneficiaries.

At Law Offices of Roshni T. Desai, we’ve guided countless trustees through this process. This guide walks you through each stage so you can fulfill your duties with confidence.

Understanding Trust Administration Basics

What Trust Administration Actually Requires

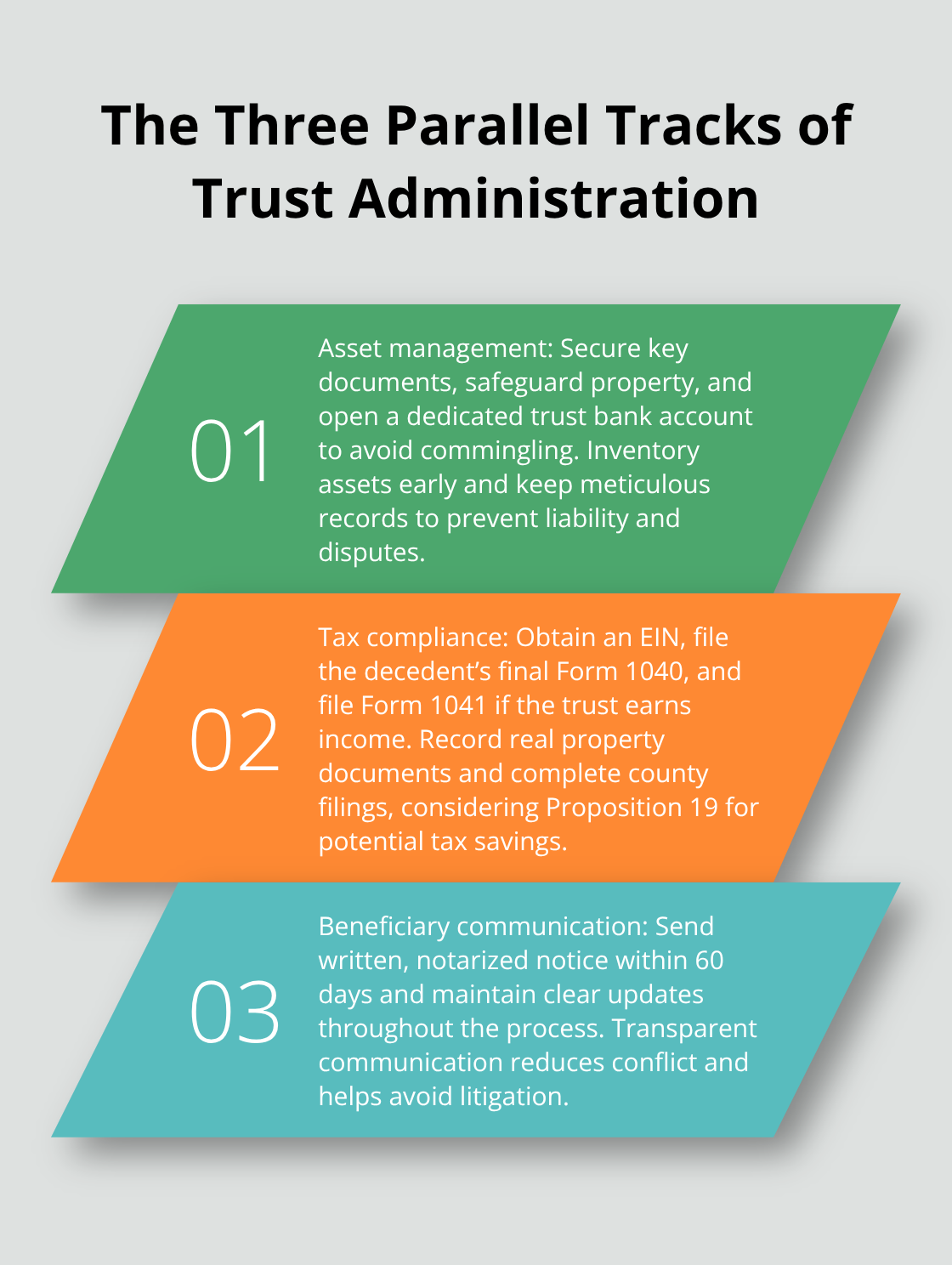

Trust administration is not a single event-it’s a structured sequence of parallel responsibilities that begin the moment a trustee accepts the role. California Probate Code sections 16000-16015 establish the legal framework, but the practical work demands immediate action across three distinct tracks: asset management, tax compliance, and beneficiary communication. On day one, you must locate the original trust document, order at least ten certified death certificates, secure all trust-related documents, and gather contact information for every beneficiary and creditor. Within 60 days of the trustor’s passing, California law requires written, notarized notice to all beneficiaries-this is non-negotiable.

Simultaneously, you must open a dedicated trust bank account separate from personal funds to prevent commingling, which exposes you to personal liability and creates audit nightmares.

The tax track runs parallel to asset management. You obtain a federal Employer Identification Number (EIN) from the IRS, file the decedent’s final Form 1040, and if the trust earns income during administration, file Form 1041. Real property requires recording an Affidavit of Death of Trustee and filing a Change in Ownership Report with the County Assessor. In Orange County, where trust-held real estate often dominates estates, you evaluate whether to sell, retain, or transfer title to beneficiaries-and if you transfer to a child, California Proposition 19 may provide property tax reassessment exclusions that save thousands annually.

Fiduciary Duties and Legal Obligations

The fiduciary duties under California law demand loyalty to beneficiaries, impartiality when multiple beneficiaries exist, and meticulous record-keeping. Asset distributions typically take six to twelve months; rushing before debts and taxes are settled increases your personal liability exposure significantly. Courts have consistently found that thorough documentation and transparent communication eliminate most disputes before litigation becomes necessary.

Managing Complex Assets and Timelines

Straightforward trusts may close in three to six months, but complexity extends timelines substantially. If the trust owns rental properties, you manage tenant communications, maintenance, and ensure rental income flows properly into the trust account. If it holds a closely held business or intellectual property, you need specialized knowledge to avoid liability-this alone can add months. Asset appraisals for real estate, business interests, or valuable personal property take time and money, typically ranging from $500 to several thousand dollars depending on the asset.

Before any distribution reaches a beneficiary, you must identify and pay all valid debts and taxes; creditors in California have a limited window to file claims, but you cannot distribute until that window closes and obligations are settled. The accounting phase-providing beneficiaries with detailed statements showing every transaction, investment, and expense-cannot be rushed if you want to avoid disputes.

Getting Started With a Structured Approach

A detailed checklist prevents oversights and legal compliance failures that transform straightforward administrations into contested nightmares. Secure documents, coordinate with the decedent’s financial advisor and accountant, determine whether to hire professional assistance, and establish clear communication expectations with beneficiaries from the start. This structured foundation sets the stage for identifying and inventorying the specific assets that make up the trust estate.

Managing Trust Assets and Distributions

Identifying and Inventorying Trust Property

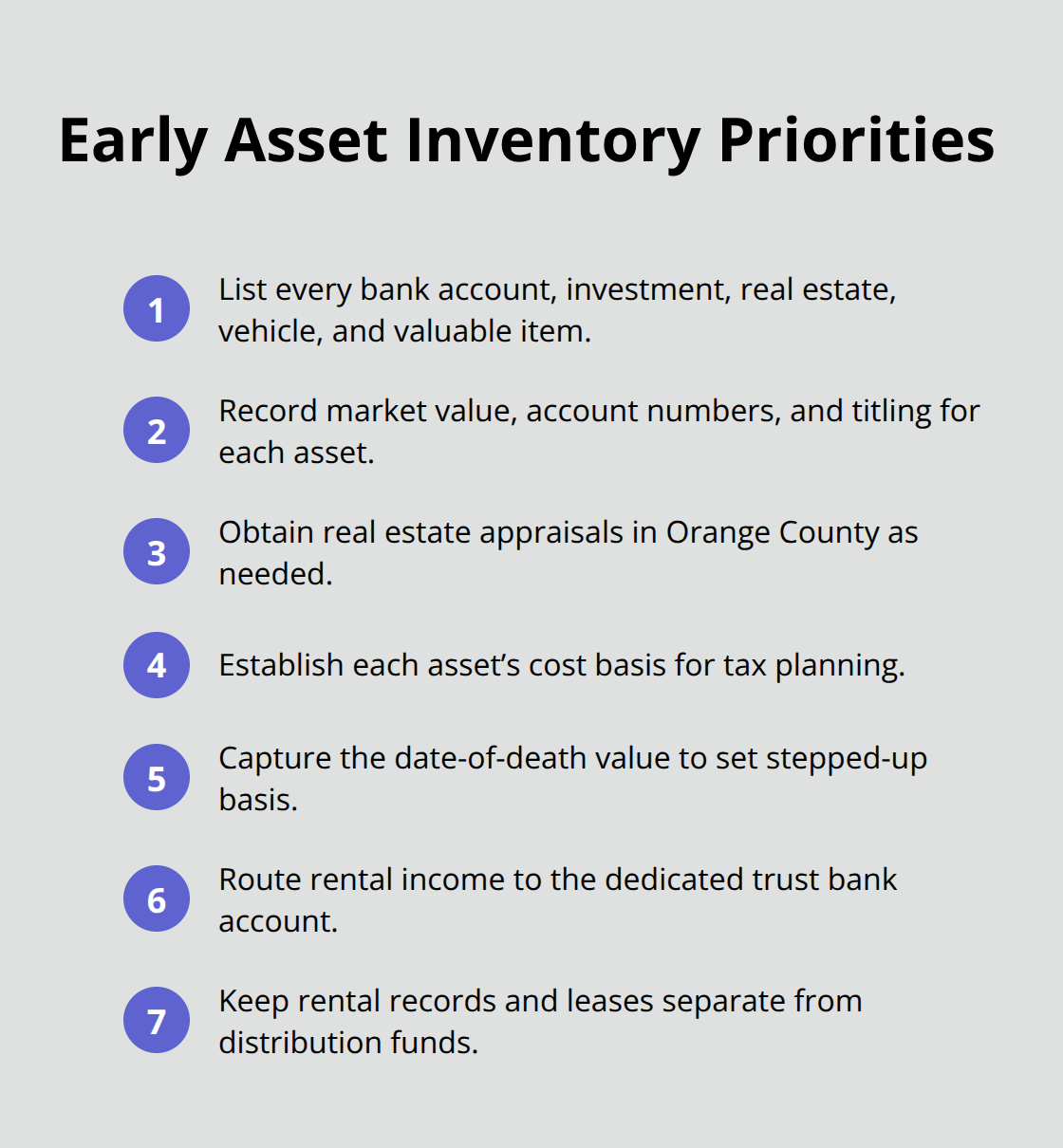

The moment you accept the trustee role, asset identification becomes your foundation for everything that follows. Create a comprehensive inventory listing every bank account, investment, real estate property, vehicle, and valuable personal item within the first two weeks. For each asset, document the current market value, account numbers, and titling information. Real estate appraisals in Orange County typically cost $500 to $2,500 per property depending on complexity, but the trust pays this expense and prevents disputes over valuation later. Once you have the inventory, you must establish cost basis for each asset-the original purchase price adjusted for improvements-because this determines capital gains taxes when beneficiaries eventually sell inherited property. The date-of-death value matters equally; this is the market price on the day the trustor died, and it becomes the basis for inherited assets under federal tax law, potentially eliminating years of accumulated gains.

If the trust holds rental properties, immediately collect all tenant information, lease agreements, and maintenance records; rental income must flow into the dedicated trust bank account and remain tracked separately from distribution funds.

Handling Debt and Tax Obligations

Debt and tax obligations demand attention before a single dollar reaches beneficiaries, and this is where many trustees stumble. File the decedent’s final Form 1040 within the standard deadline and obtain a federal EIN from the IRS to file Form 1041 if the trust earns income during administration. Contact all known creditors and file a Notice of Death with the California Department of Health Care Services if applicable. Creditors in California have a limited window to file claims, typically four months from trust notification, but you cannot distribute assets until this period closes and all valid debts are paid. Calculate final medical bills, funeral expenses, property taxes, and any outstanding loans against trust property. For real property transfers, file an Affidavit of Death of Trustee and a Change in Ownership Report with the County Assessor; if you transfer real estate to a child, California Proposition 19 may provide property tax reassessment exclusions that preserve the original assessed value and save thousands annually.

Preparing Accountings and Managing Distribution Timelines

Once debts and taxes are settled, prepare a detailed accounting for beneficiaries showing every transaction, expense, and investment decision. Provide this accounting at least 60 days before distribution and allow beneficiaries to contest it during a 120-day period. Distributions typically take six to twelve months in Orange County for straightforward trusts, but complex estates with multiple properties or business interests require longer. Never rush distributions to meet arbitrary deadlines; personal liability follows trustees who distribute before obligations are fully resolved. The disputes that arise from hasty distributions often stem from beneficiaries who feel excluded or uninformed about the process-a problem that transparent communication and detailed accountings prevent entirely. As you move toward finalizing distributions, you must also address the specific challenges that Orange County trustees face most frequently, particularly when real estate dominates the estate or beneficiaries hold conflicting interests.

Common Trust Administration Challenges in Orange County

Real Estate Disputes and Conflicting Beneficiary Interests

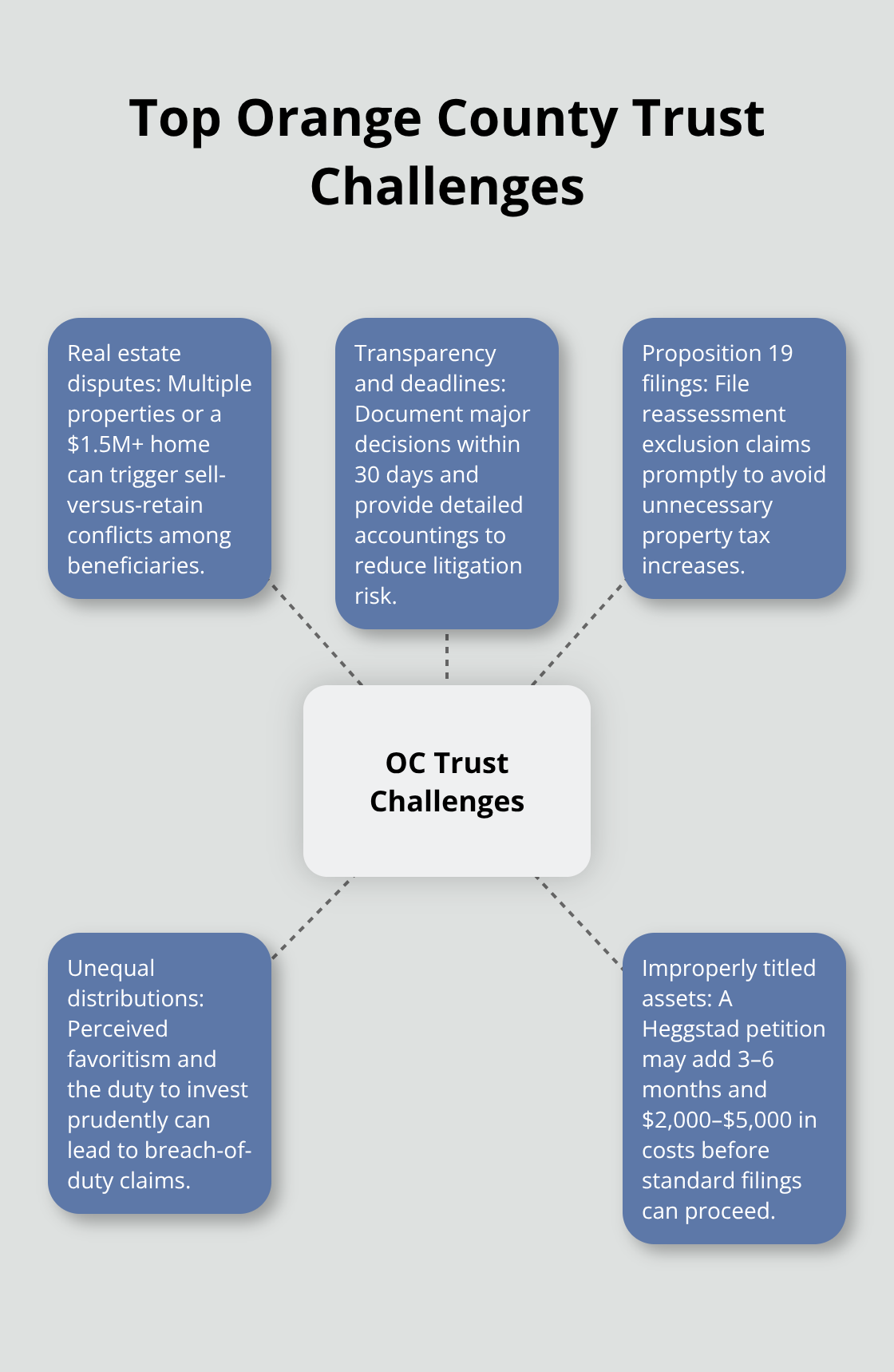

Orange County trustees face distinct challenges that rarely surface in other California counties, primarily because real estate dominates trust assets here. When a trust holds multiple properties or a family home worth $1.5 million or more, disagreements emerge quickly over whether to sell, retain, or transfer title to beneficiaries. One beneficiary may want the family home preserved while another demands immediate liquidation to receive their inheritance within months rather than years.

California Probate Code sections 16000-16015 require you to act as a reasonably prudent investor and manage trust property in furtherance of the trust’s purposes, but this obligation becomes murky when beneficiaries have conflicting visions. The code explicitly prohibits self-dealing, meaning you cannot hold an interest adverse to a beneficiary or use trust property for personal profit-yet beneficiaries sometimes suspect exactly this when a trustee delays selling valuable real estate or makes investment decisions that favor one heir over another.

Transparency as Your Primary Defense

Document every decision in writing and explain your reasoning to beneficiaries within 30 days of major moves. Provide detailed accountings showing how property values changed and why you chose your course of action. If you transfer real estate to a child, file a Claim for Reassessment Exclusion under California Proposition 19 immediately-missing this deadline costs families thousands in unnecessary property tax increases.

Courts have consistently found that trustees who communicate frequently and provide detailed written explanations eliminate most disputes before litigation becomes necessary. Those who operate silently or rush decisions face contested accountings and personal liability claims.

Managing Unequal Distributions and Investment Obligations

When a trust specifies unequal distributions-perhaps one child receives $500,000 and another receives $200,000-the disadvantaged beneficiary may claim the trustee favored their sibling, mismanaged assets, or failed to maximize returns. California law requires impartial dealing when multiple beneficiaries exist with differing interests, which means you cannot passively invest trust assets or ignore market opportunities while inflation erodes value.

Actively manage investments and adjust strategies as market conditions shift. Document these decisions monthly. If the trust holds rental properties, ensure rental income flows properly, maintain the properties adequately, and handle tenant communications professionally-neglecting a rental property that loses value due to poor maintenance opens you to breach-of-fiduciary-duty claims.

Navigating Improperly Titled Assets and Probate Complications

The third challenge involves assets that were not properly titled in the trust during the settlor’s lifetime. If real property sits outside the trust, you may need to file a Heggstad petition with the probate court to transfer it into the trust for distribution-this adds three to six months to your timeline and costs $2,000 to $5,000 in legal fees.

This complication transforms what should be a straightforward administration into a multi-track process requiring court involvement. The petition itself demands careful documentation of the settlor’s intent and the circumstances surrounding the property’s original acquisition. Once the court approves the transfer, you still must complete all standard real property filings (Affidavit of Death of Trustee, Change in Ownership Report) before distributions can proceed to beneficiaries.

Final Thoughts

Trust administration in Orange County demands attention to detail, strict adherence to California law, and transparent communication with beneficiaries from start to finish. The essential steps remain consistent across every administration: secure documents immediately, open a dedicated trust bank account, notify beneficiaries within 60 days, inventory all assets, address debts and taxes before distributions, and provide detailed accountings that explain every decision. Rushing any of these steps exposes you to personal liability and creates disputes that could have been prevented with proper planning and documentation.

The complexity of California trust administration increases significantly when real estate dominates the estate or when beneficiaries hold conflicting interests. Managing rental properties, handling property tax implications under Proposition 19, and navigating improperly titled assets all require knowledge that extends beyond basic trust accounting. Many trustees attempt to handle these responsibilities alone and discover too late that a single missed deadline or miscalculation costs thousands in unnecessary taxes or legal fees.

Professional guidance becomes invaluable when your trust holds multiple properties, includes a family business, or involves beneficiaries with competing interests. We at Law Offices of Roshni T. Desai provide personalized estate planning and probate services across Southern California, including trust and probate administration, and we offer free consultations with flexible home or office visits so you can discuss your specific situation without financial pressure. Contact Law Offices of Roshni T. Desai to discuss your trust administration needs and receive guidance tailored to your Orange County estate.