Streamlining Trust Administration Filing for Real Estate Transfers in Santa Ana, California

Trust administration filing for real estate transfers in Santa Ana involves navigating multiple agencies, strict deadlines, and complex paperwork. One misstep can delay your transfer by months or cost thousands in penalties.

We at Law Offices of Roshni T. Desai have helped families move properties through trusts efficiently. This guide walks you through the exact steps that work in Santa Ana.

What Happens During Trust Administration for Real Estate

The Core Responsibilities of Trust Administration in California

Trust administration in California involves far more than transferring property from one name to another. When a property sits in a trust, the successor trustee manages that asset according to the trust document’s terms, notifies beneficiaries and creditors within statutory deadlines, gathers documentation, secures the property, and ultimately transfers it to the rightful beneficiaries. California Probate Code sections 15600 through 15700 outline these duties in detail, and missing even one deadline can trigger penalties or court involvement. The trustee must file a Notice of Succession with the county recorder, complete a Preliminary Change of Ownership Report (PCOR) or Change of Ownership Statement (COS) with the assessor within strict timeframes, and handle property tax implications that arise when ownership transfers. For real estate specifically, this means coordinating with multiple county offices simultaneously-the recorder’s office to document the transfer, the assessor’s office to adjust property taxes, and potentially the title company if a title search is needed.

Why Real Estate Demands a Different Approach Than Other Assets

Real property transfers trigger automatic tax reassessment under California Revenue and Taxation Code Section 480. When beneficial ownership changes (whether through death or a distribution from the trust), the assessor reassesses the property at current market value, which often results in a higher tax bill. The PCOR or COS must be filed within 150 days of the triggering event, and the assessor will impose penalties reaching up to $5,000 for residential properties if this deadline is missed. Unlike bank accounts or investment holdings, real estate cannot be quickly liquidated or divided among beneficiaries. The property must remain titled and insured throughout the transition period, and the trustee bears liability if the property is damaged or neglected. Additionally, if the property has a mortgage, the lender must be notified of the ownership change, and some loans may include acceleration clauses that become problematic if not handled correctly.

Santa Ana’s Specific Procedural Requirements

Santa Ana’s location in Orange County creates specific procedural requirements that many families overlook. The Orange County Assessor requires that every change of ownership-including trust-to-beneficiary transfers-be reported on either a PCOR (if a new document is recorded) or a COS (if the assessor initiates the process). If a PCOR is not filed when a deed is recorded, the assessor will mail a COS, and the recipient then has 90 days to return it or face the $5,000 penalty. Real estate in Santa Ana also qualifies for the expanded main home exemption under Assembly Bill 2016, which allows properties valued up to $750,000 to transfer without probate-but only if the trust is properly funded and the property is titled in the trust’s name before death. Many families discover too late that their property was never actually transferred into the trust, meaning the full probate process becomes necessary despite having a trust document in place.

Hidden Complications in Santa Ana Properties

Santa Ana properties with tenants, commercial components, or shared ownership structures introduce complications around liability, tenant rights, and co-owner consent that require careful coordination with local authorities and proper documentation. These issues can create disputes or title problems after the transfer is complete if not addressed upfront. The trustee must verify the property’s current status, identify all parties with claims or interests, and document each step of the transfer process. When multiple stakeholders are involved, the timeline extends significantly, and the risk of overlooking a requirement increases. Understanding these local nuances before the transfer begins allows you to anticipate obstacles and plan accordingly-which is exactly why the documents and filing requirements in the next section matter so much.

Key Documents and Filing Requirements for Trust Real Estate Transfers

The Foundation: Proof Your Property Actually Sits in the Trust

Trust-based real estate transfers in Santa Ana start with one fundamental requirement: proof that the property sits in the trust. Many families discover their property was never formally transferred into the trust document, which means the entire transfer process derails before it begins. You need the original trust document, the deed showing the property is titled in the trust’s name, and a death certificate if the transfer occurs after the grantor’s death. Without these three items, the recorder’s office and assessor will reject your filings and force you to restart. California Probate Code Section 13100 requires you to file a Succession to Real Property petition if the estate exceeds the small estate threshold, or you can use streamlined procedures under Section 13200 if the real property value falls below $69,625 as of April 1, 2025 per Assembly Bill 2016.

The PCOR: Your Single Most Important Document

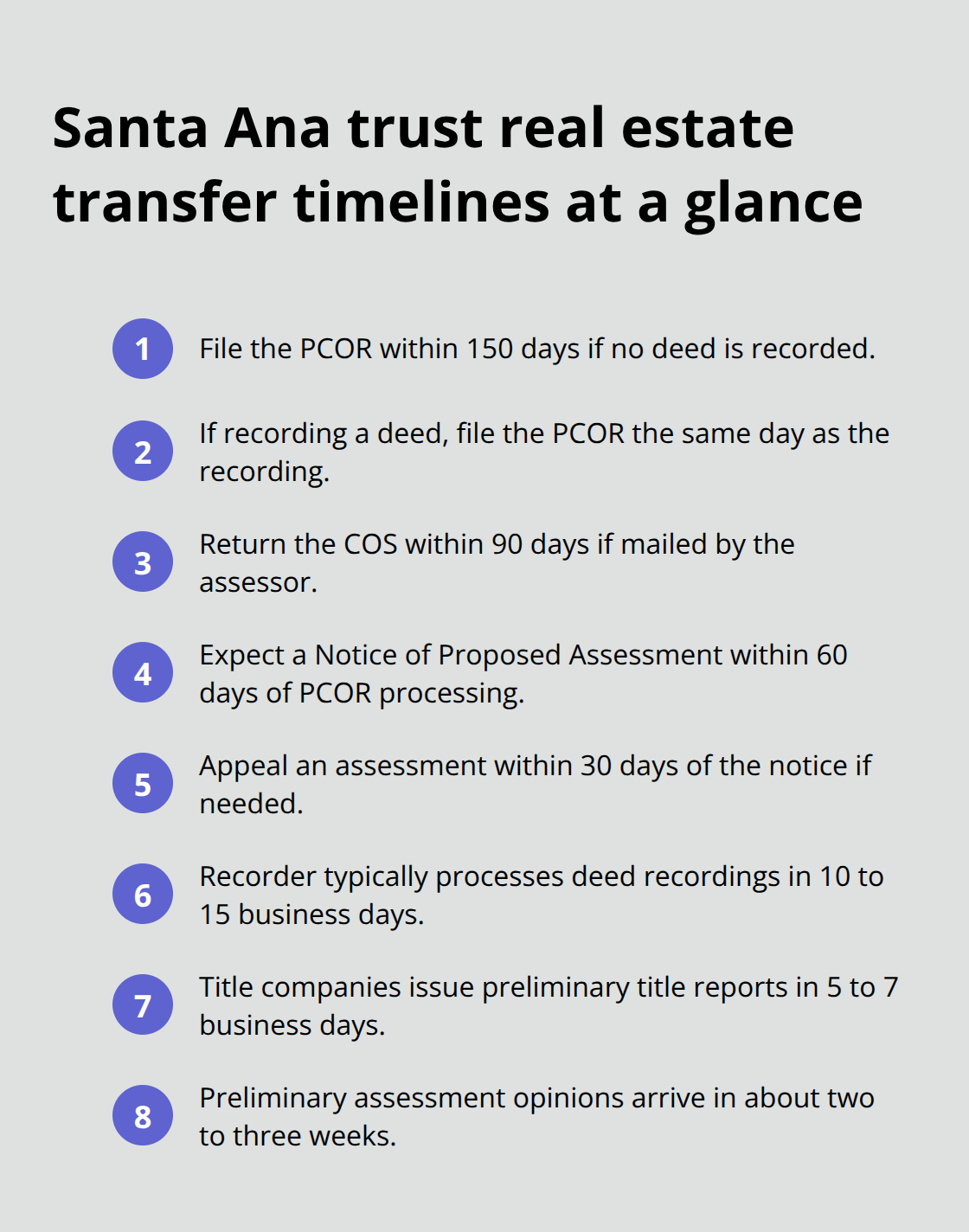

The Preliminary Change of Ownership Report (PCOR) is non-negotiable-this document triggers the assessor’s awareness that ownership has changed and prevents the $5,000 residential penalty. If you record a new deed transferring the property from the trust to the beneficiary, you must file the PCOR simultaneously with the deed at the Orange County Recorder’s office. The PCOR requires specific information: the purchase price (even if no money changed hands, you must list the property’s fair market value), financing terms, and the date of transfer. The assessor uses this data to reassess the property under Revenue and Taxation Code Section 480, which almost always results in a higher property tax bill. If you fail to file the PCOR when recording the deed, the Orange County Assessor will mail a Change of Ownership Statement (COS) within weeks, and you then have exactly 90 days to return it completed. Missing that 90-day deadline triggers automatic penalties-the $5,000 cap applies to residential properties, but the assessor can also pursue back taxes with interest dating from the transfer date.

Timing Requirements That Cannot Slip

Within 150 days of the triggering event (typically the grantor’s death), you must submit the PCOR with a copy of the death certificate to the assessor if no new deed is recorded. If you record a new deed, the PCOR must be filed with that deed at the recorder’s office on the same day. The successor trustee’s signature on the deed must match the trust document exactly, or the recorder will reject the recording and force you to resubmit and restart the timeline. Preparing the deed and PCOR simultaneously rather than sequentially compresses your filing window and reduces the risk of missing a deadline. Many families attempt these filings without legal review and make errors like misspelling the trustee’s name, using an outdated trust version, or listing an incorrect property description. These mistakes force you to record a corrective deed, which triggers a second PCOR filing and another round of assessor processing.

Property Tax Bills and Ownership Records

The property tax bill itself arrives to the owner of record on the lien date of January 1, and if you acquire the property after January 1, the prior owner’s name may still appear on the current year’s bill-this is normal and does not indicate a problem with your transfer, but it does require careful tracking so you do not miss tax payments or assume the previous owner remains responsible. Documentation must include the trustee’s authority to act (a certification of trust or a copy of the relevant trust pages), proof of the beneficiary’s identity, and any title insurance commitment if a title search was ordered. Skipping the title search saves time upfront but creates risk if a lien, easement, or prior claim emerges after the transfer closes-Santa Ana properties with older deeds sometimes carry forgotten liens or boundary disputes that surface only when the property changes hands.

Coordinating Multiple Filings Across County Offices

The real estate transfer process requires you to coordinate filings across the Orange County Recorder’s office, the Orange County Assessor’s office, and potentially the title company. Each office operates on its own timeline and uses different forms, which means a single error in one filing can cascade into delays across all three. The recorder processes deeds and PCORs, the assessor processes the COS if you miss the initial PCOR deadline, and the title company (if involved) verifies that no liens or claims block the transfer. When you prepare these documents correctly the first time, the entire process moves forward without interruption-but when errors occur, you restart from the beginning. This is where the coordination between agencies becomes critical, and understanding which office handles which requirement prevents costly delays and penalties.

How Santa Ana’s County Offices Process Trust Real Estate Transfers

The Orange County Recorder’s office and the Orange County Assessor’s office operate independently but must coordinate seamlessly for your trust transfer to succeed. The recorder documents ownership changes through deed recordings, while the assessor handles property tax reassessment. Neither office communicates directly with the other, which means you must manage both filings simultaneously to avoid penalties or delays. When you record a deed transferring property from the trust to a beneficiary, you must file the PCOR with that same deed on the same day at the recorder’s office. The recorder will timestamp both documents and forward a copy of the PCOR to the assessor electronically. If you record the deed without the PCOR, the assessor receives no notification and will mail a Change of Ownership Statement within weeks, forcing you into a reactive 90-day window to respond.

The assessor’s office processes thousands of property transfers annually across Orange County, and they prioritize PCOR filings over COS responses because the PCOR indicates you filed proactively. Submitting the PCOR upfront shows you understand the requirement and dramatically reduces the likelihood of assessment errors or delayed processing. The recorder’s office in Santa Ana typically processes deed recordings within 10 to 15 business days, but this timeline assumes the deed contains no errors and the property description matches county records exactly. A single misspelled name, incorrect parcel number, or formatting issue forces the recorder to reject the recording and return it for correction, restarting the entire timeline.

Property Tax Reassessment and Assessment Notices

Property tax implications emerge immediately after the assessor receives notice of the ownership change. California Revenue and Taxation Code Section 480 requires reassessment at current market value when beneficial ownership transfers, and the assessor uses comparable sales data from Santa Ana to determine the new assessed value.

Most trust-to-beneficiary transfers result in higher property tax bills because the original assessed value (often from years or decades earlier) is lower than current market conditions. The assessor will mail a Notice of Proposed Assessment within 60 days of processing your PCOR, and the notice includes the new assessed value and the date it becomes effective.

Santa Ana property owners frequently contest these assessments if they believe the assessed value exceeds fair market value, but the appeal process requires filing within 30 days of the notice and submitting comparable sales data or an independent appraisal. Many families miss the appeal deadline simply because they do not understand the notice or assume the assessor’s valuation is final. If you anticipate a significant tax increase, request a preliminary assessment opinion from the assessor’s office before filing the PCOR so you can plan for the financial impact. The assessor’s office provides this service at no cost and takes approximately two to three weeks to respond.

Additionally, verify whether the property qualifies for any exemptions or Proposition 19 protections that might limit the reassessment. Properties transferred between parents and children may qualify for exclusions under Proposition 19 if certain conditions are met, potentially saving thousands in annual property taxes.

Coordinating the Deed, PCOR, and Title Insurance Timeline

Prepare the deed and PCOR in parallel rather than sequentially to compress your filing window and reduce errors. The trustee’s name, the property description, and the transfer date must match exactly across the deed and PCOR or the assessor will reject the PCOR and request corrections. Obtain a title commitment from a title company before preparing either document because the title report identifies liens, easements, boundary disputes, or other claims that must be resolved before the transfer closes. If a lien exists on the property, you must pay it off at closing or obtain a lien release from the creditor.

The title company will issue a preliminary title report within five to seven business days after you submit the property information, and this report reveals issues that could derail the entire transfer if discovered later. Record the deed and PCOR simultaneously at the recorder’s office to pay a single recording fee for both documents, typically $20 to $30 depending on the number of pages. Splitting the filings into separate submissions doubles the recording fees and increases the risk that one document arrives without the other, creating a gap where the assessor sees a deed but no PCOR and initiates a COS mailing.

The successor trustee must sign the deed in front of a notary public, and the notarization must occur after the triggering event (typically the grantor’s death) for the transfer to be valid. Stale-dated notarizations or notarizations predating the death create title defects that surface during future property sales or refinances.

Managing the 150-Day Deadline and Penalty Avoidance

The 150-day deadline begins on the date of death if the property transfers due to the grantor’s passing, or on the date of the distribution if the trustee transfers the property to a beneficiary during the grantor’s lifetime. This deadline applies only if no new deed is recorded; if you record a deed, the PCOR filing deadline is the same day as the recording. Missing the 150-day deadline when a death certificate is involved triggers immediate penalties, and the assessor will assess back taxes from the date of death forward with interest accruing at the applicable rate.

The Orange County Assessor’s office website provides a COS information line at (714) 834-2727 where staff can confirm deadlines for your specific property and answer questions about filing requirements. Call this number early in the process to prevent confusion about which forms to use and which deadlines apply. If you are uncertain about the property’s assessed value or the likely tax impact, request a preliminary assessment before filing the PCOR. The assessor’s office processes these requests within two to three weeks and provides an informal estimate that helps you plan financially. Failing to anticipate the tax impact leaves beneficiaries surprised by significantly higher bills, sometimes creating family disputes about who pays the increase or whether the property should be sold to cover taxes.

Final Thoughts

Trust administration filing for real estate transfers in Santa Ana requires you to handle three core elements correctly: proof that the property sits in the trust, simultaneous filing of the deed and PCOR with the Orange County Recorder, and timely submission of ownership change documentation to the assessor within 150 days of the triggering event. The PCOR prevents the $5,000 residential penalty and signals to the assessor that you filed proactively rather than reactively. Coordinating with the recorder’s office and assessor’s office simultaneously compresses your timeline and reduces the risk of errors cascading across multiple filings.

Professional guidance reduces both timeline and costs by identifying issues before they become problems. A title commitment reveals liens or boundary disputes early, a preliminary assessment opinion from the assessor prevents tax surprises, and proper deed preparation eliminates rejections and refilings. We at Law Offices of Roshni T. Desai have guided families through trust administration filing across Santa Ana and Southern California, and our background in law and real estate streamlines the entire process.

Your next step is to gather the original trust document, the deed showing the property is titled in the trust, and the death certificate if applicable. Then contact Law Offices of Roshni T. Desai for a free consultation to review your specific situation and timeline. We offer flexible home or office visits across Southern California and can walk you through the exact steps required for your Santa Ana property.