Your Trust Administration Checklist: Stay on Track With Confidence in Orange County, California

Serving as a trustee in Orange County comes with real responsibilities and tight deadlines. Missing even one step can create legal problems and conflict with beneficiaries.

We at Law Offices of Roshni T. Desai created this trust administration checklist to guide you through each phase of the process. You’ll know exactly what to do and when to do it.

What Trust Administration Really Means

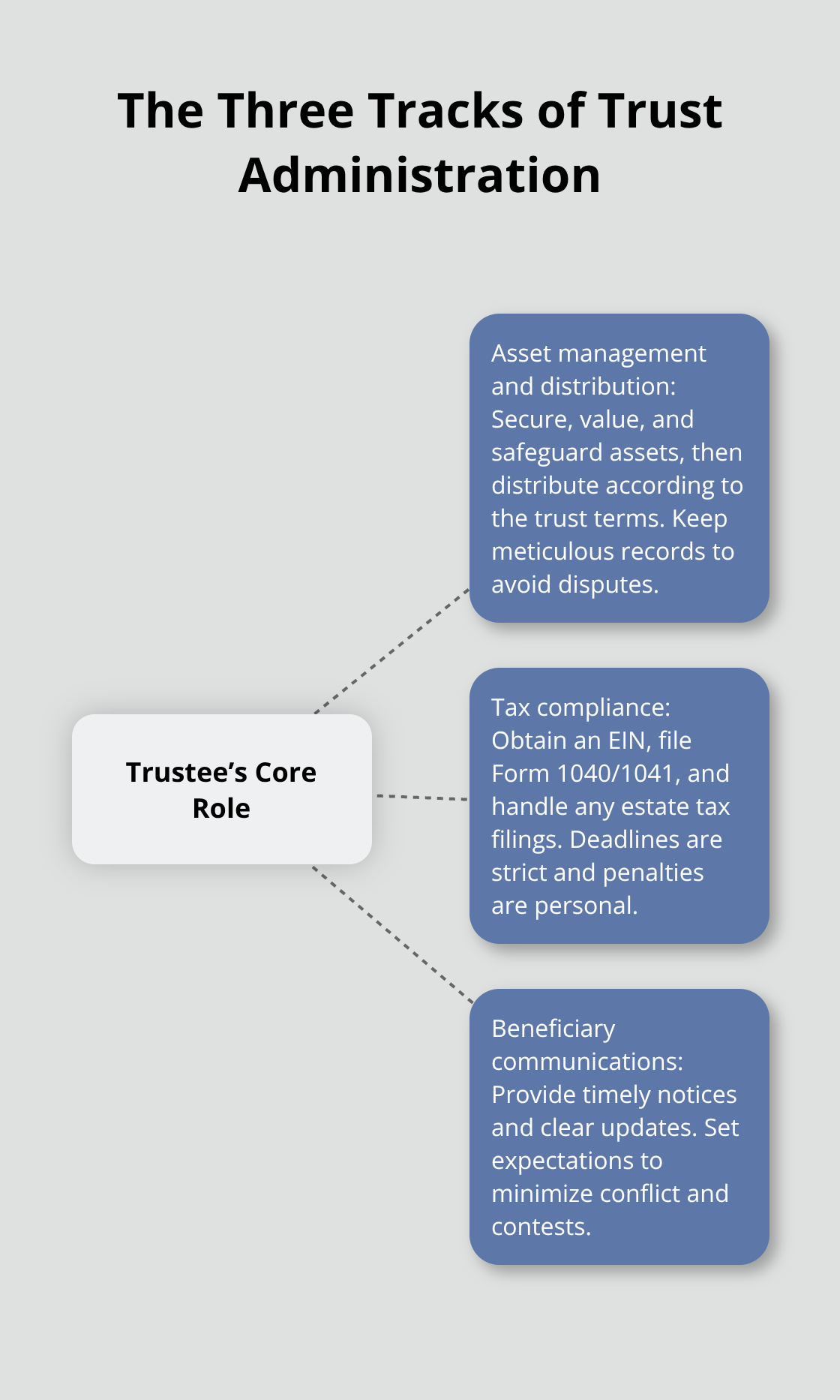

Trust administration in Orange County is a structured four-phase process governed by California Probate Code sections 16000–16015, not a simple handoff of assets. The trustee manages three parallel tracks simultaneously: asset management and distribution, tax compliance, and beneficiary communications. This is why most straightforward estates take 6–12 months to close, and complex ones with multiple properties or contested beneficiaries take significantly longer. The process begins the moment the trustor passes away and does not end until the final distribution is complete and all records are filed.

Many trustees underestimate this timeline and rush distributions, which creates personal liability and potential legal challenges from beneficiaries.

Secure and Inventory Assets Immediately

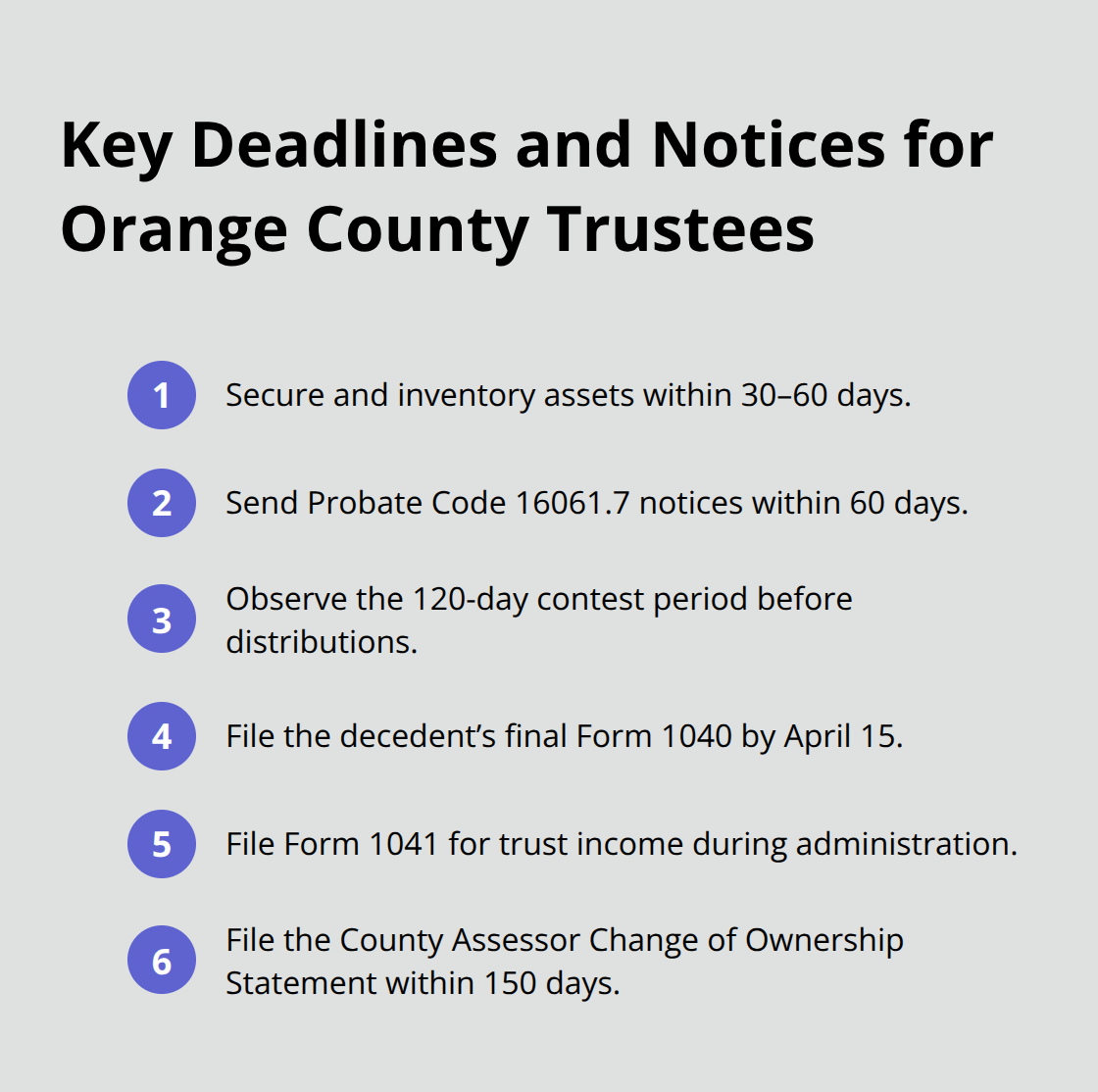

Your first obligation is to secure and inventory every trust asset within the first 30–60 days. Obtain at least five death certificates (ten if multiple real estate holdings exist), locate the original trust document and any amendments, and immediately protect property by updating insurance and safeguarding valuables. For real estate in Orange County, record an Affidavit of Death of Trustee with the county recorder to preserve title and prevent disputes. Open a dedicated trust bank account and obtain a federal Employer Identification Number (EIN) from the IRS-you cannot use the decedent’s Social Security number after death. Create a comprehensive inventory listing all bank accounts, investment portfolios, real estate, vehicles, and personal property. For significant assets like real estate, obtain formal appraisals dated to the decedent’s death to establish the stepped-up basis, which can dramatically reduce capital gains taxes when beneficiaries eventually sell. According to IRS Publication 551, this date-of-death valuation is critical and must be documented carefully. Commingling trust funds with personal accounts or failing to maintain separate records exposes you to personal liability and makes it nearly impossible to defend yourself if a beneficiary challenges your administration.

File Taxes and Notify Beneficiaries on Schedule

Tax filing runs parallel to asset management and is non-negotiable. File the decedent’s final Form 1040 by April 15 of the following year, file Form 1041 (the fiduciary income tax return) for any trust income earned during administration, and potentially file Form 706 (the federal estate tax return) if the estate exceeds the federal exemption threshold. In Orange County, file a Change of Ownership Statement with the County Assessor within 150 days due to Proposition 19, which changed how property transfers to beneficiaries are taxed-failing to file this form can trigger unexpected reassessments and higher property taxes.

Within 60 days of the trustor’s death, California Probate Code section 16061.7 requires you to send a statutory notice to all beneficiaries and heirs with specific language and the trust administration address; beneficiaries then have 120 days to contest the trust. Do not distribute assets during this contest window unless absolutely necessary, as distributions made before the 120-day period expires can be reversed, creating personal liability.

Complete Accounting and Final Distributions

Once debts, taxes, and administrative expenses are paid, prepare a final accounting under Probate Code section 16062 showing every dollar in and out, obtain written approval from beneficiaries, and only then distribute remaining assets according to the trust terms. This sequencing is critical-distributing before taxes and debts are settled is the fastest way to face personal liability claims from creditors or the IRS. The mistakes trustees make during this phase often stem from incomplete record-keeping or pressure from impatient beneficiaries, both of which we address in the next section.

Where Trustees Go Wrong

The most damaging mistakes in trust administration happen not because trustees lack good intentions, but because they underestimate the complexity of the role or fail to anticipate how quickly problems escalate. Trustees who skip the statutory 60-day beneficiary notice required by California Probate Code section 16061.7 create immediate legal exposure-beneficiaries can challenge the entire administration if they discover notification did not occur within the required window. Similarly, trustees who distribute assets before all debts and taxes are settled expose themselves to personal liability from creditors or the IRS, which can pursue individual trustees for unpaid estate obligations. The California Probate Code sections 16000–16015 impose fiduciary duties of loyalty, impartiality, and detailed record-keeping; violating these duties can result in surcharge actions where beneficiaries sue the trustee personally to recover mismanaged funds.

Distributing Assets Too Early Creates Irreversible Liability

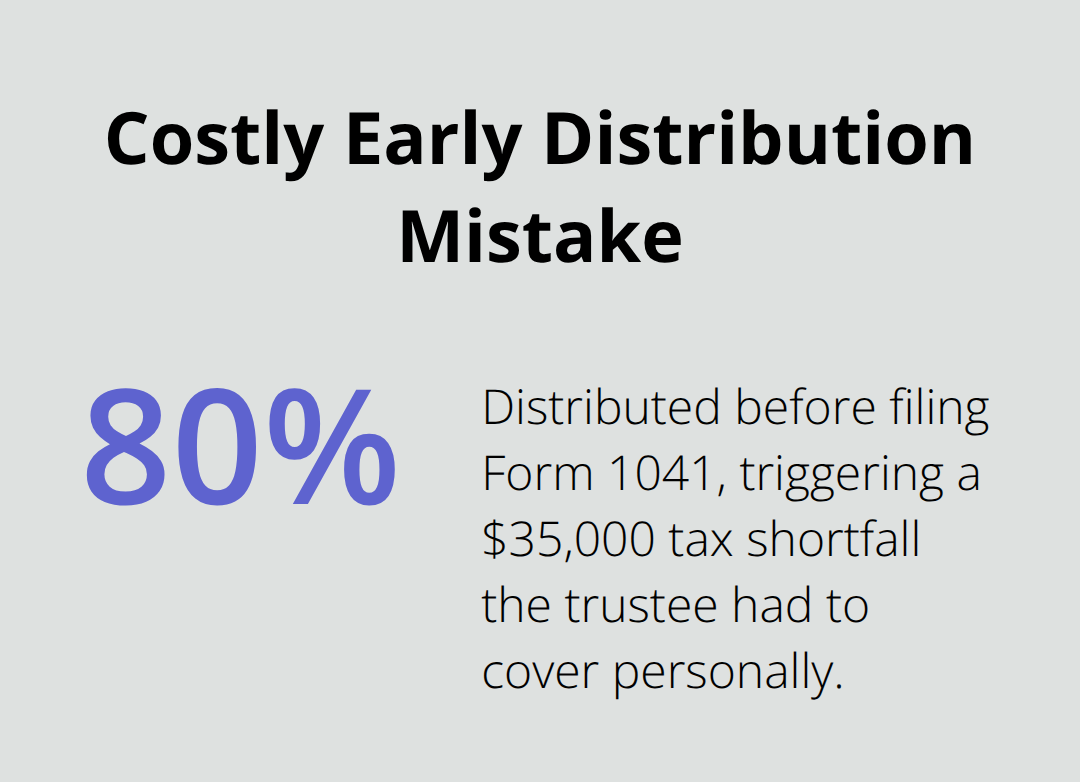

One trustee in Orange County distributed 80 percent of an estate to beneficiaries before filing the final Form 1041, only to discover the trust owed $35,000 in income taxes. The trustee then had to personally cover the shortfall because beneficiaries had already received their distributions.

This scenario is entirely preventable with proper sequencing: secure assets, obtain the EIN, file taxes, settle debts, prepare a final accounting, get beneficiary approval, and only then distribute remaining assets. The IRS and California courts hold trustees personally accountable when distributions precede tax settlement, regardless of whether the trustee acted in good faith.

Commingling Funds Destroys Your Defense

Trustees who deposit trust money into their own checking account or pay trust expenses from personal funds cannot defend themselves if a beneficiary questions where money went or whether distributions were accurate. The IRS and California courts view commingled accounts as evidence of mismanagement, and audits become far more aggressive when records are mixed. A dedicated trust bank account costs nothing to open and creates an automatic paper trail that protects the trustee. Similarly, failing to obtain an EIN and continuing to use the decedent’s Social Security number for trust accounts triggers IRS penalties and makes tax filing impossible-the IRS will not accept Form 1041 filed under a deceased person’s SSN.

Poor Communication Generates Unnecessary Conflict

Trustees who delay communicating with beneficiaries or provide vague updates about the administration timeline generate suspicion and conflict. California law requires transparency; beneficiaries are entitled to know what assets exist, what debts and taxes are owed, and approximately when distributions will occur. Trustees who treat beneficiaries as adversaries rather than stakeholders often face unnecessary disputes, mediation costs, and delays. Send written updates every 60–90 days, explain major decisions with clear reasoning, and maintain a centralized file of all communications and receipts so nothing is lost or forgotten. This approach prevents most conflicts before they start and protects you if disputes arise later.

These preventable errors-rushing distributions, mixing funds, and withholding information-account for the majority of trust administration problems in Orange County. The next section walks through the specific checklist that keeps trustees on track and protects them from liability.

Your Step-by-Step Administration Roadmap

Secure Assets and Obtain Critical Documents in the First 60 Days

The first 60 days after the trustor’s death set the tone for the entire administration. Within this window, you must obtain at least five death certificates (ten if multiple real estate holdings exist) and locate the original trust and all amendments. Secure real property immediately by updating insurance and recording an Affidavit of Death of Trustee with the county recorder. Open a dedicated trust bank account right away-do not deposit trust funds into your personal checking account under any circumstance. The IRS and California courts treat commingled accounts as evidence of mismanagement, and audits become far more aggressive when records are mixed.

Apply for a federal Employer Identification Number (EIN) from the IRS without delay. You cannot use the decedent’s Social Security number after death, and the IRS will reject Form 1041 filed under a deceased person’s SSN. Create a comprehensive inventory listing all bank accounts, investment portfolios, real estate, vehicles, and personal property. For significant assets like Orange County real estate, obtain formal appraisals dated to the decedent’s death to establish the stepped-up basis. According to IRS Publication 551, this date-of-death valuation directly reduces capital gains taxes when beneficiaries eventually sell the property.

Notify Beneficiaries and Respect the Contest Window

Within 60 days of death, California Probate Code section 16061.7 requires you to send a statutory notice to all beneficiaries and heirs using specific language and including the trust administration address. Beneficiaries then have 120 days to contest the trust. Do not distribute assets during this contest window unless absolutely necessary, as distributions made before the 120-day period expires can be reversed and create personal liability.

File Tax Returns and Property Documents on Schedule

File the decedent’s final Form 1040 by April 15 of the following year and file Form 1041 for any trust income earned during administration. File a Change of Ownership Statement with the County Assessor within 150 days due to Proposition 19, which changed how property transfers to beneficiaries are taxed. Failing to file this form triggers unexpected reassessments and higher property taxes. Identify all outstanding debts, liabilities, and creditors, then pay valid debts and ongoing expenses from trust funds in accordance with California law.

Prepare Final Accounting and Distribute Assets

Once debts, taxes, and administrative expenses are paid, prepare a final accounting under Probate Code section 16062 showing every dollar in and out. Obtain written approval from beneficiaries, then distribute remaining assets according to the trust terms. This sequencing is non-negotiable; distributing before taxes and debts are settled exposes you to personal liability claims from creditors or the IRS. Send written updates every 60–90 days, explain major decisions with clear reasoning, and maintain a centralized file of all communications and receipts. Straightforward estates with no contests typically close within about a year, but more complex cases with multiple properties or beneficiary disputes take significantly longer.

Final Thoughts

Trust administration in Orange County demands precision, timing, and knowledge of California Probate Code requirements that shift frequently. The trust administration checklist we’ve outlined covers the essential steps, but executing them correctly while managing grief, family dynamics, and complex property transactions is where most trustees struggle. Professional guidance makes the difference between a smooth administration and costly mistakes that create personal liability.

We at Law Offices of Roshni T. Desai work with trustees throughout Orange County and neighboring counties to handle every phase of trust administration. Our dual licensure as both an attorney and real estate professional streamlines property sales and transfers, reducing costs and delays that often arise when multiple professionals are involved. We coordinate appraisals, title work, and tax implications so your administration stays on track and complies with every statutory requirement under Probate Code sections 16000–16015.

Law Offices of Roshni T. Desai offers free consultations with flexible home or office visits so you can discuss your specific situation without pressure or cost. Contact us to review your trust administration checklist and get clarity on next steps.