Probate Attorney for Executors in Santa Ana, California: A Fiduciary Guide to Success

Serving as an executor comes with significant legal and financial responsibilities. At Law Offices of Roshni T. Desai, we help executors navigate probate in Santa Ana by handling court filings, asset management, and tax obligations.

This guide covers what you need to know about fiduciary duties, common mistakes to avoid, and how a probate attorney for executors can protect you from personal liability while reducing administrative costs.

What You Must Do in the First Months After Death

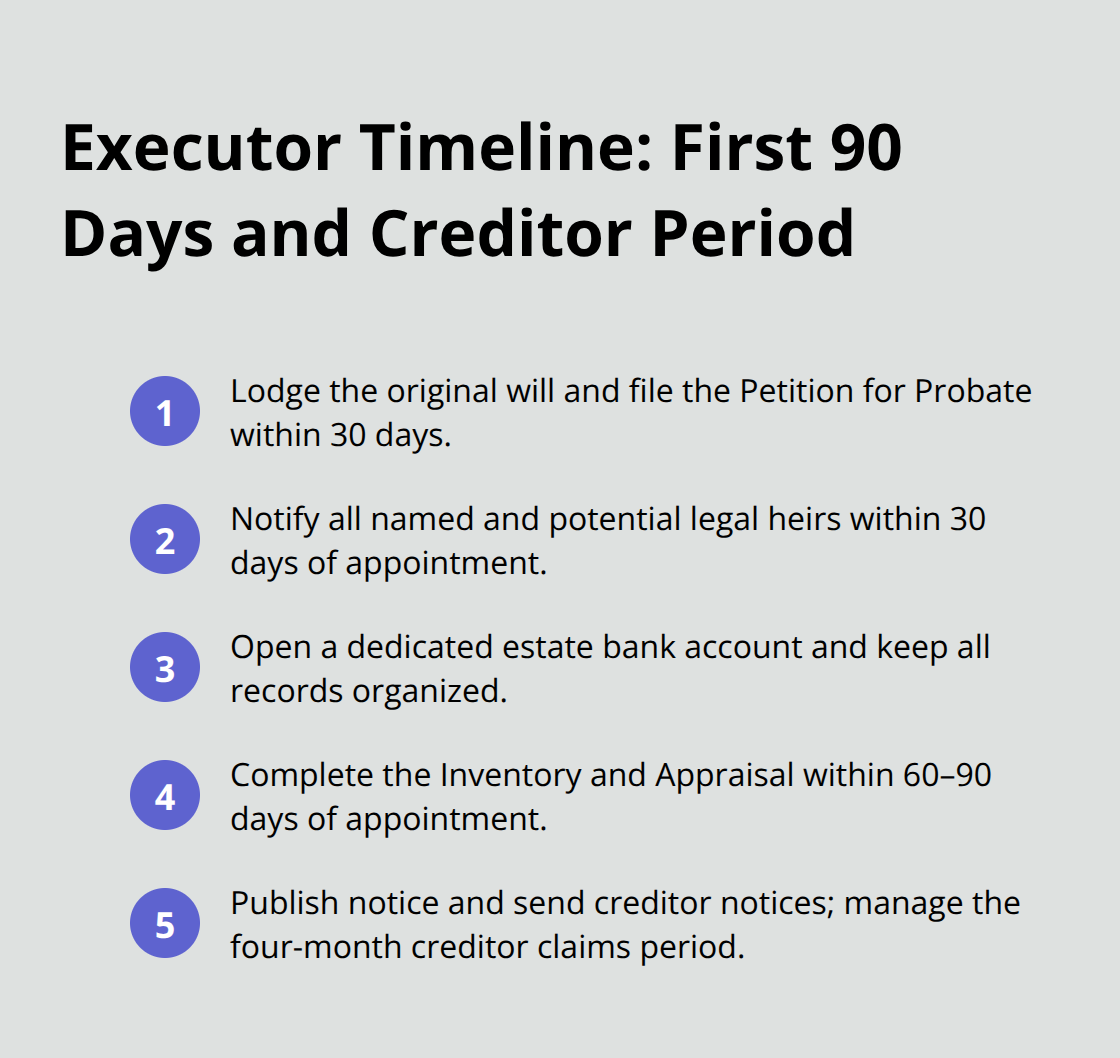

Probate in Santa Ana begins the moment you’re appointed executor, and the clock starts ticking immediately. According to the California Courts Self-Help Center, you have 30 days to lodge the original will with Orange County Superior Court’s Probate Division, and you must file a Petition for Probate within that same window. Missing this deadline doesn’t just delay the process-it signals to the court that you may be unprepared to handle the estate. The court appoints a probate referee to value non-cash assets like real estate, vehicles, and collectibles, and you’ll need to complete a full Inventory and Appraisal within 60 to 90 days of your appointment.

This inventory must account for every asset: bank accounts, investment portfolios, retirement benefits, personal property, and real estate. Undervaluing assets creates tax problems later; overvaluing them inflates administrative costs. The California Probate Code requires you to notify all named heirs and potential legal heirs within 30 days of your appointment. You must also publish notice to unknown creditors and send formal notice to all known creditors, triggering a four-month creditor claims period under California law. This notification window is non-negotiable. If you fail to properly notify a known creditor, that creditor can file a claim indefinitely, potentially depleting funds meant for beneficiaries.

Opening an Estate Bank Account

Your first financial action must be opening a separate estate checking account in the estate’s name. Do not deposit estate funds into your personal account or a joint account. The California Probate Code requires that all estate assets flow through a single account, and mixing personal funds with estate funds creates accounting nightmares that courts view unfavorably. You’ll need a federal employer identification number (EIN) from the IRS, which you can obtain online immediately. When you deposit assets into the estate account, you must document every transaction with supporting bank statements and receipts. The probate referee will examine this account during the appraisal process, so sloppy record-keeping signals mismanagement to the court.

Managing Creditor Claims and Debt Obligations

The four-month creditor period is your window to identify and resolve debts. You must review each claim carefully: legitimate claims get paid from estate funds, but fraudulent or inflated claims should be rejected. If you reject a claim, the creditor can sue the estate, and you’ll need documentation showing why the claim was invalid. You should pay legitimate claims promptly to avoid interest accrual and creditor lawsuits that drain the estate’s resources. The Central Justice Center in Santa Ana houses Orange County’s probate division, and courts here expect executors to manage creditor claims efficiently. Delaying payment or ignoring claims signals poor administration and can lead to removal.

Protecting Yourself from Early Mistakes

The first months after death set the tone for the entire probate process. Courts in Orange County scrutinize how you handle initial filings, asset documentation, and creditor notifications. Sloppy work in these early stages (missed deadlines, incomplete inventories, or improper notices) creates liability that follows you throughout administration. You face personal liability if you fail to meet statutory requirements or breach your fiduciary duties. Many executors discover too late that early mistakes compound into costly delays and potential removal by the court. The probate attorney at Law Offices of Roshni T. Desai can walk you through these first critical months, ensuring your filings meet court standards and your asset documentation protects you from future disputes.

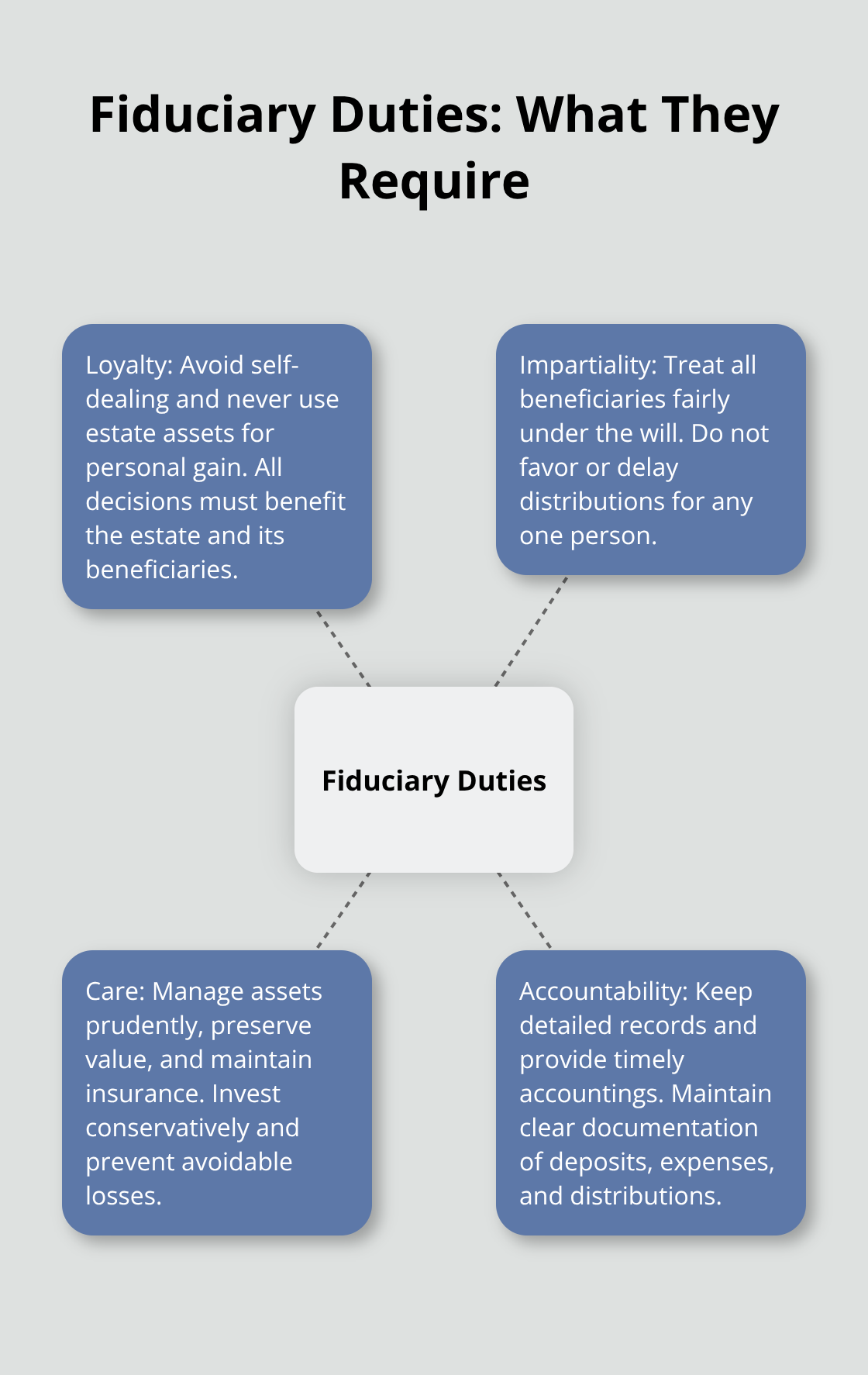

What Fiduciary Duties Actually Mean for Your Actions

As an executor, California law imposes four core duties on you: loyalty, impartiality, care, and accountability. These aren’t abstract concepts-they translate into specific actions you must take or avoid.

Your Duty of Loyalty

Your duty of loyalty prohibits you from using estate assets for personal benefit. The California Probate Code forbids self-dealing, which includes borrowing from the estate, purchasing estate property at below-market prices, or steering assets to yourself ahead of beneficiaries. Courts take this seriously. If you breach loyalty, the court can surcharge you (force you to repay the estate from your own pocket), remove you entirely, or deny you compensation.

Treating All Beneficiaries Fairly

Your duty of impartiality requires you to treat all beneficiaries fairly according to the will’s terms. If the will names three beneficiaries, you cannot favor one over the others or delay distributions to some while accelerating them to others. This duty applies throughout the entire administration process, from asset management to final distribution.

Managing Assets Prudently

Your duty of care means you must manage assets prudently, avoid unnecessary losses, and invest conservatively. If you leave estate funds in a non-interest-bearing account for months while inflation erodes value, or you fail to maintain property insurance on real estate, you’ve breached this duty. Courts expect you to act as a reasonable person would when handling someone else’s property.

Maintaining Records and Providing Accountings

Your duty to account requires you to maintain detailed records of every transaction: deposits, withdrawals, expenses, and distributions. When beneficiaries request an accounting (and they will), you must provide one within a reasonable timeframe. Missing this deadline signals mismanagement and invites litigation.

Handling Estate Debts and Tax Obligations

Paying debts and taxes is non-negotiable, and the timing matters enormously. Federal estate tax returns are due nine months after death according to the IRS, and missing this deadline triggers penalties and interest. You must also file the decedent’s final personal income tax return and any estate income tax returns if the estate generates income during administration. California requires you to file state estate tax returns if the federal return is required. Failing to file creates personal liability for unpaid taxes and penalties.

Many executors assume they can distribute assets freely once the creditor period ends, but that’s wrong. You must reserve funds for final income taxes, estate taxes, property taxes, and capital gains taxes on appreciated assets. If you distribute too early and funds run short, beneficiaries can sue you personally for the shortfall.

The probate process typically takes 12 to 18 months according to California court data, which gives you time to coordinate with accountants and tax professionals. A CPA working alongside your probate attorney helps ensure tax filings align with asset distributions and creditor payments. Real estate sales within the estate frequently trigger capital gains taxes, and improper valuation at death can inflate tax liability significantly.

Document the fair market value of all assets as of the decedent’s death date, since this becomes the tax basis for beneficiaries. Selling estate real estate without court approval in some cases, or without proper documentation in all cases, creates liability. You must disclose the sale process and avoid selling to interested parties at below-market prices. These financial and legal complexities demand attention to detail-which is exactly where probate attorneys step in to guide your next moves.

Where Executors Go Wrong

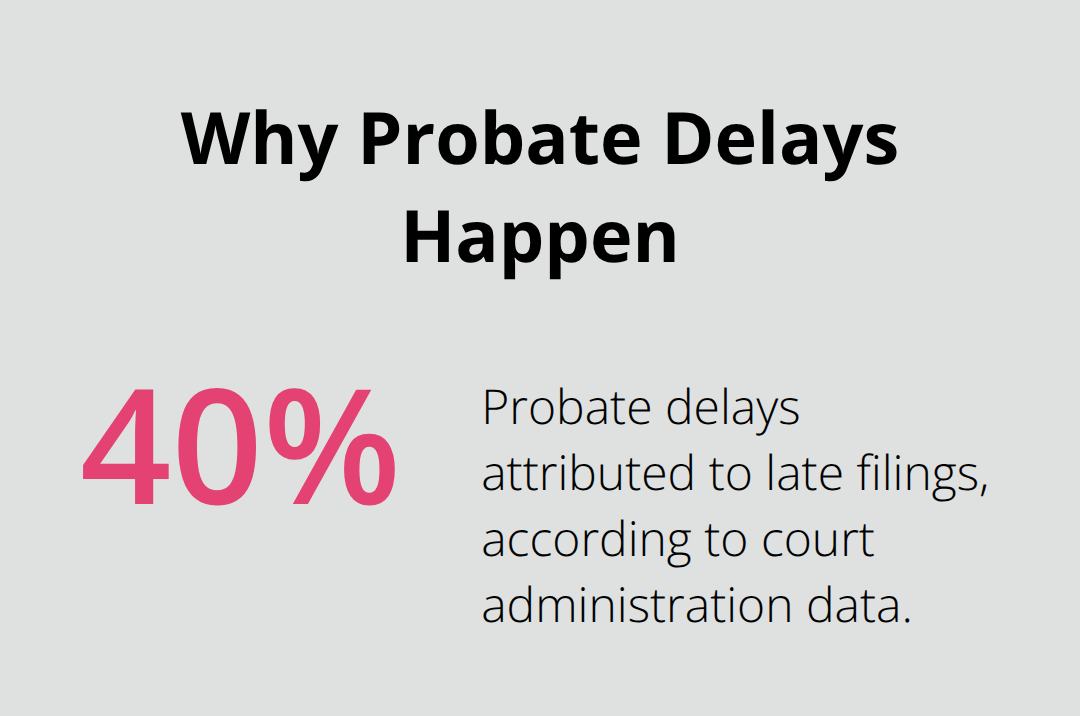

The gap between what executors think they must do and what California law actually requires creates the most preventable disasters in probate administration. Missed deadlines destroy estates more reliably than any other single factor. California law gives executors a 30-day window to lodge the will with Orange County Superior Court and file a Petition for Probate, yet approximately 40 percent of probate delays stem from late filings according to court administration data.

When you miss this deadline, the court questions your competence, and delays cascade through every subsequent step: creditor notifications slip, asset appraisals take longer, and distributions push into month 20 or beyond.

The Inventory and Appraisal Trap

The inventory and appraisal deadline typically falls 60 to 90 days after appointment, and courts in Santa Ana enforce this strictly. Failing to complete a thorough inventory creates two problems simultaneously: the probate referee cannot properly value assets, and the court cannot verify you have located all estate property. Undervaluing assets by even 10 percent creates enormous tax problems later, since beneficiaries inherit at the appraised value as their tax basis. Overvaluing assets inflates the estate’s apparent value and triggers unnecessary tax liability.

Creditor Notification Failures

The four-month creditor notification period is equally rigid. If you miss notifying a known creditor, that creditor retains the right to file claims indefinitely, potentially depleting funds meant for beneficiaries years after you thought probate was closed. This single mistake can reopen a closed estate and force you to pay claims from your own pocket.

Record-Keeping Disasters

Record-keeping failures compound these deadline mistakes into catastrophic liability. Many executors maintain incomplete or disorganized documentation: bank deposits recorded in a personal checkbook, estate expenses tracked on loose receipts, and distributions logged only in memory. When beneficiaries request accountings-and they will-you cannot produce clear records showing how money moved through the estate. Courts view this as mismanagement, and beneficiaries interpret it as evidence of theft or incompetence. A CPA or probate attorney reviewing your records should see a clear audit trail from asset deposit through final distribution.

Real Estate Valuation and Sales

Real estate presents a particular valuation trap. The fair market value as of the decedent’s death date becomes the tax basis for beneficiaries and determines whether capital gains taxes apply when the property sells. Selling estate real estate at significantly below the appraised value without documenting fair-market justification invites litigation from beneficiaries and scrutiny from tax authorities. The probate referee’s appraisal sets the official value, and deviating from that figure without court approval creates personal liability for the difference.

Premature Asset Distribution

Distributing assets before all debts, taxes, and final expenses are paid ranks among the most serious errors. Federal estate tax returns are due nine months after death, and many executors distribute funds at month six assuming taxes are settled. When the estate’s final tax bill arrives at month eight, insufficient funds remain, and beneficiaries demand reimbursement from you personally. Early coordination between the executor, a probate attorney, and a tax professional can map the complete timeline before a single distribution occurs, preventing these costly mistakes entirely.

Final Thoughts

The mistakes outlined above are entirely preventable with proper legal guidance from the start. A probate attorney for executors in Santa Ana walks you through Orange County’s specific court procedures, filing requirements, and deadlines before you make costly errors. The Central Justice Center expects filings formatted precisely, deadlines met exactly, and documentation organized clearly-standards that vary slightly from other California counties.

Personal liability is the real cost of going it alone. When you miss a deadline, undervalue assets, or fail to notify a creditor, you face surcharge (repaying the estate from your own pocket), removal by the court, or litigation from beneficiaries. A probate attorney shields you by managing filings, coordinating with tax professionals, and documenting every decision so the court sees competent administration rather than negligence.

Probate typically runs 12 to 18 months, but missed deadlines and poor record-keeping stretch that to 24 months or longer. Attorney fees paid by the estate are far cheaper than the cost of fixing mistakes, defending against removal petitions, or paying personal liability claims. Contact Law Offices of Roshni T. Desai to schedule your free consultation and take the first step toward confident, protected administration.