Trust Administration for Couples: Coordinating Joint Estates and Protections

Most couples don’t realize their separate estate plans can create chaos for the surviving spouse. Without coordinated trust administration, assets get tangled in probate, taxes spike, and family decisions stall.

At Law Offices of Roshni T. Desai, we’ve seen how the right structure protects both partners and simplifies everything when it matters most. This guide shows you what works.

Why Coordinated Trust Administration Protects Both Partners

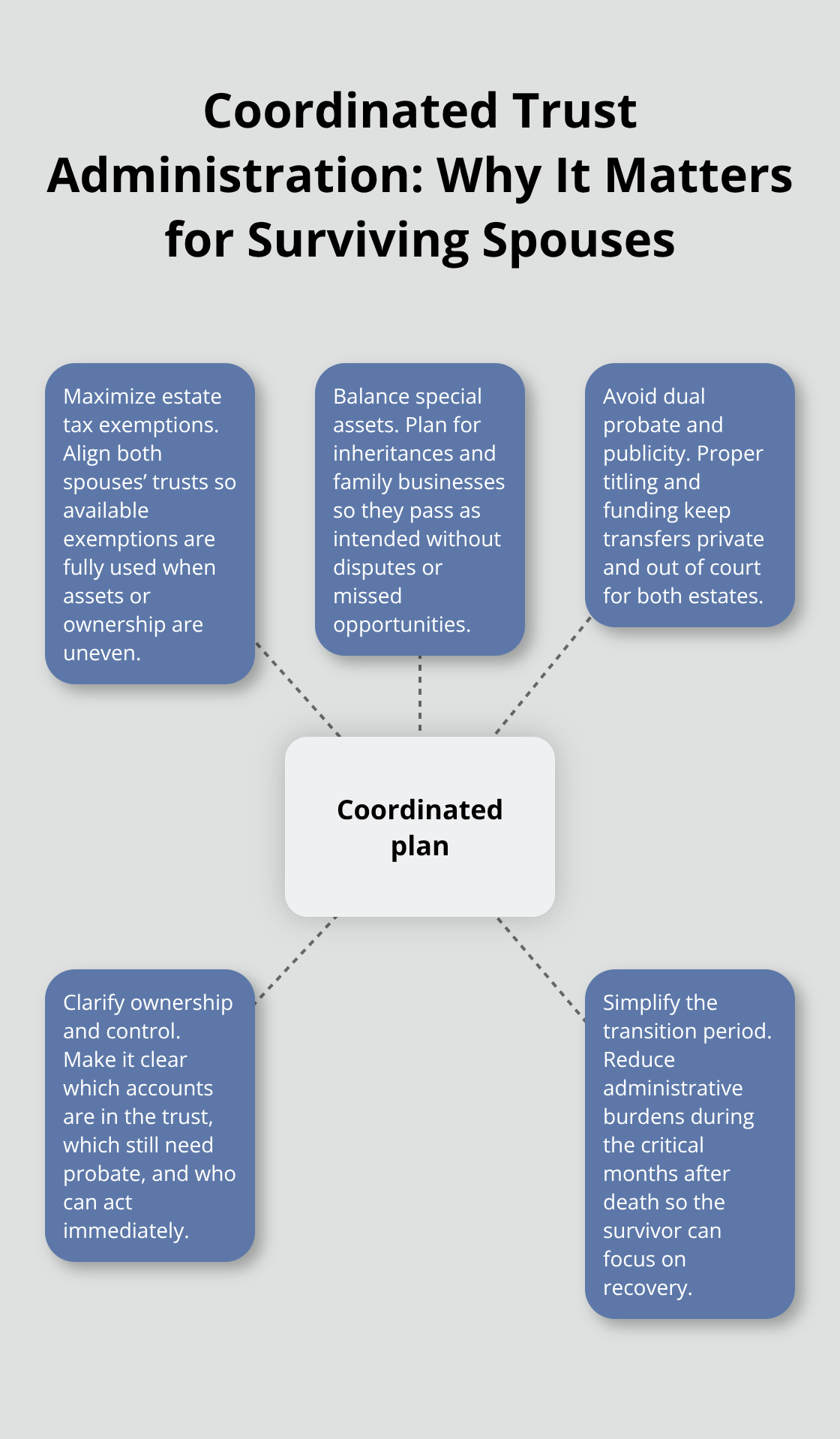

Probate in North Carolina costs approximately $4 per $1,000 of estate value, capped at $6,000, but that’s only the filing fee. When couples fail to coordinate their trusts, the surviving spouse often faces duplicate probate proceedings, court supervision of both estates, and public disclosure of all financial details. A Revocable Living Trust eliminates court involvement entirely, so assets transfer privately and immediately to the surviving spouse without the delays that probate creates. The real cost of uncoordinated planning shows up in time lost during grief and money wasted on redundant court fees and legal work that could have been prevented.

Federal estate tax exemptions currently sit at $13.99 million per person in 2025, but this nearly doubles to $15 million per person in 2026 according to the Internal Revenue Service. Couples who don’t align their trust structures miss opportunities to maximize these exemptions, particularly when one spouse holds substantially more assets or when inheritances and family businesses enter the picture. Without coordination, the surviving spouse inherits not just assets but also confusion about which accounts are in the trust, which still need probate, and who actually controls what during the critical months after death.

When Assets Get Stuck Between Plans

The transition period immediately after one spouse dies reveals every flaw in uncoordinated planning. If one partner funded their trust but the other didn’t, or if beneficiary designations on retirement accounts contradict the trust instructions, the surviving spouse becomes an unwilling administrator of chaos. Retirement accounts with outdated beneficiary names bypass the trust entirely and trigger immediate tax consequences the survivor didn’t anticipate. Joint ownership of property sounds protective but actually creates complications when one spouse dies, as the surviving spouse must prove survivorship and update titles before accessing or selling anything.

A joint trust structure keeps both spouses as co-trustees during life, so either partner can manage and use assets without restriction. When the first spouse becomes incapacitated, the surviving spouse already holds full control as co-trustee, which eliminates the need for guardianship proceedings or court intervention. At death, the surviving spouse maintains control without any required asset transfers, dramatically reducing the administrative burden during an emotionally difficult time.

Why Simplicity Matters for the Surviving Spouse

The surviving spouse shouldn’t spend months untangling financial mysteries while processing grief. A coordinated plan with clear successor trustee instructions, consistent asset titling, and aligned beneficiary designations allows administration to happen outside the courthouse entirely. The surviving spouse avoids probate delays, keeps financial affairs private, and retains flexibility to modify the trust if circumstances change.

Coordination isn’t about having the most complex plan-it’s about having one unified structure where every asset, every account, and every beneficiary designation points in the same direction. When couples use a joint trust, the executor’s role simplifies dramatically because there’s a single set of instructions rather than conflicting documents that need reconciliation. Separate trusts require explicit coordination to avoid gaps and overlaps, but when done properly, they offer greater flexibility for couples with different family situations or asset protection needs.

Moving Forward With Your Estate Structure

The choice between a joint trust and separate trusts depends on your asset complexity, family dynamics, and future life events. Couples with long, stable relationships, assets owned 50/50, and no children from prior relationships often benefit most from a joint trust structure. Those with inheritances, family businesses, or blended families typically need separate trusts to protect individual interests and prevent disputes among heirs.

Building the Right Structure for Your Assets and Family

Property ownership during marriage doesn’t automatically mean both spouses control assets equally, and this distinction shapes how you should structure your trust. North Carolina recognizes separate property owned before marriage and community property principles when assets are acquired during marriage, but your trust document must explicitly address which assets belong to each spouse and how they transfer at death. Many couples assume joint ownership solves everything, but joint titling actually creates problems when one spouse dies because the surviving spouse must update titles, prove survivorship to financial institutions, and potentially trigger unexpected tax consequences.

How Trust Structure Protects Your Assets

A joint trust lets both spouses act as co-trustees during life with equal access to all assets, while separate trusts give each spouse control over their own property and allow you to protect inheritances or family businesses from the other spouse’s creditors. The choice depends on whether you accumulated assets together or separately and whether you want to shield certain property from exposure if one spouse faces legal claims. Couples with long, stable relationships, assets owned 50/50, and no children from prior relationships often benefit most from a joint trust structure. Those with inheritances, family businesses, or blended families typically need separate trusts to protect individual interests and prevent disputes among heirs.

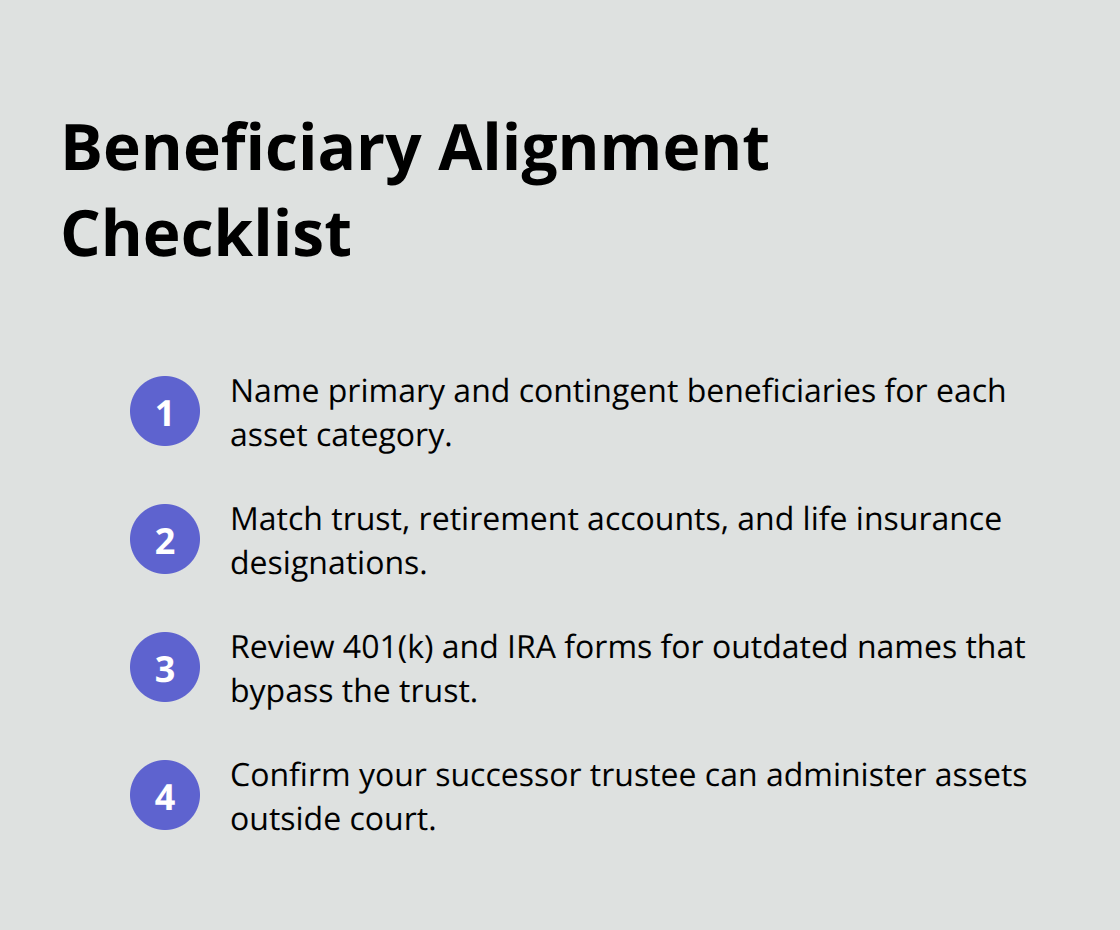

Naming Beneficiaries With Precision

Naming beneficiaries in your trust requires precision because vague language creates disputes and delays administration. You need to name primary beneficiaries for each asset category, then contingent beneficiaries in case someone dies before you do or refuses the inheritance. Retirement accounts like 401(k)s and IRAs have separate beneficiary designations outside your trust, so the person listed on those accounts overrides what your trust says, which is why many surviving spouses inherit retirement funds in ways they didn’t expect and face immediate tax bills.

A coordinated approach means your trust beneficiary designations match your retirement account designations and your life insurance beneficiaries, so everything points toward the same distribution plan. If you have children from different relationships or want to leave assets to specific people rather than your spouse, separate trusts let you control those distributions without your partner’s permission. The federal estate tax exemption of $13.99 million per person in 2025 means most couples won’t pay federal estate taxes, but state-level considerations and beneficiary coordination still matter for smooth administration and clear instructions that your successor trustee can execute without guessing your intentions.

Managing Decisions When You Cannot

A power of attorney document lets your spouse make financial decisions if you become incapacitated, and a healthcare directive lets them make medical decisions if you cannot. Many couples name each other automatically, but you need to specify exactly what authority each spouse has, whether they can act immediately or only after a doctor certifies incapacity, and who steps in if your spouse is unavailable or unwilling. These documents work outside your trust and need to align with your trust structure so your spouse can manage trust assets, pay bills from trust accounts, and make decisions about trust property without court involvement.

If you have a joint trust, your spouse already holds co-trustee authority during your life, so the power of attorney becomes a backup mechanism. Healthcare directives should name your spouse first and then identify alternate decision-makers from family or friends because your spouse might be hospitalized at the same time you are or might not want the burden of making end-of-life decisions alone. Family relationships, health status, and your preferences about medical treatment change over time, and outdated directives can override your current wishes or leave your spouse without clear authority when decisions need to happen immediately.

Aligning Your Documents for Smooth Transitions

Coordination across your trust, power of attorney, healthcare directive, and beneficiary designations prevents gaps that create confusion for your spouse. When one document contradicts another or when assets fall outside your coordinated plan, your surviving spouse faces months of untangling financial mysteries while processing grief. The next section covers the mistakes that couples make during trust administration and how to avoid them before they damage your family’s financial security.

Common Mistakes Couples Make in Trust Administration

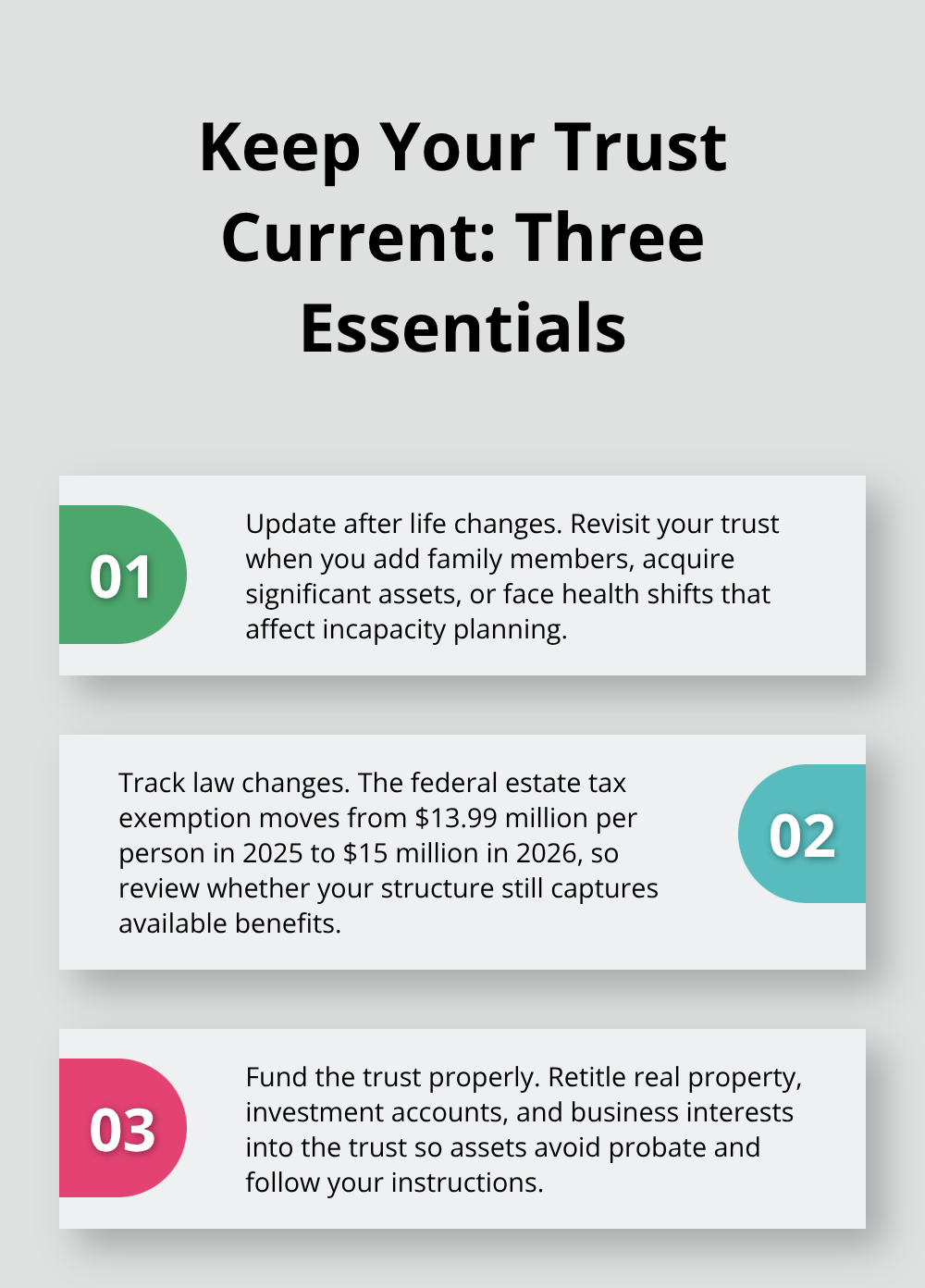

Couples create trusts with the best intentions, then life happens. A remarriage, new inheritance, or business acquisition arrives, and the original trust sits unchanged while assets accumulate outside the coordinated structure. When the first spouse dies, the surviving spouse discovers that half the estate never made it into the trust and faces probate on those assets anyway, defeating the entire purpose of the plan.

Treating Trust Creation as a One-Time Event

Trust creation is not a one-time event-it requires updates when circumstances shift. Your trust document needs revisiting whenever you acquire significant new assets, add children or grandchildren, experience a major change in net worth, or face health challenges that affect your incapacity planning. The federal estate tax exemption jumped from $13.99 million per person in 2025 to $15 million in 2026 according to the Internal Revenue Service, which means couples who have not reviewed their plans in recent years may be missing opportunities to structure their estates around these changing thresholds.

Many couples also fail to fund their trusts properly, leaving assets titled in their individual names rather than transferring them into the trust. Real property, investment accounts, and business interests all need formal transfer into the trust during your lifetime, not just mentioned in the trust document. When assets remain outside the trust, they bypass the trust entirely at death and trigger probate anyway.

Naming Different Successor Trustees

Inconsistent trustee naming creates another layer of confusion that compounds after death. One spouse might name their sibling as successor trustee while the other names their child, which means two different people suddenly have authority over different portions of the estate and may disagree about how to interpret the trust instructions or handle the surviving spouse’s needs.

If one spouse becomes incapacitated before the other, naming different successor trustees means the surviving spouse must coordinate with someone outside the marriage to manage trust assets. This slows decisions and invites conflict when quick action matters most. Alignment across both spouses’ trustee designations prevents power struggles and ensures one person can act decisively for the entire estate.

Overlooking Retirement Account Beneficiary Designations

Tax planning opportunities vanish when couples ignore the interaction between trust structure and retirement accounts. The surviving spouse who inherits a 401(k) or IRA with an outdated beneficiary designation faces an immediate tax bill because that account bypasses the trust and passes directly to whoever was named years ago. This creates a taxable event that could have been avoided with proper planning.

Spousal rollovers allow a surviving spouse to treat an inherited retirement account as their own, deferring taxes and stretching distributions. This option only works if the spouse is actually named as beneficiary on the account. Couples in blended families often overlook that a joint trust passes all assets to the surviving spouse, which means children from prior relationships may receive nothing if the surviving spouse chooses not to distribute to them later.

Protecting Children From Prior Relationships

Separate trusts protect each spouse’s intention to leave assets to their own children, but this requires both spouses to fund their trusts separately and maintain clear documentation about which assets belong to whose trust. Without this separation, the surviving spouse controls all assets and may distribute them differently than the deceased spouse intended (or not at all to stepchildren).

The coordination failures that couples make rarely show up until one spouse dies and the surviving spouse or successor trustee tries to untangle what was actually meant to happen. Assets scattered across different ownership structures, beneficiary designations that contradict trust instructions, and unclear trustee authority create months of confusion when the family needs clarity most.

Final Thoughts

Trust administration for couples succeeds when both partners align their documents before life gets complicated. Couples treat estate planning as a checkbox rather than an ongoing process, which causes the mistakes we’ve covered-outdated trusts, inconsistent trustee naming, and overlooked beneficiary designations. Your plan needs review whenever you acquire significant assets, experience major life changes, or when tax law shifts like the federal exemption increase from $13.99 million to $15 million per person between 2025 and 2026.

Start by listing all your assets and identifying which ones are actually titled in your trust versus sitting outside it. Review every beneficiary designation on retirement accounts, life insurance, and bank accounts to confirm they align with your trust instructions. Name consistent successor trustees across both spouses’ documents so one person can act decisively for the entire estate, and verify that your power of attorney and healthcare directive give your spouse the specific authority needed to manage trust assets and make medical decisions without court involvement.

The surviving spouse shouldn’t spend their grief processing financial chaos that could have been prevented. Coordinated trust administration means clear instructions, aligned documents, and assets positioned to transfer smoothly without probate delays or public disclosure. We at Law Offices of Roshni T. Desai help couples structure their estates for protection and simplicity, and we offer free consultations with flexible home or office visits so you can discuss your specific situation without pressure or complicated scheduling-contact us to start building the coordinated plan your family deserves.