Elder Law Trust Administration: Protecting Your Family’s Future

Most families put off elder law trust administration until it’s too late. By then, confusion, delays, and unnecessary costs have already taken hold.

We at Law Offices of Roshni T. Desai know that a well-structured trust protects your assets, keeps your wishes intact, and saves your family from the stress of probate court. This guide walks you through what you need to know right now.

What Trust Administration Actually Involves

The Core Tasks of Trust Administration

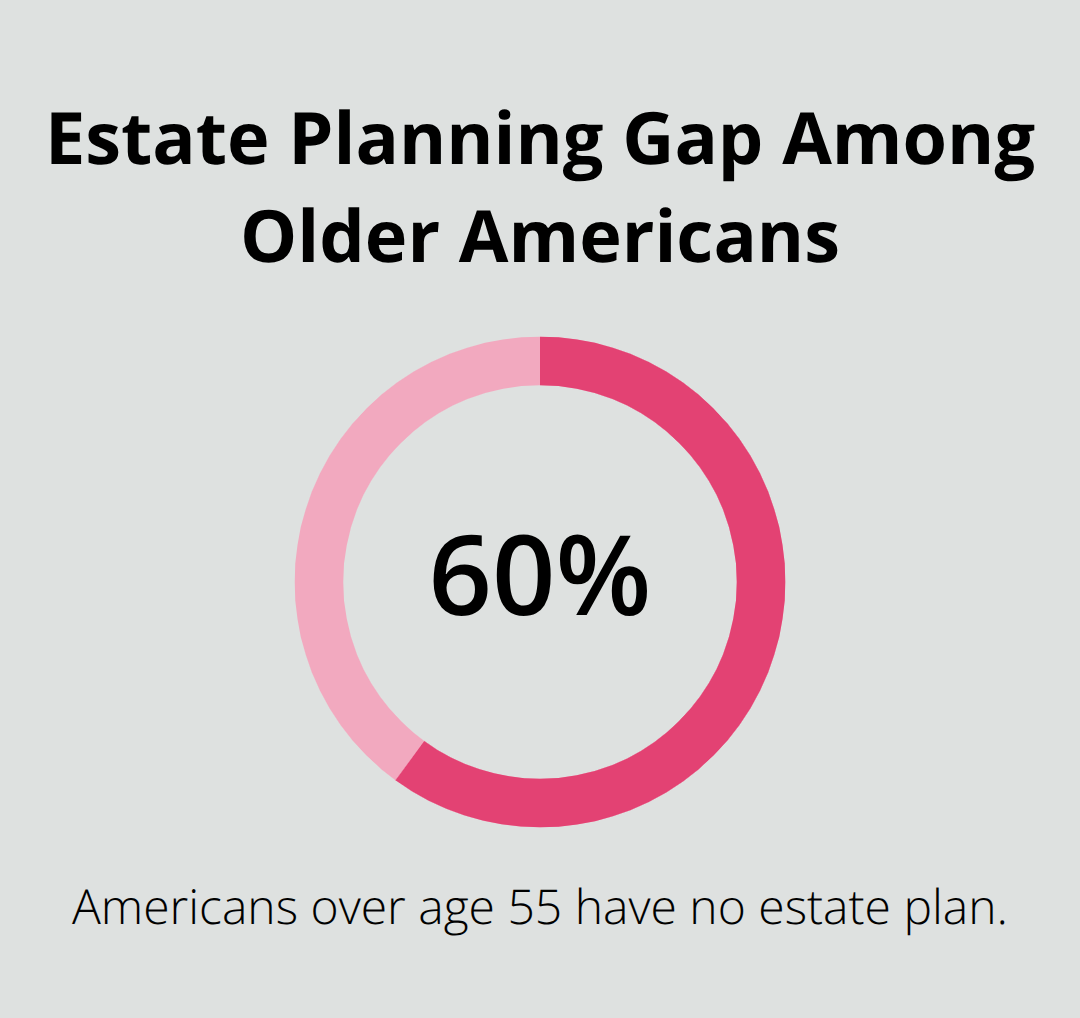

Trust administration is the operational work that happens after a trust is created. It includes identifying and inventorying all assets covered by the trust, paying outstanding debts and taxes, distributing money and property to beneficiaries according to the trust document, and filing necessary paperwork with the court or tax authorities. Someone-usually called a trustee-manages these tasks over months or sometimes years. The AARP reports that 60% of Americans over age 55 have no estate plan at all, which means when these families need trust administration, they often start from scratch under time pressure.

The trustee’s job is concrete: locate bank statements, deed records, investment accounts, and insurance policies; obtain death certificates; notify beneficiaries in writing; calculate what taxes are owed; and distribute assets on a timeline that protects everyone’s interests. If the trust holds real estate, the trustee may need to handle property management, repairs, or sales. If there’s a family business, the trustee might need to continue operations or arrange a sale.

Why This Matters Beyond Paperwork

When aging parents haven’t set up a trust, their children face probate court, which is slow and expensive. The American Bar Association estimates that probate can take 12 to 18 months and consume 3% to 7% of an estate’s value in fees and costs. A trust avoids this entirely. Families also avoid the emotional burden of fighting in court over assets or having a judge decide who gets what.

This work demands attention to detail because mistakes cost money-sometimes thousands of dollars in penalties, taxes, or legal fees to fix.

Common Mistakes That Derail Families

Trustees often fail to update beneficiary information when life changes, delay distributing assets because they’re unsure of their authority, or miss tax deadlines that trigger penalties. Some families name a trustee with no financial knowledge, then that person struggles to manage investments or understand tax obligations. Others create a trust but never actually transfer assets into it-the trust sits empty while property stays in the person’s individual name, defeating its purpose.

These mistakes happen because families treat trust administration as a one-time event rather than an ongoing responsibility. The solution requires two actions: work with someone who understands these moving parts before a crisis forces rushed decisions, and update your plan whenever major life events occur (a marriage, divorce, birth of a grandchild, or significant change in assets). This foundation sets the stage for what happens next-understanding how trusts actually protect your family’s assets and wishes.

How Trusts Protect Your Assets and Keep Control in Your Hands

Moving Assets Out of Your Name

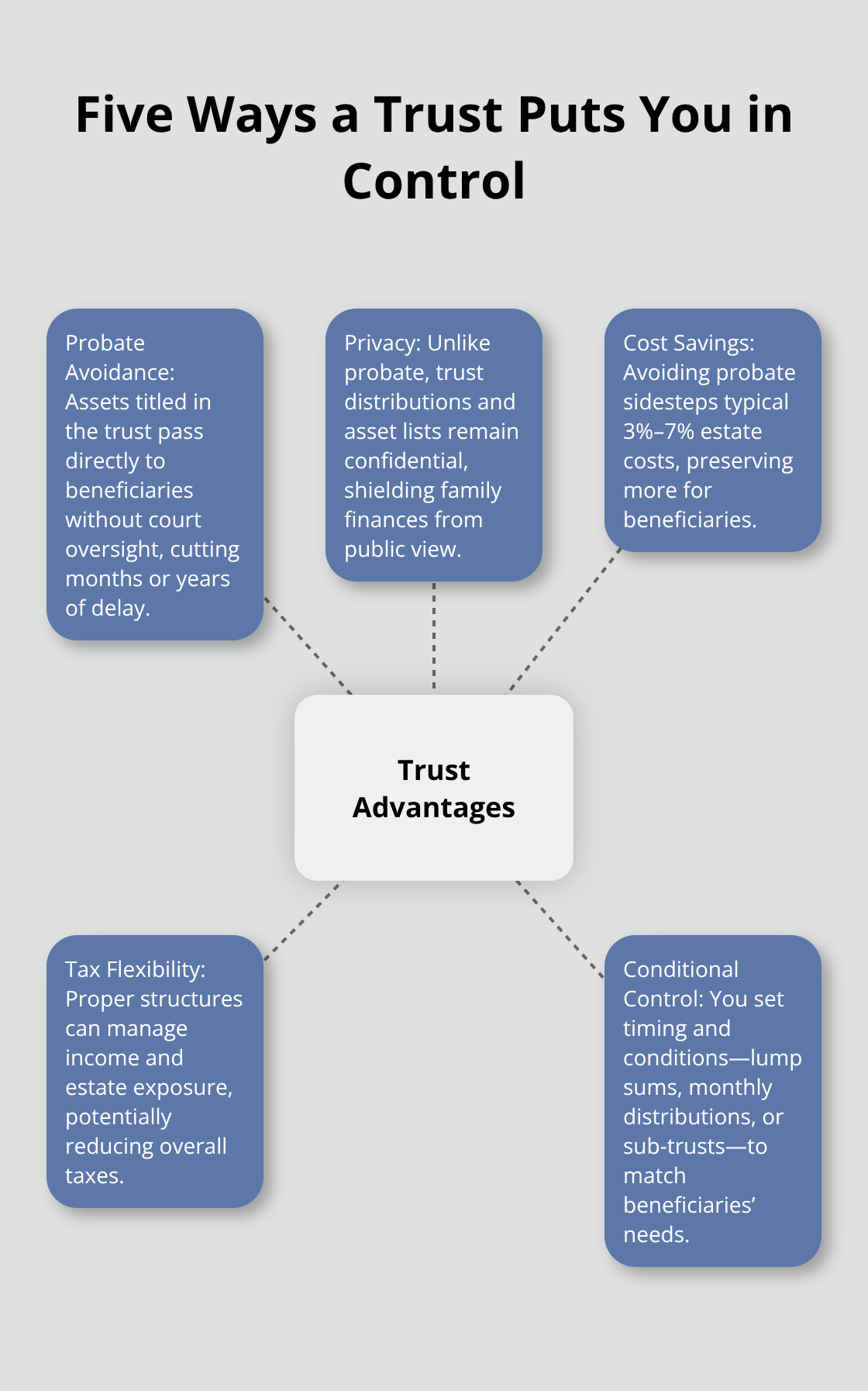

A trust works because it moves assets out of your individual name and into a legal structure that bypasses probate entirely. When you die, property titled in your trust transfers directly to beneficiaries without court involvement, no waiting period, and no public record of what you owned or who inherited it. This shift from individual ownership to trust ownership changes everything about how your estate settles.

The Privacy Advantage

Probate documents become public record, meaning anyone can walk into a courthouse and see your bank balances, real estate holdings, investment accounts, and who received them. A trust keeps all of this confidential. Your family’s financial information stays private, and your beneficiaries’ identities remain protected from creditors, distant relatives, or anyone else who might have financial motives to contact them.

Real Cost Savings

The average probate case costs 3% to 7% of your estate’s value in legal fees, court costs, and administrative expenses, according to the American Bar Association. For a $500,000 estate, that amounts to $15,000 to $35,000 in unnecessary costs that your family never sees. A properly funded trust eliminates these expenses almost entirely, leaving more money for the people you care about.

Tax Advantages When Structured Correctly

Federal estate tax applies to estates exceeding $13.61 million in 2024, but state-level taxes kick in at much lower thresholds. A trust structured correctly can split income across multiple taxpayers, reducing the overall tax hit. This requires knowing whether to use a revocable or irrevocable trust, and which assets belong inside the trust versus outside it. Most families get this wrong without guidance, costing thousands in preventable taxes.

Control That a Will Cannot Provide

The strongest reason to use a trust is control. A will tells a probate judge what you want, and the judge decides whether to grant it. A trust is a binding agreement that controls exactly what happens to your assets, when, and under what conditions. You can specify that a grandchild’s inheritance goes into a sub-trust until age 30, protecting them from their own poor decisions. You can direct that a struggling adult child receives monthly distributions rather than a lump sum, preventing them from depleting the money in months. You can name successor trustees so your wishes continue even if the first trustee becomes unable to serve.

You can protect assets from creditors or divorcing spouses through spendthrift language that restricts how beneficiaries access funds. A will offers none of this control once you’re gone.

The trustee you name has clear authority to act immediately after your death without waiting for court approval, meaning bills get paid, property gets managed, and beneficiaries receive their inheritances within months rather than years. This immediate action prevents the long delays that plague probate cases. As your circumstances shift-marriages happen, children are born, assets grow-your trust needs to shift with them. The next section shows you how to keep your trust aligned with your actual life.

When Life Changes, Your Trust Must Too

Life Events That Demand Immediate Action

Your trust is not a document you create once and forget. The moment a grandchild is born, you remarry, you sell your business, or you acquire significant new property, your trust becomes outdated. Life moves faster than most people’s estate plans, and that gap creates real problems. The Certified Financial Planner Board reports that 60% of people who have a trust never update it after creation, leaving their actual wishes out of sync with their legal documents.

A marriage or divorce alone demands immediate attention. Your former spouse may still be named as a beneficiary or successor trustee in your original trust, meaning they could inherit assets or control distributions you never intended them to have. A child who struggled with addiction ten years ago but is now thriving may no longer need the restrictive spendthrift provisions you originally included, while a different child’s financial recklessness might justify adding those same protections.

Property and Business Changes Require Trust Updates

Adding a new property requires the deed to be transferred into the trust’s name-otherwise that property goes through probate anyway, defeating the entire purpose of having a trust. New business interests, whether you started a company or received an ownership stake, need specific language in your trust about how that asset transfers, whether it sells, and who has authority to make those decisions.

When you own real estate in multiple states, those property transfers into and out of your trust require coordination with local recording offices. Miss this step and your out-of-state property still goes through probate in that state. If you operate a family business, the trust needs language addressing what happens to your ownership stake, whether the business continues, who has authority to sell it, and how the sale price gets distributed.

The Cost of Updating Versus the Cost of Fixing

When a trustee tries to follow an outdated trust, they either make decisions that contradict your real intentions or they face legal challenges from beneficiaries who claim the trustee acted wrongly. A trust amendment typically costs a few hundred dollars, while litigation over an outdated or ambiguous trust can consume tens of thousands in legal fees and court costs.

A trustee without clear guidance might liquidate a thriving business at a fraction of its value just to distribute cash to beneficiaries quickly, or they might freeze the business in operation indefinitely because they lack authority to sell. These details matter because the wrong decision can destroy years of work and wealth you built.

Keeping Your Trust Aligned With Your Life

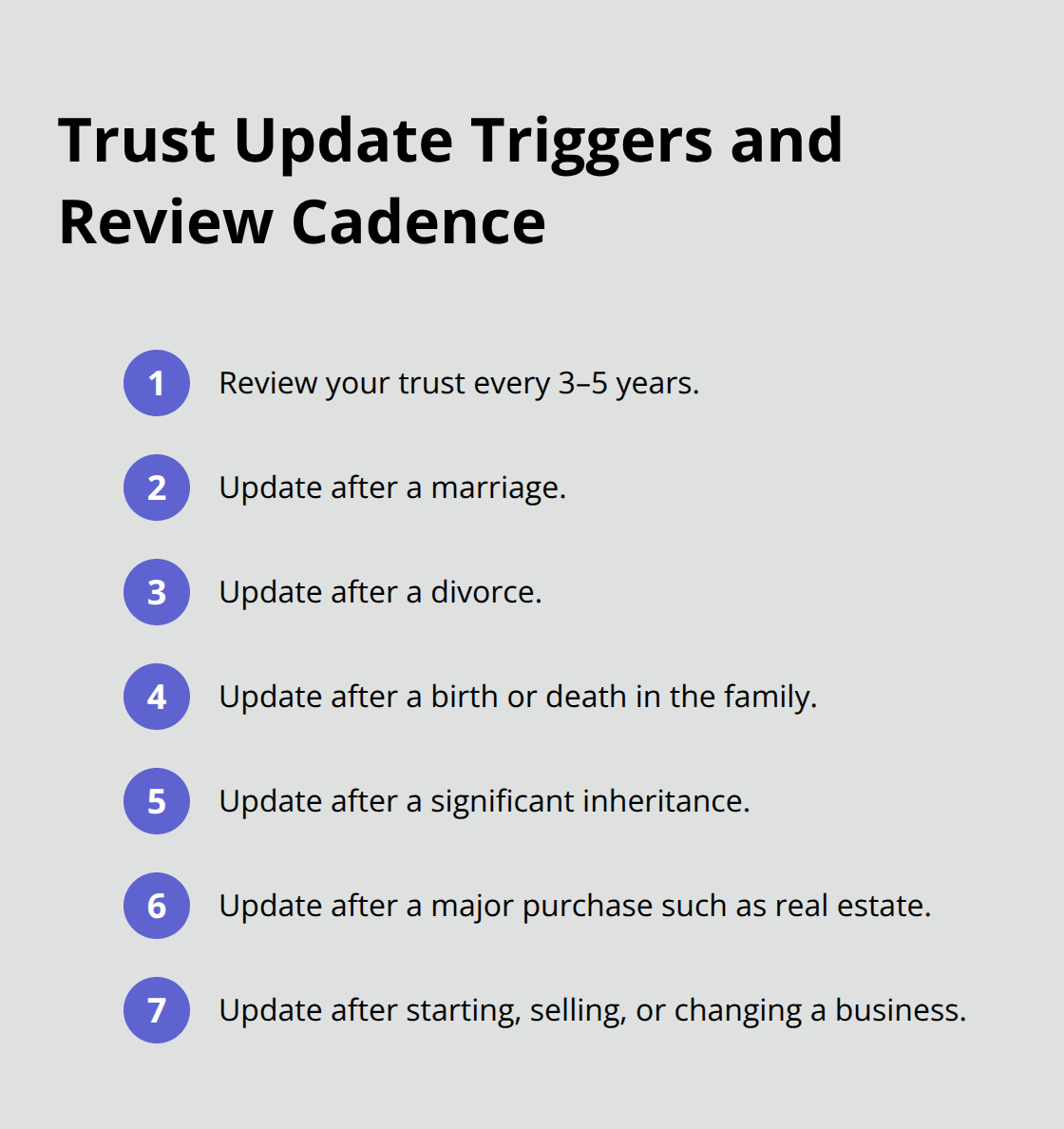

Try scheduling a review every three to five years, or immediately after any major life event like a marriage, divorce, death in the family, significant inheritance, major purchase, or business change. During that review, work with someone who understands both your trust document and your current circumstances to identify which sections need updating.

Some changes are minor-updating a beneficiary’s address or changing a successor trustee-while others require substantial revisions to how assets distribute or who controls them. A trust created before you had children looks completely different from one created after, and a trust created when your net worth was $300,000 may need restructuring now that it’s $2 million. The trustee you named fifteen years ago may have moved away, developed health problems, or simply lost the capacity to manage complex financial decisions-naming a successor trustee proactively prevents chaos when your primary trustee can no longer serve.

Final Thoughts

A well-structured trust stops probate delays, protects your family’s privacy, and keeps your wishes intact when you’re no longer here to enforce them. Elder law trust administration requires attention to detail, but it’s the difference between your family inheriting assets within months versus years. Your actual intentions stay intact rather than a judge deciding what happens to your life’s work.

Three core takeaways matter most. First, a trust only works if you actually transfer assets into it-an empty trust sitting in a drawer protects nothing. Second, your trust must change when your life changes, whether that’s a marriage, a new property, a business sale, or a shift in who you want to benefit. Third, the trustee you name carries real responsibility, so choose someone with financial competence and the willingness to act decisively when the time comes.

We at Law Offices of Roshni T. Desai help families across Southern California build and maintain trusts that actually work. With over 25 years of experience in estate planning and trust administration, we understand the details that most families miss. Contact us for a free consultation to discuss your specific situation without pressure or complicated logistics.