What probate administration explained means for heirs

When a loved one passes away, probate administration explained can feel overwhelming for heirs who don’t understand the process. The court system, legal paperwork, and financial obligations involved often catch families off guard.

At Law Offices of Roshni T. Desai, we’ve seen how confusion about probate costs heirs thousands of dollars in missed deadlines and poor decisions. This guide breaks down what actually happens during probate and how it impacts your inheritance.

What Actually Happens During Probate Administration

Probate administration is the court-supervised process where an executor or administrator takes control of a deceased person’s assets, pays debts and taxes, and distributes what remains to heirs. The executor named in the will (or an administrator appointed by the court if there’s no will) becomes the personal representative with legal authority to act on behalf of the estate. This person must file the will with the probate court, prove its validity, and receive official letters testamentary or letters of administration within the first three to four months after death. The executor’s fiduciary duty is serious-they must act in the estate’s best interest, maintain accurate records, prevent asset losses, and comply with all court orders. Many executors hire attorneys and accountants to handle the complexity, and they receive reasonable compensation for their work, though those who will inherit may decline payment. The probate court oversees the entire process to protect beneficiaries and creditors, issuing orders at key stages and approving the final accounting before the estate closes. In informal probate states that follow the Uniform Probate Code, the process involves mainly paperwork with minimal court involvement when there are no disputes.

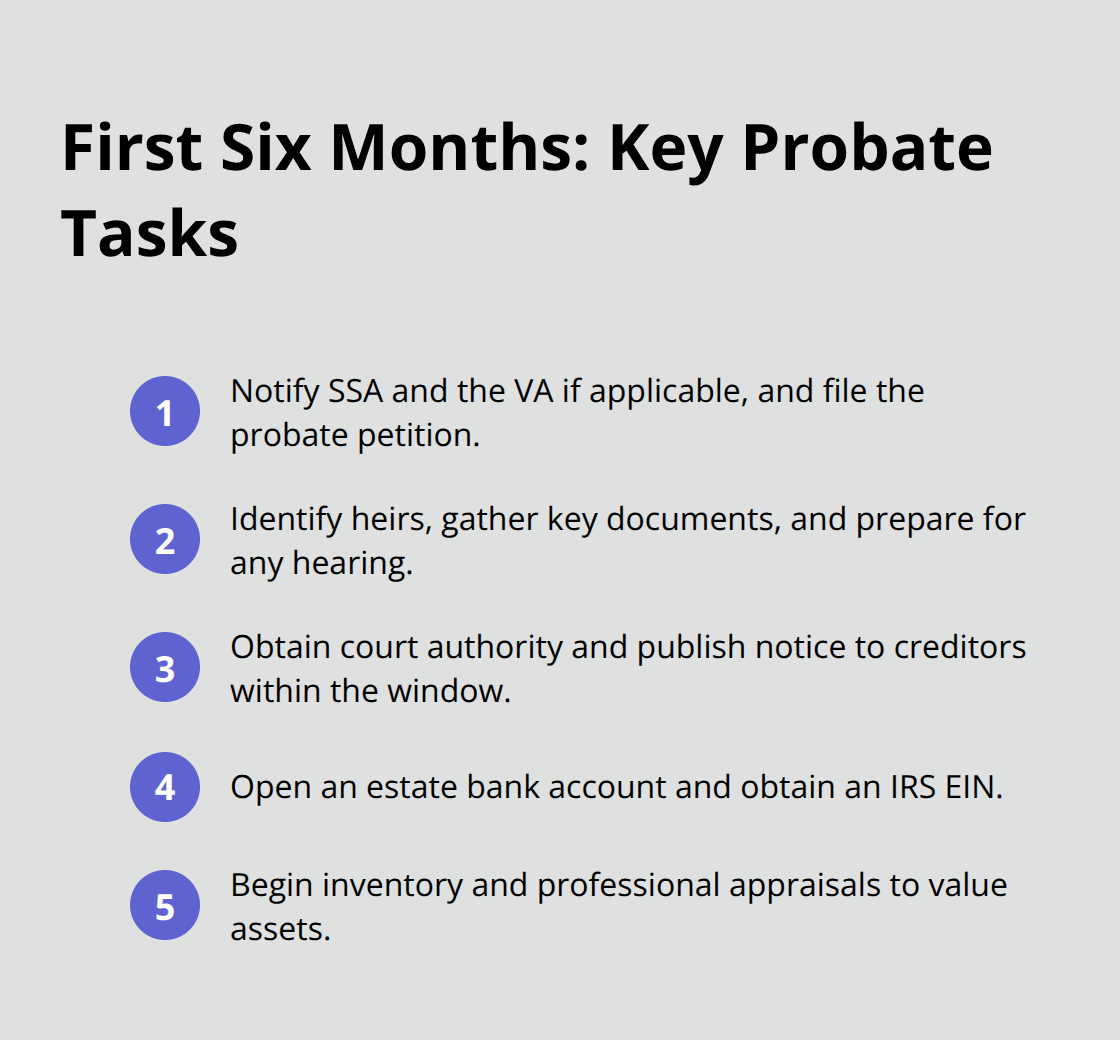

Critical Early Steps Within the First Six Months

Within one to four months of death, you must notify the Social Security Administration, the Department of Veterans Affairs if applicable, and file a petition for probate with the court. The executor needs to identify all heirs and beneficiaries, gather important documents, and prepare for any required court hearing. Between months three and six, the court issues authority documents, an estate bond may be required, and the executor must publish notice to creditors and provide formal notice to heirs-this creditor notification period typically lasts three to four months, during which claims must be filed or they’re barred. The executor opens an estate bank account and obtains an EIN from the IRS during this window to prevent commingling personal and estate funds.

The executor also begins inventorying and appraising all assets, which can require professional valuations for real estate, businesses, or specialized items. Delays in these early steps directly extend the entire timeline, so acting promptly protects the estate and speeds distribution.

Asset Distribution and Final Closure Between Months Seven and Twenty-Four

From month six onward, the executor pays debts, taxes, and administrative costs in a statutory order while collecting rents or insurance proceeds. Between months seven and fifteen, the executor presents heirs with a final accounting and files a petition for final distribution-this accounting must detail every transaction and receive court approval. The executor obtains tax clearance letters from the IRS to confirm no outstanding tax liabilities exist for the estate. A hearing on the final distribution petition typically occurs between months eight and sixteen, and once the court approves the order, the executor distributes remaining assets to beneficiaries. Real property requires deed transfers, and all beneficiaries must provide signed releases before the estate fully closes. Simple estates often finish within nine to twelve months, while complex ones with multiple properties, disputes, or tax issues can stretch to eighteen or twenty-four months. Court backlogs and creditor claims are the most common reasons probate extends beyond the typical timeframe, so maintaining clear communication with the court and addressing claims promptly keeps the process moving. Understanding these timelines helps heirs anticipate what comes next and recognize when complications may require professional guidance to protect their inheritance.

How Your Inheritance Shrinks During Probate

The moment probate begins, your inheritance starts getting smaller. The executor identifies every asset the deceased owned, has them professionally valued, pays all debts and taxes from the estate, and only then distributes what remains to heirs. Understanding exactly what happens to your money during this process prevents costly surprises.

Probate Costs Eat Into Your Estate

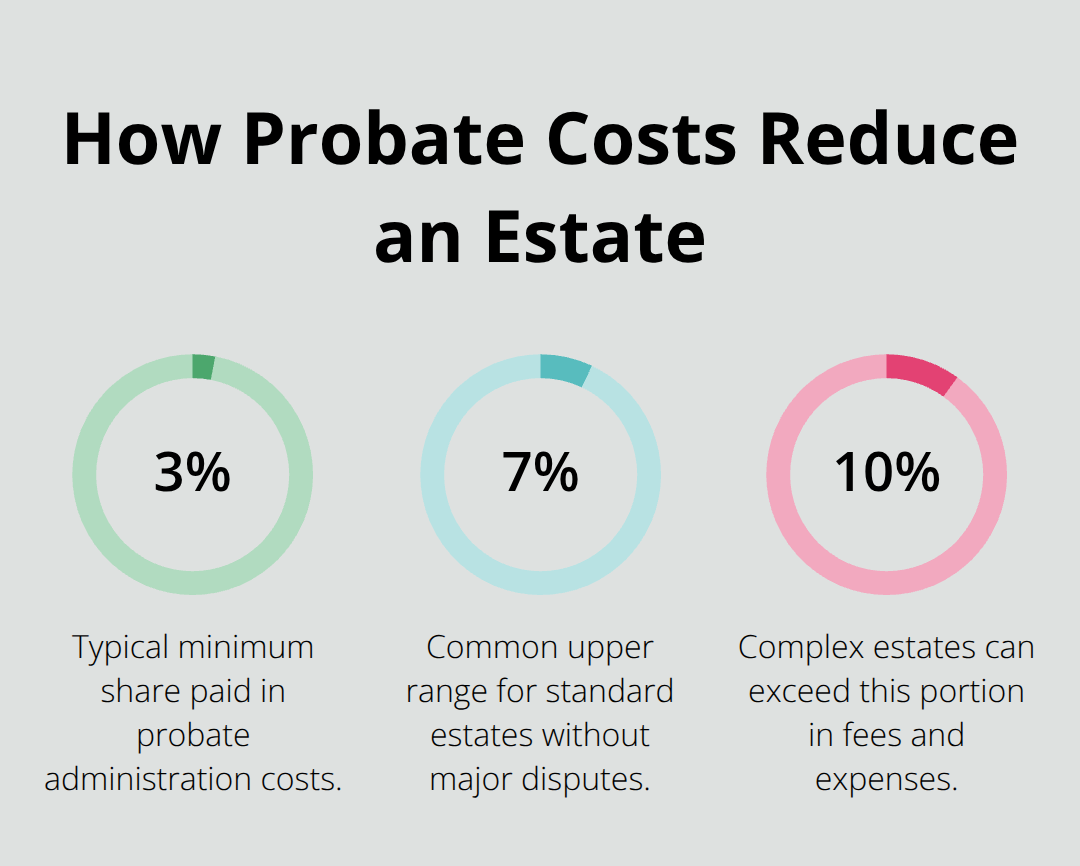

Probate administration typically costs between 3% and 7% of the estate’s total value according to industry data, though complex estates with multiple properties or disputes can exceed 10%. Court filing fees, attorney fees, executor compensation, professional appraisals, accounting services, and publication notices all drain the estate. A $500,000 estate in California loses $15,000 to $35,000 in probate costs alone before heirs receive a single dollar.

The executor must hire professionals to value real estate, artwork, business interests, and other specialized assets. Appraisals for a single property typically run $300 to $1,000, and estates with multiple properties require multiple appraisals. The executor pays these bills from estate funds immediately, not after distribution, which means the remaining amount available for heirs shrinks throughout the probate timeline.

Debts and Taxes Create the Largest Reduction

Debts and taxes create the largest reduction in what heirs actually receive. The executor must pay all outstanding debts in a specific statutory order: funeral expenses and probate administration costs first, then creditor claims, then taxes. Federal estate taxes apply to estates exceeding $13.61 million in 2024, but California has no state estate tax, so most California heirs avoid federal estate tax unless the estate is exceptionally large.

The estate must file a final income tax return and pay any income taxes owed on earnings generated during probate administration. Credit card debts, medical bills, mortgage obligations, and property taxes must all be paid before heirs receive anything. If the estate owes $200,000 in debts and taxes but only contains $300,000 in assets, heirs receive roughly $100,000 total.

Real Estate Complications Add More Expenses

Real estate often complicates this timeline because it may need to be sold to generate cash for debts and taxes. Real estate agent commissions (typically 5% to 6%) and closing costs add to the list of expenses reducing the estate. The executor typically completes debt payment and tax filing between months six and fifteen, which means heirs cannot access their inheritance until these obligations are satisfied and the court approves the final accounting.

What Heirs Should Know About Their Accounting

The executor presents heirs with a final accounting that details every transaction and expense. Ask the executor for a detailed accounting of all debts, taxes, and expenses in writing so you understand exactly why your inheritance is smaller than expected. This accounting becomes the foundation for the court’s approval of the final distribution, and heirs who review it carefully can identify errors or questionable expenses before the estate closes.

These financial reductions happen before distribution occurs, which is why many heirs face unexpected shortfalls. The next section examines the specific mistakes executors make that compound these losses and delay when heirs actually receive their inheritance.

Mistakes That Drain Your Inheritance Before Distribution

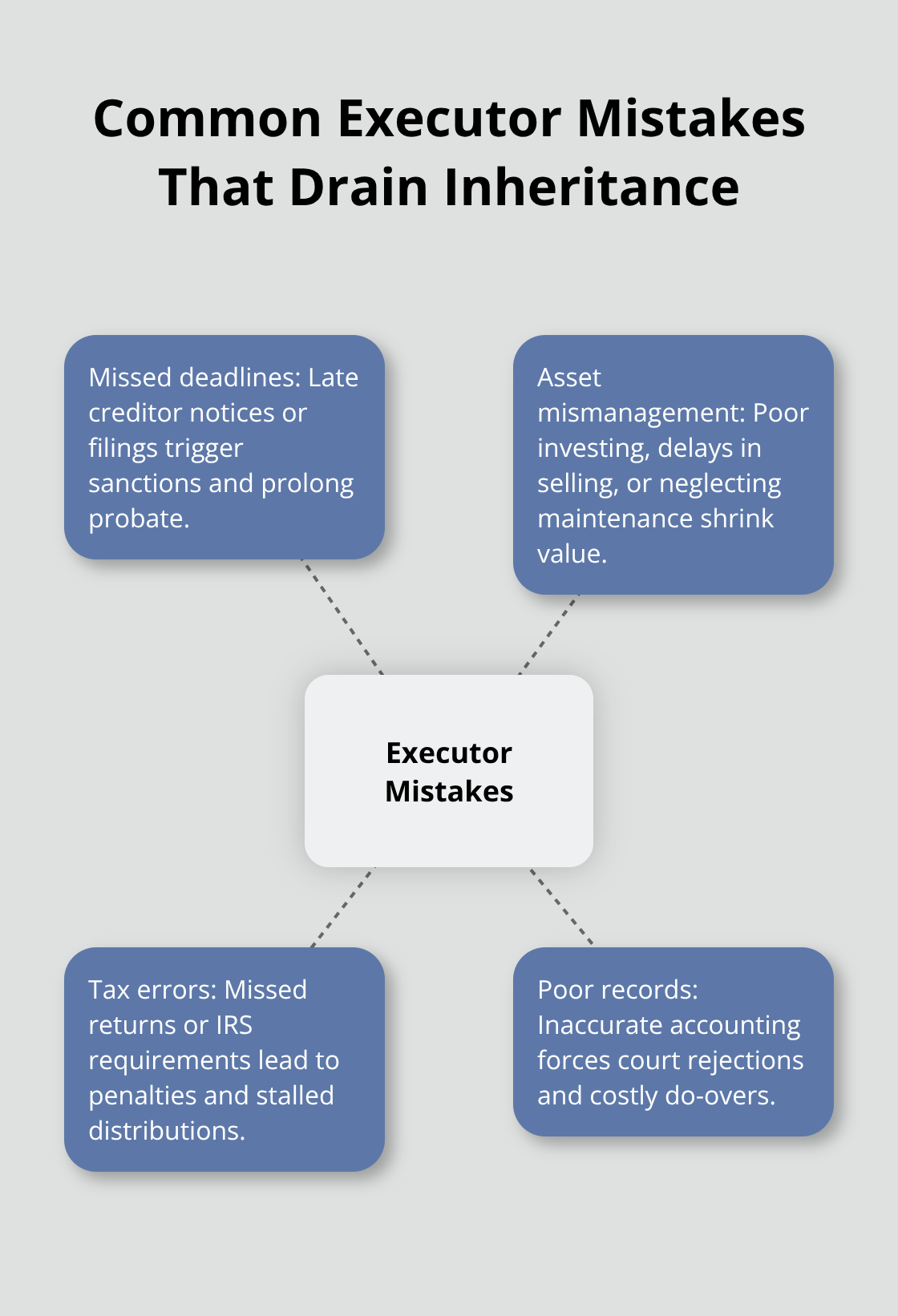

Executors make predictable errors that extend probate timelines and shrink what heirs actually receive. Missing filing deadlines triggers court sanctions and creditor claims that could have been prevented. Mishandling assets during administration creates liability that executors must pay from personal funds, not the estate. Ignoring tax deadlines costs heirs thousands in penalties and interest that accumulate monthly.

Missing Critical Filing Deadlines

These aren’t theoretical problems-they happen regularly and cost families real money. When executors miss the creditor notification deadline in month three, claims filed after that deadline still get paid, which extends probate by months. If an executor fails to publish notice to creditors or provide formal notice to heirs within the required window, creditors can pursue claims outside the normal probate process, forcing the executor to defend against lawsuits instead of closing the estate.

One common mistake occurs when executors delay opening an estate bank account and comingle personal and estate funds. This creates accounting nightmares during the final accounting and sometimes triggers IRS audits. Executors who don’t obtain an EIN from the IRS or file the estate’s income tax return by the deadline face penalties that reduce distributions by hundreds or thousands of dollars depending on estate earnings.

Another costly error happens when executors delay the estate inventory and appraisal-waiting until month nine or ten to value assets means the executor doesn’t know what debts can actually be paid. This leads to incomplete accounting and court rejection of the final distribution petition.

Mismanaging Assets and Property

Mismanaging estate assets occurs when executors invest estate funds improperly, fail to collect rent or insurance proceeds on time, or allow real estate to deteriorate without maintenance or repairs. An executor who delays selling real estate while the market declines directly reduces what heirs receive, yet some executors wait months before listing property.

Real estate requires active management during probate. Property taxes continue accruing during administration, and unpaid taxes can result in liens against real estate that complicate sales and delay distribution. The executor must maintain the property, address necessary repairs, and monitor market conditions to maximize sale proceeds.

Tax Obligations and Professional Guidance

Tax obligations create the largest mistakes because executors who don’t consult a tax professional often miss deadlines for filing the estate’s fiduciary income tax return, federal estate tax returns if applicable, or property tax payments on real estate held during probate. The executor must file the final income tax return for the estate and obtain a tax clearance letter from the IRS before the court approves final distribution-missing this step means the probate case remains open and heirs cannot receive their inheritance.

Seeking professional guidance on tax obligations rather than attempting this alone typically costs $1,500 to $3,000 and prevents penalties that would cost far more. This professional investment protects the estate and accelerates the timeline significantly.

Creditor Claims and Record-Keeping

Executors who ignore or mishandle creditor claims face personal liability if they distribute assets to heirs before verifying claims, because creditors can pursue the executor personally to recover amounts owed by the estate. The executor’s duty to maintain accurate records and present a detailed final accounting cannot be overstated-executors who keep poor records face court rejection of their accounting and must redo the entire process at additional cost and delay.

Final Thoughts

Probate administration explained means understanding that the process protects creditors and heirs through a structured legal framework, but it also costs time and money that directly reduces your inheritance. The executor’s fiduciary duties are serious, and mistakes in filing deadlines, asset management, or tax obligations create personal liability that extends probate and shrinks distributions. You now understand that probate typically takes nine to twenty-four months depending on complexity, that costs range from 3% to 7% of estate value, and that debts and taxes are paid before heirs receive anything.

When real estate is involved, family disputes exist, or the estate exceeds $300,000 in value, professional guidance becomes essential rather than optional. An attorney can address creditor claims efficiently, ensure tax deadlines are met, and prevent costly errors that would otherwise delay distribution by months or years. The investment in professional help typically costs $1,500 to $3,000 and prevents penalties and mistakes that cost far more.

We at Law Offices of Roshni T. Desai provide personalized probate administration services across Southern California. Whether you’re an executor managing an estate or an heir concerned about your inheritance, contact us early to prevent the mistakes that cost families thousands of dollars. The probate process moves forward more smoothly when someone guides you through each deadline and requirement, protecting both the estate and your interests until distribution is complete.