Irrevocable Trust Attorney: Securing Your Non-Revocable Plans

An irrevocable trust is one of the most powerful estate planning tools available, but it’s also one of the most misunderstood. Once you transfer assets into this type of trust, you cannot change your mind or take them back.

We at Law Offices of Roshni T. Desai help clients navigate irrevocable trust decisions every day. This guide walks you through what these trusts do, why they matter, and the mistakes that can derail your plans.

What Irrevocable Trusts Actually Are

An irrevocable trust is a legal structure where you transfer ownership of your assets to a trustee who then manages them for your beneficiaries. Once the transfer happens, you cannot reclaim those assets or modify the trust terms without permission from all beneficiaries and a court order-a reality that separates irrevocable trusts from their revocable counterparts. The key characteristic is permanence. When you establish a revocable trust, you retain control and can change or cancel it whenever you want. An irrevocable trust removes that flexibility entirely. The trade-off is substantial: you lose direct control over the assets, but in return, those assets exit your taxable estate, shield themselves from creditors, and can qualify you for Medicaid benefits more quickly. The Tennessee Uniform Trust Code makes this distinction clear-alterations to an irrevocable trust require exceptional court approval, whereas a revocable trust stays under your command during your lifetime.

The Mechanics of Asset Movement

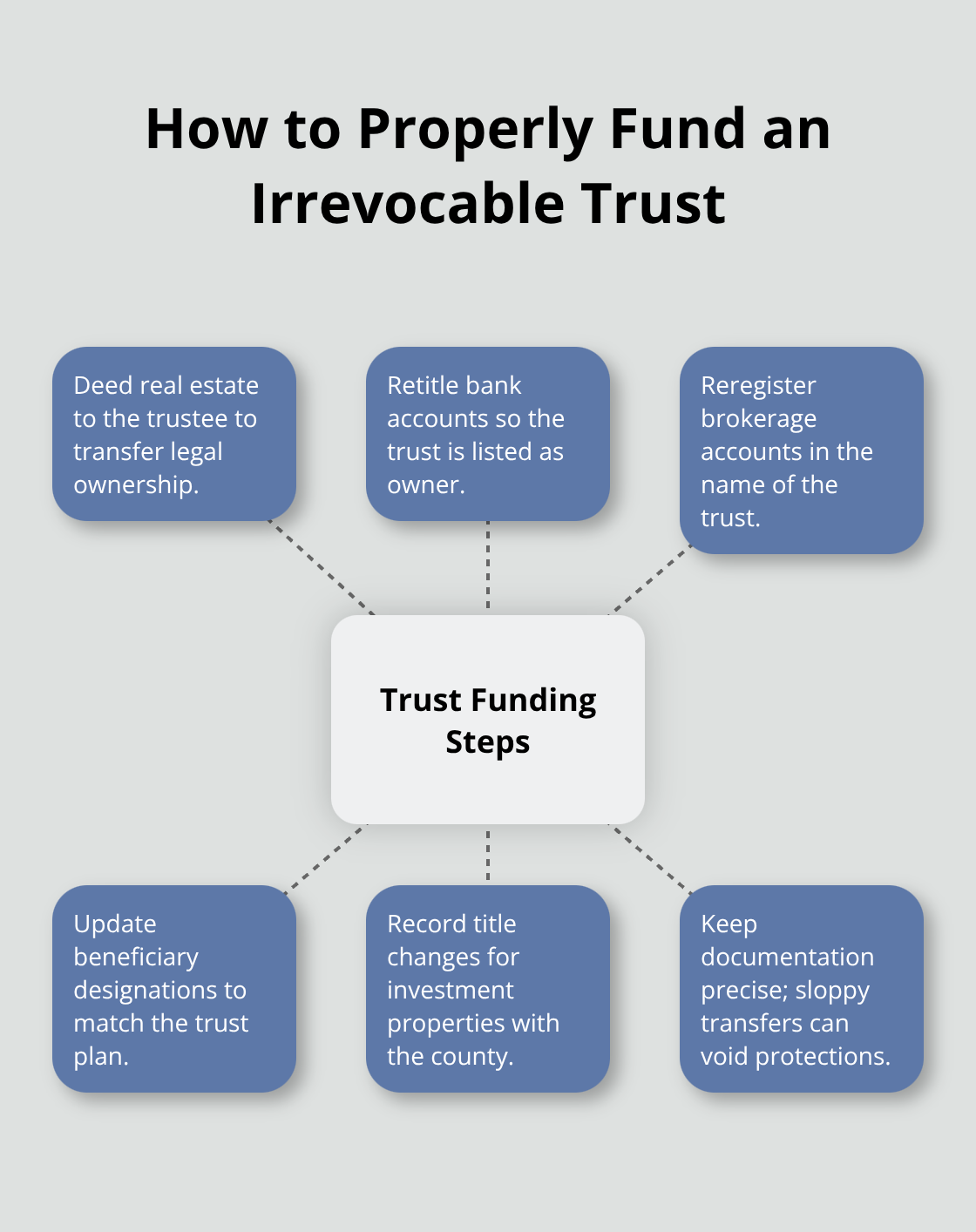

When you fund an irrevocable trust, the assets technically stop being yours. This isn’t a minor technical detail; it’s the foundation of why the trust works. If you own a home worth $500,000 and transfer it into an irrevocable trust, that home no longer appears in your personal estate for tax purposes. For Medicaid planning in Tennessee, this distinction matters tremendously because assets in an irrevocable trust don’t count against the resource limits that determine TennCare eligibility. A Nashville couple placed their retirement savings into an irrevocable trust while maintaining income distributions, which allowed them to qualify for Medicaid coverage for long-term care without liquidating their entire nest egg. The process requires precise documentation-sloppy transfers can invalidate the trust’s protections. You must formally deed property, retitle accounts, and update beneficiary designations. Many people fail at this stage because they create the trust document but never actually move assets into it, leaving themselves with no protection whatsoever.

Why Timing Changes Everything

Establishing an irrevocable trust early matters more than most people realize. Medicaid rules include a five-year lookback period, meaning assets transferred within five years of applying for benefits may disqualify you from coverage. A Franklin widow who waited until she needed nursing home care discovered she couldn’t protect her home through an irrevocable trust because she’d missed the window. Those who plan ahead avoid this trap entirely. The trust also works differently for different assets. Retirement accounts like IRAs don’t belong in irrevocable trusts because the tax consequences become punitive-you’d trigger immediate distributions and tax bills that defeat the purpose. Real estate, savings accounts, and investment properties work well. Life insurance fits perfectly into a specialized irrevocable structure called an ILIT, which removes death benefits from your taxable estate and can reduce federal estate taxes significantly for high-net-worth families.

Understanding the Limits of Permanence

The permanence of an irrevocable trust isn’t absolute. Decanting allows you to transfer assets to a new trust with revised terms if state law permits, and courts can approve modifications under specific circumstances. These exceptions are narrow and expensive. The practical reality is that once you commit assets to an irrevocable trust, that commitment sticks. Understanding what assets work best and what timing means for your situation requires careful analysis of your specific goals and state law requirements. This is where professional guidance becomes invaluable-the wrong structure or the wrong timing can cost you thousands in lost tax benefits or Medicaid eligibility.

Why Irrevocable Trusts Cut Your Tax Bill and Shield Your Assets

Estate Tax Reduction Through Asset Removal

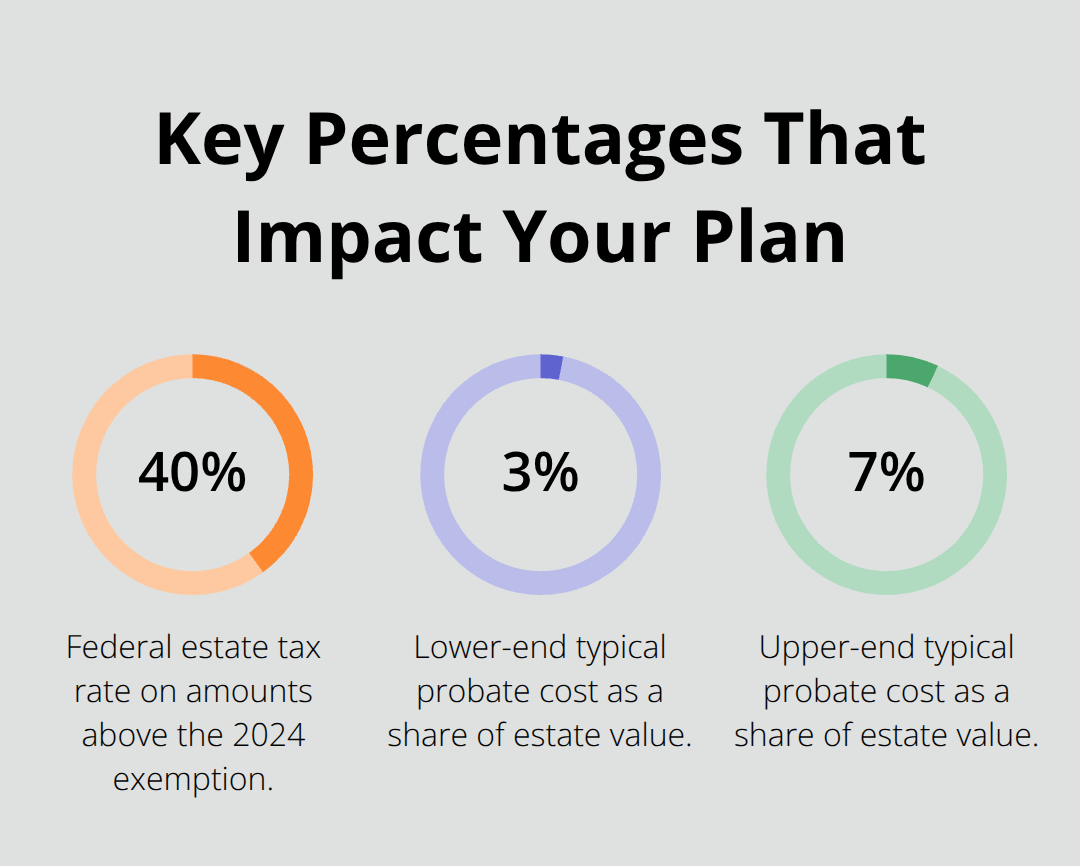

An irrevocable trust removes assets from your taxable estate immediately, and that reduction translates directly into lower federal estate taxes. If your estate exceeds $13.61 million in 2024, federal estate tax kicks in at 40% on the overage-meaning a $15 million estate would face $560,000 in federal tax without planning. Transferring $2 million into an irrevocable trust reduces your taxable estate to $13 million and eliminates that tax exposure entirely.

The IRS has no claim on assets you’ve transferred into an irrevocable trust because legally, you no longer own them.

High-net-worth families use irrevocable trusts as a cornerstone of their strategy for this reason alone. The trust structure accomplishes what individual ownership cannot: it severs the IRS’s connection to your wealth while you remain alive to see the benefit.

Creditor Protection and Liability Shielding

Beyond taxes, the trust creates a creditor-proof wall around your assets. If you face a lawsuit, medical judgment, or business liability, creditors cannot reach funds inside an irrevocable trust because you don’t own them anymore. A doctor or attorney can transfer investment property or savings into an irrevocable trust and gain genuine protection against malpractice claims or other claims that might otherwise deplete their life savings.

This protection works because the trust is a separate legal entity-your creditors have no legal claim against assets held in someone else’s name, even if that someone is a trustee managing assets for your benefit. The separation is absolute and enforceable.

Medicaid Eligibility and Long-Term Care Planning

Medicaid planning represents the most practical reason most families establish an irrevocable trust. Long-term care costs between $100,000 and $200,000 annually depending on location and care level, and TennCare in Tennessee covers these costs only if your assets fall below the resource limit of approximately $2,000 for individuals. An irrevocable trust removes assets from this calculation.

A widow in her sixties can transfer her home and investment accounts into an irrevocable trust, maintain income distributions for living expenses, and five years later qualify for Medicaid coverage without losing her home or depleting her savings. The five-year lookback period matters critically-assets transferred within five years of applying for benefits may trigger a penalty period that delays coverage. This means planning cannot wait until you need care; it must happen years in advance.

Probate Avoidance and Faster Asset Distribution

Probate avoidance operates differently but delivers substantial value. When you own assets in your individual name, your estate must go through probate after death, a process that typically costs 3% to 7% of your estate value and takes six months to two years. Assets held in an irrevocable trust bypass probate entirely because the trustee distributes them according to the trust terms-no court involvement, no delays, no public disclosure of your financial details.

Your beneficiaries receive their inheritance faster, and your family avoids the emotional burden and expense of court proceedings. The trustee’s authority to act immediately (rather than waiting for court approval) accelerates the entire process and reduces professional fees substantially. These benefits compound when you combine irrevocable trusts with proper titling of real estate and beneficiary designations on accounts. The coordination between these tools creates a seamless transfer mechanism that protects your wealth while honoring your wishes. Understanding which assets belong in an irrevocable trust and which do not determines whether you capture these benefits or miss them entirely-a distinction that separates effective planning from costly mistakes.

Where Your Irrevocable Trust Fails Before It Starts

Creating an irrevocable trust document and actually transferring assets into it are two completely different things. Families spend thousands drafting a trust, then never move the assets that need protection into it. The trust sits dormant while their home, investment accounts, and savings remain in their personal name-vulnerable to creditors, exposed to probate, and counting against Medicaid resource limits.

The Funding Gap That Destroys Protection

Funding means formally retitling assets. A house requires a new deed that transfers ownership to the trustee. Bank accounts need new signatures and account registrations showing the trust as owner. Brokerage accounts must be reregistered. Investment properties need title changes recorded with the county. Each step matters because incomplete transfers leave gaps.

A widow who transferred her home into an irrevocable trust but never updated her bank account titles left half her assets unprotected. When she needed Medicaid coverage, those liquid assets disqualified her from benefits. The five-year lookback period also creates a timing trap that catches people off guard. If you transfer assets within five years of applying for Medicaid, Tennessee’s TennCare program imposes a penalty period that delays or denies coverage. Someone who waits until age 75 to establish protection and then applies for benefits at 77 loses everything because their timing was two years too late.

Retirement accounts compound the error because IRAs and 401(k)s should never go into irrevocable trusts. The tax consequences trigger immediate distributions and create bills that defeat the entire purpose of planning.

The Permanence Problem

Not understanding what irrevocability actually means leads to second thoughts and expensive attempts to undo what cannot be undone. Some people imagine they can change their minds later or that decanting provides easy flexibility. Decanting does exist but requires state law permission and court approval in many cases-it’s not a simple revision process. The reality is that once assets transfer into an irrevocable trust, you cannot reclaim them, modify the trust terms unilaterally, or access funds without trustee approval.

If circumstances change dramatically (a beneficiary develops addiction problems, a trustee proves unreliable, or your financial situation shifts), your options are limited and expensive. This permanence is precisely why the trust works for asset protection and tax reduction, but it also means you need absolute clarity about your goals before transferring assets into it.

Trustee Selection and Its Lasting Consequences

Selecting the wrong trustee creates another permanent problem. A family member who seems responsible during your lifetime might mismanage funds, fail to file tax returns, or neglect beneficiaries after you die. Professional trustees cost money but provide fiduciary accountability, mandatory reporting, and liability insurance that family members cannot offer.

The decision between a family trustee and a professional institution should depend on the complexity of your assets, the trustee’s financial literacy, and whether family dynamics create conflicts of interest. This choice locks in place once the trust is funded, so the selection process demands careful thought.

Why Professional Guidance Prevents Costly Mistakes

An attorney who understands Tennessee’s Uniform Trust Code, current Medicaid rules, and your specific asset situation will structure the trust to accomplish your actual goals rather than create problems. Without that guidance, you might establish a trust that fails to reduce estate taxes, doesn’t qualify you for Medicaid benefits, or creates unintended income tax burdens for beneficiaries.

The cost of setup pales compared to the cost of fixing mistakes later or losing benefits you should have received. An attorney can identify which assets belong in the trust, verify that transfers happen correctly, and confirm that your trustee selection aligns with your family’s needs and your estate’s complexity.

Final Thoughts

An irrevocable trust is not a document you create and forget-it’s a permanent commitment that requires careful planning and precise execution. The permanence that makes these trusts valuable for tax reduction, creditor protection, and Medicaid eligibility also means you cannot change your mind without court approval and beneficiary consent. The mistakes outlined in this guide (failing to fund the trust, misunderstanding irrevocability, and skipping professional guidance) are entirely preventable with the right approach.

An irrevocable trust attorney brings clarity to decisions that affect decades of your family’s financial security. The right structure protects your home from long-term care costs, reduces federal estate taxes, shields assets from creditors, and accelerates inheritance distribution after you die. The wrong structure or poor timing can cost you thousands in lost benefits or create tax consequences that undermine your goals.

We at Law Offices of Roshni T. Desai help families navigate these decisions with personalized planning that accounts for your assets, your family situation, and your actual goals. Schedule a consultation to discuss whether an irrevocable trust fits your situation and what timing means for your family by visiting Law Offices of Roshni T. Desai.