Small Business Trust Planning: Protecting Your Legacy

Small business owners often overlook one critical reality: without proper planning, your business and personal assets face unnecessary taxes, delays, and family conflict after you’re gone.

At Law Offices of Roshni T. Desai, we’ve seen how small business trust planning protects what you’ve built. The right trust strategy keeps your business running smoothly, reduces tax burden on heirs, and keeps succession details private.

Why Small Business Owners Need Trust Planning

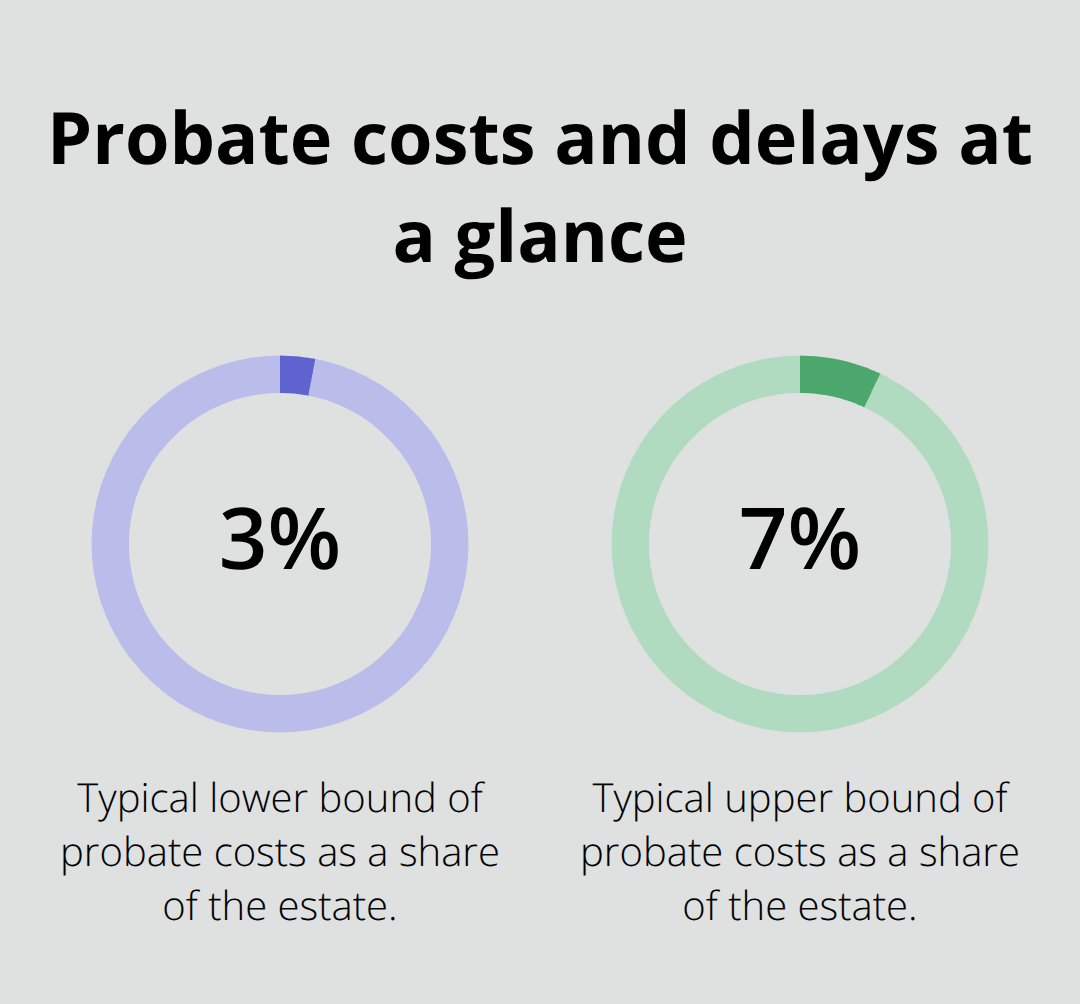

Probate costs time and money your heirs can’t afford to lose

Probate is expensive and slow. When a small business owner dies without a trust, their business and personal assets enter probate court-a public process that typically costs between 3% and 7% of the estate’s value and takes 6 to 12 months or longer to complete. During this time, your business sits in limbo.

Customers question continuity, employees face uncertainty, and key decisions get delayed while the court handles paperwork. A revocable living trust bypasses probate entirely, transferring your business directly to your chosen successor within weeks, not months. The process stays private-no court filings, no public record of your assets, and no information disclosed to competitors or the public. For family businesses especially, this privacy protects your competitive position. You control who knows what happened to your company and when successors take over, rather than having that information broadcast through court documents.

Estate taxes shrink what heirs actually receive

Federal estate tax exemptions currently sit at 13.61 million dollars per individual as of 2024, but this exemption drops to 7 million dollars in 2026 unless Congress acts. Many small business owners mistakenly assume they won’t owe estate taxes because their business seems modest in value. The problem is that business assets, real estate, equipment, and accounts receivable add up fast. A business worth 3 million dollars suddenly triggers significant federal and state taxes. Irrevocable trusts remove assets from your taxable estate permanently, meaning your heirs inherit without the tax hit. The business stays in the family or transfers to your chosen successor without a forced liquidation or loan to cover tax bills. This matters most for owners in high-value states like California, which imposes no state estate tax but forces heirs to navigate federal obligations carefully.

Succession planning keeps operations running when you can’t

Without a trust naming a successor and granting them authority, your business halts when you die or become incapacitated. Banks freeze accounts, vendors pull credit, and employees leave for more stable jobs. A trust with clear successor designations and trustee instructions keeps the business running. The trustee can manage day-to-day operations, pay employees, service customers, and execute buy-sell agreements without waiting for probate or court approval. If you become disabled, a successor trustee steps in immediately, preventing months of lost revenue and damaged relationships. This continuity protects not just your legacy but also your employees’ livelihoods and your customers’ trust in the business.

Understanding these three reasons shows why trust planning matters for small business owners. The next section examines the specific trust structures that address each of these concerns and how they work in practice.

Which Trust Structure Fits Your Small Business

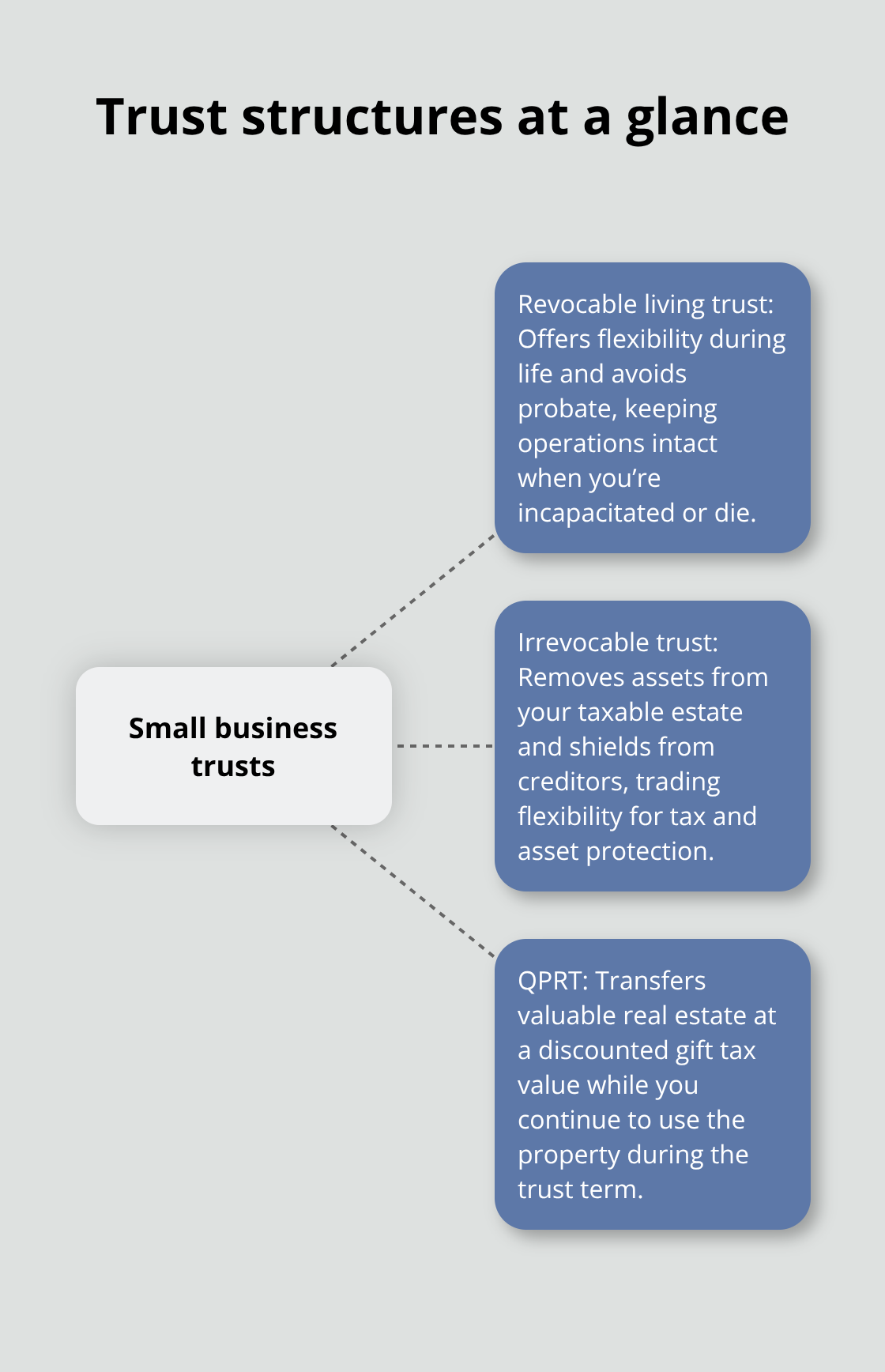

Revocable living trusts keep control in your hands

Revocable living trusts offer the flexibility small business owners need during their lifetime. You maintain full control, modify trust terms at any time, and change beneficiaries or trustees as circumstances shift. This matters because your business evolves-you may bring in partners, sell a division, or restructure operations. The trust adjusts with you. When you die or become incapacitated, the successor trustee takes over without court intervention, keeping operations intact. However, revocable trusts don’t reduce estate taxes because assets remain in your taxable estate. They solve the probate problem effectively but don’t address the tax burden your heirs face. If your business is worth under 7 million dollars and you prioritize avoiding probate over minimizing taxes, a revocable living trust handles the job efficiently. Setup costs run between 1,500 and 3,000 dollars depending on complexity, making this the affordable entry point for many small business owners.

Irrevocable trusts lock in tax and asset protection

Irrevocable trusts take the opposite approach-they lock in place but deliver serious tax and asset protection advantages. Once you transfer your business into an irrevocable trust, you cannot change your mind or reclaim the assets. This permanence sounds restrictive, yet it’s precisely what makes irrevocable trusts powerful for wealth preservation. Assets removed from your estate permanently escape federal estate taxes and creditor claims. If your business generates significant income or you expect its value to grow, an irrevocable trust stops that future growth from inflating your taxable estate. The IRS allows you to gift assets into an irrevocable trust using your annual exclusion (18,000 dollars per person in 2024) without triggering gift taxes. For business owners concerned about lawsuits, creditors, or leaving a substantial legacy, irrevocable trusts provide fortress-level protection. The tradeoff is loss of control and higher setup costs-typically 3,000 to 5,000 dollars or more.

Qualified Personal Residence Trusts protect valuable property

Qualified Personal Residence Trusts work specifically for business owners who own valuable real estate alongside their operating business. This trust removes property from your taxable estate while letting you live in or use the property during the trust term. After the term ends, ownership passes to beneficiaries at a discounted gift tax value. If your office building or commercial property represents significant net worth, a QPRT can reduce estate taxes substantially. The strategy works best when property values are expected to appreciate significantly.

Matching your trust to your situation matters most

Each trust structure addresses different priorities. A revocable living trust prioritizes flexibility and probate avoidance. An irrevocable trust prioritizes tax reduction and creditor protection. A QPRT prioritizes real estate transfer at favorable tax rates.

Your business size, growth trajectory, asset composition, and family situation determine which structure (or combination of structures) makes sense. The wrong choice leaves money on the table or creates unnecessary restrictions. The right choice protects your legacy while fitting your actual circumstances. Understanding these distinctions prepares you to evaluate which approach aligns with your goals-and what questions to ask when you review your options with a professional.

Common Mistakes Small Business Owners Make

Outdated trust documents create succession chaos

A trust only works if it matches your actual life. Small business owners create a trust, fund it properly, and name successors-then forget about it for ten years. Meanwhile, they marry, divorce, have children, sell a business division, relocate to another state, or bring in a partner. None of these changes appear in the trust. When succession happens, the trustee follows outdated instructions that no longer fit reality. A successor who moved away years ago receives the role to run a business they no longer understand. A business division that was sold off years ago still sits in the trust as a listed asset. A spouse who divorced five years ago remains listed as a beneficiary.

These gaps create conflict, delay transitions, and sometimes trigger litigation among heirs. The IRS also scrutinizes outdated trusts, especially when business valuations or ownership structures have changed materially. Review your trust every three to five years, or immediately after major life events like marriage, divorce, the birth of children, significant business sales, partnership changes, or relocation to a new state. Each review should confirm that successor trustees still fit the role, beneficiary designations still reflect your wishes, and business assets listed in the trust match what you actually own. This work directly affects whether your business transfers smoothly or gets tangled in confusion.

Unfunded trusts leave assets vulnerable to probate

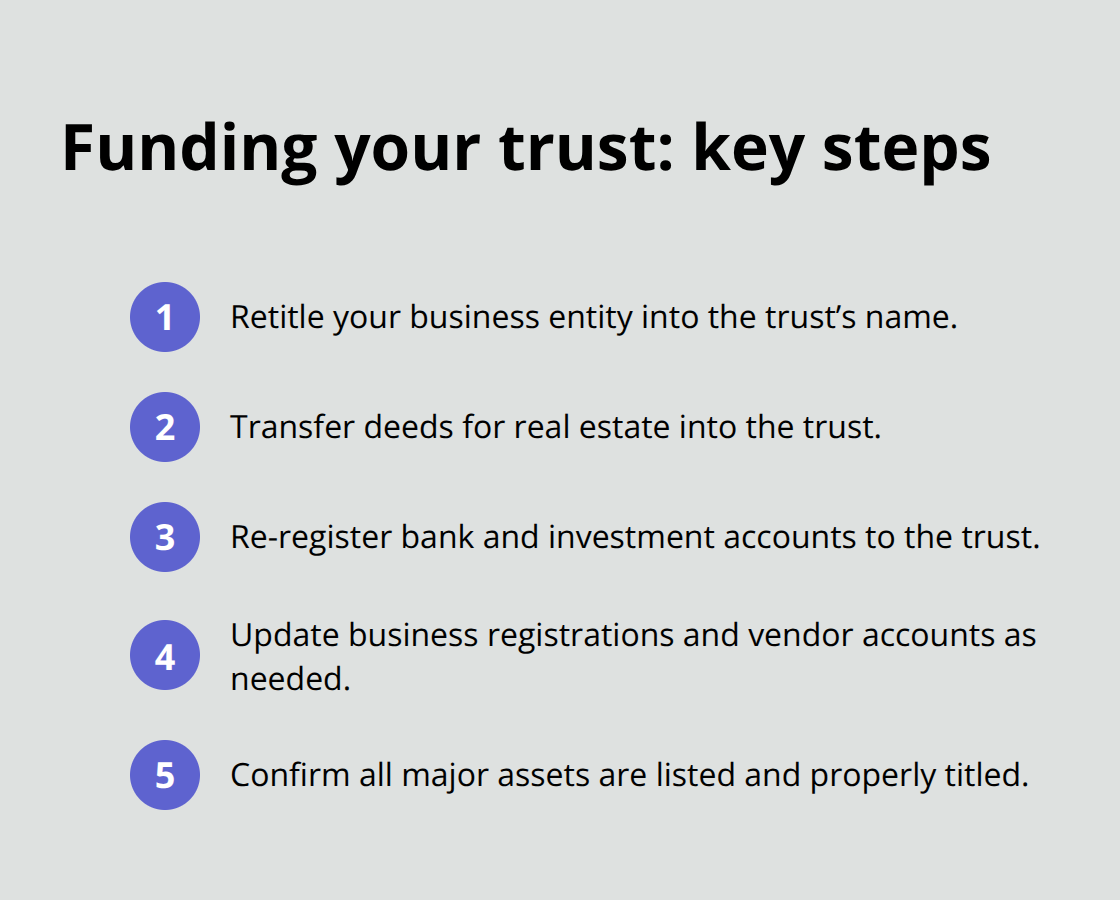

The second critical mistake is leaving a trust on paper without actually funding it. You create a trust document, sign it, and assume the job is done. But a trust only controls assets that are titled in the trust’s name. If your business is still registered in your personal name, held in an LLC under your individual ownership, or listed on bank accounts in your name alone, the trust has no power over these assets when you die or become incapacitated. They still go through probate. They still trigger estate taxes. They still sit frozen while courts sort things out.

Funding means retitling your business, real estate, investment accounts, and other significant assets into the trust’s name. This requires paperwork-new business registrations, deed transfers, account reregistrations-but it’s the step that makes the trust actually work. Many owners skip this because the paperwork feels tedious or they worry about operational disruption. In reality, retitling a business into a trust typically involves minimal disruption and can often be completed within weeks. Bank accounts and investment accounts retitle in days. The cost runs between five hundred and two thousand dollars depending on complexity, far less than the estate planning costs that result from leaving assets untitled.

Unclear successor authority creates disputes and hesitation

The third mistake is naming successors without clarity about their actual authority and responsibilities. You designate your adult child as trustee and successor manager, but you don’t specify whether they can sell the business, take on debt, hire and fire employees, or modify operations. You don’t explain the difference between their role as trustee and their role as a beneficiary. You don’t document which decisions require their judgment and which decisions require consultation with other beneficiaries or outside advisors.

When succession actually happens, confusion erupts. Other heirs challenge decisions. The successor hesitates because they’re unsure of their authority. Customers and vendors question whether the new person can legally bind the business. Clear successor designation means writing down specific powers, limitations, decision-making protocols, and contingencies. It means naming a backup successor in case your first choice becomes unavailable. It means documenting whether the successor gets paid for their trustee work and how much. These details prevent disputes and give your successor confidence to act decisively when the time comes.

Final Thoughts

Small business trust planning protects what you’ve built by addressing three realities most owners face: probate delays that halt operations, estate taxes that shrink what heirs receive, and succession uncertainty that creates conflict. A revocable living trust keeps you in control while avoiding probate, an irrevocable trust locks in tax and asset protection, and a Qualified Personal Residence Trust handles valuable real estate efficiently. The structure that fits your situation depends on your business size, growth plans, and family circumstances.

The mistakes we outlined-outdated documents, unfunded trusts, and unclear successor authority-are entirely preventable with consistent attention. Review your trust every three to five years or after major life changes like marriage, divorce, or significant business transitions. Fund it completely by retitling business assets into the trust’s name, and write down your successor’s specific powers, limitations, and decision-making authority. These steps transform a trust from a document into a working protection system that actually functions when you need it.

Assess whether your current plan addresses probate, taxes, and succession, then contact Law Offices of Roshni T. Desai to review your trust strategy and confirm your legacy is protected. We help small business owners build and maintain trusts that work, and we offer free consultations with flexible home or office visits across Southern California.