Trust Administration for Heirs: Ensuring Fair and Timely Distribution

When a loved one passes away, trust administration for heirs often becomes complicated and stressful. Delays in distribution, unclear trustee actions, and tax complications can leave beneficiaries waiting months or even years for their inheritance.

We at Law Offices of Roshni T. Desai help heirs understand their rights and navigate the distribution process. This guide covers what you need to know to protect yourself and move forward.

What Happens During Trust Administration

Initial Steps and Notifications

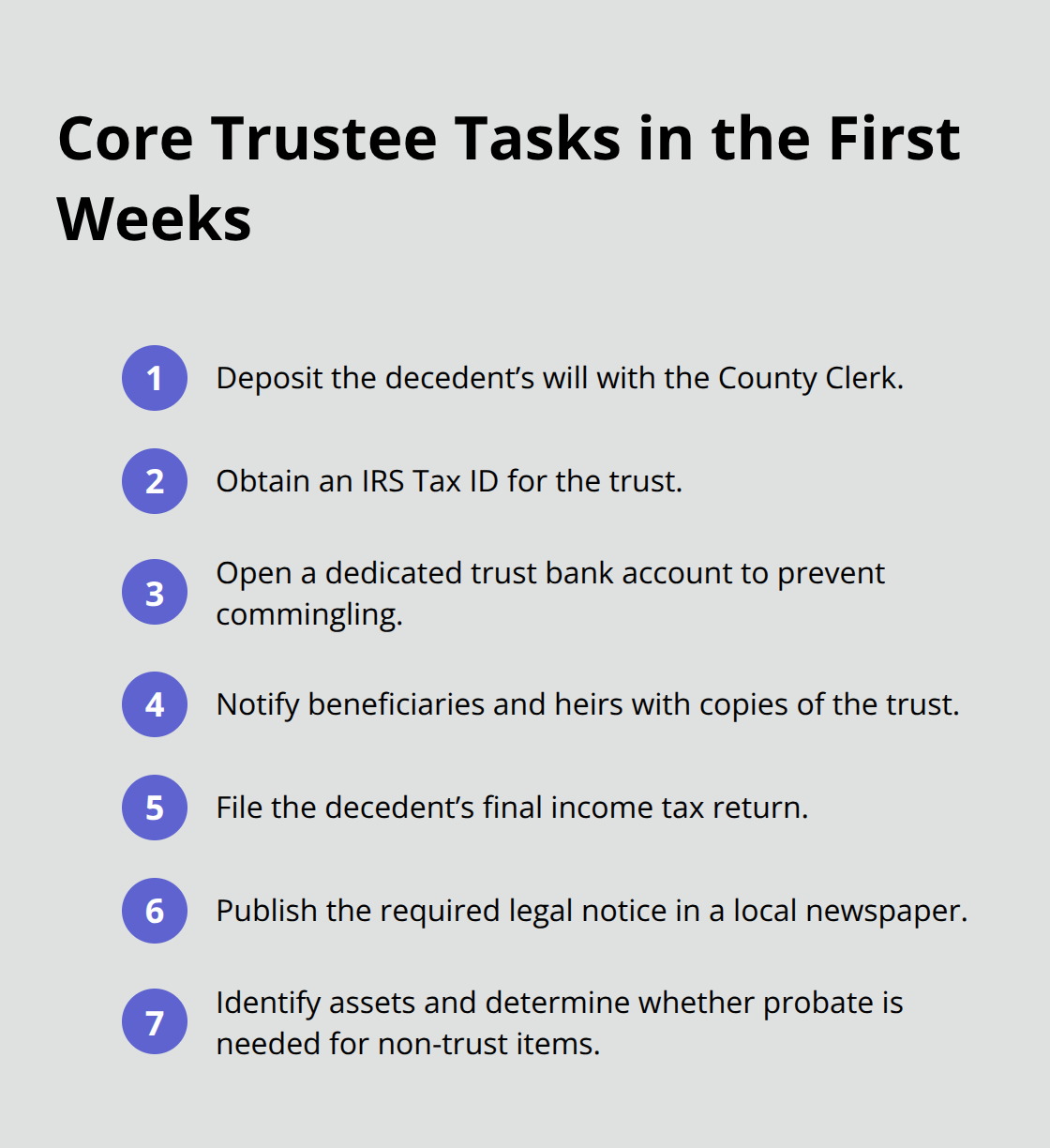

Trust administration begins the moment a trustee learns of the grantor’s death. The trustee must notify beneficiaries and heirs promptly with copies of the trust document, as California Probate Code §16060 requires. Many heirs wrongly assume the process is automatic, but it actually involves dozens of concrete tasks that must happen in a specific order. The trustee obtains an IRS Tax ID for the trust, files the decedent’s final income tax return, publishes a legal notice in a local newspaper as required by law, and notifies banks and financial institutions of the death. Within the first few weeks, the trustee deposits the decedent’s will with the County Clerk to determine whether probate is needed for any assets not titled in the trust. These early steps set the foundation for everything that follows, and mistakes here create cascading delays. The trustee also opens a bank account in the trust’s name to track all expenses separately, which protects both the trustee and beneficiaries from commingling issues that can trigger legal liability.

Marshaling Assets and Handling Valuations

Once initial notifications are complete, the trustee marshals and protects all trust assets by obtaining valuations as of the date of death for tax and distribution purposes. This valuation step is not optional-it determines what beneficiaries ultimately receive and affects estate tax calculations. The trustee collects life insurance proceeds, reviews retirement account beneficiary designations to determine if stretch-out options exist for 401(k)s and IRAs, and notifies the VA and Department of Health Services if applicable. Simultaneously, the trustee must handle the decedent’s debts, final medical bills, funeral expenses, and attorney and CPA fees from trust assets. California Probate Code §16003 requires trustees to treat all beneficiaries fairly and impartially, which means creditors cannot be favored over heirs.

Managing Tax Obligations

Tax obligations are substantial and often extend the administration timeline significantly. The trustee files annual trust income tax returns while the trust remains open, and for estates exceeding several million dollars, an estate tax return may be required, adding significant time to administration. Simple trusts typically settle in four to five months, while typical revocable living trusts take twelve to eighteen months according to probate guidelines. Major delays arise from taxes due, outstanding debts, and real estate sales or title issues. If a joint trust splits into a Survivor’s Trust and Bypass Trust, an administrative trust with its own tax ID is typically created for accounting purposes, which adds another layer of compliance.

Distributions and Fiduciary Accountability

The final phase involves distributing trust assets to beneficiaries after all debts, taxes, and expenses are paid. California Probate Code §16062 requires trustees to provide formal accountings at least annually and upon termination of the trust, allowing beneficiaries to track every asset movement and verify distributions. The trustee’s fiduciary duty under the Probate Code requires managing assets prudently and distributing them according to the trust terms without unreasonable delay. Beneficiaries have the right to request copies of the trust document under §16060.7 and to demand accountings if the trustee fails to provide them voluntarily. If the trustee refuses to distribute or withholds distributions without valid cause, beneficiaries can file petitions in probate court to compel distribution or accounting. Understanding these fiduciary duties and accountability measures helps heirs recognize when trustee actions align with the law-and when they do not.

What Causes Trust Administration Delays

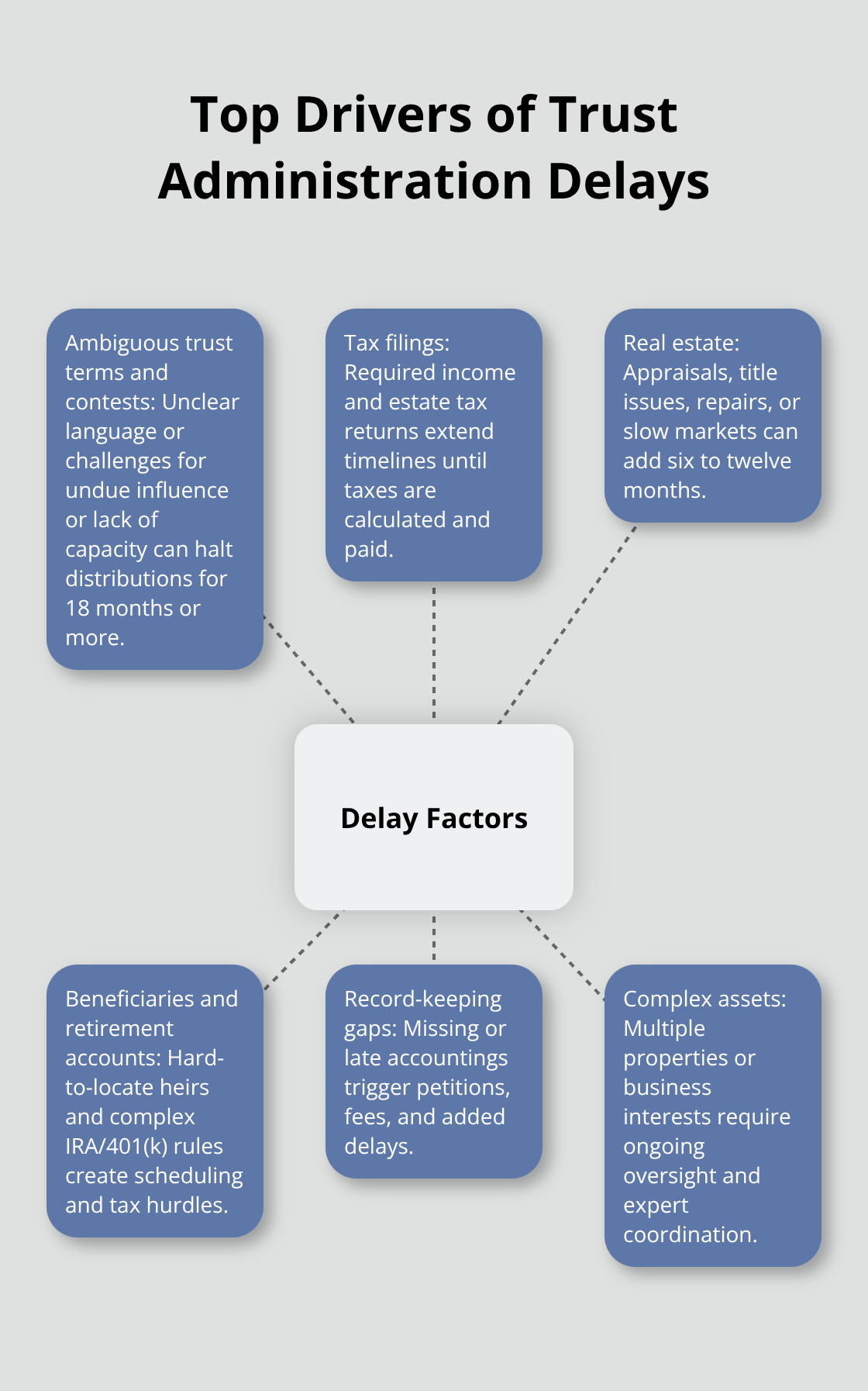

Delays in trust distribution rarely stem from a single cause. Instead, multiple issues compound to extend administration timelines from the typical twelve to eighteen months into years of waiting.

Ambiguous Trust Language and Contested Documents

Unclear trust language sits at the root of many problems. When a trust document contains ambiguous instructions about asset distribution, beneficiary definitions, or trustee powers, the trustee faces a choice: interpret the language independently and risk a beneficiary challenge, or seek court guidance through a petition for instruction. Either path stalls distributions. Contested trust documents create far worse delays. Beneficiary challenges citing undue influence, lack of capacity, or fraud can halt all distributions and trigger probate court proceedings that last eighteen months or longer.

Tax Filings and Estate Settlements

Tax obligations compound delays significantly because trustees cannot distribute assets until estate and income tax returns are filed and any taxes are paid. For estates exceeding several million dollars, federal estate tax returns must be prepared and filed, which can take months beyond the standard filing deadlines. The trustee must coordinate with tax professionals to optimize outcomes for the trust and its beneficiaries, and this coordination adds weeks or months to the timeline.

Real Estate Valuations and Sales

Real estate valuations add substantial time, particularly when the trust holds rental properties, commercial real estate, or family homes requiring appraisals as of the date of death. If the trustee decides to sell real property, title issues, needed repairs, or a slow market can extend timelines by six months to a year. These complications often represent the single largest source of delay in trust administration.

Beneficiary Location and Retirement Account Complexity

Locating all beneficiaries also causes delays, especially in blended families or when beneficiaries live overseas. Retirement account beneficiary designations require careful review because stretch-out options for IRAs and 401(k)s depend on the beneficiary’s status and the trust’s language, and missed deadlines here can trigger unwanted tax consequences for heirs. The trustee must verify each designation against the trust terms to avoid costly errors.

Record-Keeping and Accountability Gaps

Simple trusts with clear language, modest assets, and no real estate settle fastest. Complex trusts with multiple properties, business interests, or discretionary provisions require ongoing oversight and often benefit from professional guidance. Trustees who lack accounting experience or fail to maintain meticulous records of valuations, expenses, and distributions create additional friction because California Probate Code §16062 mandates formal accountings, and beneficiaries can demand them at any time. If a trustee delays providing required accountings, beneficiaries can file court petitions to compel disclosure, which triggers legal fees and further delays. Mediation or alternative dispute resolution can resolve many disputes without lengthy litigation, but only if both the trustee and beneficiaries agree to participate. Heirs who suspect mismanagement should request accountings in writing immediately and consult with a trust attorney to assess whether delays are reasonable or whether the trustee is breaching fiduciary duties. Statutes of limitations apply to claims against trustees, and waiting too long can bar remedies entirely.

Understanding these delay factors helps heirs recognize when administration is progressing normally and when trustee actions warrant closer scrutiny. The next section examines how heirs can actively protect their rights throughout the distribution process.

Protecting Your Rights During Trust Administration

Request Documentation and Accountings Immediately

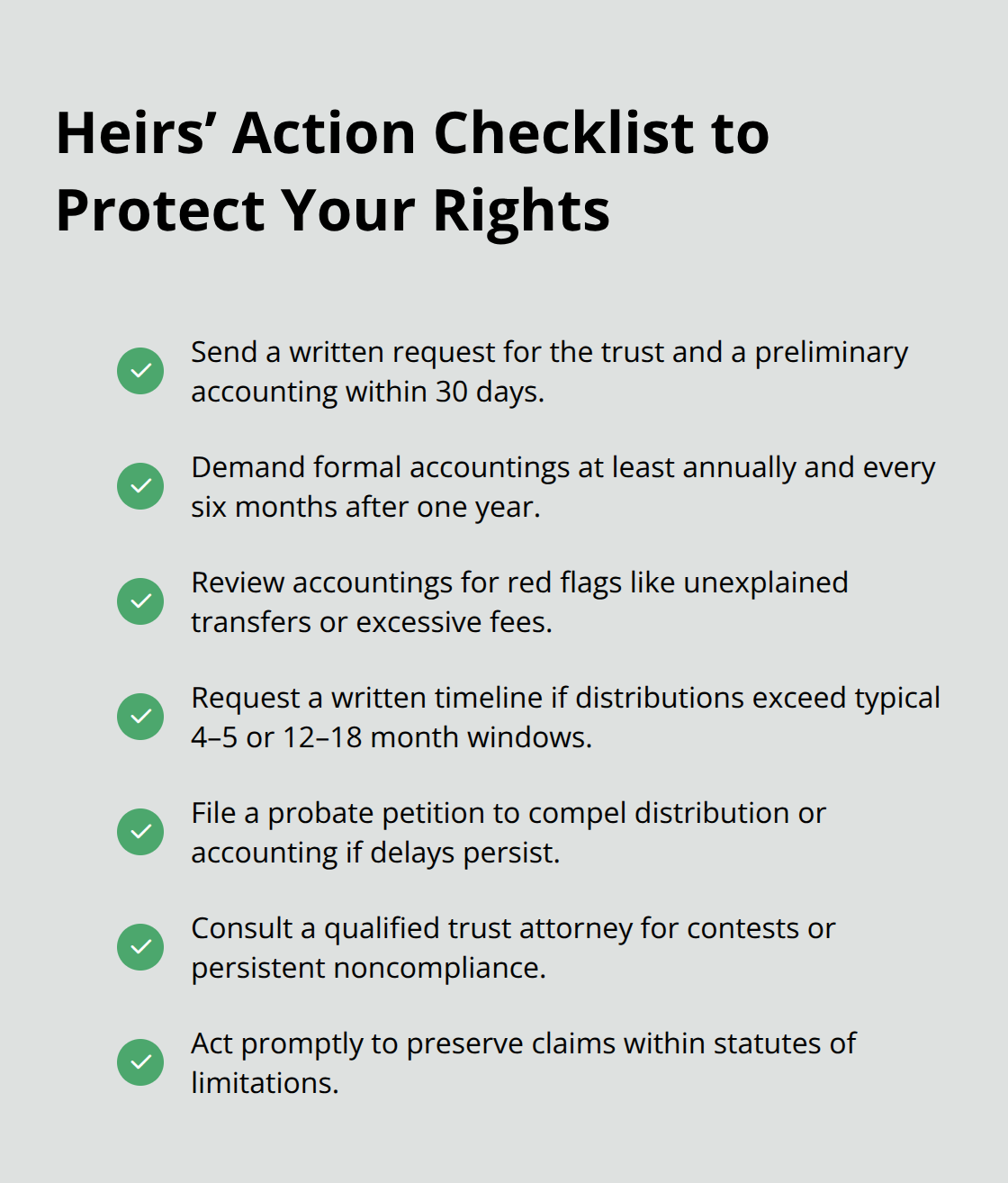

Waiting passively for distributions while a trustee controls your inheritance is a mistake. California Probate Code §16060 grants you concrete rights to information, and using those rights aggressively from day one prevents trustees from delaying unfairly or hiding misconduct. Send a written request for the trust document and a preliminary accounting within thirty days of the grantor’s death. This written request creates a paper trail and forces the trustee to respond formally rather than with vague excuses.

California Probate Code §16062 requires trustees to provide formal accountings at least annually and upon termination of the trust, so demand them every six months if administration extends beyond one year.

Accountings must show the opening balance, all income received, all expenses paid, all distributions made, and the closing balance for each asset. Red flags in accountings include unexplained transfers, unusual fees that seem excessive compared to the trust’s size, missing assets that don’t align with the initial inventory, or vague descriptions like administrative costs without itemization. If the trustee refuses to provide accountings or supplies incomplete ones, file a written demand citing Probate Code §16062. If the trustee still refuses, consult with a qualified attorney to file a court petition. This step costs money upfront but prevents years of delay and protects your inheritance.

Establish Clear Timelines and Demand Written Explanations

Knowing the legal timeline for distributions is equally important because trustees often cite vague timelines to justify indefinite delays. Simple trusts with clear language and modest assets typically settle in four to five months according to probate guidelines, while complex trusts average twelve to eighteen months. If your trustee claims distributions will take longer, demand a written explanation detailing specific obstacles such as pending tax filings, real estate sales, or creditor claims. A trustee cannot simply withhold distributions indefinitely without valid cause, and California Probate Code §16004.5 prohibits unreasonable delays.

If eighteen months have passed and the trustee has not distributed assets, this signals either incompetence or breach of fiduciary duty. File a petition in probate court to compel distribution or accounting, and the trustee may be ordered to pay your attorney’s fees and costs if the court finds the withholding unjustified. Trust contests citing undue influence or fraud are the only legitimate reason for extended delays, and even then, the trustee must notify you of the contest and provide regular updates on its status.

Identify Misconduct and Act Within Statutory Deadlines

If you suspect the trustee is mismanaging assets, commingling trust funds with personal accounts, or paying excessive fees to themselves, do not wait. Statutes of limitations apply to breach of fiduciary duty claims, and waiting too long can bar your remedies entirely. Common red flags include asset transfers that lack clear documentation, fees paid to the trustee or related parties that seem disproportionate to the work performed, or refusals to answer straightforward questions about trust administration. Courts can compel trustees to act, and beneficiaries may seek suspension or removal of a trustee; prevailing claims allow recovery of attorney’s fees and costs under California Probate Code §16420.

Final Thoughts

Trust administration for heirs requires you to act decisively rather than wait passively for distributions. Simple trusts settle in four to five months, while typical revocable living trusts take twelve to eighteen months-but trustees cannot withhold distributions indefinitely without valid cause. Send a written request for the trust document and preliminary accounting within thirty days of the grantor’s death, then demand accountings every six months if administration extends beyond one year. Scrutinize these accountings for red flags like unexplained transfers or excessive fees, and file court petitions if the trustee refuses to provide them.

Professional guidance makes a measurable difference when trust administration extends beyond eighteen months, when real estate or retirement accounts complicate distributions, or when you suspect trustee misconduct. Tax professionals help optimize outcomes for the trust and its beneficiaries, while trust attorneys interpret ambiguous language, file court petitions, and enforce your rights under California Probate Code. Statutes of limitations apply to breach of fiduciary duty claims, so waiting passively can bar your remedies entirely.

We at Law Offices of Roshni T. Desai provide personalized estate planning and probate services across Southern California, including trust administration with over 25 years of experience. Ms. Desai’s dual licensure as an attorney and real estate professional streamlines estate-related property sales to reduce costs and delays. Contact us today for a free consultation with flexible home or office visits to discuss your trust administration for heirs.