Probate Administration Overview: Roles, Steps, and Timelines

Serving as an executor brings real responsibility. You’ll manage assets, handle debts, communicate with beneficiaries, and file court documents-often while grieving.

This probate administration overview walks you through each role and step. We at Law Offices of Roshni T. Desai help executors navigate the process smoothly and avoid costly mistakes.

Understanding the Executor’s Role in Probate

Serving as an executor brings real responsibility. You’ll manage assets, handle debts, communicate with beneficiaries, and file court documents-often while grieving. This section walks you through each role and step so you understand what the position actually demands.

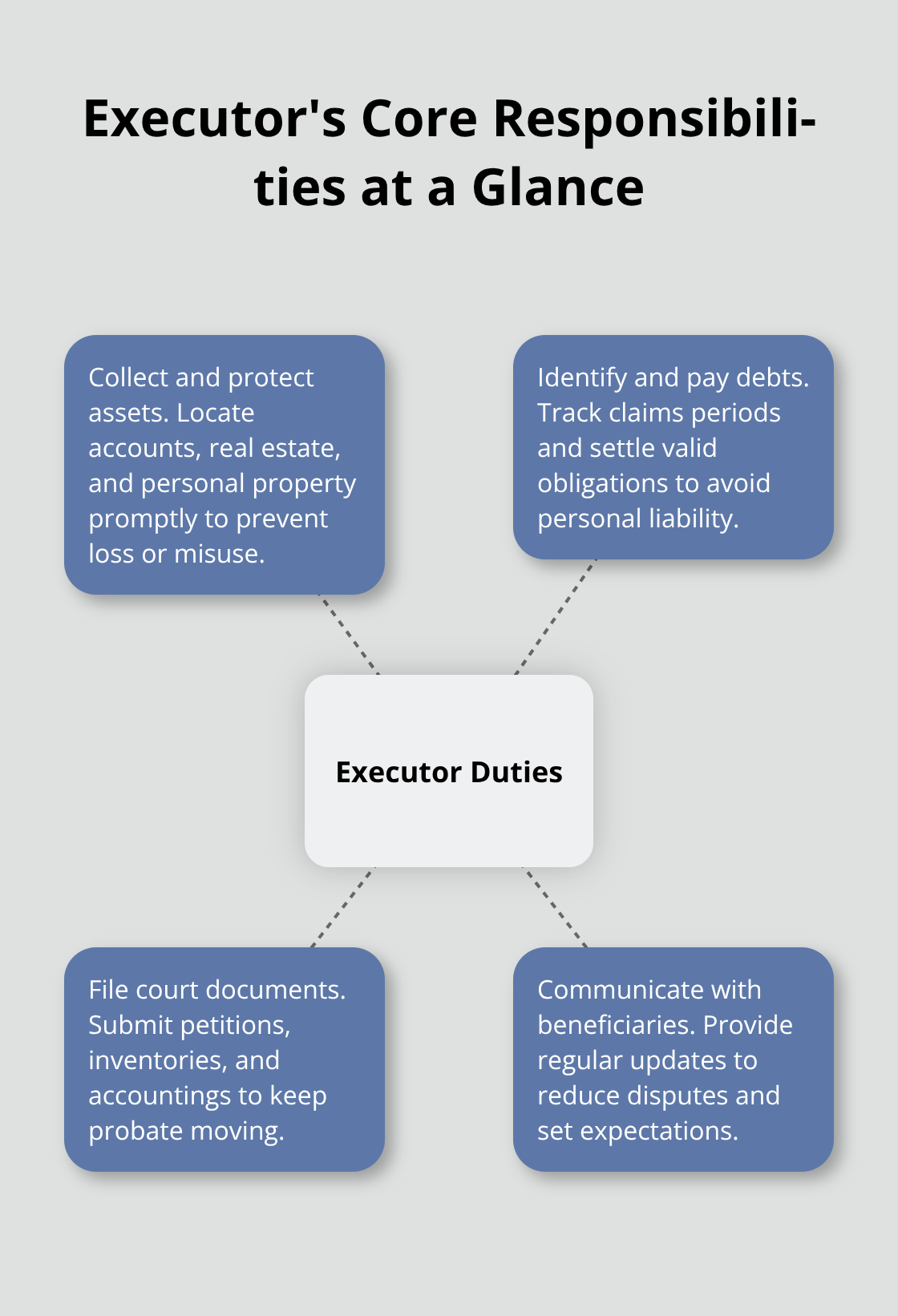

The Three Core Responsibilities

The executor’s job breaks down into three concrete responsibilities that run parallel throughout probate. You’ll collect and protect the deceased’s assets, which means locating bank accounts, investment statements, real estate deeds, and personal property within weeks of death. You’ll also identify and pay debts-creditors have a limited window to file claims, typically 60 days in Texas or 4 months in California-so missing these deadlines can create liability problems for you personally. Finally, you’ll file court documents that prove your authority and keep the probate moving forward. These three tasks overlap constantly, so treating them as separate phases leads to mistakes.

Opening an Estate Bank Account Immediately

Start by obtaining an Employer Identification Number from the IRS immediately, even before you file the initial petition. This EIN lets you open an estate bank account, which separates the deceased’s money from your own and prevents commingling that could trigger audits or personal liability claims. Many executors skip this step and use personal accounts, which is a serious error that accountants and probate attorneys see regularly. Once the account is open, every dollar the estate receives goes there, and every bill or expense comes from that account. This creates a clear paper trail that the court will demand when you close the estate.

Managing Assets and Debts Simultaneously

Don’t wait until you’ve inventoried everything to start paying bills. Federal estate tax applies to estates over 12 million dollars, but state and federal income taxes on the estate itself come due regardless of size. You must file the estate’s final income tax return and any required estate tax returns on time-missing these deadlines triggers penalties that reduce what beneficiaries receive. Real estate presents particular challenges because property taxes and mortgage payments continue even during probate, so you should prioritize these obligations first. If the estate lacks liquid funds to cover immediate expenses, you may need to sell assets quickly, which is another reason to seek professional guidance early.

Keeping Beneficiaries Informed Throughout Probate

Communication with beneficiaries prevents disputes that can triple your timeline and legal costs. You should send written notices explaining the probate process, the timeline specific to your state, and what you’ve found during asset inventory. Beneficiaries who feel informed rarely challenge distributions; those kept in the dark often hire their own attorneys to investigate you. Set clear expectations about when distributions will happen-Texas typically resolves probate in 6 to 12 months, while California often takes 12 to 18 months or longer due to court congestion, so you should be honest about your state’s reality rather than promising speed you can’t deliver. The next section covers the specific steps and timelines that shape how long probate actually takes in your jurisdiction.

How Probate Moves From Filing to Final Distribution

The Filing Process Sets Your Timeline

Probate follows a strict sequence that varies dramatically by state. The moment you file the initial petition with the court, a clock starts running on creditor claims periods, inventory deadlines, and distribution windows that differ across jurisdictions. In Texas, you have 60 days to notify creditors after the court appoints you as executor, while California requires a 4-month creditor claims period and New York stretches it to 7 months. Missing these windows doesn’t just slow probate-it exposes you personally to creditor claims and forces the court to hold back funds longer than necessary.

The filing itself requires the original will, a certified death certificate, and a petition stating the decedent’s domicile and date of death. You must initiate this filing yourself or work with an attorney; it doesn’t happen automatically. Once filed, the court schedules a hearing within 2 to 4 weeks in most states to admit the will and formally appoint you. Letters Testamentary or Letters of Administration-which prove your legal power to act-arrive only after the court approves your petition.

Locating and Valuing All Assets

Asset inventory comes next, and this step determines everything that follows. You must locate and value all probate assets (bank accounts, investment statements, real estate, vehicles, and valuable personal property) within 60 to 90 days depending on your state’s rules. Most executors underestimate this work because they overlook assets in safe deposit boxes, online accounts without beneficiary designations, and insurance policies where the estate is named as beneficiary rather than a person.

Pull credit reports, search property records, and contact the decedent’s employers about retirement accounts or deferred compensation. This thorough approach prevents costly oversights that surface months later during the final accounting.

Running Parallel Tracks: Debts, Taxes, and Distributions

Once you have the inventory, you’ll run parallel tracks: paying debts and taxes while the creditor claims period runs, and preparing final distributions after the court approves your accounting. Federal estate tax applies to estates over 12 million dollars, but state and federal income taxes on the estate itself come due regardless of size. You must file the estate’s final income tax return and any required estate tax returns on time-missing these deadlines triggers penalties that reduce what beneficiaries receive.

The final distribution happens only after debts, taxes, and court fees are paid. Beneficiaries who understand this upfront rarely complain about delays, while those expecting quick payouts often hire attorneys to investigate you.

State-Specific Timelines Shape Your Process

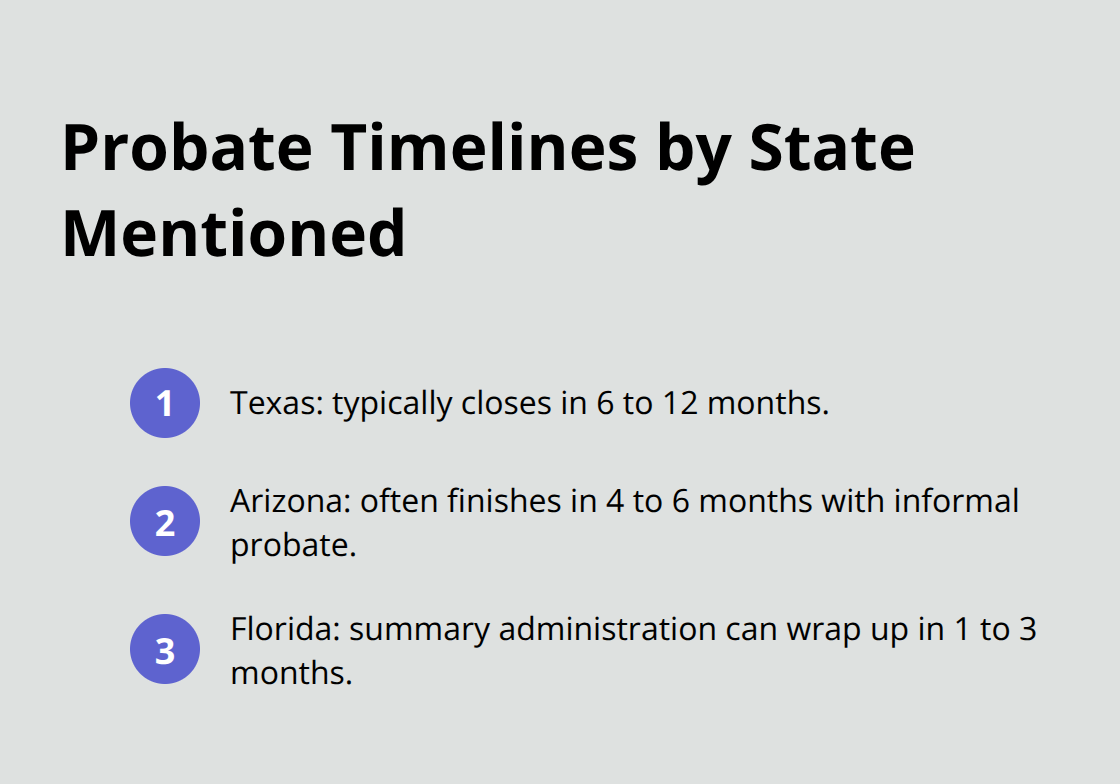

In Texas, probate typically closes in 6 to 12 months, but Arizona often finishes in 4 to 6 months using informal probate procedures that bypass court hearings unless someone objects. Florida’s summary administration for small estates under 75,000 dollars can wrap up in 1 to 3 months, making state choice and procedure selection critical to your timeline.

These variations mean that your state’s specific rules-not general probate principles-determine how quickly you can close the estate and distribute assets to heirs.

Understanding your jurisdiction’s creditor claims period, inventory deadlines, and court backlogs helps you set realistic expectations with beneficiaries and plan your asset sales or debt payments accordingly. The next section addresses the obstacles that most often derail probate timelines and how to handle them when they arise.

Common Probate Challenges and How to Navigate Them

Beneficiary Disputes Stop Distributions Cold

Beneficiary disputes are the single biggest reason probate timelines explode beyond state averages. When one heir questions distributions, demands a recount of assets, or suspects mismanagement, the entire process freezes while attorneys investigate and courts mediate. You cannot ignore these concerns and move forward. The moment a beneficiary files an objection with the court, the judge must hold a hearing, and distributions halt until the dispute resolves.

Disputes add 6 to 18 months to otherwise straightforward probate cases. The solution is radical transparency from day one.

Send beneficiaries a detailed written inventory of all assets within 30 days of your appointment, include valuations with supporting appraisals, and explain the creditor claims period and tax obligations that delay final distributions. Beneficiaries who understand why they cannot receive money immediately rarely hire attorneys to investigate you. Those kept in the dark almost always do.

Contested Wills Require Court Validation

Contested wills present a different problem entirely. If a beneficiary or excluded heir challenges the will’s validity, the probate court must determine whether the document meets legal standards for execution, testamentary capacity, and freedom from undue influence. California courts receive thousands of will contests annually, and these cases routinely consume 18 to 24 months of additional litigation beyond standard probate timelines.

You cannot settle a will contest quickly through negotiation alone because the court must make a formal ruling on validity. Gather evidence of the decedent’s mental state at signing, witness testimony, and documentation that the will was prepared free from pressure. If the decedent used a video recording during signing or had a physician document capacity, these materials become invaluable if a challenge emerges.

Estate Taxes Demand Early Action

Federal estate tax applies to estates exceeding 12 million dollars, and these returns demand meticulous documentation and professional preparation. State income tax on the estate itself comes due regardless of size, and filing delays trigger penalties that reduce what beneficiaries ultimately receive.

Many executors wait until the final distribution phase to address taxes, which is a costly mistake. File the estate’s final income tax return within nine months of the decedent’s death and address any federal estate tax liability on the same timeline. Working with a tax professional or CPA from month two of probate prevents penalties and allows you to calculate distributions accurately.

Address Challenges Head-On With Professional Support

Probate challenges rarely resolve themselves. You must address them head-on with clear communication, thorough documentation, and professional guidance when complexity exceeds your knowledge. Ignoring disputes, hoping contested wills fade away, or delaying tax filings transforms a six-month process into a two-year burden that exhausts you and angers beneficiaries who expected timely distributions.

Final Thoughts

Probate administration requires you to manage multiple deadlines, communicate clearly with beneficiaries, and handle complex tax and legal obligations simultaneously. This probate administration overview shows that success depends on understanding your state’s specific rules, staying organized from day one, and recognizing when professional guidance becomes necessary rather than optional. You cannot avoid probate challenges by working harder alone-beneficiary disputes, contested wills, and tax complications demand knowledge that most executors simply don’t possess.

Missing a creditor claims deadline, filing taxes late, or failing to document asset valuations properly creates personal liability that follows you long after probate closes. These mistakes cost thousands in penalties and legal fees that reduce what beneficiaries ultimately receive. We at Law Offices of Roshni T. Desai work with executors throughout Southern California to handle probate administration from start to finish, and contact us for a free consultation if you’re serving as an executor or facing probate challenges.

We offer flexible home or office visits across Southern California and provide straightforward guidance tailored to your estate’s specific situation. The cost of professional support early in probate is far less than the expense of fixing mistakes later or managing disputes that could have been prevented through clear communication and proper documentation from the start.