Probate Administration Asset Inventory: Organize Your Estate Now

Most people don’t realize how many assets they actually own until it’s too late. Without a proper probate administration asset inventory, families often miss bank accounts, forgotten investments, or digital holdings that should have been included in the estate.

At Law Offices of Roshni T. Desai, we’ve seen firsthand how disorganized records create unnecessary delays and conflict among heirs. The good news is that creating a comprehensive inventory now prevents these problems and makes the probate process significantly smoother for everyone involved.

Why Asset Inventory Matters Right Now

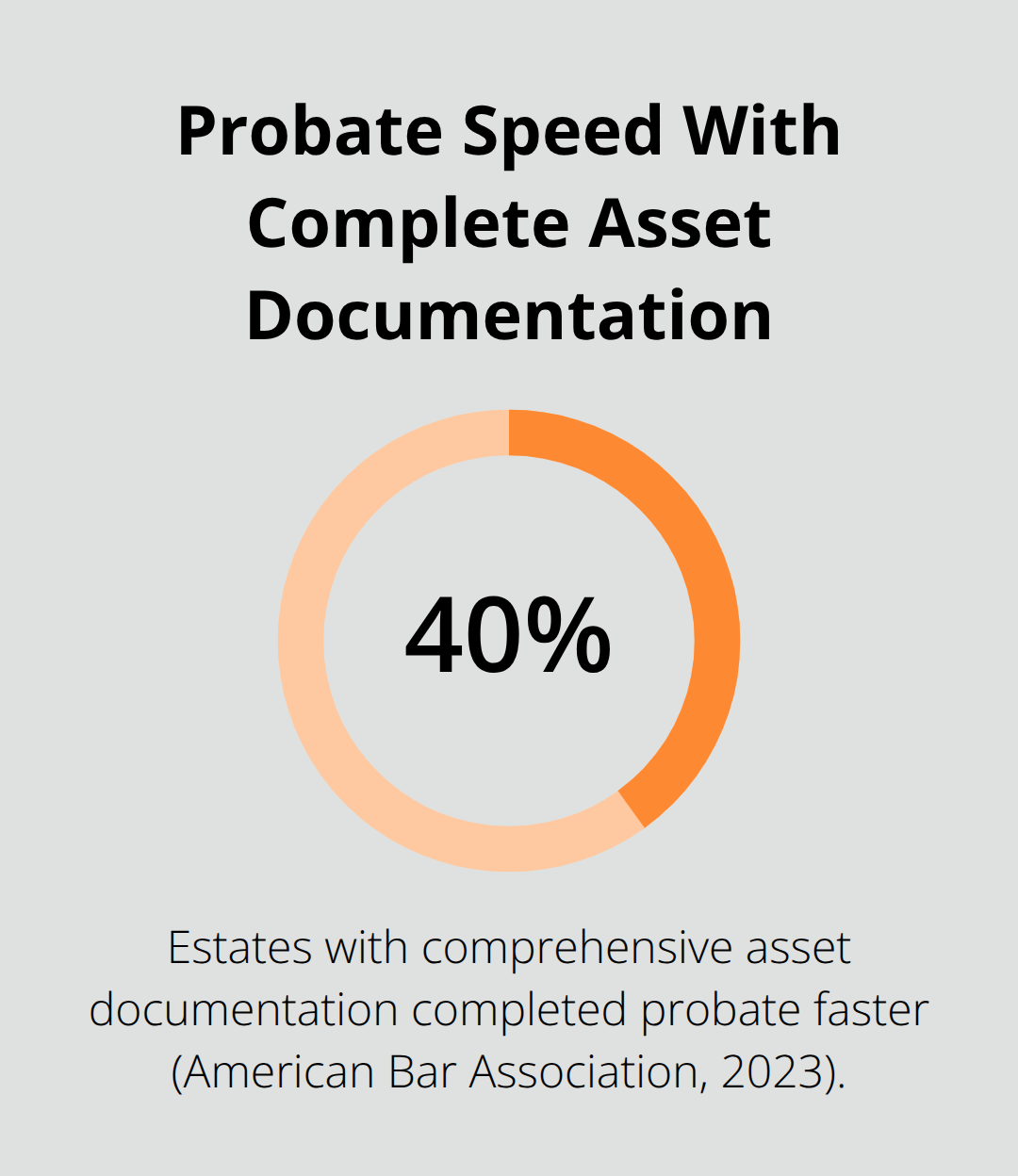

An asset inventory isn’t just paperwork-it’s the difference between a probate process that takes months and one that takes years. Disorganized records create unnecessary delays and conflict among heirs. Courts in California require a complete accounting of all estate assets, and missing items force executors to file amendments, which delays distributions to heirs and increases legal fees. A 2023 survey by the American Bar Association found that estates with comprehensive asset documentation completed probate 40% faster than those without. The inventory also serves as your legal protection.

When you document everything at the time of death with specific values and locations, you create an undisputed record that protects you from claims that assets were mismanaged or hidden. Without this documentation, heirs can question whether you handled their inheritance fairly, leading to costly disputes and family conflict that could have been prevented.

Stopping Assets From Disappearing

Forgotten assets happen more often than people think. Bank accounts at regional institutions close without notice, online investment platforms send statements to outdated email addresses, and cryptocurrency wallets sit untouched because no one knows the login information. You must search systematically for everything your loved one owned. Start with tax returns from the past three years-these typically list rental properties, investment income, and business interests that might otherwise go unnoticed. Check for safe deposit boxes at banks and credit unions, search for unclaimed property through your state’s unclaimed property database, and review credit card statements to identify recurring subscriptions or memberships that might indicate hidden accounts. Digital assets present a particularly complex challenge. Social media accounts, cryptocurrency holdings, domain names, and online storage accounts have real monetary or sentimental value, yet most families never locate them because they don’t know where to look. An inventory that specifically catalogs digital assets with access information prevents these holdings from being permanently lost.

Why Courts Demand Complete Documentation

California probate law requires executors to file a complete inventory within 60 days of opening probate. This isn’t bureaucratic busy work-the inventory is how the court oversees the estate’s management and confirms that beneficiaries receive what they’re entitled to. The inventory must list each asset’s description, location, and fair market value as of the date of death. Properties, vehicles, and collectibles require professional appraisals to establish accurate values that satisfy tax authorities and prevent disputes over inheritance shares. When an inventory is incomplete or inaccurate, courts can hold the executor personally liable for missing assets, and beneficiaries can sue for breach of fiduciary duty. A comprehensive inventory eliminates this liability because it provides transparent documentation of what existed and what was properly accounted for.

Now that you understand why courts demand complete documentation, the next step is learning how to actually create that comprehensive inventory. The process requires you to organize multiple asset categories and track information systematically-something we’ll cover in detail in the next section.

Building Your Asset Inventory From Scratch

Gather Documents First

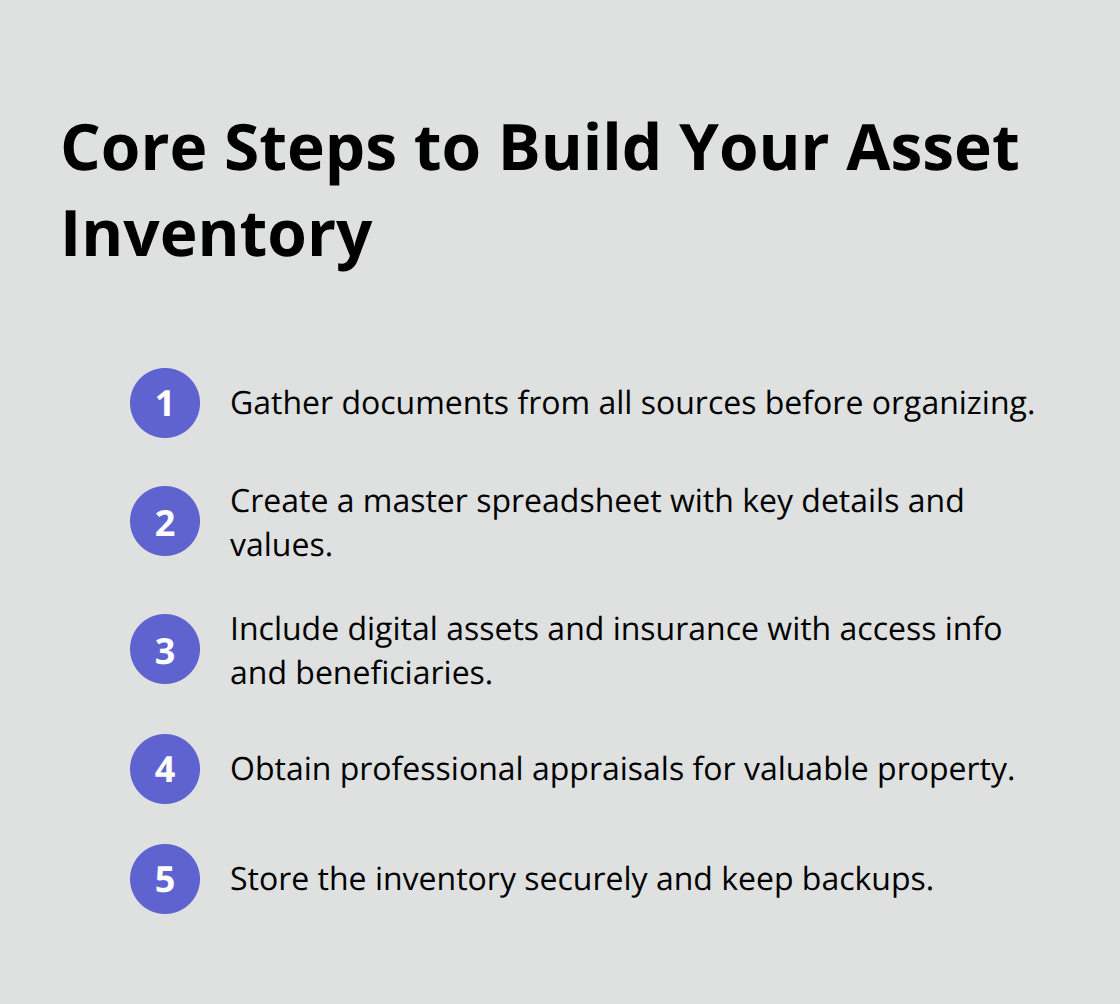

You must collect every document you can find before you organize anything. Bank statements from the past year, property deeds, vehicle titles, investment account statements, insurance policies, tax returns from the last three years, and any correspondence from financial institutions all belong in one place. Open every drawer, check the safe deposit box, and search email accounts for account statements and confirmation emails. This foundational step takes time, but it prevents the costly mistakes that emerge later when assets surface unexpectedly.

The American Bar Association found that executors who spent an average of 15 to 20 hours on initial document collection reduced probate delays by nearly half.

Create Your Master Spreadsheet

You need a master spreadsheet with separate columns for asset type, description, account number or identifying details, institution or location, and estimated fair market value. For real estate, you should include the property address, the legal description from the deed, and the assessed value from county tax records as a starting point. For bank and investment accounts, you must record the institution name, account type, and the balance as of the date of death. For vehicles, you can use Kelley Blue Book or Edmunds to establish fair market values based on make, model, year, and condition.

Account for Digital Assets and Insurance

Digital assets demand the same rigor as physical property. Cryptocurrency holdings, domain names, social media accounts with commercial value, and online storage accounts must appear in your inventory with access information or at least a note about where credentials are stored. Many families lose thousands in cryptocurrency alone because no one knew the wallet existed or had the password. Insurance policies, whether life insurance or property coverage, belong in the inventory with the policy number, issuer, face amount, and named beneficiaries clearly documented. Retirement accounts like IRAs and 401(k)s must be listed separately with their beneficiary designations noted, since these assets often pass outside probate but still require accounting in the overall estate picture.

Obtain Professional Appraisals

Professional appraisals are non-negotiable for items of significant value. Jewelry, artwork, collectibles, and antiques should be appraised by qualified professionals who provide written documentation of their findings. County assessor records provide valuations for real property, though you may need independent appraisals if the property’s value has changed substantially since the last assessment. These documented values protect the estate from disputes and satisfy tax authorities when the time comes.

Protect Your Inventory With Secure Storage

You must store all critical documents together in multiple locations-a copy with your attorney, a copy in a fireproof safe, and a digital copy in a password-protected cloud service. You should update the inventory whenever major life changes occur, such as acquiring new property, opening investment accounts, or receiving inheritances. An inventory that remains current throughout your lifetime eliminates scrambling and guesswork when it matters most. With your asset inventory complete and properly stored, you’re ready to address the documentation mistakes that derail many estates and how to avoid them.

Common Mistakes People Make With Asset Documentation

Most executors treat asset documentation as a one-time task completed when probate opens, then abandon it. This approach creates cascading problems that surface months or years into administration. Your inventory becomes outdated the moment you stop maintaining it, and outdated records undermine the entire purpose of having created one in the first place. An inventory that reflects assets from five years ago but misses recent purchases, closed accounts, or transferred properties gives the court and beneficiaries an incomplete picture of what actually existed at death.

Update Your Records When Life Changes

Courts in California expect executors to file amendments when discoveries surface, and each amendment extends probate timelines and increases legal costs. The solution requires you to treat your asset documentation as a living document that you review and update whenever significant changes occur in your life. Every time you purchase real estate, open an investment account, acquire valuable items, or change beneficiary designations on insurance policies, your inventory needs updating. This ongoing maintenance takes perhaps one hour per year but prevents the urgent scrambling that happens when an executor inherits disorganized records and must reconstruct years of financial activity under time pressure.

Store Documents in Multiple Secure Locations

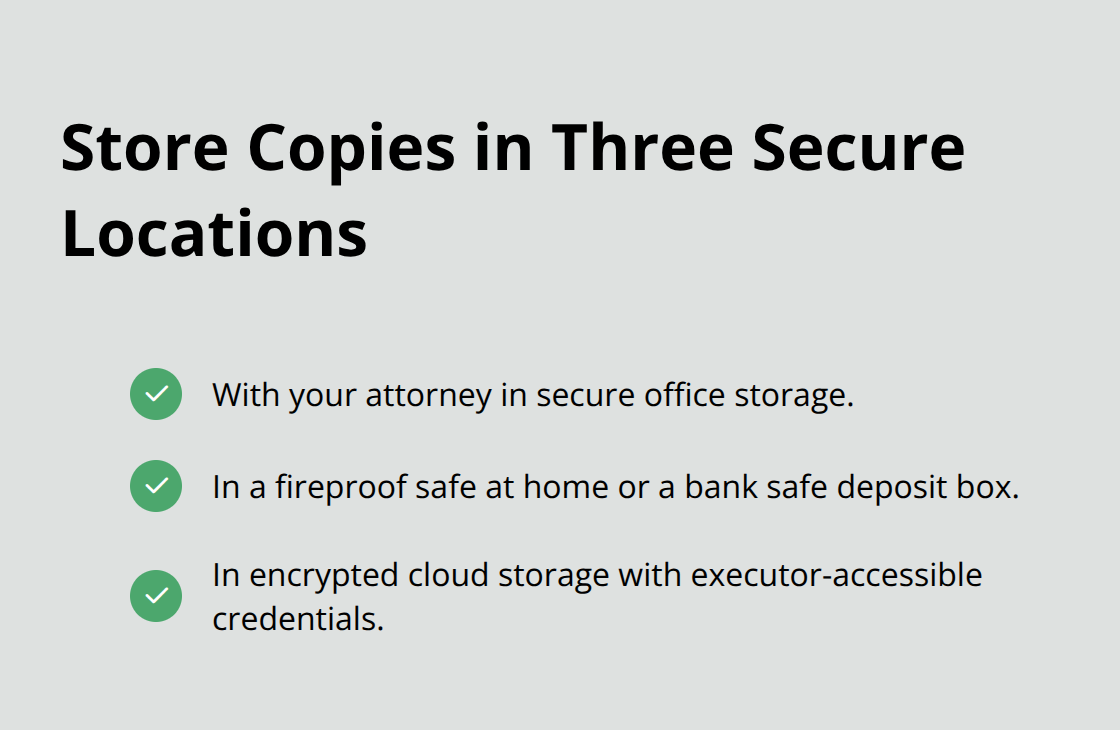

Keeping everything in a single desk drawer or filing cabinet means that if your home floods, burns, or is burglarized, your entire estate planning infrastructure vanishes. You should maintain three copies: one with your attorney in their secure office storage, one in a fireproof safe at home or a bank safe deposit box, and one in encrypted cloud storage with a password your executor can access after your death. This redundancy protects your estate from catastrophic loss and ensures that your executor can locate critical information when needed.

Protect Digital Assets and Credentials

Digital assets present a unique storage challenge because traditional document repositories don’t capture cryptocurrency wallets, online account credentials, or access information for social media accounts with commercial value. Many executors discover cryptocurrency holdings months after probate closes because the wallet address was stored in a notebook buried in a desk drawer or written on a piece of paper in a file folder. Your inventory spreadsheet must include not just asset descriptions and values but also the specific location of credentials, passwords stored in a password manager, or instructions for accessing digital holdings. Without this information, digital assets often become permanently inaccessible, representing complete loss to the estate.

Maintain Your Inventory as a Living Tool

The discipline of maintaining updated records in multiple secure locations transforms your inventory from a compliance document into an actual tool that protects your beneficiaries and simplifies administration when it matters most. You accomplish this by scheduling annual reviews of your asset list, updating values for significant holdings, and noting any new accounts or properties you’ve acquired. Your executor will inherit a clear, current picture of your financial life rather than scattered documents and forgotten accounts that require months to reconstruct.

Final Thoughts

Starting your probate administration asset inventory today eliminates the scrambling that derails most estates. When you organize your assets now, you give your executor a clear roadmap and your beneficiaries the confidence that their inheritance stays protected. The 40% reduction in probate timelines that comes with comprehensive documentation translates directly into lower legal fees and faster distributions to heirs.

The practical next step is straightforward: gather your documents this week, create your master spreadsheet, and schedule annual reviews to keep everything current. Store copies in three locations, document your digital assets with access information, and obtain professional appraisals for valuable items. This foundation takes perhaps 20 hours of your time now but saves your executor months of reconstruction work and protects your family from disputes that could cost thousands in legal fees.

We at Law Offices of Roshni T. Desai understand that probate administration feels overwhelming when you’re starting from scratch. Contact us today for a free consultation, and let’s get your estate organized so your family can focus on what matters most.