A Clear Guide to Trust Administration Steps for Heirs and Executors in Santa Ana, California

Inheriting a trust or serving as an executor brings real responsibilities and complex decisions. At Law Offices of Roshni T. Desai, we help Santa Ana residents navigate trust administration steps with clarity and confidence.

This guide walks you through each phase of the process, from reviewing documents to distributing assets to heirs. You’ll learn how to handle common obstacles and when to bring in professional support.

What Trust Administration Really Means

Trust administration is the legal and financial process of managing a deceased person’s trust assets, paying debts and taxes, and distributing remaining property to beneficiaries according to the trust document. Unlike probate, which moves through the court system and takes 12 to 18 months on average in California, trust administration happens outside court and typically completes faster when structured properly. As successor trustee or executor, you safeguard assets, notify beneficiaries within 60 days of death, inventory all property, obtain professional valuations for significant items like real estate, and maintain detailed records of every transaction. Your fiduciary duty is absolute-you must act in the best interests of all beneficiaries, follow the trust terms exactly, and comply with California Probate Code requirements. This means you cannot take shortcuts, hide information, or prioritize one beneficiary over another. Many trustees underestimate the scope of this role and assume it’s simply paperwork, but in reality, you manage potentially millions in assets while navigating tax deadlines, creditor claims, and family dynamics. The administration process typically spans 6 to 12 months for straightforward trusts, though complex estates with multiple properties, business interests, or disputed beneficiary claims can extend beyond two years.

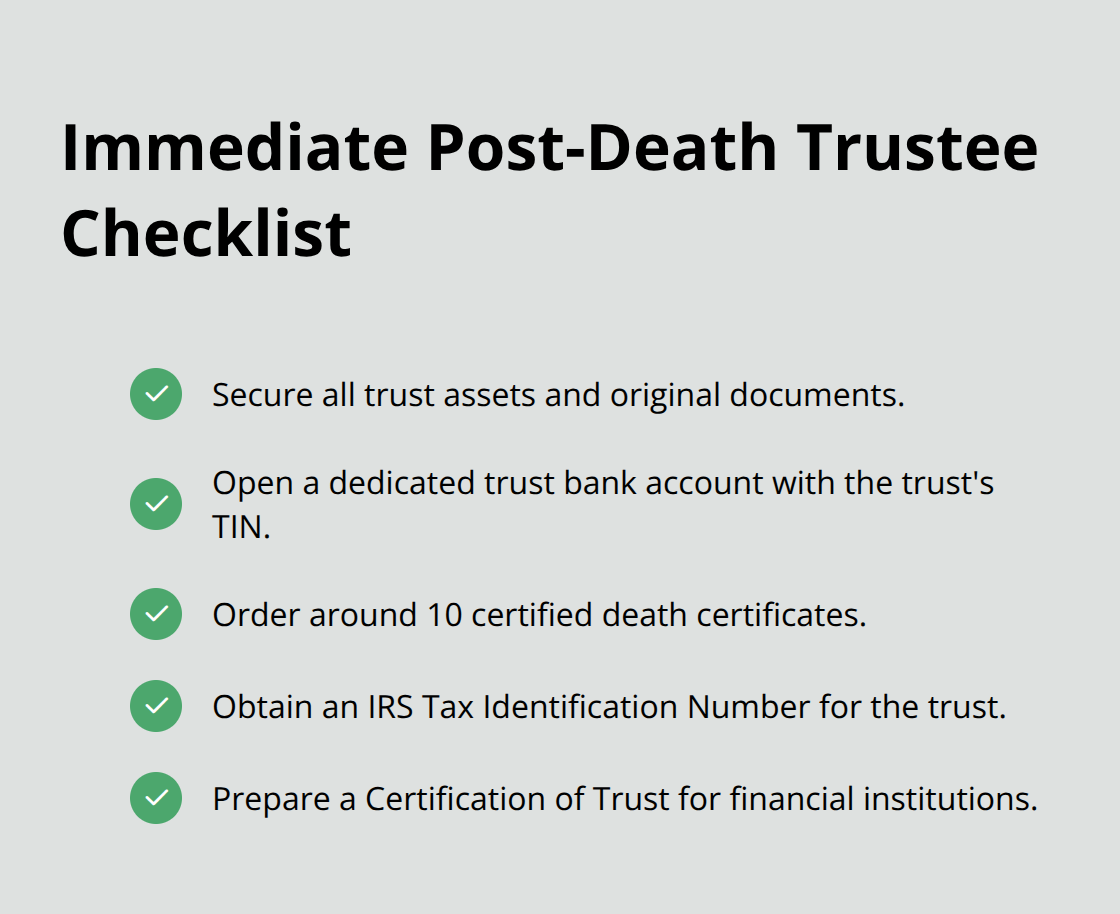

Immediate Actions After Death

You must locate the original trust document and supporting papers immediately and secure all trust assets. Open a dedicated trust bank account using the trust’s tax identification number to separate trust finances from personal funds.

Order multiple death certificates-typically around 10-because banks, title companies, and government agencies each require originals. Obtain a Tax Identification Number from the IRS for the trust and prepare a Certification of Trust to provide to financial institutions. These initial steps establish the foundation for everything that follows and prevent delays in accessing accounts or transferring property.

Inventorying Assets and Valuations

Inventory every asset: bank accounts, investment portfolios, real estate, vehicles, business interests, and personal property with monetary value. For real property, obtain professional appraisals to establish fair market value, which affects both tax calculations and equitable distributions to heirs. Create a comprehensive spreadsheet listing each asset, its location, current title holder, and estimated value. This documentation protects you from disputes and provides beneficiaries with transparency about what the trust contains.

Managing Debts and Tax Obligations

Pay all valid creditor claims within the 120-day window California law provides. File the deceased’s final income tax return and the trust’s fiduciary return on time to avoid penalties. Reserve funds for any estate taxes owed and coordinate with a tax professional to understand capital gains implications and trust tax bracket considerations. Proper tax planning at this stage can significantly reduce what beneficiaries ultimately owe.

Communicating With Beneficiaries

Communicate transparently with beneficiaries about asset status, distribution timing, and amounts. Provide them with copies of the trust document, regular updates on administration progress, and detailed accounting of all income and expenses. This transparency prevents misunderstandings and reduces the likelihood of disputes that can spiral into expensive litigation. Beneficiaries have the legal right under California Probate Code to information about trust assets, liabilities, and transactions, so proactive disclosure protects both the trust and your position as trustee.

With these foundational responsibilities in place, you’re ready to move into the specific steps that guide the entire administration process-from the initial document review through final asset distribution.

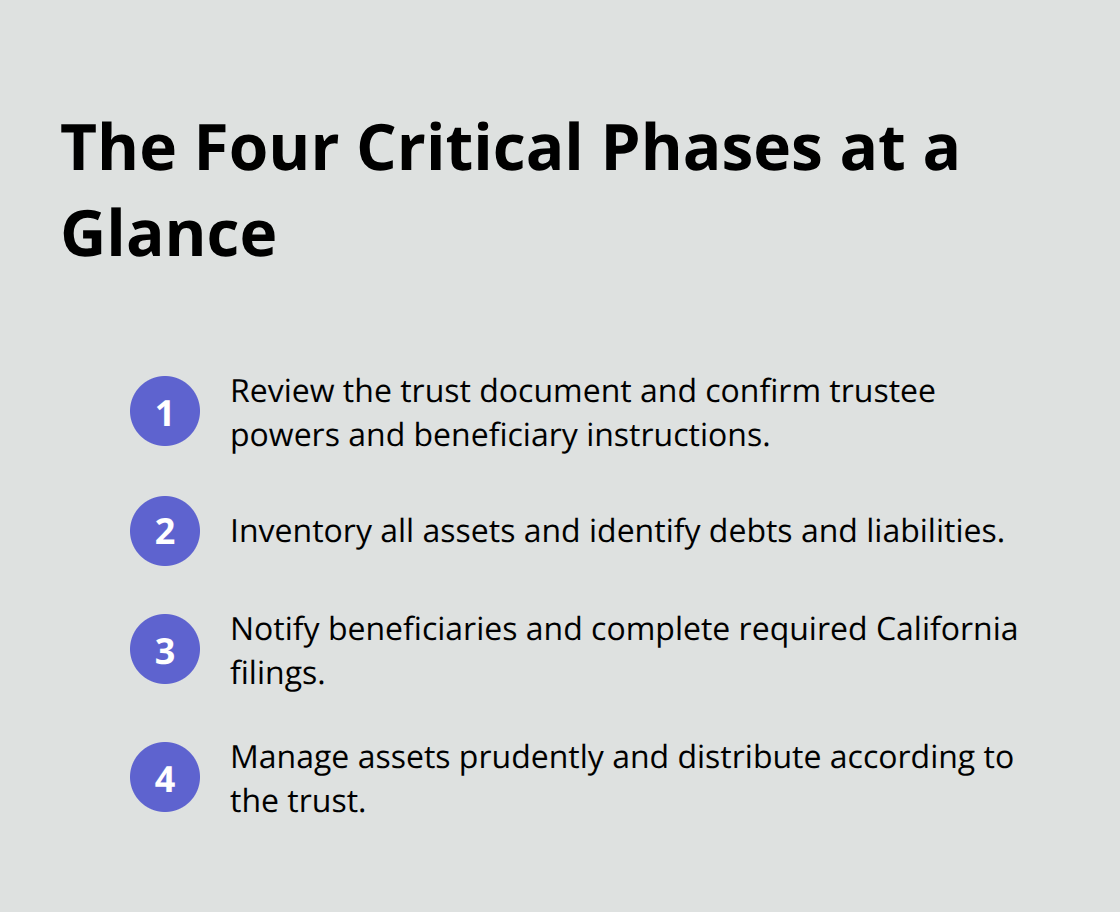

The Four Critical Phases of Trust Administration

The foundation of solid trust administration rests on four interconnected phases that must happen in sequence. You locate and thoroughly review the trust document to understand what you’re managing and what the grantor intended. You inventory every asset and identify all debts owed by the trust or the deceased. You notify beneficiaries and file the legally required documents with California authorities. You manage those assets strategically and distribute them according to the trust’s terms.

Skip or rush any of these phases and you risk beneficiary disputes, tax penalties, or personal liability. The entire process typically takes 6 to 12 months for straightforward trusts, but complexity adds time. A trust with multiple properties, business interests, or contested beneficiary claims can stretch to two years or beyond. The key is treating each phase with the attention it deserves rather than treating trust administration as a single monolithic task.

Finding and Understanding Your Trust Document

The original trust document is your roadmap. Without it, you cannot act legally as trustee. Locate the signed, original document first-not a photocopy or digital scan-because banks and title companies require verification of the original. Review the entire document carefully, paying special attention to the grantor’s specific instructions about asset distribution, trustee powers, and any conditions beneficiaries must meet to receive their inheritance. Note whether the trust includes an A/B trust structure or exemption trust provisions, as these affect funding decisions and tax planning. Identify the successor trustee named after you in case you need to step down, and confirm the beneficiaries listed. Look for any special instructions about specific assets-for example, some grantors leave their family home to one child and investment accounts to another. These details matter enormously because distributing assets incorrectly exposes you to lawsuits from beneficiaries who received less than entitled. If the trust document is unclear or contains contradictory language, consult an attorney before proceeding. California Probate Code Section 16061.7 requires you to provide beneficiaries with a copy of the trust document upon request, so transparency about what the document says prevents later disputes about your interpretation.

Creating a Complete Asset Inventory and Valuation Plan

Inventory work separates amateur trustees from effective ones. Create a detailed spreadsheet listing every asset the trust owns: bank accounts with account numbers and balances, investment portfolios with current values, real property with addresses and estimated values, vehicles with VIN numbers, business interests, life insurance policies, and personal property with monetary value. For each asset, note how it’s currently titled and whether it transferred into the trust properly during the grantor’s lifetime. Many families discover that probatable assets-those titled only in the deceased’s individual name-were never funded into the trust, which triggers the need for a Heggstad petition to transfer them into the trust through court order. This discovery process takes time but prevents costly errors later. Obtain professional appraisals for real estate and valuable items like artwork or collectibles, as these valuations establish fair market value for tax calculations and ensure equitable distributions when multiple heirs exist. The IRS requires date-of-death valuations for any estate exceeding the federal exemption threshold, currently 13.61 million dollars for deaths in 2024. Even estates below this threshold benefit from proper valuation documentation because beneficiaries receive a step-up in basis to the date-of-death value, which reduces capital gains taxes if they later sell inherited assets. Track every appraisal expense and receipt because these costs become part of the trust’s administration expenses and reduce what beneficiaries ultimately receive.

Notifying Beneficiaries and Meeting Legal Deadlines

California law requires you to notify beneficiaries within 60 days of the grantor’s death using the formal Notice of Death under Probate Code Section 16061.7. This notice must include the beneficiary’s name, the date of death, your name and contact information, and a statement that beneficiaries have the right to request a copy of the trust document and an accounting of trust activities. Failure to provide this notice can result in lawsuits against you personally, even if the trust has sufficient assets to cover claims. File a Change of Ownership Report with the Orange County Assessor’s office if the trust owns real property, as this triggers property tax reassessment under Proposition 13. If adult children inherited the family home from a parent, file a Claim for Reassessment Exclusion to preserve the parent’s lower property tax basis and avoid unexpected tax increases. Lodge the original will with the Probate Court within 30 days of death if one exists, even if most assets are in the trust. Notify known creditors in writing and publish a notice to creditors in a local newspaper to trigger California’s 120-day claims period. During this window, creditors can file claims against the trust for debts owed by the deceased. Legitimate claims must be paid before distributions go to beneficiaries, so reserve adequate funds. Open a dedicated trust bank account using the trust’s tax identification number and deposit all trust funds there, keeping trust money completely separate from your personal accounts. This separation protects you from commingling accusations and makes record-keeping transparent.

Strategic Asset Management and Distribution Timing

Managing trust assets means more than simply holding them until distribution time. You must maintain insurance on real property, pay property taxes on time, manage investment accounts prudently, and preserve liquidity to cover ongoing expenses and tax obligations. If the trust owns a home, you ensure property taxes, homeowners insurance, and necessary maintenance continue without interruption. If the trust holds business interests, you decide whether to operate the business, sell it, or transfer it to a designated beneficiary. Business valuations often require professional appraisers, and the decision to sell versus transfer affects both tax liability and beneficiary outcomes. Before you distribute assets, file the deceased’s final Form 1040 income tax return and the trust’s Form 1041 fiduciary return with the IRS. Pay any income taxes owed from trust funds. If the estate exceeds the federal exemption threshold, you may need to file a Form 706 estate tax return, which requires careful coordination with a tax professional. Distribute assets in stages rather than all at once. Make primary distributions to beneficiaries once debts, taxes, and major expenses are paid, but hold back a reserve for any final claims or unexpected costs. Provide each beneficiary with a detailed accounting showing all income received, expenses paid, assets distributed, and the value of their distribution. This accounting becomes your legal protection if a beneficiary later challenges your actions. If all beneficiaries agree, they can waive the 120-day creditor claims period to receive distributions sooner, but get this waiver in writing. Once all distributions are complete and final tax returns are filed, formally close the trust by filing a notice of trust termination and maintaining distribution records for at least seven years in case of future disputes or tax audits. With these four phases executed properly, you’ve laid the groundwork for a smooth administration-but real-world trust management often surfaces obstacles that test even the most organized trustee.

Real Obstacles That Derail Trust Administration

Beneficiary Disputes and Communication Failures

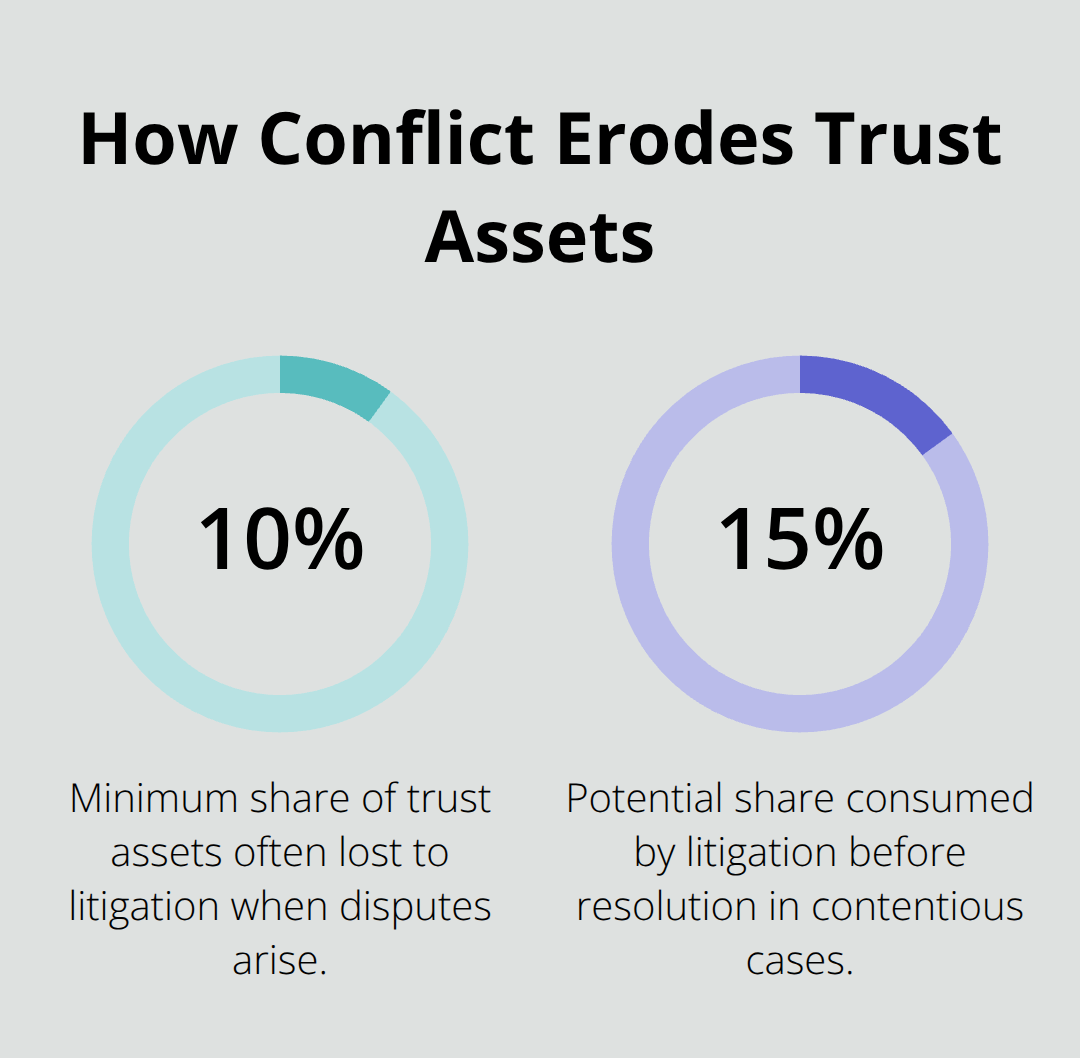

Beneficiary disputes emerge as the top reason trust administration stalls or becomes expensive. When one heir believes another received preferential treatment or when the trustee’s decisions seem unfair, litigation costs consume 10 to 15 percent of trust assets before resolution. The primary trigger for disputes is poor communication early in the process. If beneficiaries don’t understand why certain assets sold at specific prices or why distributions arrived on particular timelines, they assume misconduct.

Prevent this through written accounting statements provided quarterly, not just at the end of administration. Include itemized lists of expenses, asset valuations, and the reasoning behind major decisions like selling real estate or liquidating investment accounts. When beneficiaries see detailed documentation showing every transaction, suspicion diminishes significantly. If disagreement does arise over distribution amounts or trustee conduct, mediation costs far less than litigation. A mediator in Orange County typically charges 200 to 400 dollars per hour, and most disputes resolve in two to four sessions. Court litigation for trust disputes averages 30,000 to 75,000 dollars in attorney fees alone, with trials extending timelines by months or years. Choose mediation first, always.

Tax Compliance and Reporting Deadlines

Tax compliance issues create another major pitfall because trustees often miss deadlines or misunderstand reporting requirements. The trust’s Form 1041 fiduciary return must file by April 15 following the calendar year of the grantor’s death, and late filing triggers penalties of 25 dollars per month for each month late, capped at 100 dollars. The deceased’s final Form 1040 must file by the same deadline. If the estate exceeds 13.61 million dollars, federal estate tax Form 706 must file within nine months of death, and missing this deadline costs thousands in penalties and interest. Many trustees assume they only need to file taxes once, but if the trust generates income during administration, the trustee must file annual Form 1041 returns every year until the trust closes. Coordinate with a tax professional immediately after death, not months later. This coordination prevents costly errors and ensures the trust meets every filing requirement on schedule.

Property Tax Reassessment and Proposition 13 Implications

Real property valuations present another compliance challenge because California’s Proposition 13 reassesses property when ownership changes. If the trust transfers real estate to a beneficiary, the county assessor recomputes property taxes based on current market value, not the deceased’s original purchase price. A home purchased for 300,000 dollars thirty years ago might reassess to 1.2 million dollars in today’s market, triggering property tax increases of hundreds of dollars monthly. Some transfers qualify for exemptions. If a parent’s home transfers to a child, filing a Claim for Reassessment Exclusion within three years preserves the parent’s lower tax basis. This exemption saves beneficiaries thousands over time but requires proactive filing. Without this action, beneficiaries face unexpected tax burdens that reduce the value of their inheritance.

Complex Assets and Distribution Challenges

Managing complex or illiquid assets demands tactical decisions that affect both tax liability and distribution fairness. If the trust owns a family business, you cannot simply hand it to the designated beneficiary without addressing valuation, tax implications, and operational continuity. Business valuations require professional appraisers who charge 3,000 to 10,000 dollars depending on the business size and complexity. The IRS scrutinizes business valuations on estate tax returns, so documentation from a qualified appraiser protects you from future audit challenges. If multiple beneficiaries exist and only one receives the business, the trustee must ensure equal distribution through compensation to other heirs with cash or other assets. This often requires liquidating portions of the portfolio or arranging loans, adding complexity and cost. Real estate similarly creates distribution challenges when one beneficiary wants to keep the family home while others prefer cash. You cannot force a beneficiary to accept real property if they prefer liquidity. Instead, either sell the property and distribute proceeds equally, or arrange for the beneficiary keeping the home to compensate others through installment payments or other asset transfers.

When Professional Guidance Becomes Essential

When professional guidance becomes necessary, many trustees hesitate to hire attorneys or accountants because they fear added costs. This thinking backfires consistently. A 5,000 dollar attorney consultation upfront prevents 40,000 dollars in litigation costs later. Trustees should hire counsel immediately if the trust exceeds 500,000 dollars in assets, contains real property, involves business interests, or names multiple beneficiaries with potential conflicting interests. The cost of professional guidance is paid from trust assets, meaning beneficiaries ultimately bear the expense regardless, so delaying professional help does not save money. It only increases the final cost.

Final Thoughts

Trust administration steps demand patience, organization, and honest assessment of what you can handle alone versus what requires professional support. The four phases outlined in this guide-locating documents, inventorying assets, notifying beneficiaries, and managing distributions-form the backbone of every successful administration. You now understand that this process typically spans 6 to 12 months for straightforward trusts, though complexity extends timelines significantly, and you recognize the legal deadlines that cannot slip without triggering penalties.

The most important decision you’ll make as trustee is recognizing when to bring in professional guidance. If the trust exceeds 500,000 dollars, contains real property, or involves multiple beneficiaries with competing interests, hiring an attorney immediately protects both the trust and your personal liability. Tax professionals become essential when the estate approaches federal exemption thresholds or when the trust generates ongoing income during administration, and these professionals are paid from trust assets, so their cost does not come from your pocket.

We at Law Offices of Roshni T. Desai understand the weight of trustee responsibilities and the complexity Santa Ana families face when managing trust administration. If you’re managing a trust and need clarity on next steps, contact Law Offices of Roshni T. Desai to schedule your consultation and move forward with confidence.