California Trust Administration Updates: Staying Compliant in a Changing Law Landscape

California trust administration updates have created new compliance obligations for trustees. The rules changed significantly in 2024, and many trustees are still catching up with what’s required.

At Law Offices of Roshni T. Desai, we’ve seen firsthand how these changes affect trust management. This guide walks you through the updates and shows you how to stay compliant.

What Changed in California Trust Administration in 2024

The UDTA and UFIPA Framework Now Governs Directed Trusts

California’s Uniform Directed Trust Act and Uniform Fiduciary Income and Principal Act took effect January 1, 2024, and they fundamentally changed how trustees manage certain trusts. The UDTA applies to directed trusts-arrangements where a trustee delegates investment, distribution, or other decisions to a directed trustee or advisor. The UFIPA gives trustees more flexibility in managing income and principal. Trustees can now convert income trusts to unitrusts under specific conditions, and they have broader authority to allocate tax receipts and distributions. This flexibility creates a real compliance burden. If your trust document doesn’t clearly spell out whether a directed trustee has exclusive authority or shared authority with the main trustee, the statute fills in the gaps-and those gaps may not match your original intentions. Review trust language immediately to confirm whether your trust is a directed trust and whether modification methods are explicitly exclusive.

The Haggerty v. Thornton Decision Exposed a Major Modification Risk

The California Supreme Court’s Haggerty v. Thornton decision from February 8, 2024 settled a major question: if your trust doesn’t state that the modification method is exclusive, beneficiaries or other parties can use the statutory revocation and modification procedure even if another method is described in the document. This means trusts drafted before 2024 may now face unintended modifications unless the trust language explicitly blocks statutory methods. Trustees who fail to address this gap expose themselves to challenges they never anticipated. The decision applies to all trusts, regardless of when they were created, so older trust documents need immediate attention.

Probate Thresholds and Real Property Transfer Rules Shifted in 2025

AB 2016 increased California’s small estate probate threshold for real property to $750,000 effective January 1, 2025. This sounds like a win for avoiding probate, but the reality is more complicated. The Petition to Determine Succession to Real Property applies only to a decedent’s primary residence valued at or below $750,000-not to vacation homes, rental properties, or investment real estate. You must also give notice to every intestate heir, beneficiary, and devisee named in the petition, which increases administration costs and can trigger additional claims. The Small Estate Affidavit for personal property remains at $184,500 and still offers a streamlined path.

The notice requirement under AB 2016 can be a trap. Many trustees assume the higher threshold means simpler administration, but the notice obligation means you cannot quietly transfer property. If you fail to give proper notice, heirs or other claimants can challenge the transfer later. Treat the $750,000 threshold as a starting point for conversation with an attorney, not as a green light to skip legal review. For estates with multiple properties, out-of-state real estate, or complex family situations, the savings from a higher threshold evaporate quickly once you account for proper notice procedures.

Professional Fiduciary Registration and Trustee Accountability Tightened

AB 2148, also effective in 2024, requires professional fiduciaries to register with California’s Professional Fiduciaries Bureau and allows them to organize as professional corporations. Courts can no longer appoint unregistered fiduciaries. This change matters because it raises the bar for who can serve as a trustee or estate administrator. If your trust names a professional fiduciary as successor trustee, confirm that person or firm is registered. If your trust names a family member or friend, the stricter standards for professional fiduciaries do not directly apply-but the heightened regulatory environment means courts expect higher performance from all trustees.

Documentation becomes even more important in this new landscape. Keep detailed records of how you manage assets, communicate with beneficiaries, and handle distributions. The tighter regulatory environment means that sloppy administration exposes you to removal and personal liability more readily than it did before 2024. These compliance shifts set the stage for understanding what trustees must actually do to stay on the right side of California law.

What Trustees Must Actually Do to Stay Compliant

Core Fiduciary Duties Under California Law

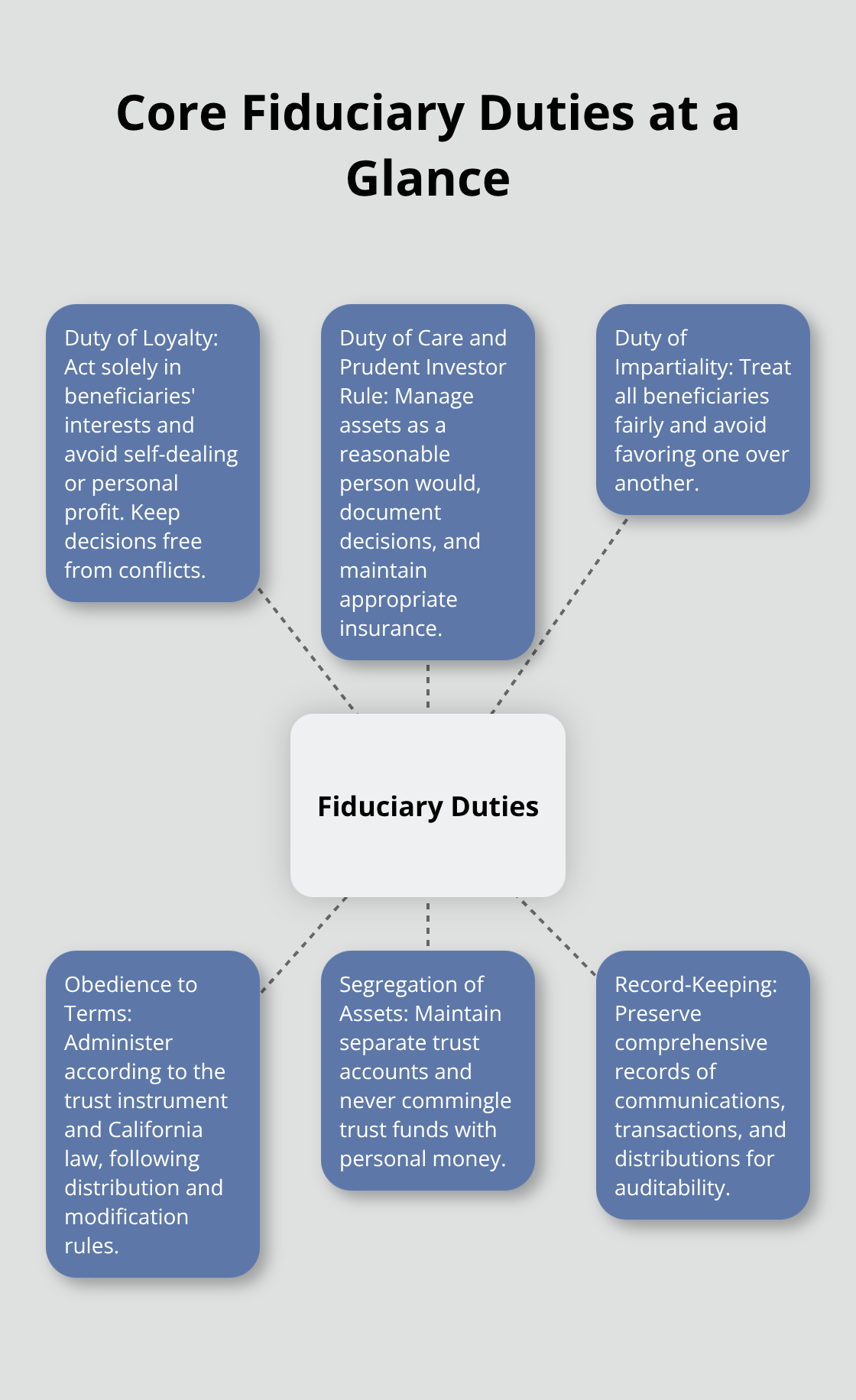

California Probate Code sections 16000 and 16002 require trustees to administer trusts according to the trust document and state law, but compliance runs far deeper than reading the fine print once. Your fiduciary duty is absolute: you must act solely in beneficiaries’ interests, avoid personal profit from trust property, refrain from borrowing trust funds, and never commingle trust assets with your own accounts. California Probate Code 16004 codifies the duty of loyalty, and violations carry real penalties-removal from office, personal liability for losses, and court-ordered payment of all parties’ legal fees. The duty of care under Probate Code 16004 and the Prudent Investor Rule in section 16047 requires you to manage assets as a reasonable person would, including securing proper insurance and making documented investment decisions.

The duty of impartiality prohibits you from favoring one beneficiary over another, even if personal relationships tempt you to do so.

Preparing Your Trust Administration Foundation

The 2024 changes amplified these duties because courts now expect trustees to navigate UDTA and UFIPA rules, track whether modification methods are exclusive under Haggerty v. Thornton, and maintain records that prove compliance. Start by reviewing your trust document word-for-word to identify any directed trustee language, modification procedures, and distribution rules. Then create a detailed asset inventory with date-of-death valuations for each property, investment, and account. For real estate held in the trust, record an Affidavit of Death of Trustee and maintain comprehensive insurance coverage and expense records. Apply for a Taxpayer Identification Number or Employer Identification Number for the trust to enable proper tax reporting and separate accounting from your personal finances. Consider publishing a Notice to Creditors in a local newspaper to limit creditor claims-this simple step can prevent surprise liability months or years into administration.

Beneficiary Notification and Accounting Obligations

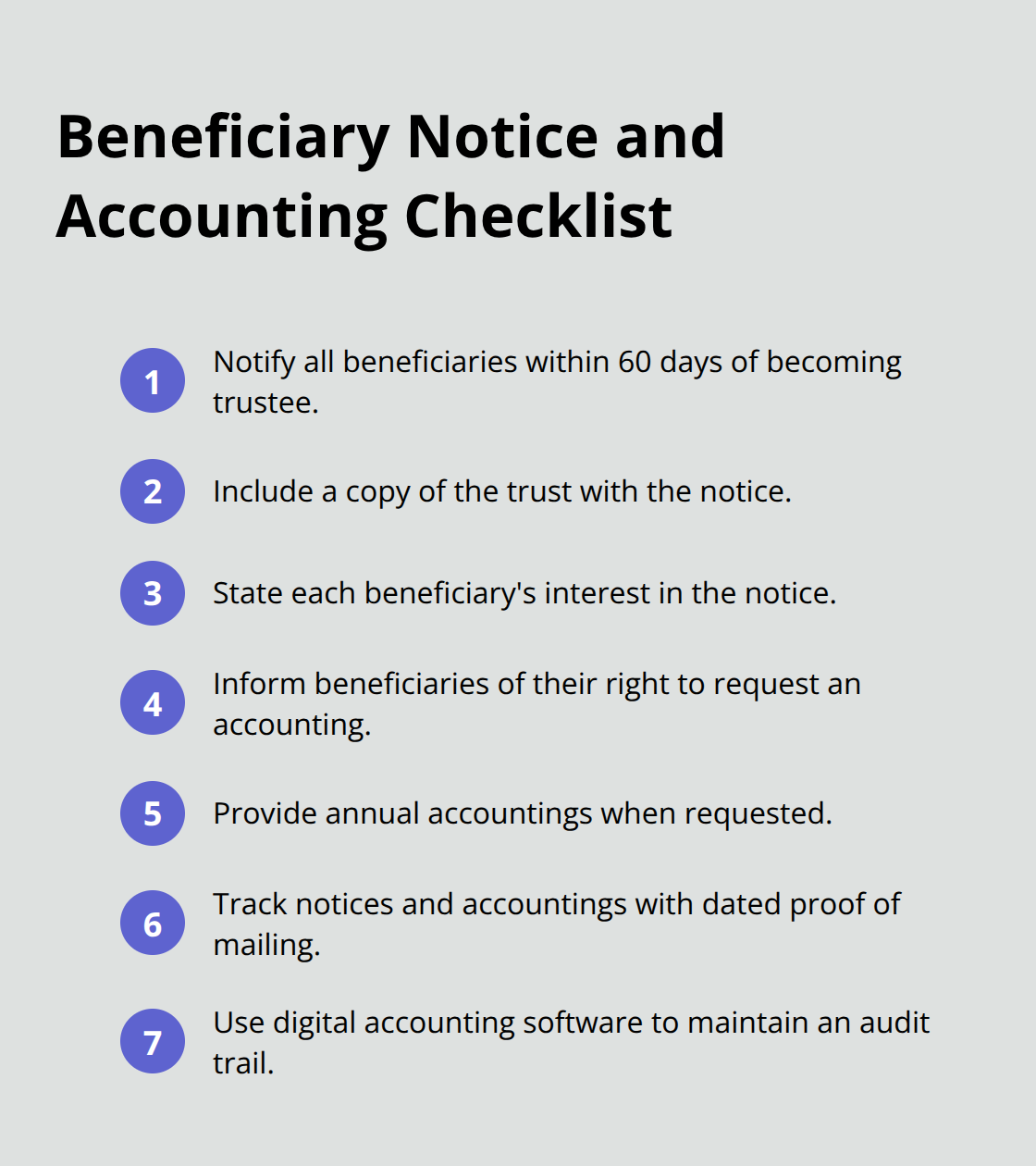

Beneficiary notification and accounting are where trustees stumble most often. California Probate Code 16061.7 requires you to notify all beneficiaries within 60 days of becoming trustee, even if they are not named in the trust document. This notification must include a copy of the trust, a statement of the beneficiary’s interest, and notice of their right to request an accounting.

Annual accountings are not optional if a beneficiary requests them; Probate Code 16062 mandates regular reporting and transparency. Failure to provide timely accountings exposes you to surcharge actions where beneficiaries can recover losses caused by your negligence.

Managing Distributions and Tax Obligations

Distinguish between mandatory distributions, which you must make per the trust language, and discretionary distributions, which you control. For discretionary distributions, document your analysis in writing-why you distributed that amount, to whom, and when. Trustees must obtain signed receipts from beneficiaries for all distributions to protect against future claims that assets were never received. Tax timing matters enormously: trusts face compressed tax brackets and often pay higher rates than individual beneficiaries, so coordinate distribution timing with your tax advisor to minimize overall tax burden. For special needs beneficiaries or those with management difficulties, follow the trust provisions exactly as written; those provisions reflect the settlor’s specific concerns.

Record-Keeping, Co-Trustee Coordination, and Risk Management

Record-keeping is non-negotiable: maintain copies of the trust document and all amendments, track every financial transaction, save all beneficiary communications and advisor correspondence, and keep receipts for every expense. If co-trustees are involved, Probate Code 16013 requires active participation by each one, clear mutual communication, and prompt action if one trustee breaches duties; inaction by one co-trustee can extend liability to all co-trustees. The safest path is to seek court instruction when uncertain, obtain professional help for complex assets or distributions, and stay within your authority at all times. Fiduciary liability insurance may be appropriate for large trusts or those with multiple beneficiaries, providing coverage if a beneficiary sues for breach of duty. These foundational steps position you to handle the specific compliance challenges that arise during trust administration, particularly when beneficiaries question your decisions or when trust assets include complex property holdings.

Where Trustees Go Wrong

The 60-Day Notification Trap

Trustees fail most often not from malice but from underestimating the 2024 compliance changes and the documentation burden they create. The gap between what trustees think they must do and what California law actually requires is where liability lives. Probate Code 16061.7 mandates beneficiary notification within 60 days of becoming trustee, yet many trustees notify beneficiaries months later or skip notification entirely because they assume the trust document alone suffices. That notification must include a copy of the trust, a statement of each beneficiary’s interest, and explicit notice of the right to request an accounting. Failing to meet this 60-day window opens the door to surcharge actions where beneficiaries recover damages for losses caused by your negligence. The cost of a certified letter and a trust copy runs under $50 per beneficiary; the cost of defending a surcharge action reaches tens of thousands of dollars.

Accounting Requests and Record Failures

Annual accountings are not optional if beneficiaries request them under Probate Code 16062, yet trustees routinely ignore written requests because they believe annual accountings are burdensome or unnecessary. Courts disagree. A trustee who skips an accounting after a beneficiary requests one has essentially forfeited any defense against a surcharge claim. The solution is straightforward: send the 60-day notification, include the right-to-accounting language, and prepare written accountings every year without exception. Digital record-keeping systems like QuickBooks Online or similar accounting software eliminate friction from this work and create a clear audit trail that protects you if a beneficiary later disputes your management.

Commingling Funds and Violating the Duty of Loyalty

Asset management and tax compliance trip up trustees because they conflate personal financial habits with fiduciary obligations. A trustee who co-mingles trust funds with personal accounts violates Probate Code 16004’s duty of loyalty, even if no theft occurs and every dollar is accounted for. Courts treat commingling as a breach regardless of intent because it makes auditing impossible and creates the appearance of impropriety. Separate trust bank accounts cost nothing to open and eliminate this entire category of liability.

Missing Tax Deadlines and Losing Portability

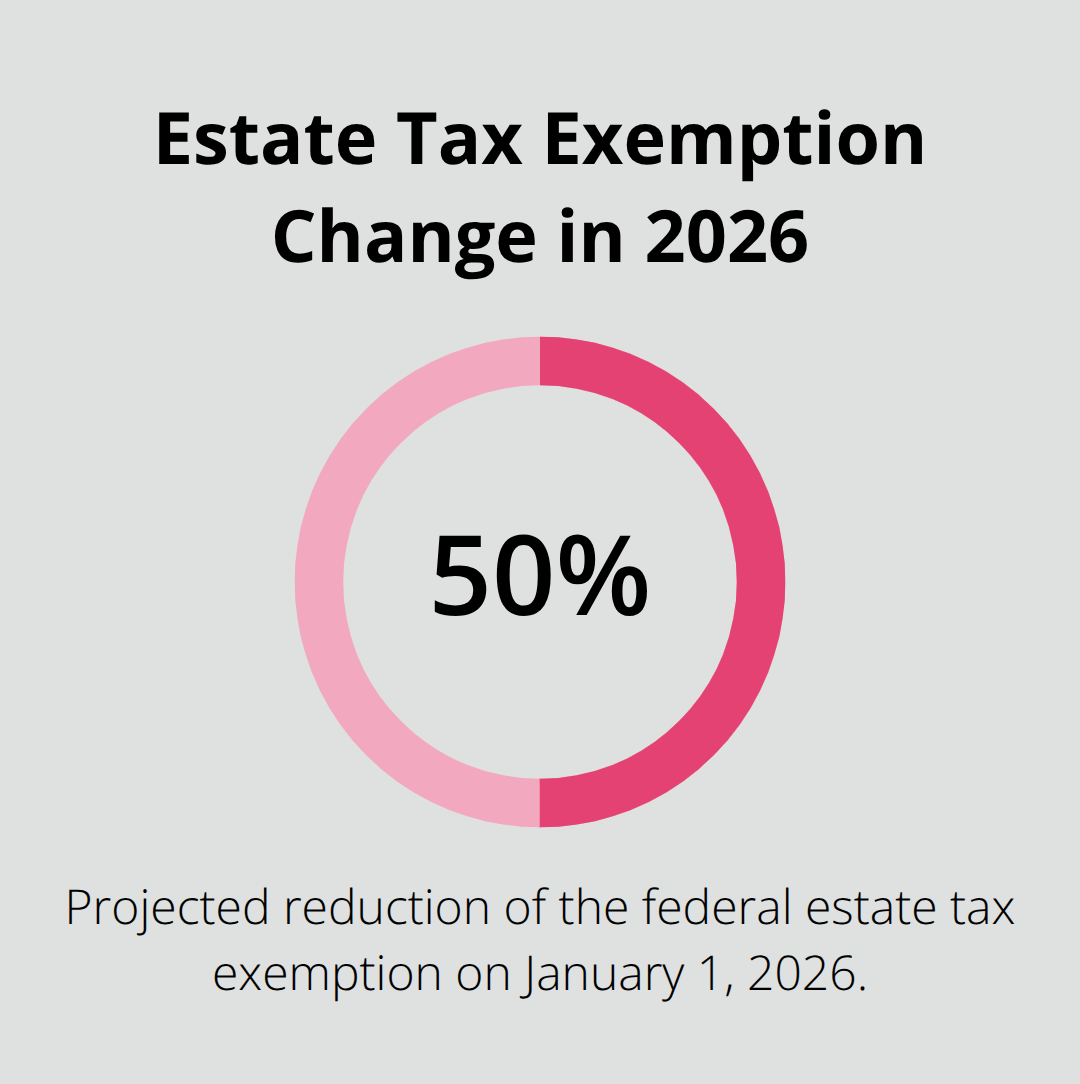

Trustees routinely delay filing tax returns because they assume estate assets take priority, but the IRS does not care about that assumption. A decedent’s final Form 1040 is due by the normal tax deadline (April 15 of the following year), and a fiduciary income tax return Form 1041 is due annually if the trust has income above $600. Missing either deadline triggers penalties and interest that compound monthly. The federal estate tax return Form 706 is due nine months after death if the estate exceeds the current exemption (over $13 million per person in 2025, but projected to drop approximately 50 percent on January 1, 2026, according to IRS projections). Missing that deadline costs you portability of unused exemptions between spouses, a loss that can be worth hundreds of thousands of dollars in future estate taxes.

Hire a CPA or tax attorney immediately after becoming trustee; the cost of professional tax preparation ($1,500 to $5,000 depending on complexity) is trivial compared to the penalties for missed deadlines.

Documentation as Your Defense

Document every distribution, every expense, and every investment decision in writing. If a beneficiary later sues claiming you mismanaged assets, your written record showing careful analysis and professional consultation becomes your strongest defense. This documentation protects you when disputes arise and demonstrates that you acted with the care and diligence California law requires.

Final Thoughts

California trust administration updates in 2024 and 2025 have reshaped what trustees must do to stay compliant. The UDTA and UFIPA framework now governs directed trusts with new flexibility for income and principal allocation. The Haggerty v. Thornton decision means older trust documents face unintended modification risks unless modification methods are explicitly exclusive. AB 2016 raised the probate threshold for primary residences to $750,000, but the notice requirements that accompany it can increase costs and trigger claims. AB 2148 tightened professional fiduciary standards across the board, and these changes affect how you notify beneficiaries, manage assets, file taxes, and document every decision.

Trustees who stay compliant do three things consistently: they notify beneficiaries within 60 days and provide annual accountings without exception, they maintain separate trust accounts and keep detailed records of every transaction and distribution decision, and they file tax returns on time. Trustees who skip these steps expose themselves to surcharge actions, removal from office, and personal liability for losses-costs that far exceed the price of doing things right from the start. Professional guidance matters because California trust law moves faster than most trustees can track alone, and the compressed tax brackets that trusts face, the portability rules that expire on January 1, 2026, and the new virtual representation framework under AB 565 all require coordination with someone who understands both the law and your specific situation.

We at Law Offices of Roshni T. Desai work with trustees across Southern California to navigate these compliance obligations and avoid the mistakes that create liability. Our team provides personalized guidance on trust administration, tax planning, and asset management to help families and trustees stay on track. If you are managing a trust or facing questions about California trust administration updates, contact us for a free consultation to discuss your situation and get clarity on what comes next.