Discretionary Trust Administration: Powers, Roles, and Limitations

Discretionary trust administration gives trustees significant power to make decisions on behalf of beneficiaries. But that power comes with strict legal boundaries and responsibilities that many trustees don’t fully understand.

We at Law Offices of Roshni T. Desai help trustees navigate these complex rules. This guide breaks down what trustees can do, what they must do, and where the law draws the line.

What Trustees Can and Cannot Do With Discretionary Trust Assets

Trustees in discretionary trusts hold expansive powers that go far beyond simply handing money to beneficiaries when asked. A trustee can decide not only when distributions happen, but also whether they happen at all. This flexibility is the entire point of discretionary trusts, but it’s also where trustees often misunderstand their authority. The trust document itself sets the boundaries, and those boundaries matter more than many trustees realize. If your trust deed says distributions must follow Health, Education, Maintenance, and Support (HEMS) standards, you cannot suddenly distribute $500,000 for a luxury vacation just because you feel generous. Courts have consistently rejected trustee arguments that broad discretion means unlimited discretion. In one Virginia case, a trustee tried to distribute trust assets for purposes nowhere mentioned in the trust document and lost.

Impartiality Between Current and Future Beneficiaries

The Uniform Principal and Income Act, adopted in most states, requires trustees to act impartially between current beneficiaries who need income now and remainder beneficiaries who will inherit what’s left. This duty of impartiality is not optional, and violating it can expose you to surcharge actions where beneficiaries sue to recover losses. You cannot favor one group over another without explicit authorization in the trust document. When you make distribution decisions, you must consider how those decisions affect both the beneficiary receiving funds today and the beneficiary who receives the remaining assets later.

Investment Authority Requires Prudent Decision-Making

When managing trust assets, you must invest as a prudent person would under the Uniform Prudent Investor Act. This means considering the trust’s purposes, the distribution requirements, and economic conditions, then making investment decisions with reasonable care, skill, and caution. You cannot simply put all trust money into speculative stocks because past performance was good, nor can you ignore inflation and keep everything in savings accounts. Trustees with special skills in investing must use those skills; if you have a background in finance, courts will hold you to a higher standard than someone without that background. Diversification is expected unless the trust document clearly authorizes concentration in a single asset.

Many trustees delegate investment decisions to financial advisors, which is allowed, but you remain liable for selecting an imprudent advisor and failing to monitor their performance. Documentation of your investment rationale is critical. If you decide to keep 60 percent in bonds and 40 percent in equities, write down why that allocation serves the trust’s purposes. When disputes arise, trustees without documentation lose, even if their decisions were reasonable.

Modification Powers Are Narrower Than You Think

Some trustees believe they can amend trust terms on their own if circumstances change. This is wrong. Only the settlor can modify an irrevocable discretionary trust unless the trust document explicitly grants modification power to the trustee, which is rare. If a trust becomes impractical because property values change dramatically or tax law shifts, you cannot unilaterally fix it. Courts can modify trusts under doctrines like deviation and cy pres, but that requires filing a petition and going before a judge.

What you can do is decant the trust into a new trust if the original trust document permits it. Decanting means distributing trust assets into a new trust with modified terms, which can help with tax planning or adapt to beneficiary needs without court involvement. However, decanting has limits. You cannot decant in ways that harm beneficiaries or violate the original settlor’s intent. If the original trust requires equal distributions to three children and you decant into a trust that favors one child heavily, that crosses the line.

Understanding Your Fiduciary Duties

Your powers as a trustee exist within a framework of fiduciary duties that the law imposes on you automatically. These duties-loyalty, impartiality, prudence, and transparency-are not suggestions. They are enforceable obligations that courts take seriously. A trustee who acts outside the trust document’s terms, fails to document decisions, or treats beneficiaries unequally faces personal liability. The next section covers these fiduciary duties in detail and explains what accountability actually means in practice.

What Trustees Must Actually Do Every Day

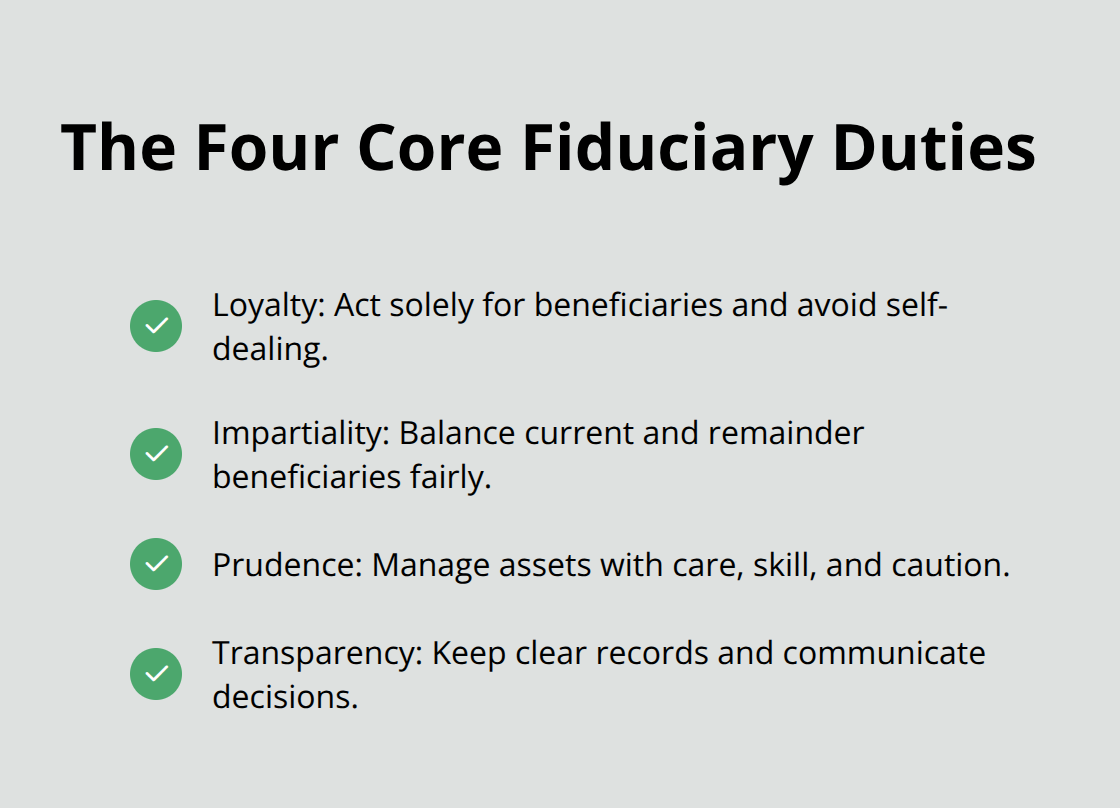

Fiduciary duty sounds abstract until you realize it means you’re personally liable if you get it wrong. The law imposes four core duties on every trustee automatically: loyalty, impartiality, prudence, and transparency.

The Four Core Fiduciary Duties

Loyalty means you administer the trust solely for beneficiaries and never mix trust assets with your own money or steer opportunities to yourself. If you’re a trustee and you own a rental property, you cannot rent it to the trust at inflated rates. If the trust needs investment advice and your brother-in-law offers it for free, you cannot accept without documenting why that choice serves the beneficiaries’ best interest.

Impartiality requires you to balance current beneficiaries who need income distributions today against remainder beneficiaries who inherit what’s left later. Courts interpret this strictly. In one New York case, a trustee distributed heavily to the income beneficiary while ignoring inflation that eroded the principal’s value, and the court surcharged the trustee for breach.

Prudence means you manage investments and trust assets with reasonable care, skill, and caution, considering the trust’s purposes and distribution requirements. Transparency means you keep records that prove you followed all three duties above. Without documentation, even reasonable decisions fail in court. A trustee who invested conservatively to protect principal but never wrote down the investment philosophy loses disputes with beneficiaries claiming the portfolio was too cautious.

Managing Co-Trustee Relationships

You must also act impartially when multiple trustees serve together. If co-trustees disagree on a distribution, you cannot simply override them or ignore their concerns. The trust deed typically specifies how disagreements get resolved-majority vote, unanimous consent, or mediation. Violating this process exposes both trustees to liability.

Annual Reporting and Beneficiary Communication

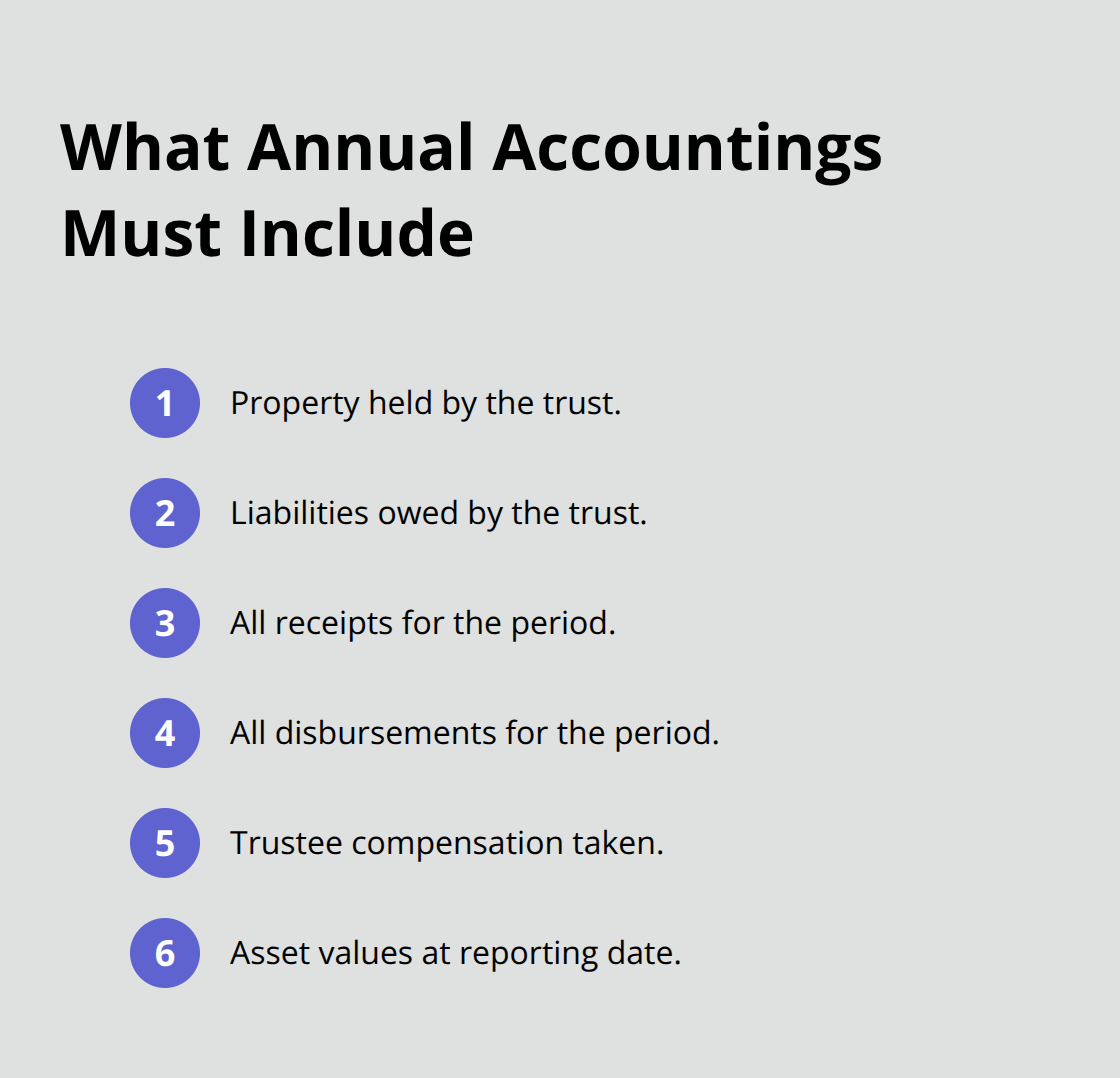

Annual reporting is not optional; state law and the Uniform Trust Code require you to provide qualified beneficiaries with annual accountings that detail property held, liabilities owed, receipts, disbursements, compensation taken, and asset values. You must provide this report within 60 days of accepting the trusteeship and then yearly thereafter. Many trustees skip this or provide vague summaries, which is a mistake. Courts view the annual report as evidence of good faith administration. If a beneficiary sues claiming mismanagement, your detailed annual report showing investment rationale, distribution decisions, and fee justification becomes your strongest defense.

Beneficiaries also have the right to request copies of the trust document itself and to receive notice if the trust becomes irrevocable. Communication beyond the annual report prevents disputes. When a beneficiary asks about a distribution decision, answer directly rather than deflecting. If you deny a request, explain why in writing. If a beneficiary has a disability and needs ongoing support, document how distributions align with that need and how they affect means-tested benefits.

Documentation and Record Keeping Standards

Record keeping transforms administration from guesswork into defensible practice. You must maintain separate bank accounts for the trust and never commingle trust money with personal funds. Every distribution, investment decision, and expense requires documentation with dates, amounts, and the reason. If you invest $200,000 in municipal bonds, write down why that allocation serves the trust’s purposes-whether it’s because the beneficiary needs stable income, the trust’s distribution schedule is predictable, or tax efficiency matters.

When you hire advisors like accountants or financial planners, document the selection process and monitor their performance in writing. If an advisor underperforms, address it or replace them and record your decision. Trusts with multiple assets across different states require you to track who owns what and where. Property titles, account statements, and deed copies should be organized and updated. Many trustees store originals in safe deposit boxes and keep copies at home.

When disputes arise, trustees without documentation lose even when decisions were sound. The effort required is modest-a spreadsheet tracking distributions, a folder for investment statements, and annual summaries take a few hours yearly but protect you from surcharge actions that cost tens of thousands in legal fees. These documentation practices also prepare you for the next critical phase of trust administration: handling the tax obligations and compliance requirements that govern how trusts operate within the broader legal system.

Where Trustee Discretion Ends

Trustee discretion sounds broad until you hit the legal walls that surround it. State law, the trust document itself, and the courts all impose hard limits on what you can actually do. These constraints exist because discretionary trusts benefit from flexibility, but that flexibility cannot become a blank check.

The Trust Document Sets Your Boundaries

The trust document is your primary constraint. If it says distributions must follow HEMS standards, you cannot distribute $100,000 for a vacation home down payment. If it names five specific beneficiaries, you cannot add a sixth person because they seem deserving. Courts in Virginia, New York, and California have consistently held that trustees who exceed their document’s terms face surcharge actions and personal liability.

The Uniform Trust Code, adopted across most states, reinforces this principle by stating that trustees must act in accordance with the trust’s terms and purposes. Your first step before any major decision is to reread your trust document and identify exactly what powers it grants and what limits it imposes. Many trustees skip this step and rely on memory or assumptions, which is how mistakes happen.

State Law Overrides Informal Preferences

State law adds another layer of constraint. The Uniform Prudent Investor Act governs how you must invest trust assets regardless of what the trust document says. You cannot ignore this standard even if the trust gives you broad discretion. Similarly, state trust codes require you to provide annual accountings, maintain separate trust accounts, and act impartially between beneficiary classes.

These duties are mandatory and override informal trustee preferences. If your state’s law requires a trustee to invest with reasonable care and diversification, you must do it. If state law requires annual reporting to beneficiaries, you cannot skip years because you think it is unnecessary.

Courts Intervene When You Exceed Authority

Courts rarely second-guess discretionary decisions made in good faith and within the trust document’s terms, but they intervene immediately when you exceed your authority or act in bad faith. A trustee in California distributed trust funds to pay a beneficiary’s criminal defense attorney, claiming broad discretion to distribute for the beneficiary’s benefit. The court reversed the distribution, finding it outside the trust’s purposes.

Courts also intervene when you fail to act impartially. If the trust requires supporting all three children equally and you distribute 80 percent to one child while ignoring the others, courts will surcharge you for the difference. In most jurisdictions, beneficiaries file a petition in the court where the trust is administered, alleging breach of fiduciary duty, improper distribution, or mismanagement. You then have the burden of proving your actions were proper, which is why documentation matters enormously.

Tax Compliance Constrains Distribution Decisions

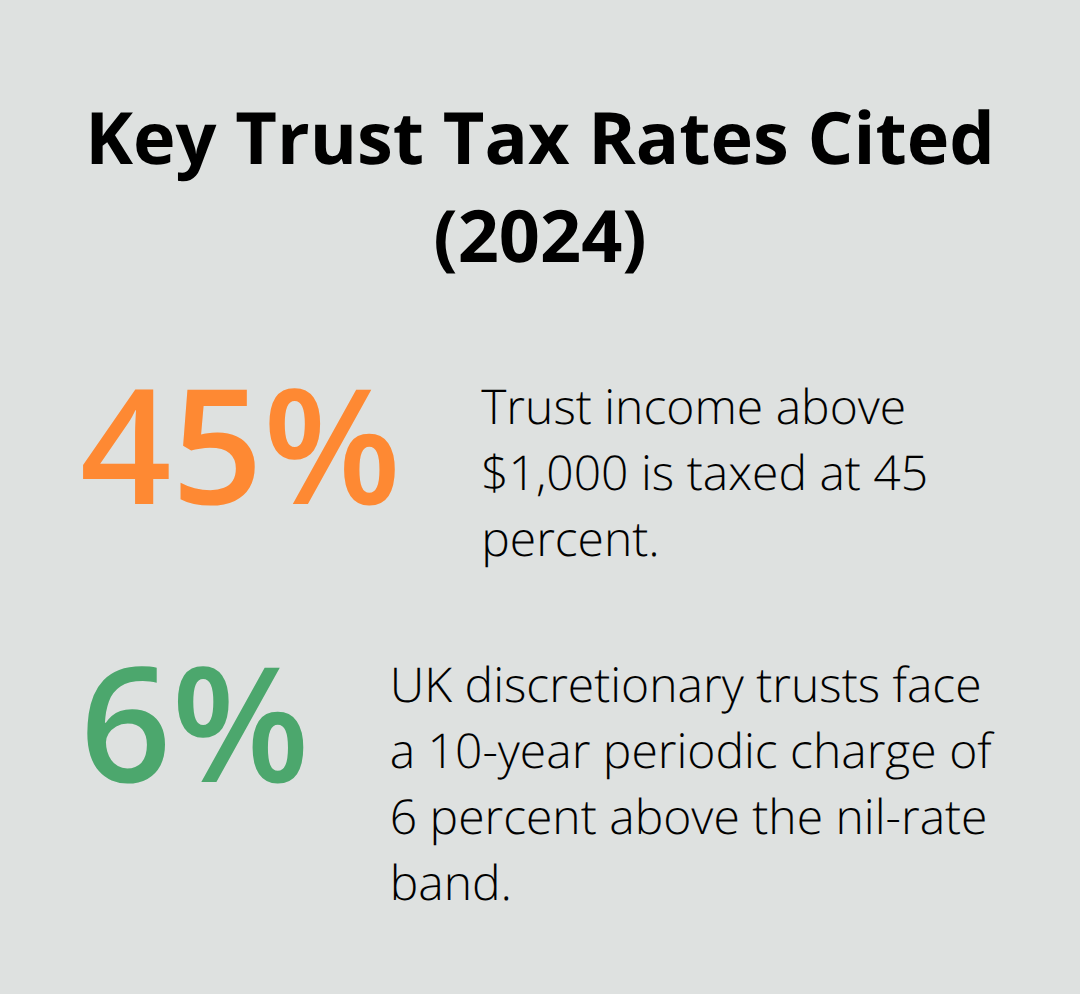

Federal tax law treats discretionary trusts as separate taxpayers with steep income tax rates. Trust income above $1,000 is taxed at 45 percent, and dividend income above that threshold faces a 39.35 percent rate according to 2024 IRS standards. This means your distribution decisions have immediate tax consequences.

Distributing income to beneficiaries in lower tax brackets reduces the overall tax burden, which is legal tax planning. Failing to distribute income and accumulating it in the trust results in crushing tax bills that could have been avoided. You must file annual Form 1041 income tax returns for the trust, and the IRS matches these returns against beneficiary K-1 forms. Mistakes trigger audits and penalties.

Additionally, if the trust holds appreciated assets, selling them triggers capital gains tax. If you hold appreciated stock worth $500,000 that the trust bought for $100,000, selling it generates a $400,000 taxable gain. This tax consequence must factor into your distribution and investment decisions. Many trustees make asset decisions without considering tax impact, then face beneficiary complaints when taxes consume more than expected.

Inheritance tax adds complexity if the trust was created in certain jurisdictions or holds significant assets. Discretionary trusts can trigger immediate inheritance tax charges if assets exceed the nil rate band, currently £325,000 in UK contexts. The trust faces a 10-year periodic charge of 6 percent on value above that band. If the settlor dies within seven years of creating the trust, additional charges apply. These tax consequences mean you cannot simply accumulate income or hold appreciated assets without considering the tax bill. Working with an accountant familiar with trust taxation is not optional for discretionary trusts with substantial income or assets.

Final Thoughts

Discretionary trust administration requires trustees to balance significant power with equally significant responsibility. Throughout this guide, we’ve covered what trustees can do-make distribution decisions, manage investments, and potentially modify trusts through decanting-and what they cannot do without risking personal liability. The trust document sets your boundaries, state law imposes mandatory duties, and courts stand ready to intervene when you exceed your authority or act in bad faith.

The core takeaway is straightforward: discretion is not freedom. Your power to decide when and how to distribute assets exists within strict legal constraints. Loyalty, impartiality, prudence, and transparency are not optional principles-they are enforceable duties that courts take seriously. A trustee who fails to document investment decisions, treats beneficiaries unequally without authorization, or ignores tax consequences faces surcharge actions that cost tens of thousands in legal fees and personal liability for losses.

The complexity of discretionary trust administration-balancing beneficiary needs against tax obligations, managing co-trustee relationships, and navigating state law requirements-makes professional guidance invaluable for anything beyond routine administration. We at Law Offices of Roshni T. Desai help trustees and beneficiaries navigate these rules with personalized guidance tailored to your specific situation.