Discretionary Trust Administration: Understanding Flexible Estate Tools

Estate planning often feels overwhelming when you’re trying to balance control, flexibility, and protection. A discretionary trust offers a powerful way to achieve all three, giving you meaningful say over how your assets are distributed while adapting to changing circumstances.

We at Law Offices of Roshni T. Desai help clients understand discretionary trust administration because it’s one of the most misunderstood planning tools available. This guide walks you through how these trusts work, their real advantages, and the practical challenges you’ll face managing them.

How Discretionary Trusts Actually Work

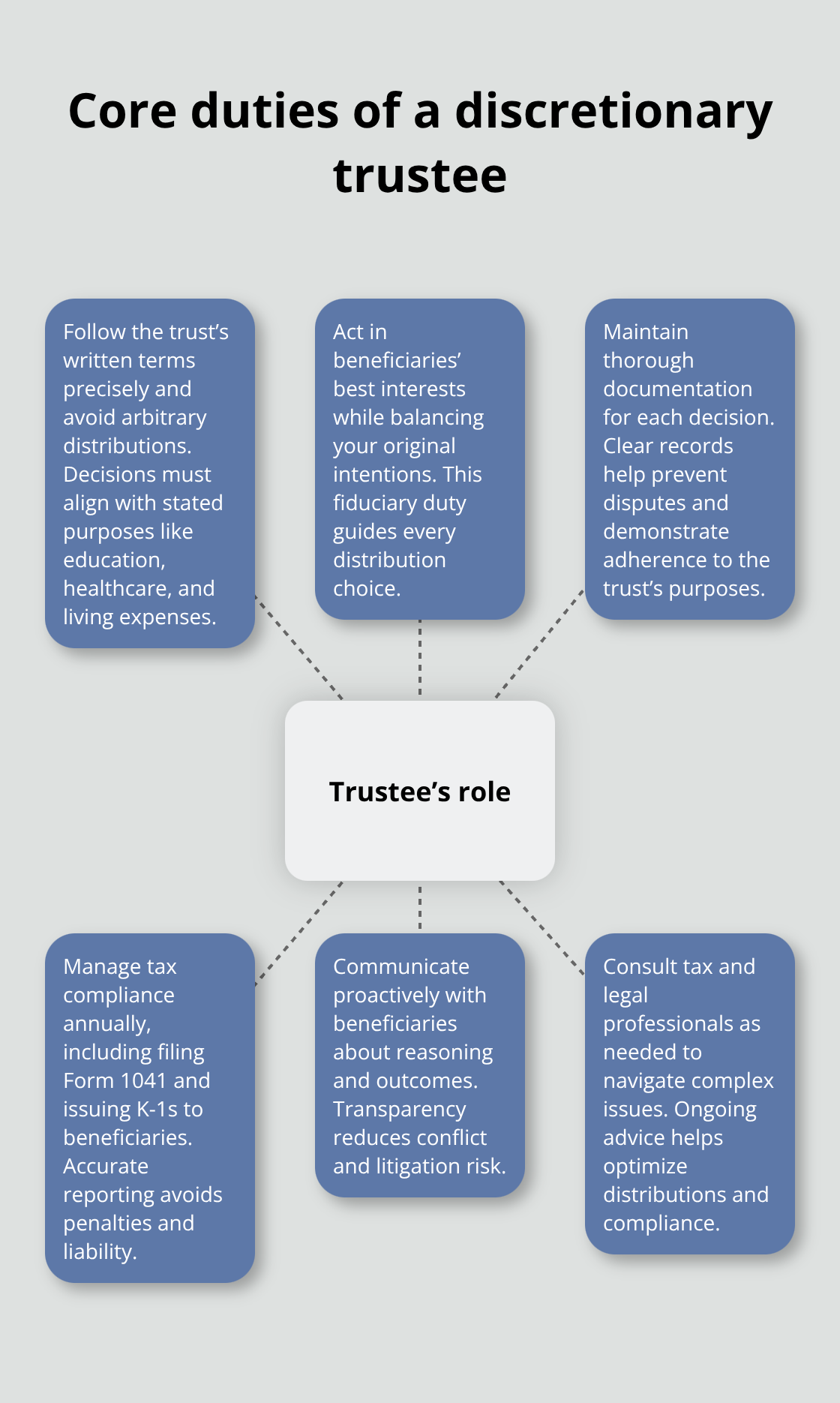

A discretionary trust places assets under a trustee’s control, and here’s what makes it fundamentally different from other structures: the beneficiaries have no automatic right to receive anything. The trustee decides when, how much, and whether to distribute funds based on guidelines you set in the trust document. This isn’t theoretical flexibility-it’s practical power. If a beneficiary faces a lawsuit, creditors cannot claim trust assets because the beneficiary technically owns nothing. If a beneficiary struggles with spending, the trustee can fund education or healthcare directly to providers instead of handing over cash. If circumstances change dramatically (job loss, divorce, addiction), the trustee adjusts distributions accordingly rather than remaining locked into a fixed payment schedule.

What Separates Discretionary Trusts from Fixed Alternatives

Fixed trusts spell out exactly who gets what and when, offering certainty but removing adaptability. A life interest trust, for example, guarantees one person receives income for their lifetime, then assets pass to named heirs-no room for adjustment. Discretionary trusts flip this model. The trustee becomes your planning agent, responding to real-world situations rather than rigid timelines. This matters enormously when beneficiaries are minors, have special needs, or lack financial discipline.

The tradeoff is real: you lose absolute control after you sign the trust document, and the trustee’s decisions rest on their judgment of your original intentions.

The Trustee’s Actual Responsibilities in Distribution Decisions

Your trustee must balance two competing demands: following your written guidelines while acting in beneficiaries’ best interests. They cannot distribute arbitrarily. If your trust deed specifies that distributions should cover education, healthcare, and living expenses only, the trustee violates their fiduciary duty if they fund a vacation home purchase. If the trust is irrevocable (which most discretionary trusts are), you cannot modify these instructions later, so precise drafting matters intensely. The trustee also manages tax reporting. Discretionary trust distributions trigger income tax obligations, and the trustee must file Form 1041 with the IRS and provide beneficiaries with K-1 statements that show their share of trust income.

Why Tax Administration Demands Professional Attention

The administrative burden of tax compliance explains why many families choose professional trustees like banks or trust companies rather than relying on family members who lack accounting and legal knowledge. A trustee who mishandles tax obligations exposes the trust to penalties and creates liability for themselves. This complexity makes the next phase of discretionary trust administration-understanding the real advantages these structures provide-essential to your planning decision.

Why Discretionary Trusts Shield Assets and Reduce Taxes

Discretionary trusts deliver three concrete financial advantages that other estate planning structures simply cannot match. First, they create a genuine barrier against creditors. When you place assets inside a discretionary trust, beneficiaries own nothing legally-the trustee controls everything. A creditor pursuing a beneficiary cannot seize trust assets because the beneficiary has no enforceable claim to distributions. This protection extends beyond lawsuits to divorce settlements and bankruptcy proceedings. If a beneficiary faces marital dissolution, their spouse cannot demand half the trust assets because those assets never belonged to the beneficiary in the first place. Research confirms that discretionary trusts offer this level of asset protection by keeping distributions under trustee control rather than automatically vesting in heirs.

How Distribution Discretion Stops Creditors Cold

The mechanics work because discretionary trusts contain spendthrift provisions that prevent beneficiaries from assigning or pledging their interest in the trust. A creditor can obtain a judgment against a beneficiary, but they cannot force the trustee to distribute funds. The trustee retains absolute discretion over when and whether distributions occur, which means a creditor has no leverage. This creates a powerful planning tool for beneficiaries in high-risk professions-physicians facing malpractice exposure, business owners vulnerable to commercial litigation, or professionals in contentious fields benefit enormously from this structure. The trustee can simply refuse distributions if a creditor judgment exists, effectively making the trust assets unreachable.

Tax Efficiency Through Strategic Distribution Timing

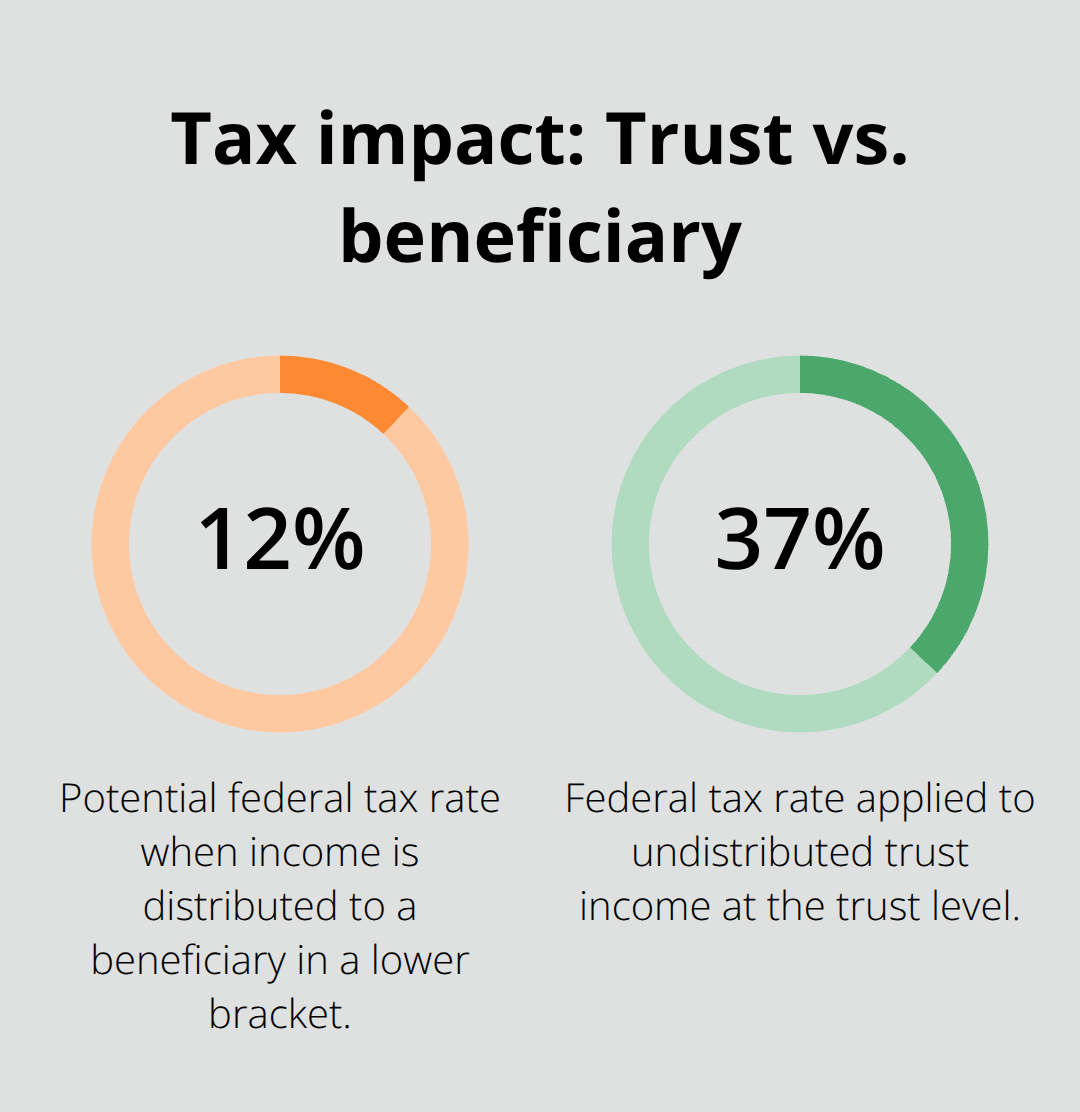

Discretionary trusts allow you to split income among multiple beneficiaries, potentially reducing overall tax burden significantly. When trust income flows to beneficiaries in lower tax brackets rather than concentrating in the trust itself, the combined tax liability decreases. A beneficiary earning minimal income may pay 12% federal tax on trust distributions, while the trust entity itself would pay 37% on the same income. Over multiple years, this differential compounds substantially. Additionally, if a trust holds appreciated assets for more than one year, distributions may qualify for capital gains treatment with preferential tax rates rather than ordinary income rates.

You can also structure distributions to avoid triggering higher Medicare premiums or means-tested benefit thresholds for beneficiaries receiving government assistance-a critical consideration for families managing special needs or elderly relatives on fixed income programs.

Timing Distributions to Match Real-World Needs

The flexibility to adjust distributions based on actual circumstances separates discretionary trusts from rigid alternatives. A beneficiary facing unemployment receives support without waiting for a predetermined distribution date. A beneficiary with medical emergencies receives funding immediately rather than months later. A beneficiary who demonstrates financial responsibility can receive larger distributions while a struggling beneficiary receives only essential payments. This responsiveness prevents the harm caused by fixed trusts, where a beneficiary receives money on schedule regardless of whether they need it or can handle it responsibly. The trustee acts as your planning agent across decades, adapting to job changes, family circumstances, health crises, and shifting financial needs that no one could predict when the trust was created. These advantages explain why discretionary trusts appeal to families with complex situations, but they also introduce administrative challenges that require careful attention and professional guidance.

The Real Obstacles in Running a Discretionary Trust

Discretionary trusts sound ideal until you actually administer one. The flexibility that makes them powerful creates friction with beneficiaries who expect distributions on their timeline, not the trustee’s judgment. A beneficiary who receives nothing while watching another beneficiary fund education expenses feels resentment, even when the trust document explicitly grants the trustee discretion. These disputes arise frequently because beneficiaries confuse discretion with unfairness.

Managing Beneficiary Expectations and Conflict

A trustee who distributes funds to one beneficiary for a down payment on a home but refuses another beneficiary’s request for the same purpose triggers conflict, regardless of legitimate differences in financial readiness or need. The trustee must document every decision carefully, explaining how each distribution aligns with the trust’s stated purposes. Without this paper trail, beneficiaries challenge decisions and sometimes pursue litigation against the trustee.

Professional trustees like banks handle this by maintaining detailed records and communicating reasoning to beneficiaries proactively, which costs money but prevents costly disputes. Family members serving as trustees often lack this discipline, leading to hurt feelings that escalate into formal legal challenges. The IRS Form 1041 reporting requirement compounds beneficiary tension because it reveals income distributions to the trust and allocations to beneficiaries, making every financial decision visible and potentially subject to question. Many family conflicts stem simply from poor communication about why certain beneficiaries received distributions while others did not.

Tax Obligations That Catch Trustees Off Guard

Tax obligations in discretionary trust administration demand precision that catches many trustees off guard. The trustee must file Form 1041 with the IRS annually if the trust generates income exceeding $600, and the trust itself pays income tax at the highest federal rate of 37% on undistributed income. This creates a powerful incentive to distribute income to beneficiaries, who typically face lower tax brackets. However, distributing to beneficiaries triggers K-1 statements showing each beneficiary’s share of trust income, which can disrupt means-tested benefits for elderly or disabled beneficiaries receiving Supplemental Security Income or Medicaid.

A single distribution can disqualify a beneficiary from government assistance for months, creating a crisis the trustee never anticipated. State tax obligations add another layer. Some states impose income tax on trusts, and beneficiaries receiving distributions may owe state taxes in multiple states depending on where they reside and where the trust is administered. A trustee who fails to withhold adequate taxes from distributions leaves beneficiaries with unexpected tax bills.

The fiduciary duty to manage these obligations responsibly means trustees cannot simply ignore tax planning. The trustee must balance distributing enough income to avoid the trust’s 37% tax rate while not disrupting beneficiary benefits or creating surprise tax liabilities. This requires ongoing consultation with tax professionals, which adds significant annual costs. Many trustees discover too late that they needed a CPA or tax attorney involved from the beginning, not after mistakes accumulate.

Trustee Judgment and the Limits of Your Control

The tension between trustee discretion and your original intentions creates a fundamental problem with discretionary trusts. Once you sign the trust document and it becomes irrevocable, you lose the ability to correct a trustee who interprets your wishes differently than you intended. If your trustee makes distributions you would never have approved, you cannot change the trust to prevent future similar decisions.

A trustee who favors one beneficiary over another, or who interprets education expenses to include an expensive private university when you meant public school, operates within their legal authority even if they violate your spirit. The written trust document controls everything. Vague language like “distribute for the beneficiary’s health, education, maintenance, and support” gives trustees enormous discretion to rationalize almost any distribution. The trustee’s fiduciary duty requires them to act in good faith and follow the trust’s terms, but disputes over what those terms actually mean generate litigation that drains the trust.

Beneficiaries who disagree with distributions can sue the trustee, forcing the trustee to defend decisions in court at trust expense. Even when the trustee wins, legal fees deplete assets that should have gone to beneficiaries. This risk explains why professional trustee selection matters intensely. A trustee with a financial incentive to distribute aggressively, or one with poor judgment, creates ongoing problems. Families considering discretionary trusts should invest heavily in trustee selection and crystal-clear trust language that minimizes interpretation disputes before the trust takes effect.

Final Thoughts

Discretionary trusts solve real problems that fixed trusts cannot address. They protect assets from creditors, adapt to changing circumstances, and reduce taxes through strategic income distribution. The flexibility to respond to unemployment, medical emergencies, or shifting family dynamics gives you control that extends decades into the future, long after you’re gone.

Discretionary trust administration works best when you have beneficiaries who need protection from poor financial decisions, face creditor exposure, or have special needs requiring ongoing support. These trusts fail when you need absolute certainty about who receives what, or when you want to maintain tight control over distribution decisions after creation. Consider this structure if you’re concerned about a beneficiary’s ability to manage inheritance responsibly, if you have beneficiaries in high-risk professions vulnerable to lawsuits, or if you want to shield assets from divorce settlements.

The next step involves consulting with an attorney who understands both the legal mechanics and practical realities of discretionary trust administration. We at Law Offices of Roshni T. Desai help families across Southern California determine whether discretionary trusts fit their specific circumstances, and we handle the detailed drafting that prevents disputes and tax problems down the road. Contact us for a free consultation to explore whether a discretionary trust belongs in your estate plan.