Family Trust Administration Planning: Securing Your Heirs’ Future

A family trust can protect your heirs, but only if it’s managed correctly. Many families overlook critical details during trust administration, leading to unnecessary taxes, delays, and conflict among beneficiaries.

We at Law Offices of Roshni T. Desai help families navigate family trust administration planning with clarity and confidence. This guide walks you through what actually happens during trust administration and how to avoid the mistakes that cost families thousands of dollars.

What Happens During Trust Administration

Trust administration starts the moment the settlor dies. The trustee obtains the death certificate and immediately notifies beneficiaries and financial institutions of the change in control. This notification step matters because it establishes the trustee’s legal authority to act on behalf of the trust. Next, the trustee locates and reviews the trust document to understand distribution terms, trustee duties, and any conditions that apply. Many trustees skip this review and later discover they’ve made distributions that violate the settlor’s actual wishes, creating unnecessary conflict. The trustee files any required affidavits verifying the grantor’s death and the trustee’s authority, then opens a dedicated trust bank account to keep trust assets separate from personal funds.

This separation prevents commingling and simplifies record-keeping when the time comes to account for every dollar spent.

Inventorying and Valuing Assets

The trustee compiles a comprehensive inventory of all assets, including real estate, bank accounts, investments, and valuable personal property. This step takes time and precision. The trustee then determines fair market values for all assets and hires professional appraisers where necessary (particularly for real estate or high-value items). Skipping professional appraisals is a false economy that often costs families thousands in missed tax deductions or inflated estate tax liability. The trustee manages trust assets responsibly by maintaining real estate, monitoring investments, and paying valid debts before distributions. These ongoing management duties continue throughout the administration period, which can last anywhere from months to years depending on the complexity of the estate.

Tax Compliance and Strategic Distribution

Tax obligations represent the largest financial exposure during trust administration. The trustee prepares and files the decedent’s final income tax return and coordinates with tax professionals on any tax liabilities. If the estate exceeds the Massachusetts exemption threshold of $2 million, the trustee must file a Massachusetts estate tax return and set aside funds for any estate tax obligations. Retirement accounts like IRAs and 401(k)s demand special attention because distributions must follow specific rules to avoid penalties. The trustee applies distributions in a tax-efficient manner, often consulting with a CPA to minimize the tax burden on beneficiaries. The trustee distributes assets according to the trust terms, confirming that conditions such as age milestones or other requirements are met before releasing funds. Clear communication with beneficiaries throughout this process prevents disputes and keeps everyone informed about timing and amounts-setting the stage for the next critical phase of trust administration.

Common Mistakes Families Make During Trust Administration

Trustees commonly misread or completely ignore the language inside trust documents, leading to distributions that contradict what the settlor actually wanted. A trustee might assume a beneficiary should receive funds immediately upon the settlor’s death, only to discover the document specifies distributions at age 30 or upon completion of college. This mistake costs time and creates resentment among beneficiaries who feel cheated or confused about the timeline. The trustee’s obligation is to follow the document precisely, not to interpret it based on what feels fair or generous.

Failing to Maintain Records and Obtain Appraisals

Many trustees fail to maintain organized records during administration, which later creates tax compliance problems. The IRS requires trustees to document every transaction, asset valuation, and distribution, and missing records can trigger audits that delay final settlement by months. One critical step trustees overlook is obtaining professional appraisals for high-value assets. A real estate property worth $500,000 might be undervalued by 20 percent without a professional appraisal, costing the estate unnecessary capital gains tax exposure for heirs.

Massachusetts law requires trustees to act impartially and prioritize beneficiaries’ interests above all else, yet many family trustees let personal preferences influence distribution decisions, creating grounds for legal contests.

The Cost of Delayed Distributions

Trustees often delay distributions to beneficiaries without clear justification, sometimes for months or years. This delay generates frustration and suspicion among heirs, who naturally wonder whether the trustee is mismanaging assets or simply procrastinating. State law typically requires trustees to distribute assets within a reasonable timeframe once conditions are met, and prolonged delays can expose trustees to liability claims. Tax inefficiency represents another hidden cost during delayed administration. If a trust holds appreciated assets that should have been distributed earlier, the beneficiary misses the step-up in basis that occurs at the settlor’s death, meaning higher capital gains taxes when the asset is eventually sold. A portfolio of stocks worth $100,000 at death but $150,000 two years later could have saved the beneficiary thousands in taxes if distributed promptly after valuation.

Tax Mistakes That Cost Thousands

Trustees frequently fail to coordinate with a CPA or tax professional before making large distributions, resulting in unexpected tax bills for beneficiaries. A beneficiary receiving a $200,000 distribution might face a surprise tax liability if the trustee didn’t plan the timing or structure the distribution tax-efficiently. Retirement account distributions demand specialized knowledge because the rules differ significantly from other assets. An IRA inherited by a non-spouse beneficiary must be distributed within ten years under current federal law, yet many trustees miss this deadline entirely, triggering penalties and unnecessary taxation. Ignoring state estate taxes also creates problems in Massachusetts, where estates exceeding $2 million face state-level taxation. A trustee who fails to file the required Massachusetts estate tax return on time may face penalties and interest charges that reduce the amount available for beneficiaries.

Getting Professional Help Before Distributions

The trustee should consult a tax professional immediately after the settlor’s death to map out a distribution strategy that minimizes taxes across all beneficiaries and asset types. Engaging a CPA with trust administration experience before making any major distributions typically saves families thousands in unnecessary taxes and prevents costly errors that cannot be reversed once distributions occur. These mistakes compound when trustees act alone, which is why the next section examines how to select a trustee who possesses both the judgment and the support network to avoid these pitfalls entirely.

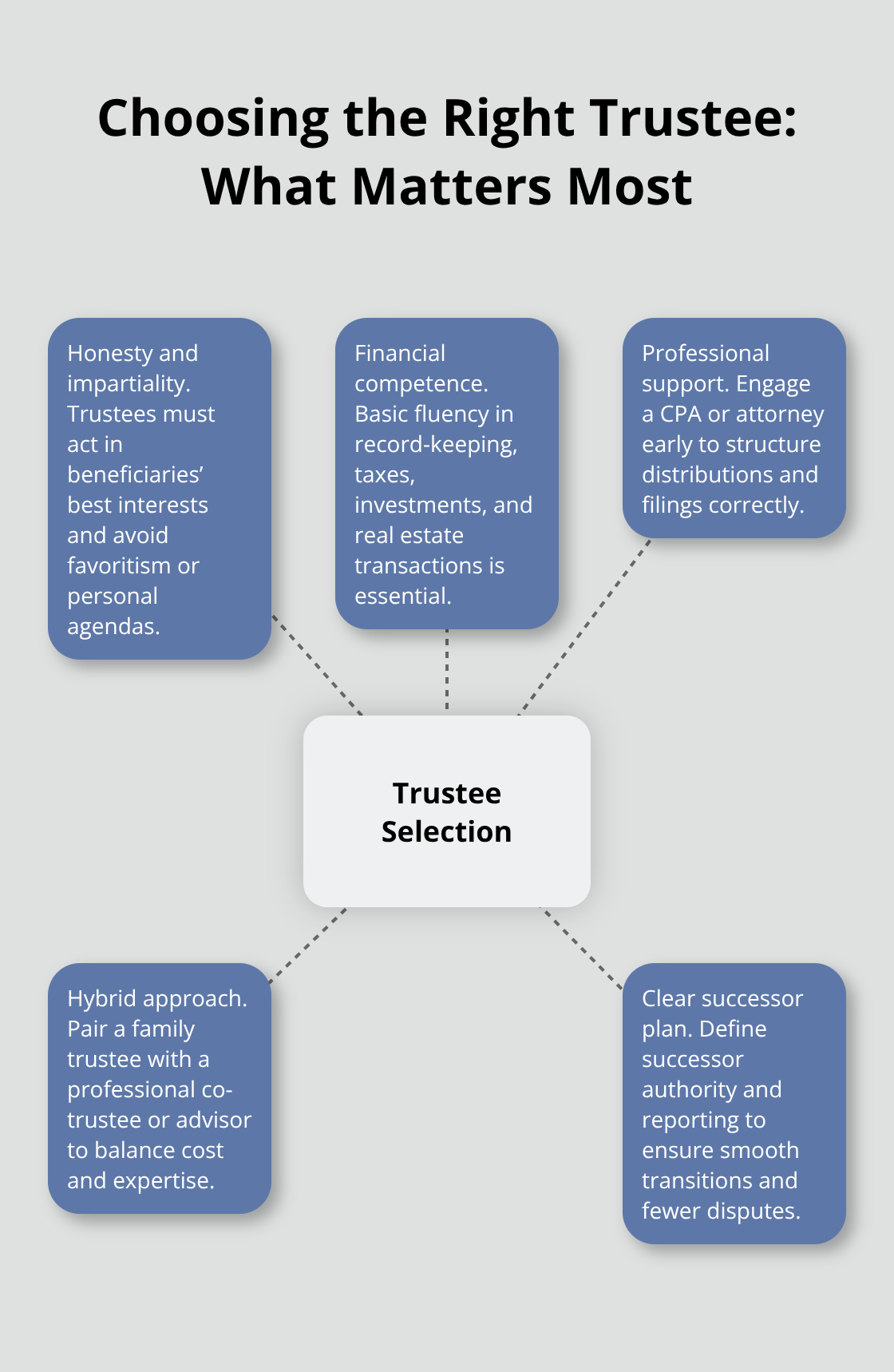

Who Should Manage Your Family Trust

The trustee you select determines whether your family trust functions smoothly or becomes a source of conflict and financial loss. A trustee needs three things: unwavering honesty, basic financial competence, and the willingness to seek professional help when needed. Most families struggle with this decision because they assume a close relative automatically makes the best trustee. That assumption is wrong. A trustworthy family member who lacks financial knowledge will make costly mistakes during administration, just as a financially savvy person with questionable judgment will misuse their authority. Your trustee will control hundreds of thousands or millions of dollars, make binding legal decisions, file tax returns, and communicate directly with beneficiaries during a sensitive time. The wrong choice creates years of friction and expense.

Family Members Rarely Have the Right Combination of Skills

Selecting a family member as trustee feels natural because they understand your values and family dynamics. In practice, family trustees frequently misunderstand the legal requirements of their role and confuse trustee duties with personal preferences. A parent might favor one child and unconsciously delay distributions to another, or a sibling might postpone asset sales because they feel emotionally attached to property. Massachusetts law requires trustees to act impartially and prioritize beneficiaries’ interests above personal relationships, yet family members often struggle with this obligation. The emotional weight of the role also creates stress that strains family relationships. A family trustee managing a $500,000 trust faces years of record-keeping, tax compliance, investment decisions, and communication with beneficiaries, all while managing their own life. Many family trustees report feeling overwhelmed by the responsibility and worried they might make costly errors.

Professional trustees handle hundreds of trusts annually and understand the technical requirements that family members overlook. A professional trustee knows exactly how to structure distributions to minimize taxes, when to obtain appraisals, how to file required returns, and what records to maintain. They make decisions based on legal requirements rather than family politics. The trade-off is cost: a corporate trustee typically charges between 0.5 and 1.5 percent of assets under management annually, which means a $500,000 trust costs $2,500 to $7,500 per year. For smaller trusts under $200,000, this fee structure becomes prohibitively expensive relative to the assets involved.

A Hybrid Approach Often Works Best

The most practical solution for many families combines a trusted family member with a professional co-trustee or professional advisor. One family member serves as the primary trustee, handling day-to-day decisions and maintaining family relationships, while a corporate trustee or attorney provides oversight and technical guidance. This structure reduces costs compared to a full corporate trustee while ensuring professional standards are met. The family trustee benefits from institutional support and can delegate complex decisions to someone with proper training.

Another option involves naming a family member as trustee but requiring them to work with an attorney or CPA for major decisions like tax planning or asset sales. The upfront cost of hiring professional guidance typically saves families far more in prevented mistakes. A trustee who consults a CPA before distributing $200,000 to a beneficiary might save $15,000 to $30,000 in unnecessary taxes through strategic timing or structure.

A trustee who hires a real estate professional before selling trust property avoids the common mistake of underpricing assets or missing tax deductions. These professional relationships cost $2,000 to $5,000 upfront but generate savings that dwarf the expense.

Evaluate Your Trustee’s Financial Background Honestly

Consider your trustee’s financial background honestly when making this decision. If your chosen trustee has never managed significant investments, has limited tax knowledge, or lacks experience with real estate transactions, they need professional support. A trustee’s willingness to admit knowledge gaps and seek help matters more than their raw financial knowledge. An honest trustee who recognizes they need guidance will make better decisions than an overconfident trustee who attempts complex tasks without proper training.

Successor Trustees Require Clear Instructions

Many families name a primary trustee but fail to clearly define the successor trustee’s role and authority. The successor trustee steps in when the primary trustee dies, becomes incapacitated, or resigns, so their responsibilities must be explicitly documented in the trust. A vague successor trustee clause creates confusion and potential conflict when the transition occurs. Your trust document should specify whether the successor trustee has the same authority as the original trustee or whether their powers are limited. Some families restrict successor trustees to distribution decisions only, requiring them to hire a professional manager for investments and property. Others grant full authority but require the successor to report annually to beneficiaries. The clearer your instructions, the fewer disputes arise.

Successor trustees also need practical support. If your primary trustee is a family member with limited financial experience, try naming a professional trustee as successor rather than another family member. This ensures that if the primary trustee becomes unable to serve, professional management automatically takes over without requiring beneficiaries to petition the court for a trustee change. The successor trustee should also be someone significantly younger than the primary trustee, ensuring they can serve for the full duration of trust administration. Naming a trustee who is already in their 80s as a successor creates the same problem you were trying to solve by naming them as backup.

Final Thoughts

Family trust administration planning protects your heirs only when you make informed decisions today. The three most important takeaways are straightforward: choose a trustee with both honesty and financial competence, ensure your trust document is crystal clear about distributions and conditions, and plan for professional support before administration starts. A trustee who understands their legal obligations, maintains organized records, and consults with tax professionals will save your family thousands in unnecessary taxes and legal disputes.

Tax compliance, asset valuation, retirement account distributions, and state-level estate taxes demand specialized knowledge that most families lack. A CPA or attorney who reviews your trust before administration starts can identify potential problems and create a distribution strategy that minimizes taxes across all beneficiaries (this guidance typically costs $2,000 to $5,000 but generates savings that far exceed the investment). Without professional input, trustees commonly make errors that cannot be reversed once distributions occur, leaving beneficiaries with unexpected tax bills or delayed access to their inheritance.

Review your current trust document and honestly assess whether your named trustee has the financial knowledge and time to manage administration properly. If gaps exist, consider naming a co-trustee or establishing a relationship with a professional advisor now rather than scrambling to find help after the settlor’s death. We at Law Offices of Roshni T. Desai help families create clear, legally sound trusts and guide trustees through administration with confidence-contact us for a free consultation to discuss your family trust administration planning and protect your heirs’ financial future.