Living Trust Tax Planning: Minimizing Taxes While Protecting Heirs

A living trust can save your heirs thousands in taxes, but only if it’s structured correctly. Many families miss critical opportunities because they don’t understand how to position assets within their trust.

We at Law Offices of Roshni T. Desai help clients use living trust tax planning to reduce what the government takes and increase what your family keeps. This guide shows you exactly how.

How Living Trusts Cut Your Estate Tax Bill

Understanding the Federal and State Tax Landscape

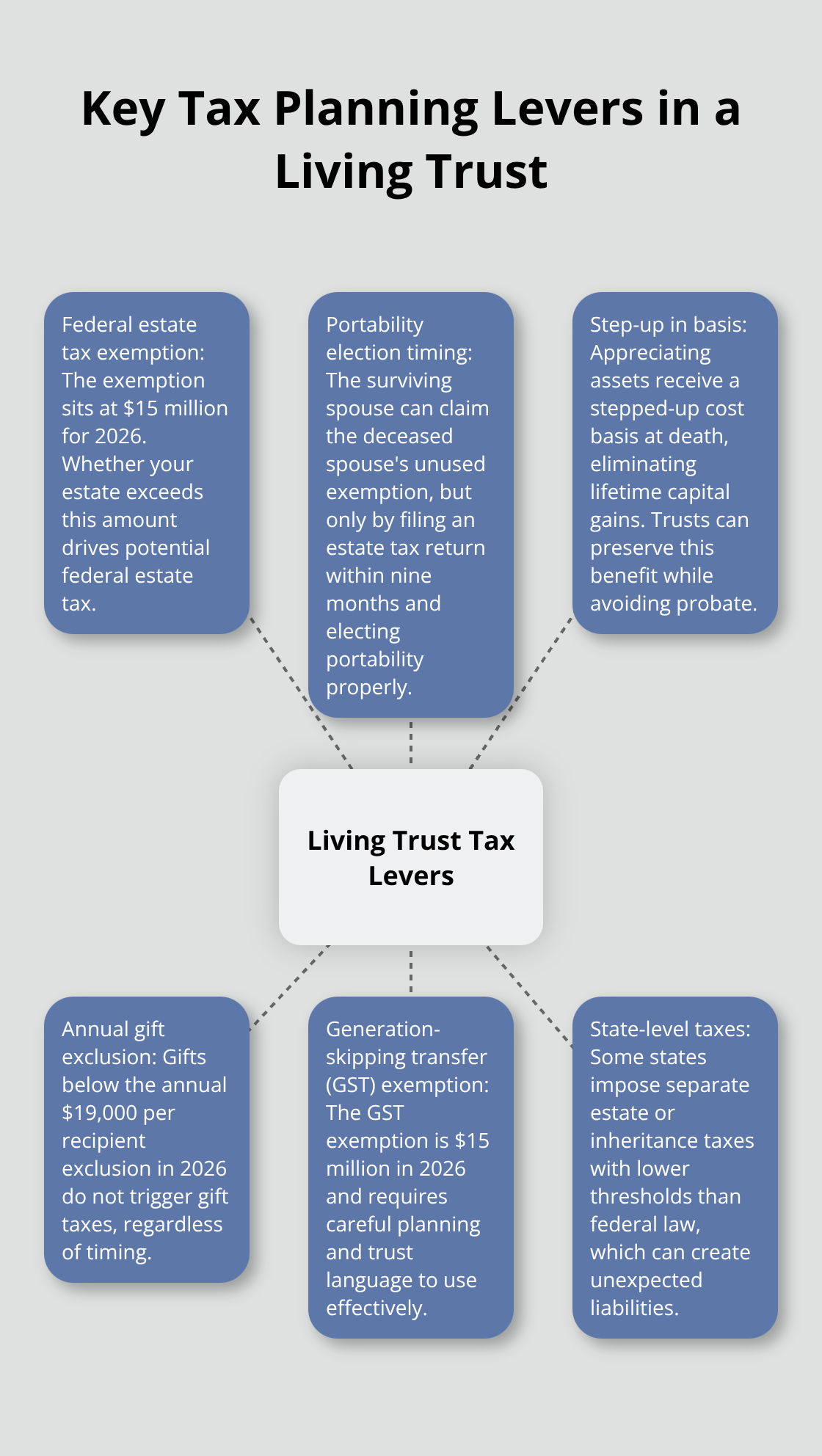

The federal estate tax exemption sits at $15 million for 2026, but this number drops significantly in states with their own estate taxes. The gap between what you can pass tax-free and what your estate actually contains determines whether your heirs face a substantial tax bill. A living trust alone doesn’t reduce estate taxes, but the right trust structure combined with strategic asset placement transforms your tax outcome. Married couples have double the exemption room if they coordinate their trusts correctly-both spouses can shelter $30 million from federal estate tax in 2026, but only if their trusts are set up to use each spouse’s exemption separately.

Maximizing Your Spouse’s Exemption Through Proper Planning

Many families waste one spouse’s exemption entirely by titling everything jointly or leaving everything to the surviving spouse outright. The surviving spouse can use portability to claim the deceased spouse’s unused exemption, but this requires filing an estate tax return within nine months of death, and it only works if you elect it properly. Without the right trust structure, you lose this opportunity permanently.

Positioning Appreciating Assets for Tax Efficiency

Appreciating assets belong inside your trust for a fundamental reason: the step-up in basis rule. When someone inherits property outside a trust, the cost basis resets to the fair market value on the death date, eliminating capital gains taxes on appreciation that happened during your lifetime. If you place those same appreciating assets in a revocable living trust, your heirs still get the step-up, but they avoid probate and keep the transaction private. Real estate held in your personal name creates probate delays and public record exposure that a trust eliminates.

Timing Asset Transfers and Generation-Skipping Strategies

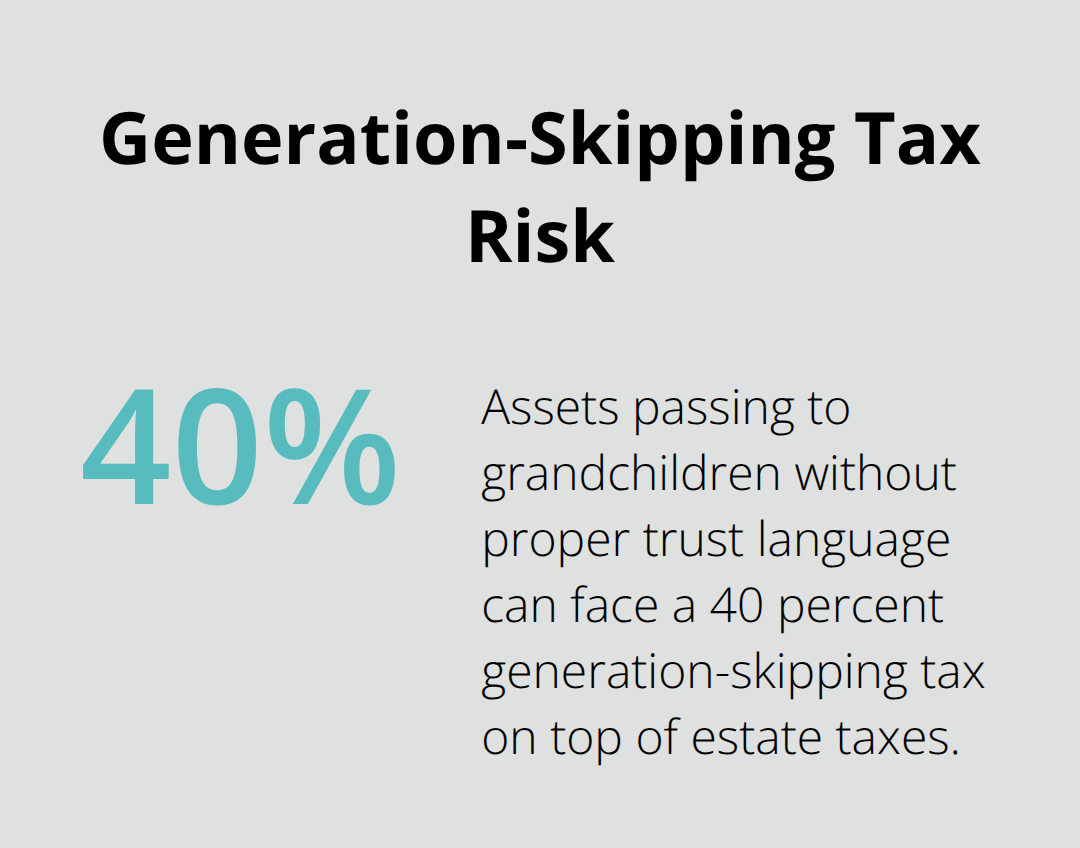

Timing matters when you transfer assets into the trust. Assets transferred more than three years before death avoid certain gift tax complications, though gifts below the annual $19,000 per recipient exclusion don’t trigger gift taxes anyway. For high-net-worth families, generation-skipping transfer tax strategies become necessary when assets pass to grandchildren or skip generations. The generation-skipping exemption is $15 million in 2026, but it requires careful planning to use it effectively. Without proper trust language, assets passing to grandchildren face a 40 percent tax on top of estate taxes, making this one of the costliest oversights families make.

Protecting Wealth Across Multiple Generations

The structure of your trust determines whether your wealth reaches future generations intact or diminished by unnecessary taxes. Automatic allocation of generation-skipping exemptions within your trust protects assets across multiple generations without constant monitoring or amendments. Charitable trusts offer another layer of tax efficiency for families committed to philanthropic goals while reducing estate taxes. This foundational work sets the stage for understanding where your specific assets should sit within your trust structure-a decision that separates tax-efficient plans from those that leave money on the table.

What Assets Should Go Into Your Living Trust

Appreciating Assets and the Step-Up in Basis Rule

Placing the right assets into your living trust makes the difference between a tax-efficient plan and one that leaves thousands on the table. Appreciating assets like stocks, rental properties, and investment real estate belong inside your trust because your heirs receive a stepped-up cost basis when they inherit them, eliminating capital gains taxes on appreciation that occurred during your lifetime. The step-up in basis rule applies whether assets sit in a revocable living trust or remain in your personal name, but only the trust structure eliminates probate and keeps details out of public records.

Real Property and Probate Avoidance

Real property held in your personal name creates probate delays, public record exposure, and unnecessary friction during transfer. When you retitle real estate into your trust, your heirs avoid probate entirely and keep the transaction private, which matters especially for high-value properties in California where probate costs can reach 3 to 7 percent of the estate’s value. Move appreciating assets into the trust now, not later, because timing affects which tax rules apply to your transfer.

Timing Transfers to Prevent Tax Complications

Timing your asset transfers correctly prevents unnecessary gift tax complications and positions your heirs for maximum tax efficiency. Assets transferred more than three years before death avoid certain gift tax issues entirely, though gifts below the annual $19,000 per recipient exclusion in 2026 never trigger gift taxes regardless of timing. We at Law Offices of Roshni T. Desai recommend transferring appreciating assets into your trust within the next 12 months rather than waiting, because market fluctuations and life changes create unnecessary delays and complexity.

Generation-Skipping Strategies for Multi-Generational Wealth

High-net-worth families must coordinate asset placement with generation-skipping transfer tax strategies when wealth passes to grandchildren, since the 40 percent generation-skipping tax compounds on top of regular estate taxes and represents one of the costliest oversights families make. The trust document should include automatic allocation language for generation-skipping exemptions, which protects assets across multiple generations without constant amendments or monitoring. Your real estate holdings deserve special attention because retitling property into the trust takes weeks, not months, yet families routinely delay this step until it’s too late to implement other tax strategies.

The specific assets you hold and their current tax basis determine which trust structures work best for your situation-a decision that requires understanding how different asset types interact with estate and generation-skipping tax rules.

Common Mistakes in Living Trust Tax Planning

The Empty Trust Problem

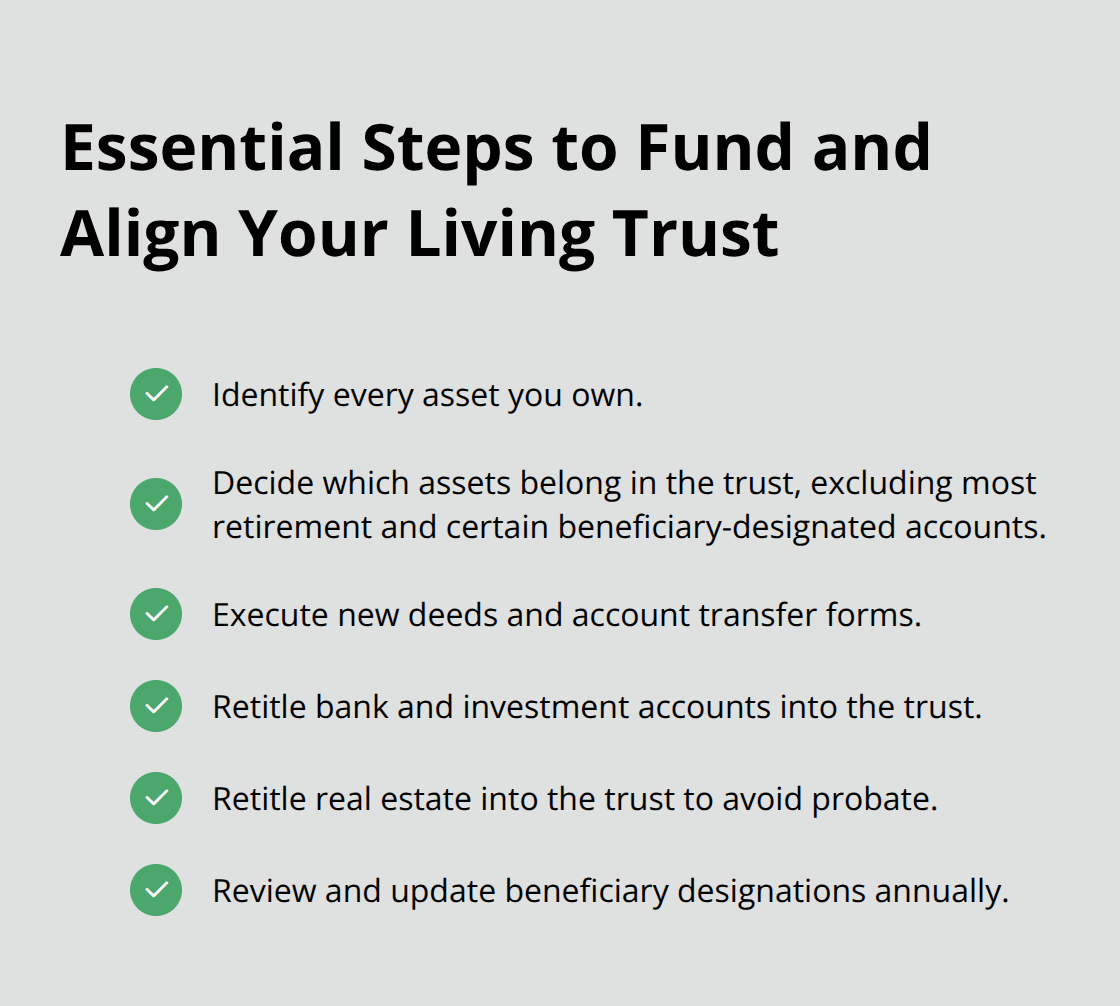

Most families don’t fail because they lack a living trust-they fail because the trust sits empty. A living trust that contains no assets provides zero protection and zero tax benefits, yet this happens constantly. Families spend money drafting the document, then never transfer property into it, leaving everything in their personal name where it faces probate, public exposure, and full estate taxation.

The mechanics of funding are straightforward: you retitle bank accounts, investment accounts, and real estate into the trust’s name. This takes weeks, not months, and costs nothing beyond the time investment. Clients often create a trust five or ten years ago but never complete the funding process. When death occurs, their heirs inherit an empty trust and a full probate case.

The fix requires identifying every asset you own, determining which ones belong in the trust (nearly everything except retirement accounts and certain beneficiary-designated assets), and executing new deeds and account transfer forms. Start this process immediately rather than assuming you’ll handle it later, because market swings, life changes, and unexpected health events make delays costly and complicated.

State-Level Tax Blind Spots

State-level estate and inheritance taxes create a second major blind spot that federal planning alone cannot address. Six states impose inheritance taxes on beneficiaries: Iowa, Kentucky, Maryland, Nebraska, New Jersey, and Pennsylvania. Two additional states impose state estate taxes on the deceased’s estate itself, with different exemption thresholds than federal law provides.

A client with a $12 million estate may fall below the federal $15 million exemption for 2026 but exceed New Jersey’s $6.94 million state exemption, triggering state estate taxes despite no federal liability. Your living trust structure must account for these state rules, yet many plans drafted years ago ignore them entirely. The gap between state and federal exemptions creates unexpected tax bills that proper planning prevents.

Outdated Beneficiary Designations

Beneficiary designations create the third critical failure point because they operate outside your trust and override what your will or trust document specifies. A retirement account, life insurance policy, or transfer-on-death account with outdated beneficiary designations bypasses your entire trust plan.

If you named your ex-spouse as beneficiary on a $500,000 life insurance policy and forgot to update it after divorce, that policy passes to your ex regardless of what your trust says. Review every beneficiary designation annually and cross-reference them against your current trust structure, because misalignment defeats tax planning and creates family conflict. Coordinate your trust with your beneficiary designations so assets flow through the intended structure rather than around it entirely.

Final Thoughts

Living trust tax planning works only when you implement it completely. The federal exemption of $15 million in 2026 means nothing if your trust remains empty, and state-level taxes blindside families who ignore rules in their own jurisdiction. Outdated beneficiary designations defeat your entire strategy by routing assets around your trust structure, costing families tens of thousands in unnecessary taxes and probate delays.

Your situation is unique because your assets, family structure, and state of residence create different tax exposures than your neighbor’s situation. A $12 million estate triggers no federal tax in 2026 but may face state liability depending on where you live, and married couples can shelter $30 million from federal estate tax only if both spouses’ exemptions are used separately through proper trust coordination. Life insurance proceeds, retirement accounts, and transfer-on-death designations require separate attention because they operate outside your trust document.

We at Law Offices of Roshni T. Desai help clients implement living trust tax planning that protects their heirs and keeps more wealth in your family. Contact us today to review your current trust structure, identify which assets need retitling, and determine whether state-level taxes affect your plan.