Planning a Smooth Trust Administration Timeline for Orange County, California Estates

Trust administration in Orange County involves strict deadlines and procedural requirements that can feel overwhelming. At Law Offices of Roshni T. Desai, we’ve guided countless families through this process and know exactly where delays happen.

This guide breaks down the trust administration timeline step-by-step, showing you what to expect and how to avoid common pitfalls that extend the process unnecessarily.

What Deadlines Actually Matter in Orange County Trust Administration

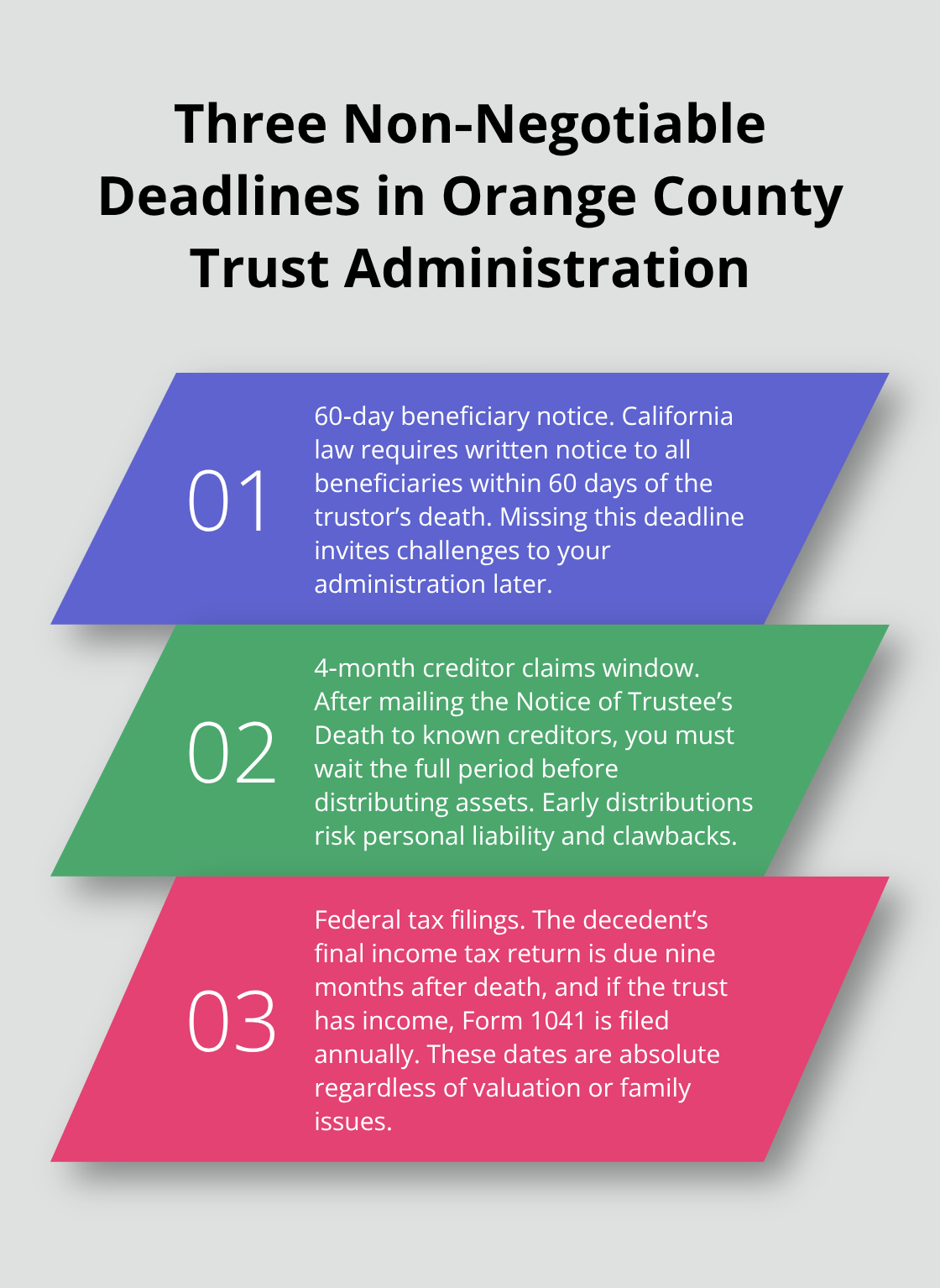

California Probate Code sections 16000 through 16015 establish the legal framework for trust administration, but the real timeline pressure comes from specific, non-negotiable deadlines that most trustees don’t anticipate. The 60-day beneficiary notification requirement under California law is your first critical deadline-you must notify all beneficiaries in writing within 60 days of the trustor’s death. Miss this, and beneficiaries can challenge your administration later, even if you’ve handled everything else correctly. The second major deadline involves the creditor claims period, which typically runs four months from the date you mail the Notice of Trustee’s Death to known creditors. Distributing assets before this window closes exposes you to personal liability if unpaid debts surface afterward. Orange County courts don’t forgive this mistake, and it can force you to claw back distributions from beneficiaries-a situation that destroys family relationships fast.

Federal tax deadlines add another layer: the decedent’s final income tax return is due nine months after death, and if the trust generates income during administration, Form 1041 filings are required annually. The IRS doesn’t care about your family drama or asset valuation delays; these dates are absolute. Property tax reassessment under California Proposition 19 has its own timeline too, and missing the exclusion window means your beneficiaries pay higher property taxes on transferred real estate. Most Orange County trust administrations take 6 to 12 months, but this assumes you move quickly on the front end.

Start Immediately After Death

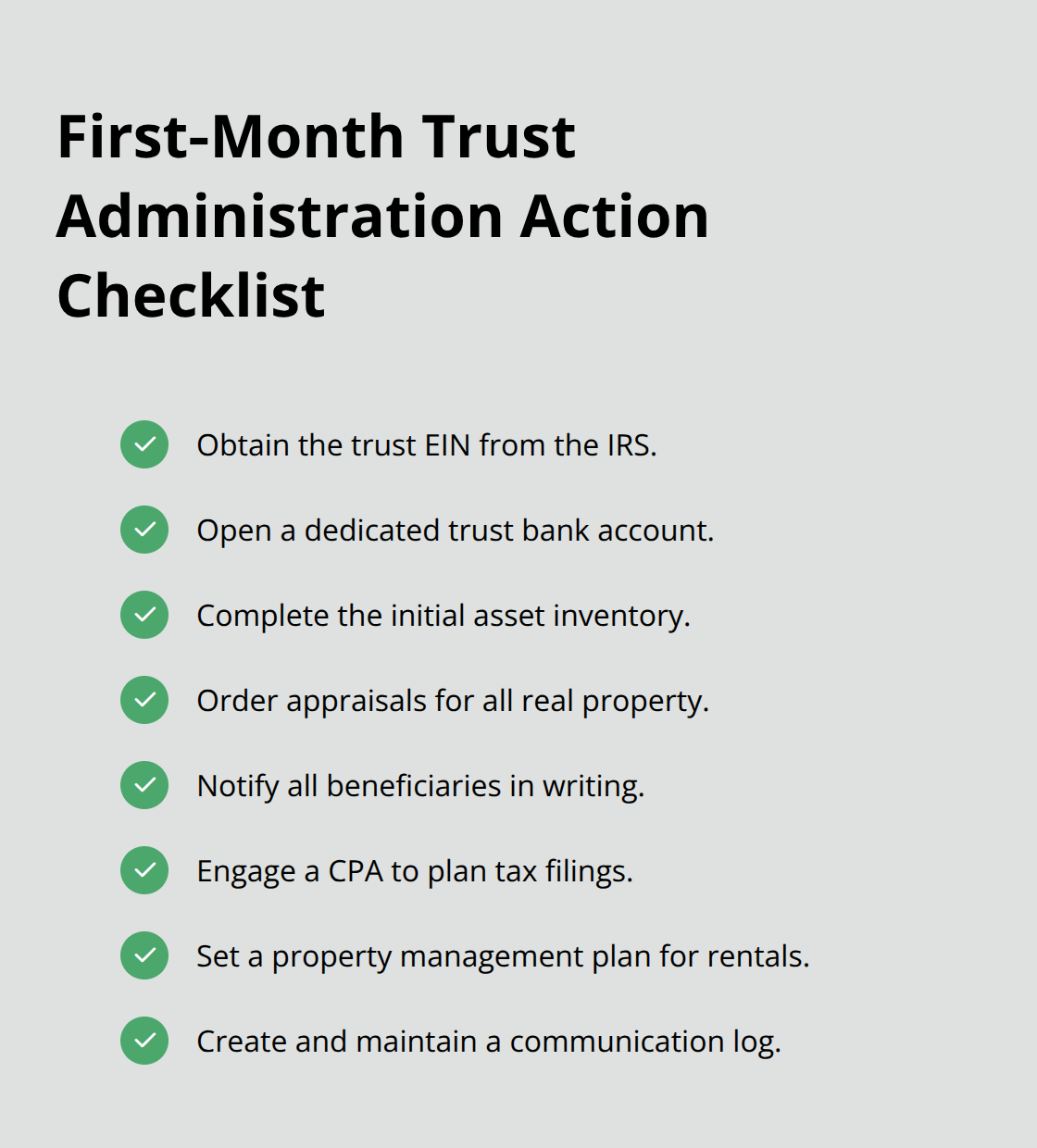

The moment the trustor passes, your clock starts running. Many trustees wait weeks to gather documents, notify beneficiaries, or open a trust bank account, which compresses your timeline dangerously. Open a dedicated trust bank account within the first two weeks and obtain a federal Employer Identification Number immediately-this prevents commingling personal and trust funds and gives you a clear paper trail for the IRS. Identify and value all trust assets in the first month, including real estate, investment accounts, and personal property. For real estate, obtain a professional appraisal right away because property tax reassessment decisions depend on accurate valuations. Orange County property transfers require an Affidavit of Death of Trustee recorded with the county recorder, and delays here can hold up title transfers for months. Notify beneficiaries early and provide a preliminary timeline rather than waiting until you’ve resolved every detail. Beneficiaries who understand what’s coming rarely challenge the process.

Manage Taxes and Debts Before Distributions

This is where most trustees stumble. You cannot legally distribute assets until you address all debts, taxes, and administrative expenses. Coordinate with a CPA immediately to plan for income tax returns, potential estate taxes on larger estates, and property tax filings. If the trust holds rental properties, those generate income that requires tax filings during administration. Hold back enough liquid assets to cover estimated taxes, trustee fees, legal fees, and any outstanding debts. California law allows reasonable trustee compensation, typically around 1 to 2 percent of the trust’s value, but only if you document your time and effort. Many trustees skip this documentation and then cannot justify their fees later. The creditor claims window is your absolute final deadline for distributions-after those four months expire, you can distribute remaining assets, but not before. Orange County courts have seen trustees sued by beneficiaries for early distributions that later got clawed back to pay creditors, and those lawsuits are expensive and public.

Coordinate Professional Help for Complex Assets

Real estate, business interests, and investment portfolios require specialized knowledge that most individual trustees lack. Engage professionals early-a CPA for tax planning, a title company for property transfers, and an attorney for compliance questions-to avoid costly mistakes. These professionals help you meet deadlines without scrambling at the last minute. If you hold rental properties (a common situation in Orange County), property management decisions affect your timeline significantly. You must maintain the properties, communicate with tenants, and ensure they generate income during administration. Failing to manage these assets actively can constitute a fiduciary breach under California law, and beneficiaries can hold you personally liable for losses. The complexity of your trust determines how much professional support you need, but waiting until problems arise costs far more than planning ahead.

Your next steps depend on how organized your records are and whether you’ve already identified all beneficiaries and assets. The foundation you build in these first weeks determines whether your administration stays on track or spirals into delays and family conflict.

Where Trust Administrations Actually Get Stuck

Tax Deadlines Create Cascading Delays

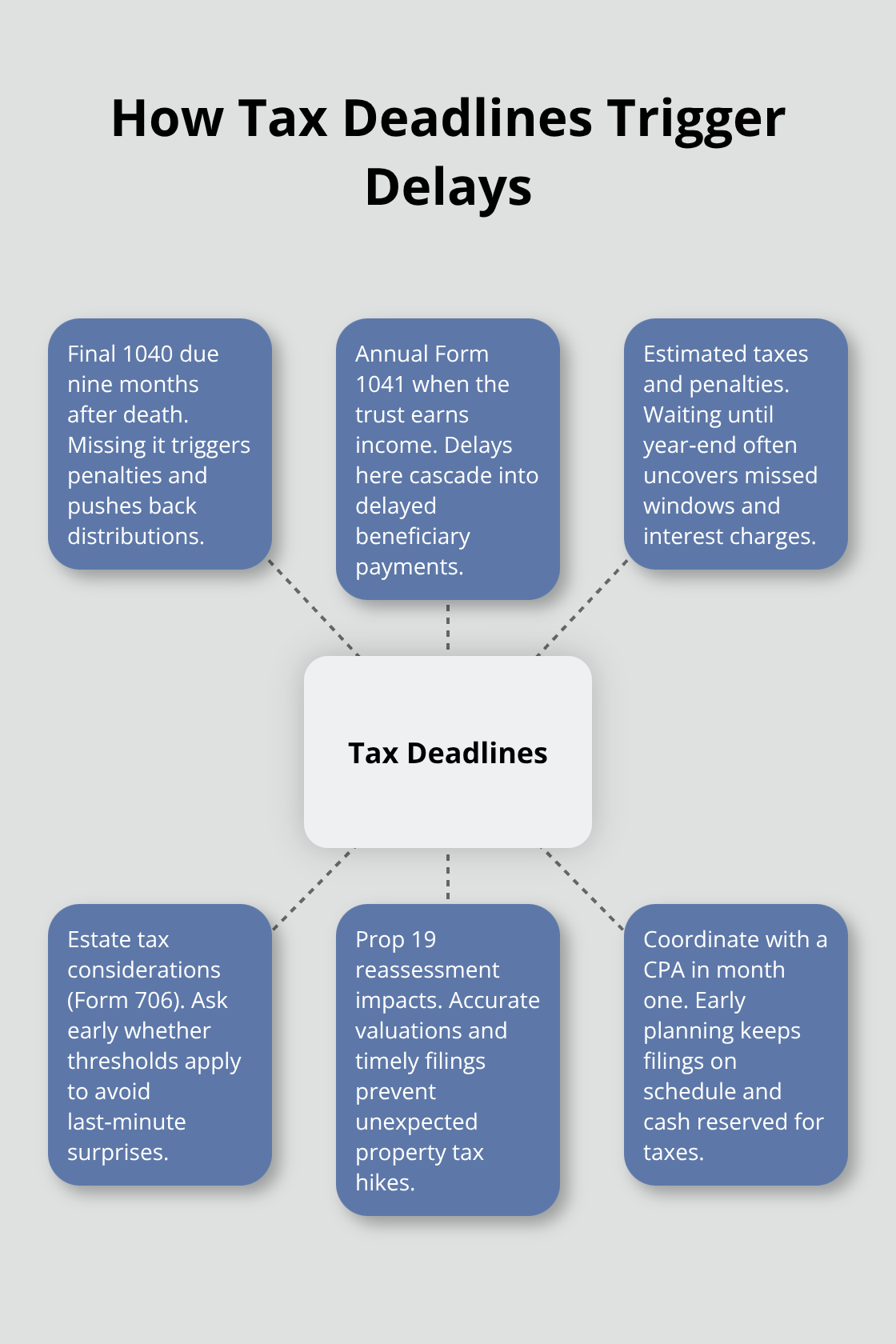

Tax complications emerge faster than most trustees expect, and the IRS does not negotiate timelines based on your circumstances. The decedent’s final income tax return must be filed nine months after death-that’s a hard deadline, not a suggestion. If the trust generates income during administration (which happens with rental properties, investment accounts, or business interests), you file Form 1041 annually, and delays here cascade into beneficiary distribution delays. Many trustees wait until December to address taxes, only to realize they’ve missed critical filing windows that trigger penalties and interest charges.

Orange County trustees administering estates with significant investment portfolios often face surprise income from dividends or capital gains that weren’t anticipated, and failing to set aside funds for these taxes forces you to delay distributions or, worse, claw back assets from beneficiaries. Coordinate with a CPA in month one, not month six. Ask specifically about estimated tax liability, quarterly filing requirements if administration stretches beyond a year, and whether Form 706 (estate tax return) applies to your situation.

Estates exceeding $13.61 million face federal estate tax under current law, and even if you’re below that threshold, California property transfers under Proposition 19 trigger reassessment calculations that require precise valuations. Hold back 15 to 20 percent of liquid assets for tax contingencies to prevent the scramble that destroys timelines.

Communication Gaps Fuel Beneficiary Conflicts

Property disputes and beneficiary conflicts often stem not from actual disagreements about the trust terms but from communication gaps that breed suspicion. A beneficiary who hasn’t heard from you in three months assumes you’re hiding something, even if you’re simply waiting for appraisals or tax documents.

Orange County family dynamics amplify this problem-multiple adult children inheriting real estate together frequently clash over whether to sell or retain the property, and without clear communication about the timeline and decision-making process, these disputes escalate into formal challenges that require court involvement. Document every decision in writing and send it to beneficiaries. If you decide to hold rental property for six months to assess market conditions before selling, explain that decision and the reasoning to all beneficiaries in a brief email. If asset valuations aren’t complete, send a preliminary accounting showing what you know and what’s still pending.

Beneficiaries who understand the process rarely litigate; beneficiaries kept in the dark almost always do.

Asset Valuation and Document Gathering Sabotage Timelines

Asset valuation and document gathering delays sabotage more timelines than any other factor, particularly in estates with real property. Orange County real estate requires professional appraisals for trust administration, and getting a qualified appraiser scheduled, completed, and paid takes six to ten weeks if you move fast. Personal property-art, antiques, vehicles, collectibles-often requires specialized appraisers, and these professionals book months in advance.

Start appraisals immediately after death, even before the trust is fully inventoried. The trustee who waits until month three to order appraisals watches the timeline slip into month nine because appraisers are booked.

Missing original trust documents, unclear deed recordings, or scattered investment account statements compound these delays exponentially. Create a master spreadsheet in week one listing every known asset, account number, current custodian, and approximate value, then systematically track which items have been located and valued. Financial institutions hold assets that beneficiaries don’t know exist-safe deposit boxes, forgotten investment accounts, life insurance proceeds-and you’re legally responsible for finding them.

Contact the decedent’s employer, banks, and insurance agents directly; don’t rely on what beneficiaries remember. Orange County probate courts have seen trustees miss millions in assets because they accepted incomplete information from family members.

Moving Forward with Professional Coordination

The trustee who stays ahead of these three problems-taxes, communication, and documentation-keeps administration moving. The trustee who reacts to them watches the 6 to 12 month timeline become 18 to 24 months. Your next challenge involves deciding whether to handle these coordination tasks alone or bring in professional support to manage the complexity, which directly affects both your timeline and your personal liability exposure.

How to Build a System That Keeps Your Trust Administration on Track

Create Your Master Asset Spreadsheet

The difference between a trust administration that finishes in nine months and one that drags into year two comes down to systems, not luck. Start a master asset spreadsheet on day one with columns for asset type, account number, financial institution, estimated value, appraisal status, tax ID number, and date located. This single document becomes your accountability tool and prevents the chaos of scattered information. Orange County trustees who skip this step typically lose weeks searching for duplicate accounts, missing statements, or forgotten safe deposit boxes. The spreadsheet tracks every account and document location systematically, which protects you from accusations of incomplete administration.

Establish a Dedicated Trust Bank Account and Communication Log

Open a dedicated trust bank account within two weeks of death and route all trust income, reimbursements, and expense payments through it. This account creates an auditable record that protects you from accusations of self-dealing. When a beneficiary questions whether you spent trust money on personal expenses, the bank statements tell the complete story. For the communication log, record the date and method of every notification to beneficiaries, whether email, certified mail, or in-person meeting. Include what information you provided and who received it. This documentation defends you if a beneficiary later claims they were kept in the dark, and courts view trustees with contemporaneous records far more favorably than those reconstructing communications months later.

Execute Your First-Month Action Plan

Assign yourself a hard deadline for the first month: complete the asset inventory, obtain the trust EIN from the IRS, notify all beneficiaries in writing, order appraisals for real property, and contact a CPA about tax planning. Orange County estates with rental properties need immediate attention to property management decisions because neglecting tenant communications or maintenance issues creates liability and eats into your timeline with crisis responses. Schedule monthly check-ins with your CPA and attorney starting in month one, not month six. These professionals spot problems early when they’re still fixable, rather than discovering tax complications in month eleven when distributions are already delayed. Ask your CPA specifically whether Form 706 applies to your estate and when estimated tax payments are due if administration extends past year-end.

Manage Investments and Communicate Proactively

If your trust holds investment accounts, direct the custodian to freeze the portfolio in a conservative allocation rather than leaving it exposed to market risk during administration. Active management is required under California’s Prudent Investor Rule, but that does not mean taking unnecessary risk while assets are being valued and distributed. Document this decision and the reasoning in writing to your beneficiaries. The trustee who communicates proactively about investment strategy, tax planning, and timeline expectations eliminates the suspicion that breeds litigation. Send beneficiaries a written preliminary accounting within 60 days showing what assets you have located, which are still pending appraisal, and your estimated timeline for distributions. This single document prevents months of tension because beneficiaries understand what is happening and why they are not receiving money yet.

Final Thoughts

Trust administration in Orange County typically takes 6 to 12 months when you move decisively from day one. This timeline assumes you open a dedicated trust bank account, notify beneficiaries within 60 days, coordinate with a CPA on tax planning, and order appraisals for real property immediately. The trustees who finish on schedule treat the first month as the most critical period, not a time to gather information slowly.

The common thread running through every delayed trust administration is reactive management rather than proactive planning. Trustees who wait for problems to surface before contacting a CPA, ordering appraisals, or communicating with beneficiaries inevitably miss deadlines that cascade into tax complications, property disputes, and litigation. The creditor claims window, the nine-month federal tax deadline, and the 60-day beneficiary notification requirement are non-negotiable, and missing any of these creates personal liability that no amount of later effort can fix.

If your trust holds rental properties, significant investment accounts, or real estate in multiple counties, professional guidance from day one prevents costly mistakes. We at Law Offices of Roshni T. Desai provide personalized estate administration support tailored to Orange County estates, and a free consultation helps you build a customized action plan for your trust administration timeline and clarifies which tasks you can handle independently and which require professional coordination.