Probate Executor Checklist: A Clear, Actionable Roadmap

Serving as an executor is one of the most demanding roles you can take on after someone passes away. The responsibilities are real, the deadlines are strict, and mistakes can cost the estate thousands of dollars.

We at Law Offices of Roshni T. Desai created this probate executor checklist to give you a clear, step-by-step roadmap through the entire process. You’ll know exactly what to do, when to do it, and where to get help when you need it.

Understanding Your Role as Executor

Your Fiduciary Duty Is a Legal Obligation

The executor’s job is not ceremonial. You hold a fiduciary duty, which means you must act in the best interest of the estate and its beneficiaries, not yourself. This is a legal obligation enforced by the probate court. According to Forbes and Justia, your primary duty is to administer the deceased’s financial affairs according to the will and serve as a fiduciary for the estate and its beneficiaries. The court can hold you personally liable if you mishandle funds, fail to pay valid debts, or distribute assets improperly.

The Real Stakes of the Role

The stakes are real: one misplaced transaction or missed deadline can trigger lawsuits from beneficiaries or creditors. You must keep meticulous records of every dollar spent, every asset moved, and every decision made. Open a separate estate bank account immediately to keep estate money completely separate from your personal funds. This single step protects you and makes the final accounting transparent.

Timeline and Workload Expectations

The timeline varies by state and estate complexity, but simple estates typically close within six to twelve months, while complicated ones can stretch two to three years. Forbes notes that the typical estate requires about 570 hours of work over roughly 16 months, so this is not a casual responsibility. You’ll face strict deadlines: filing the will with the probate court, notifying creditors and beneficiaries within specific windows, filing tax returns, and obtaining court approval before distributing anything to beneficiaries. Miss a deadline and the court may deny your petition or extend the process.

How to Prevent Common Mistakes and Family Conflict

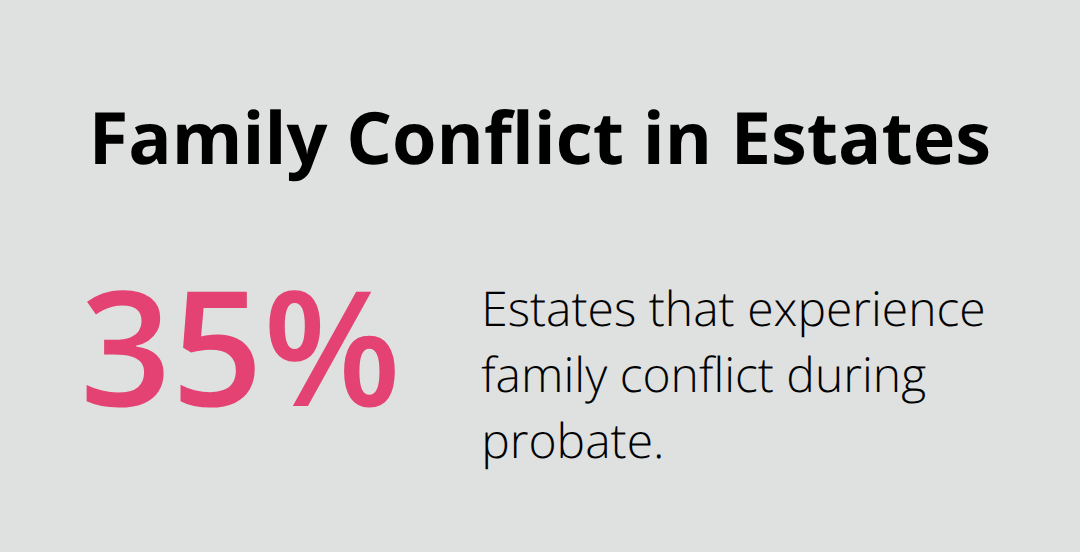

The most common executor mistakes are commingling personal and estate funds, failing to notify all creditors, skipping the formal inventory filing, and distributing assets before debts and taxes are paid. About 35 percent of estates experience family conflict, and most of it stems from poor communication, unclear asset tracking, or perceived unfairness in distributions. You prevent this by maintaining absolute transparency with beneficiaries, sharing your records regularly, and following the will or state law precisely.

If you’re unsure about any step, get help early rather than guessing and creating problems later. The next section walks you through the essential tasks that demand your immediate attention once probate begins.

What to Do First When Probate Begins

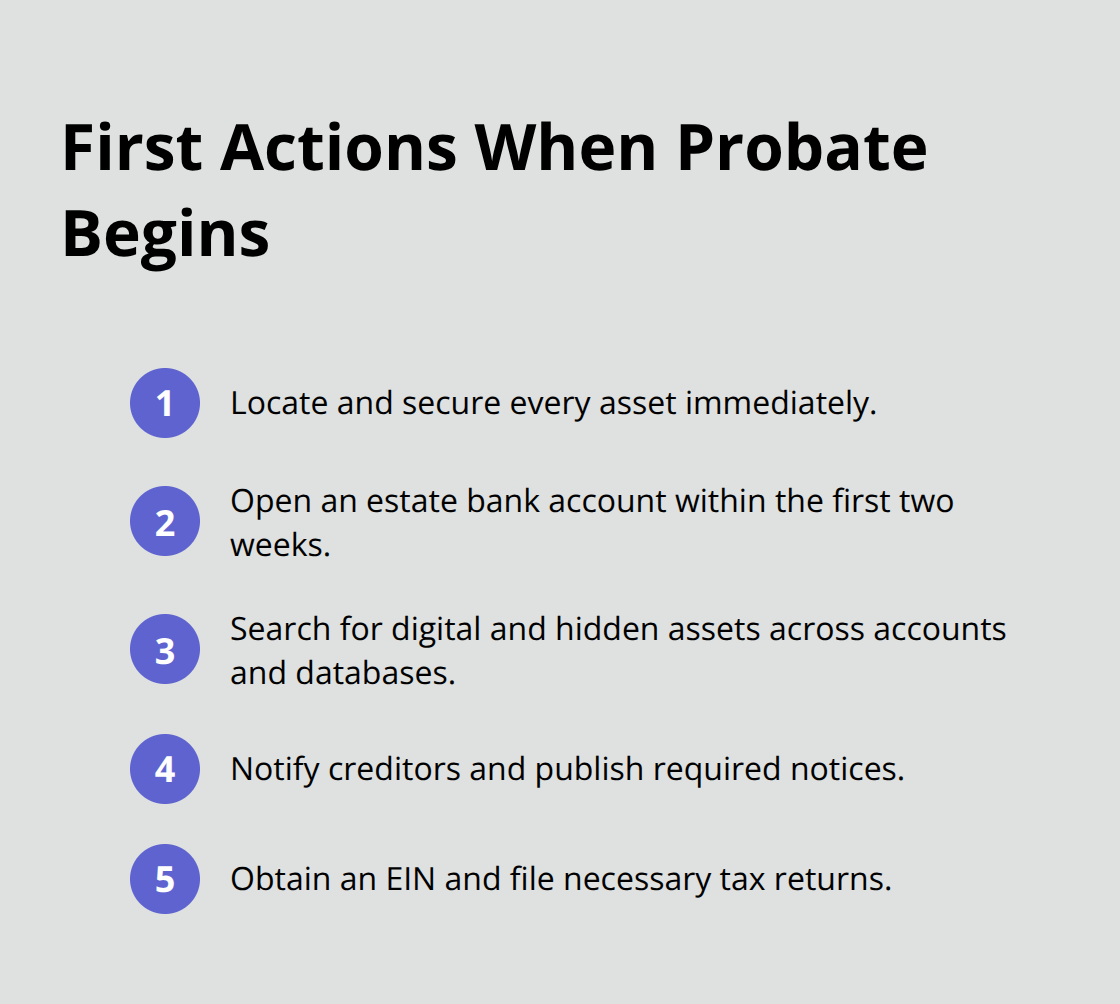

Locate and Secure Every Asset Immediately

The moment probate opens, you shift from grief to action. Your first priority is locating and securing every asset the deceased owned. Search through the deceased’s home, safe deposit boxes, and storage units for financial statements, deeds, insurance policies, and bank account records. You must compile a complete inventory of probate assets that includes real estate, bank accounts, retirement accounts, stocks and bonds, and personal effects. Open an estate bank account within the first two weeks and transfer all liquid assets into it immediately. This account becomes your command center for managing the estate’s money. Do not commingle these funds with your personal accounts under any circumstances.

Uncover Hidden and Digital Assets

Conduct a thorough search for digital assets: check email accounts, cryptocurrency wallets, domain names, cloud storage services, and any online accounts tied to the deceased. Many executors miss thousands of dollars in forgotten bank accounts or unclaimed property. Search your state’s unclaimed property database and the national database to uncover assets the deceased may have forgotten about years ago. Once you have a preliminary list, hire a certified appraiser for major assets like real estate, art, or collectibles. The probate court requires formal valuations, and these appraisals establish the estate’s fair market value for tax purposes.

Notify Creditors and Manage Outstanding Debts

Simultaneously, you must notify creditors and manage the estate’s debts before distributing anything to beneficiaries. File a creditor notice in the probate court, and in many states you must publish this notice in a local newspaper to inform potential claimants. You should examine creditor claims and pay valid debts in the order required by state law (typically secured debts first, then unsecured debts). Set aside money from the estate to cover all final expenses, funeral costs, and outstanding bills like mortgages and utilities.

Handle Tax Filings and Estate Administration

File the deceased’s final Form 1040 income tax return and obtain an employer identification number (EIN) for the estate so you can open that bank account and file estate tax returns. If the estate’s gross value exceeds the federal threshold, you may need to file Form 706 for federal estate tax. Hire a CPA or tax attorney to handle these filings correctly because mistakes trigger audits and penalties. The filing deadline for the final income tax return is typically the same as any other individual return, but the EIN application can be completed online immediately through the IRS website.

Move Forward With Confidence Into Asset Distribution

These early months are hectic, but proper asset documentation and debt management prevent disputes later and keep you compliant with court deadlines. With assets secured, creditors notified, and taxes filed, you now have the foundation to move into the next phase: distributing the estate to beneficiaries and closing probate through the court system.

Distributing Assets and Closing the Estate

File Your Final Accounting With the Probate Court

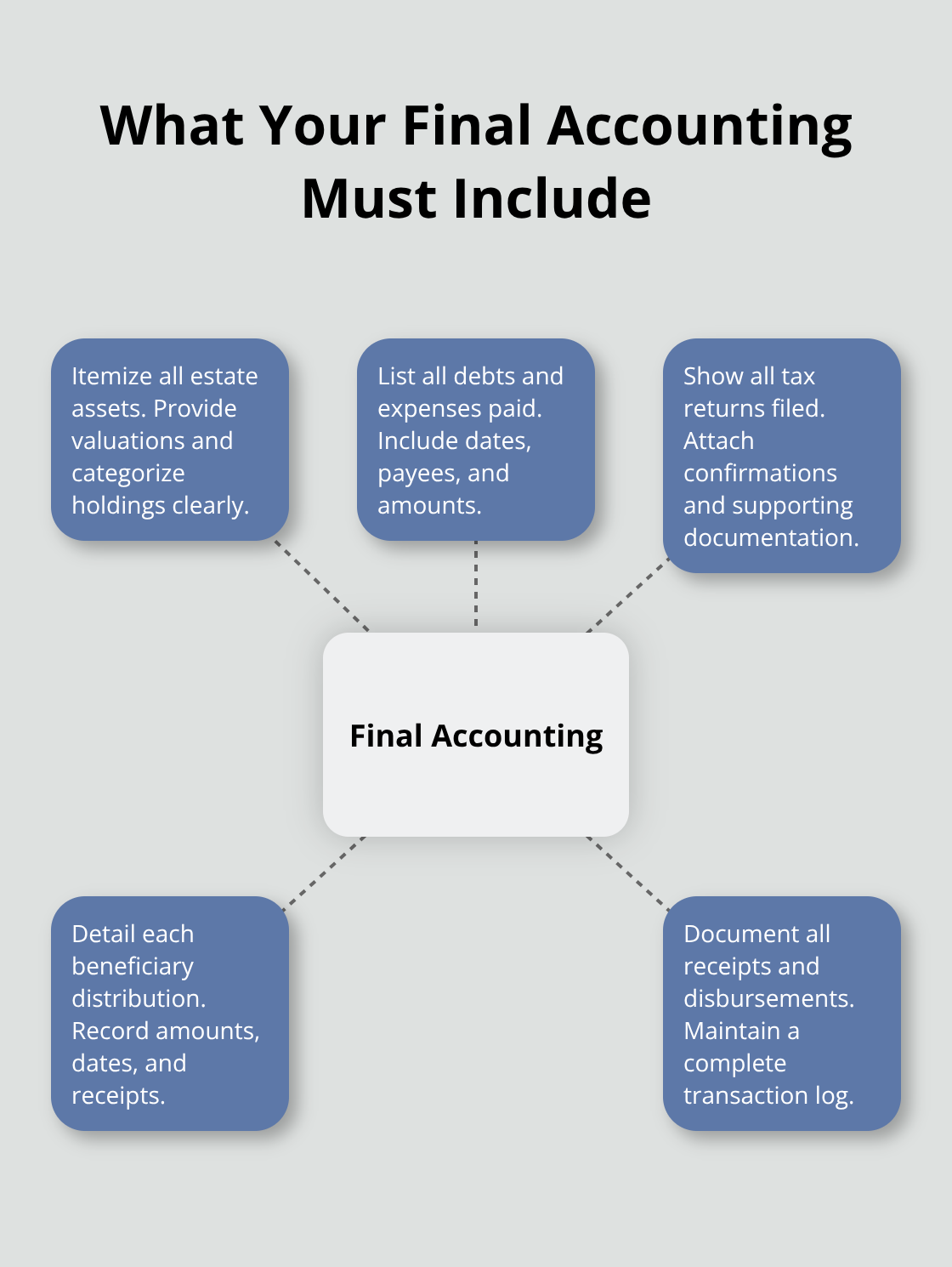

Once debts, taxes, and final expenses are paid, you move into the distribution phase-the moment beneficiaries finally receive their inheritance. This is where many executors make costly mistakes because they rush to hand out money before obtaining formal court approval. The probate court requires you to file a final accounting that documents every dollar received, spent, and distributed. This accounting must itemize all assets, list all debts paid, show tax returns filed, and detail each distribution to beneficiaries.

The court reviews this accounting to verify you’ve acted properly and within the will’s terms or state law. Only after the judge approves your accounting can you legally distribute the remaining assets.

Protect Yourself and Beneficiaries With a Reserve Fund

If you skip court approval and distribute early, beneficiaries can sue you personally if creditors or tax authorities later make claims against the estate. Set aside a reserve fund-typically 5 to 10 percent of the remaining assets-to cover unexpected final expenses or tax liabilities that emerge during the closing process. This buffer prevents you from having to clawback distributions from beneficiaries, which creates resentment and legal complications.

Calculate and Document Each Beneficiary’s Share

When calculating each beneficiary’s share, follow the will exactly. If the will specifies dollar amounts, percentages, or specific items, distribute accordingly. If multiple beneficiaries want the same personal item and the will doesn’t specify who gets it, use a fair method such as an auction or round-robin selection process. Document every decision in writing and have each beneficiary sign a receipt acknowledging what they received. This protects you from future disputes and proves you acted transparently.

Obtain the Court’s Order of Discharge

After all distributions are complete, you file a petition for closure with the probate court. This petition includes your final accounting, proof that all debts and taxes are paid, and documentation that all beneficiaries received their distributions. The court reviews this petition and issues an Order of Discharge, which formally releases you from your duties and closes the estate. This discharge is your legal protection against future claims. Without it, beneficiaries or creditors could theoretically pursue you years later. The entire closing process typically takes 30 to 60 days once you file the petition, assuming no objections arise.

Maintain Records and Seek Professional Guidance When Needed

Retain all estate records-bank statements, receipts, tax returns, court filings, beneficiary agreements-for at least seven years. These records prove compliance if questions arise later and protect you from audit exposure. If you’re managing a complex estate with multiple properties, business interests, or significant tax issues, work with a probate attorney during the distribution and closing phase. A final accounting error or missing document can extend probate by months and cost thousands in additional legal fees.

Final Thoughts

Serving as an executor demands organization, attention to detail, and the willingness to ask for help when you need it. This probate executor checklist walks you through every phase: understanding your fiduciary duty, securing assets and managing debts, filing taxes, and distributing the estate with court approval. The stakes are high, but following these steps protects you from personal liability and prevents the family conflict that derails so many estates.

Most executors are first-timers who handle legal and financial responsibilities during grief, and you’re not expected to know probate law or tax code. The 570 hours of work spread across 16 months is substantial, and rushing through any phase creates expensive problems later. If you’re uncertain about notifying creditors, calculating tax liability, or filing your final accounting, that’s the moment to bring in professional support.

We at Law Offices of Roshni T. Desai understand the weight of this role and provide personalized probate services across Southern California. Contact Law Offices of Roshni T. Desai to discuss your specific situation with a free consultation and flexible scheduling, with no pressure or cost upfront.