The Trust Administration Process Demystified for Property Owners in Orange County, California

Many property owners in Orange County create trusts to protect their assets, but few understand what happens next. The trust administration process involves specific steps, timelines, and responsibilities that can feel overwhelming without proper guidance.

At Law Offices of Roshni T. Desai, we’ve seen firsthand how confusion during trust administration leads to costly mistakes. This guide breaks down what you need to know to manage your property and trust effectively.

What Happens When You Transfer Property Into a Trust

Creating a trust means shifting ownership of your property from your personal name into the trust’s name. This transfer is not optional-it’s the foundation that makes your trust actually work. Without moving property into the trust, the trust sits empty and provides no protection. Orange County property owners often create the trust document but then fail to retitle their assets, which defeats the entire purpose.

How Property Moves Into Your Trust

The transfer process requires updating deeds for real estate, changing titling on bank accounts and investment accounts, and updating beneficiary designations on retirement accounts. For real estate in Orange County, you record a new deed with the county recorder showing the trust as the owner. The process is straightforward but requires attention to detail. You’ll need the original property deed, the trust document, and sometimes a title company to prepare the new deed correctly.

Banks and financial institutions require a Certification of Trust, which proves the trust exists and shows who has authority to act, without revealing the full trust contents to third parties. Once property is titled in the trust, the trustee-the person you named to manage it-steps into the role of legal owner, though they hold that ownership for the benefit of your beneficiaries.

Managing Trust Property While You’re Alive

While you’re alive and able, your role as trustee allows you to manage trust property as you normally would. You pay the mortgage, collect rental income, maintain insurance, and make investment decisions. The trustee’s duties under California Probate Code sections 16060 through 16069 require acting in the beneficiaries’ best interests, keeping trust property separate from personal property, and investing with reasonable care. This doesn’t mean you need to hire professionals or make dramatic changes-it means treating trust property with the same prudence you’d use for your own finances.

Many property owners worry that creating a trust complicates daily management, but it doesn’t. You still live in your home, collect rent from investment properties, and access your accounts normally. The real shift comes after death, when the successor trustee takes over and must follow specific rules.

Property Taxes and Ongoing Maintenance Duties

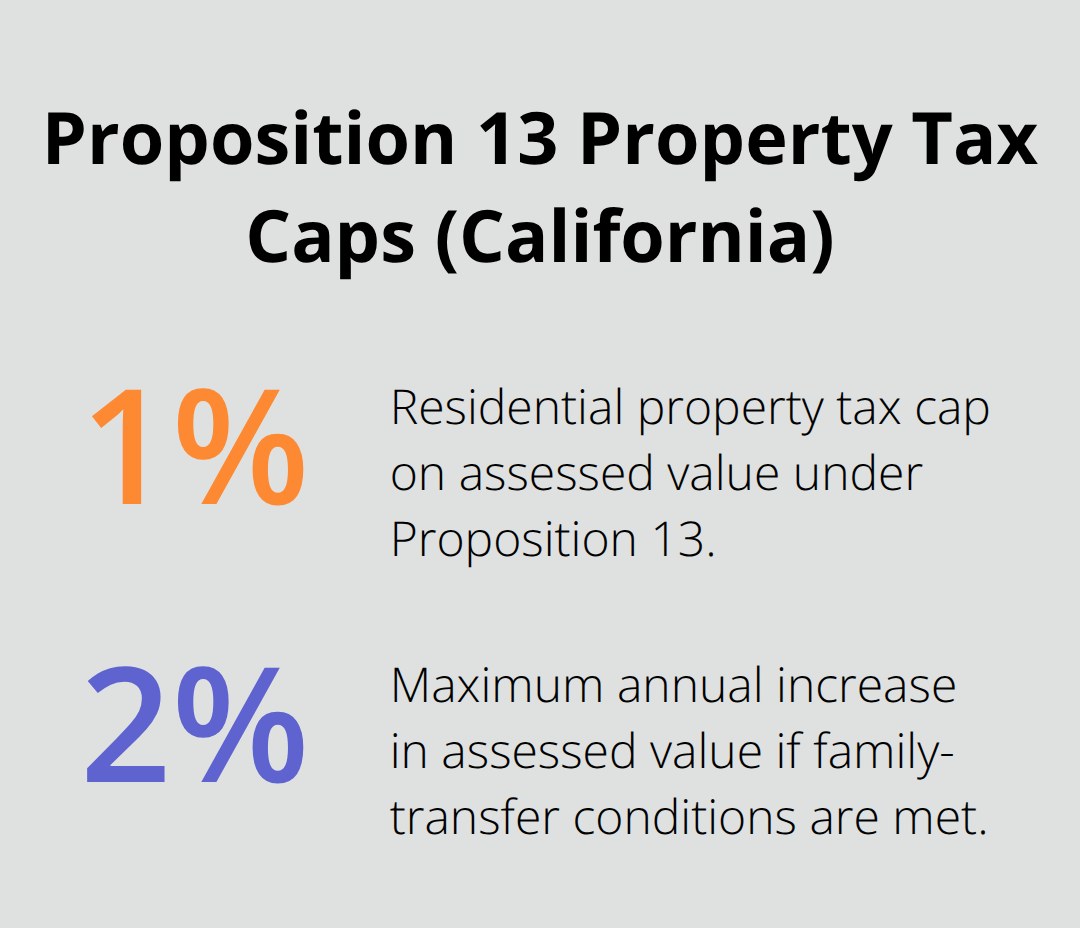

For Orange County property owners with real estate, the trustee must maintain the property, pay property taxes, and handle insurance. California Proposition 13 caps residential property taxes at 1% of assessed value with annual increases limited to 2%, but only if the property stays in the family under specific conditions.

If a trustee fails to maintain proper records or mixes trust property with personal assets, it creates problems later when distributions must happen or if beneficiaries question whether the trust was managed correctly.

These foundational steps-proper titling, clear record-keeping, and attention to tax obligations-set the stage for what happens next. When the grantor passes away, the successor trustee inherits not just the property but also a detailed set of responsibilities that begin immediately.

The First 90 Days After Death: Critical Tasks and Deadlines

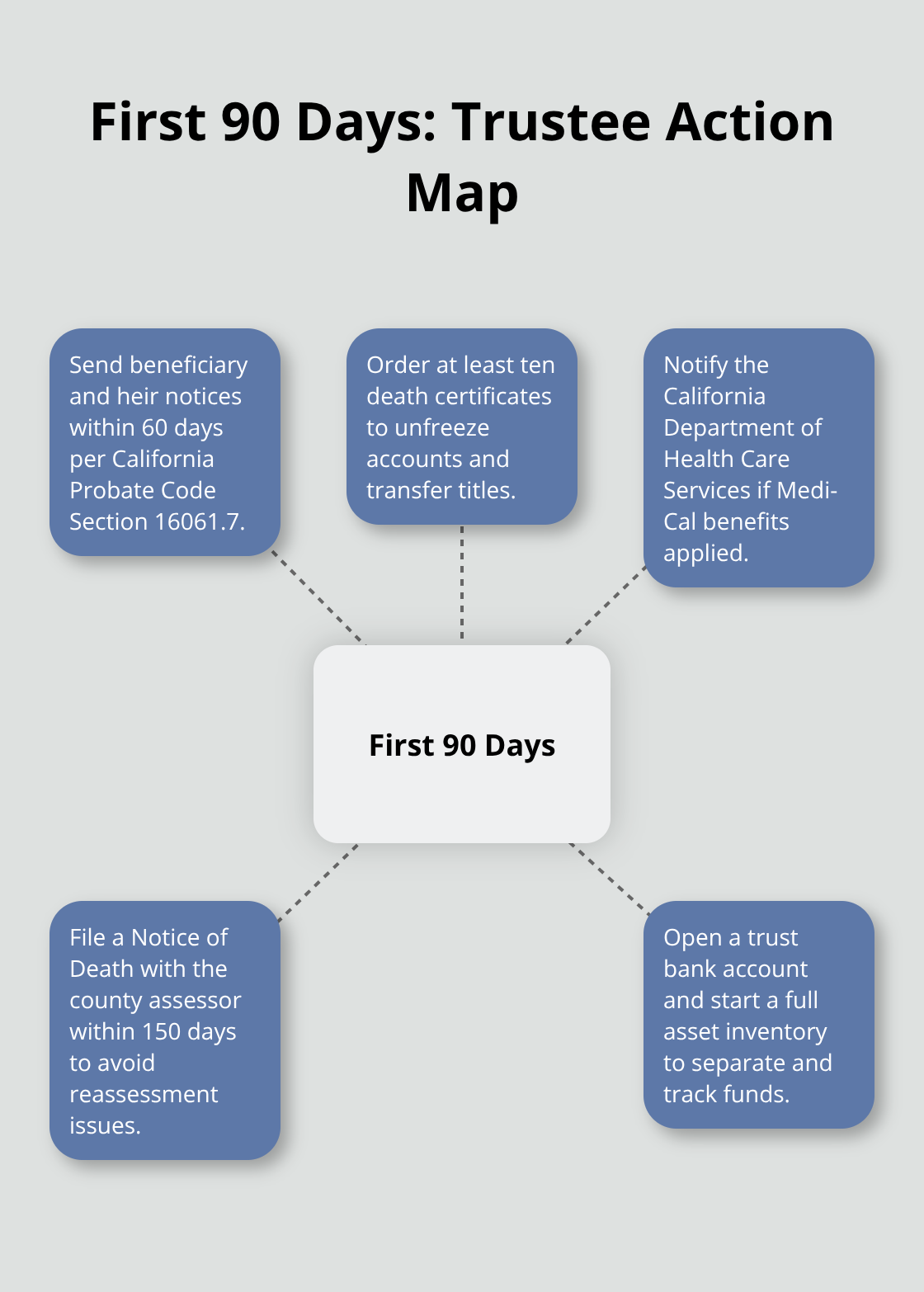

The moment a grantor passes away, the successor trustee faces a compressed timeline with multiple statutory deadlines. California Probate Code Section 16061.7 requires notice to all beneficiaries and heirs within 60 days of death. The trustee must also obtain at least ten death certificates immediately-one for each financial institution, the county assessor, and tax authorities. Without these certificates, banks freeze accounts and won’t transfer property titles.

Securing Documents and Notifying Required Parties

The successor trustee should secure the original trust document and locate the grantor’s final tax returns without delay. Compile a complete list of beneficiaries with current contact information to streamline notices. The trustee must notify the California Department of Health Care Services if the grantor received Medi-Cal benefits. File a Notice of Death with the county assessor within 150 days per Revenue and Taxation Code Section 480(b). For Orange County property owners, property tax reassessment can trigger unexpectedly if the trustee misses this deadline.

Hiring an attorney at this stage prevents costly errors. Trustees who lack guidance often miss deadlines because they don’t understand which documents to file first or in what order.

Opening a Trust Bank Account and Inventorying Assets

The trustee must open a trust bank account in the trust’s name using an Employer Identification Number from the IRS. This step segregates trust funds from personal money and creates an auditable record that protects the trustee from liability claims. Many trustees mistakenly deposit trust assets into their personal accounts, which courts view as commingling and can lead to beneficiary disputes or accusations of theft.

Simultaneously, the trustee should inventory all trust assets, including bank balances, investment accounts, real estate, vehicles, and personal property. Determine which assets were titled in the trust versus which require a Heggstad petition to bring into the trust through court action. This inventory becomes the foundation for all subsequent decisions about distributions and tax obligations.

Valuing Property and Understanding Tax Implications

For real estate, obtain appraisals at the date of death to establish the step-up in basis for tax purposes. This valuation determines how much capital gains tax beneficiaries owe if they sell the property later. If the grantor owned property in Orange County, the trustee must address California Proposition 19 implications immediately. As of February 2025 through February 2027, the reassessment exclusion amount is $1,044,586 for parent-to-child home transfers. Exceeding this threshold triggers partial reassessment that can dramatically increase property taxes.

The trustee must also decide whether to file IRS Form 706 for federal estate tax and prepare the grantor’s final Form 1040 income tax return, along with Form 1041 for the trust itself if it generates income. Delaying these decisions compounds complications later when distributions cannot happen until tax obligations are settled. These early determinations shape the entire administration timeline and affect how much property beneficiaries ultimately receive.

Three Trust Administration Mistakes That Cost Orange County Property Owners Thousands

The gap between creating a trust and administering it correctly is where most property owners stumble. The trustee inherits not just assets but legal obligations that demand precision from day one. Missing even one requirement can trigger tax penalties, property reassessment, or beneficiary litigation that drains the estate. Orange County property owners face particular pressure because California Proposition 19 rules around property reassessment create time-sensitive decisions that cannot be undone.

Failing to Retitle Assets Into the Trust During Your Lifetime

A trust only controls property that sits inside it. If you created a trust document but never transferred the deed, bank accounts, or investment titles, those assets bypass the trust entirely and require probate court intervention through a Heggstad petition. This probate process costs $3,000 to $7,000 in attorney fees and court costs, delays distributions by six to twelve months, and exposes family financial details to public court records. Orange County property owners who kept real estate in personal names discover too late that the trustee cannot simply transfer the deed without court approval.

The solution is straightforward: transfer property into the trust while alive, obtain a Certification of Trust from the trustee, and confirm with banks that the title change is complete. You continue to live in your home, pay the same property taxes, and access your accounts identically. The only difference is the legal owner is now the trust rather than your personal name. This step takes weeks to complete but prevents months of probate court delays later.

Neglecting to File Required Tax Returns on Time

The trustee must file your final Form 1040 within the normal tax deadline (April 15 following the year of death), obtain an Employer Identification Number for the trust, and file Form 1041 for any income the trust generates during administration. Missing these deadlines triggers IRS penalties of 5% to 25% per month of unpaid tax, plus interest that compounds daily. If the trust owns rental property or investment accounts, the failure to file Form 1041 prevents beneficiaries from claiming their share of deductions and can result in double taxation.

For Orange County estates with real property, the trustee must also file with the county assessor within 150 days of death to avoid reassessment penalties under Revenue and Taxation Code Section 480(b). Many trustees wait to hire an accountant or attorney until months after death, thinking they can catch up later. That approach backfires. The IRS does not grant extensions for trusts, and the Franchise Tax Board in California assesses penalties immediately. A trustee who waits six months to file a return owes penalties on six months of unpaid tax. Contact a tax professional within two weeks of death, gather your final documents, and establish a filing timeline before deadlines arrive.

Mixing Personal and Trust Finances

A trustee who deposits trust assets into a personal bank account or pays personal expenses from the trust account creates liability for themselves and reasonable grounds for beneficiaries to question the administration. California Probate Code Section 15001 requires the trustee to keep trust property separate from personal property. Courts interpret commingling as evidence of mismanagement or breach of fiduciary duty. If a beneficiary sues and the trustee cannot produce clear trust bank statements showing every deposit and withdrawal, the court may surcharge the trustee personally for the missing funds.

Beyond legal risk, commingling makes accounting nearly impossible. When the trustee closes the trust, they must provide a final accounting showing where every dollar came from and where it went. A trustee who mixed funds cannot produce this accounting without months of bank statement reviews and reconstruction. Open a dedicated trust bank account immediately after death using the trust’s Employer Identification Number, deposit all trust assets into this account, and pay all trust expenses from this account only. Keep personal expenses entirely separate. If the trustee needs reimbursement for expenses paid from personal funds, document each expense with a receipt and request reimbursement from the trust account once it is established. This separation takes thirty minutes to set up but prevents years of potential disputes and protects the trustee from personal liability.

Final Thoughts

Trust administration requires precision, timing, and knowledge of California law that most property owners simply don’t possess. The mistakes outlined in this guide-failing to retitle assets, missing tax deadlines, and commingling funds-are preventable, yet they happen repeatedly because trustees attempt to navigate the process alone. Each error costs thousands in penalties, delays distributions, or triggers litigation that consumes time and money that should go to beneficiaries.

The trust administration process demands attention to multiple deadlines within the first 90 days of death. Missing the 60-day notice requirement, the 150-day assessor notification, or tax filing deadlines creates cascading problems that compound over months. For Orange County property owners, California Proposition 19 rules add another layer of complexity because reassessment decisions cannot be reversed once made. A trustee who waits too long to address property valuation or fails to file the correct forms with the assessor may inadvertently trigger thousands in additional property taxes that beneficiaries must absorb.

Professional guidance at the outset prevents these outcomes. An attorney who understands California probate law can establish the correct timeline, ensure all documents are filed on schedule, and coordinate with tax professionals to handle Form 1041 and final income tax returns correctly. Contact Law Offices of Roshni T. Desai to schedule a free consultation and discuss how we can help you navigate the trust administration process with confidence.