Trust Administration Attorney Guidance: Practical Tips for Clients

Trust administration requires careful attention to legal requirements and deadlines. Many clients face confusion about what steps to take first and which mistakes could create costly problems down the road.

At Law Offices of Roshni T. Desai, we provide trust administration attorney guidance to help you navigate this process with confidence. This guide covers what you need to know and how professional support can protect your interests.

What Trust Administration Requires

Locating and Cataloging Trust Assets

Trust administration begins the moment the trustmaker passes away. Your first responsibility involves locating and cataloging every asset titled to the trust, plus any property that should have been transferred into the trust before death. This includes real estate, bank accounts, investment portfolios, business interests, and digital assets.

Most trustees miss assets because they only check obvious places. They forget about old savings accounts, safe deposit boxes, or insurance policies where the trust is named beneficiary. The Uniform Trust Code, adopted in most states, requires trustees to identify and marshal all trust property-incomplete asset discovery creates legal exposure and delays distributions.

Start by obtaining a copy of the trust document and any amendments, then request certified copies of the trustmaker’s death certificate. Contact banks, brokerages, and insurance companies directly with the death certificate and trust document to locate accounts. Pull property tax records and deed searches through your county assessor’s office to find real estate. Check for digital assets by reviewing email accounts, password managers, and statements for cryptocurrency exchanges or online brokerage accounts (this step is often overlooked and causes families to lose access to significant holdings).

Settling Debts and Taxes Before Distribution

Your second responsibility involves settling debts and taxes before making distributions to beneficiaries. North Carolina law requires trustees to pay outstanding debts, funeral expenses, and state and federal income taxes from trust funds. File a final income tax return for the trustmaker and an estate tax return if the gross estate exceeds $13.61 million in 2024.

Many trustees underestimate tax liability and distribute funds prematurely, leaving beneficiaries responsible for unpaid taxes. This mistake creates serious problems. Work through all outstanding obligations systematically and verify payment before moving forward with any distributions to beneficiaries.

Distributing Assets According to Trust Terms

Your third duty involves distributing remaining assets to beneficiaries according to the trust terms. The trust document specifies whether distributions happen immediately, over time, or under certain conditions. Do not distribute funds until you have settled all debts and taxes, verified you have paid all required bills, and obtained written acknowledgments from beneficiaries confirming receipt.

Maintain detailed records of every transaction, payment, and distribution (this documentation protects you if a beneficiary later disputes your administration). Proper record-keeping also helps you track what remains in the trust and what has already transferred to beneficiaries, preventing confusion and disputes down the line.

When multiple beneficiaries are involved or when the trust contains complex assets, the distribution phase becomes more intricate. This is where professional guidance helps you navigate competing interests and ensure compliance with both the trust document and state law.

Common Mistakes Clients Make During Trust Administration

Trustees often rush through the early stages of administration and create problems that take months to unwind. The most damaging mistakes happen when beneficiaries stay uninformed, when trust assets get mixed with personal money, or when tax obligations are ignored. These errors are not technical slip-ups-they reflect a failure to treat trust administration with the seriousness it demands. The Uniform Trust Code requires trustees to act with prudence and loyalty, and violating these duties through carelessness exposes you to liability and damages family relationships permanently.

Failing to Notify Beneficiaries Promptly

Notifying beneficiaries within a reasonable timeframe ranks as the costliest mistake trustees make. North Carolina law requires trustees to provide beneficiaries with notice of the trustmaker’s death and information about the trust within specific timeframes. Many trustees delay this notification hoping to resolve issues quietly, but silence breeds suspicion and legal challenges. Beneficiaries have a right to know the trust terms, the assets involved, and the administration timeline.

When you withhold this information, beneficiaries assume the worst and often hire their own attorneys to investigate. This defensive posture turns a straightforward administration into a contested matter with legal fees that drain trust assets. Write to beneficiaries immediately after the trustmaker’s death, provide a copy of the trust document, and establish a communication schedule so they understand what happens next and when to expect updates. This transparency prevents disputes and demonstrates that you are managing the trust responsibly.

Mixing Trust Assets with Personal Funds

Mixing trust assets with personal funds undermines the entire legal structure of the trust. Trustees who deposit trust money into their personal bank account lose the clear accounting that protects them from accusations of theft or misappropriation. If the trustee’s personal account is ever audited or frozen by creditors, trust assets can be seized to satisfy personal debts.

Separate trust accounts with clear labeling prevent these problems and satisfy fiduciary duties. Open a dedicated trust checking account at your bank immediately after death, use the trust name on all account documents, and deposit all trust assets there before paying any bills or making distributions. Never use personal funds to pay trust expenses and then reimburse yourself later-this creates documentation gaps that invite scrutiny. Maintain monthly reconciliations between the trust account and the trust’s asset list to catch errors early.

Neglecting to File Required Tax Returns

Neglecting to file required tax returns creates serious consequences that follow trustees for years. Federal estate tax returns are required if the gross estate exceeds $13.61 million in 2024, but state income tax returns and final individual income tax returns are required regardless of estate size. Trustees who skip these filings face penalties, interest charges, and personal liability for unpaid taxes.

The IRS and state tax authorities will pursue the trustee personally if trust funds are insufficient. File the trustmaker’s final 1040 tax return and the estate income tax return (Form 1041) within the required deadlines, even if you believe no taxes are owed. Work with a tax professional or trust administration attorney to calculate estimated tax liability before you make any distributions to beneficiaries. Once beneficiaries receive distributions, they become responsible for their share of unpaid taxes, which damages your credibility and invites litigation.

These three mistakes-silence, commingling funds, and tax neglect-create cascading problems that pull you into disputes you could have prevented. Understanding how a trust administration attorney supports you through each phase of administration helps you avoid these pitfalls and keep the process moving forward.

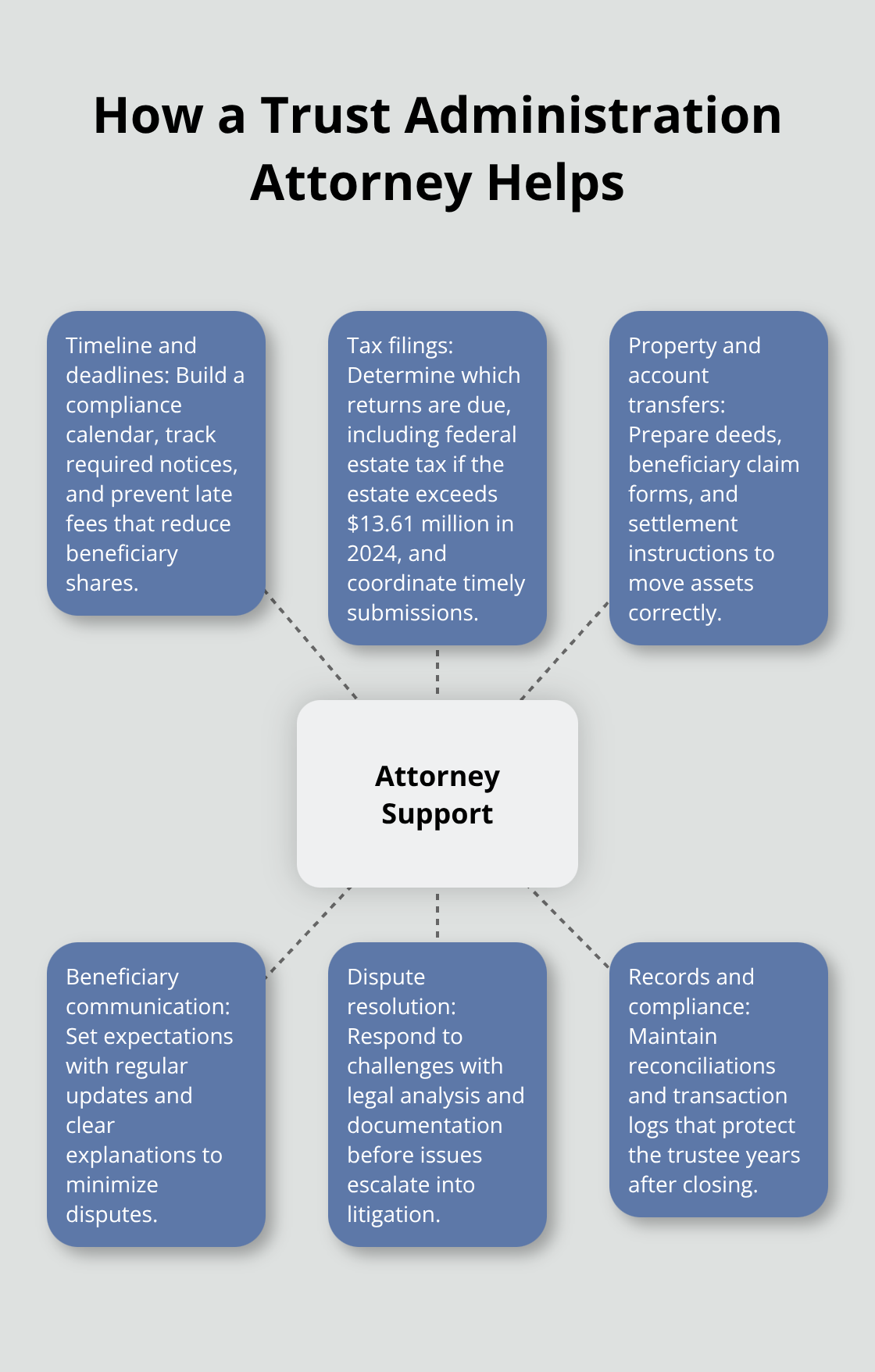

How a Trust Administration Attorney Supports You

A trust administration attorney handles the paperwork, deadlines, and legal requirements that trip up most trustees acting alone. We at Law Offices of Roshni T. Desai work with trustees and beneficiaries to transform confusion into clarity by managing tax filings, asset transfers, and account settlements while keeping beneficiaries informed throughout. The Uniform Trust Code requires trustees to act with prudence and loyalty, which sounds straightforward until you face competing beneficiary interests, unclear trust language, or assets that don’t fit neatly into the trust document.

Managing Paperwork and Deadlines

An attorney analyzes your specific trust and state law requirements, then builds a timeline that prevents costly delays. We identify which tax returns must be filed, when they are due, and what documentation you need to gather. For estates exceeding $13.61 million in 2024, federal estate tax returns become mandatory, but state income tax filings apply regardless of size. Missing even one deadline triggers penalties and interest that reduce what beneficiaries ultimately receive.

Handling Property Transfers and Account Settlements

We also handle the property transfers that trustees often botch by moving too slowly or using incorrect procedures. Real estate titled to the trust requires deed transfers with proper legal descriptions and notarization. Bank accounts need beneficiary claim forms or transfer paperwork signed by the trustee. Investment accounts demand specific settlement instructions and tax identification numbers. Digital assets present unique challenges because cryptocurrency exchanges rarely recognize trust authority without explicit platform documentation, and password managers require proper access procedures to avoid permanent loss of funds.

Resolving Beneficiary Disputes

When beneficiaries disagree about distributions, trust interpretation, or the trustee’s actions, an attorney prevents disputes from escalating into litigation that consumes months and depletes trust assets. We draft communication letters that explain the trustee’s decisions clearly and document why certain distributions are delayed or denied. If a beneficiary challenges the trustee’s actions or questions the trust’s validity, we respond with legal analysis and evidence rather than defensive silence.

Coordinating Tax and Distribution Strategy

We also coordinate with accountants and tax professionals to ensure that income tax liability is calculated correctly before distributions occur, preventing the scenario where beneficiaries receive money only to face unexpected tax bills. Trustees who handle administration alone often underestimate tax consequences and distribute funds prematurely, creating personal liability that follows them long after the trust closes. An attorney manages the reconciliation between trust assets, liabilities, and distributions, maintaining records that protect the trustee if disputes arise years later.

Advising on Long-Term Asset Management

We also advise on whether the trust should continue holding assets for minor beneficiaries or special needs individuals, or whether distributions should happen immediately. This guidance prevents trustees from making irreversible decisions based on incomplete information or misunderstanding the trust terms.

Final Thoughts

Trust administration demands attention to detail, legal compliance, and clear communication with beneficiaries. The mistakes we outlined-silence, commingled funds, and tax neglect-are entirely preventable when you understand what the process requires and when you obtain professional support early. Trustees who act alone often discover too late that they have created liability, damaged family relationships, or missed critical deadlines that trigger penalties and interest.

Professional trust administration attorney guidance transforms a complex, stressful process into a manageable one. An attorney identifies which deadlines matter most, coordinates tax filings before distributions occur, and handles property transfers using correct legal procedures. More importantly, an attorney communicates with beneficiaries on your behalf, explaining decisions clearly and preventing misunderstandings that escalate into disputes.

We at Law Offices of Roshni T. Desai provide personalized estate planning and probate services, including trust and probate administration. If you are administering a trust or facing questions about your responsibilities as trustee, contact us for a free consultation to discuss your situation and develop a clear path forward.