Trust Administration Basics: A Clear Roadmap for Families

When a loved one passes away, managing their trust becomes a responsibility that many families approach without clear direction. Trust administration basics involve several moving parts-from handling assets to filing taxes-and mistakes at any stage can create costly delays.

We at Law Offices of Roshni T. Desai have guided countless families through this process, and we know where confusion typically happens. This roadmap walks you through what trust administration actually requires and how to avoid the pitfalls that slow families down.

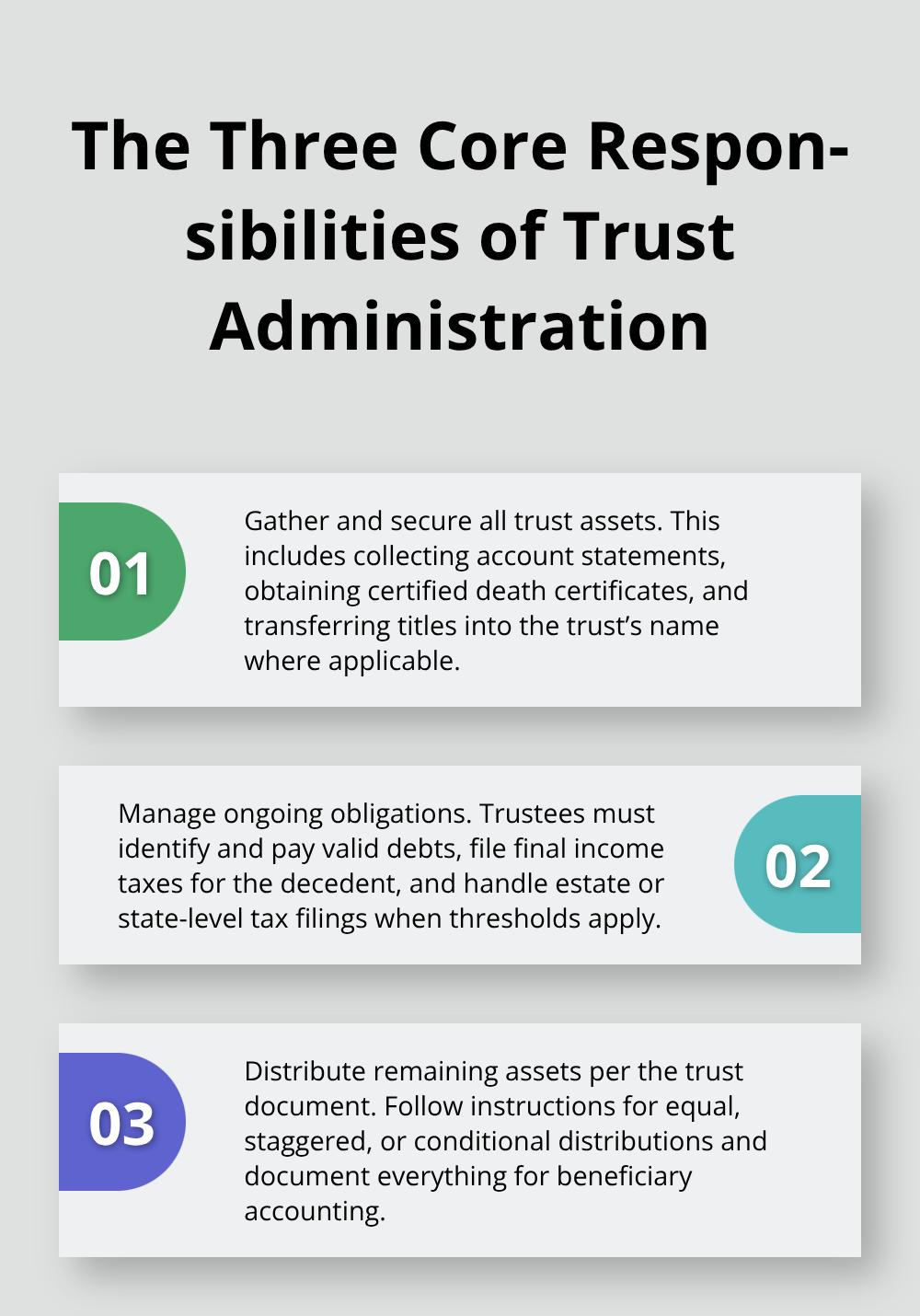

The Three Core Responsibilities of Trust Administration

Trust administration breaks down into three concrete responsibilities that trustees must handle sequentially. First, trustees gather and secure all trust assets, which typically include real estate, bank accounts, investment portfolios, vehicles, and personal property. This step requires obtaining certified copies of the death certificate, locating all relevant account statements, and transferring titles into the trust’s name where applicable. Second, trustees manage ongoing obligations by identifying and paying valid debts, filing final tax returns for the deceased, and handling estate tax filings if the estate exceeds federal exemption thresholds. The federal estate tax exemption for 2026 stands at $13.99 million per individual, meaning most families won’t face federal estate taxes, but state-level taxes may still apply depending on where the trust is administered. Third, trustees distribute remaining assets to beneficiaries according to the trust document’s specific instructions, whether that means equal distributions to multiple children, staggered payments over time, or conditional distributions tied to certain milestones.

Gathering and Securing Assets

The initial asset inventory phase determines whether administration proceeds smoothly or encounters costly delays. Trustees should create a detailed spreadsheet listing every asset, its current value, and the account or title information needed to transfer it. Real estate requires appraisals to establish the property’s fair market value at the time of death, which affects both tax filings and equitable distribution among beneficiaries. Bank accounts, investment accounts, and retirement accounts each have different transfer procedures-some institutions allow direct transfer to the trust upon presentation of a death certificate and trust certification, while others demand full trust documents or impose their own forms. Opening a dedicated trust bank account with a federal tax identification number (EIN) prevents commingling trust funds with personal assets, a critical mistake that undermines the trust’s legal protections. Trustees must document every transaction meticulously because beneficiaries will review annual accountings and may challenge distributions if records appear incomplete or questionable.

Handling Taxes and Financial Obligations

Tax compliance represents the most time-sensitive responsibility in trust administration. The decedent’s final income tax return must be filed by the standard April deadline following the year of death, and the trustee typically acts as the executor for this filing. If the estate generates income during administration-from rental properties, investment dividends, or interest-the trustee must file annual fiduciary income tax returns (Form 1041) for each year the trust remains open. Estate tax returns become necessary only if the gross estate exceeds the federal exemption, but state estate or inheritance taxes may apply at lower thresholds depending on the state where the trust is administered. Working with a CPA or tax professional familiar with trust administration prevents costly errors and ensures the trustee claims all available deductions and credits. Debts and funeral expenses must be paid from trust assets before any distributions reach beneficiaries, and the trustee should maintain copies of all invoices, bills, and payment confirmations in a centralized file.

Distributing Assets to Beneficiaries

The distribution phase requires strict adherence to the trust document’s language, not the trustee’s personal preferences or sense of fairness. Some trusts direct equal distributions to all named beneficiaries, while others specify unequal shares or conditional distributions based on factors like age, education, or financial need. Trustees should provide beneficiaries with a detailed accounting before distributions, showing all assets received, expenses paid, and the amounts each beneficiary will receive. Special needs trusts demand heightened caution because distributions must comply with the SSA’s sole benefit rule to preserve public benefits eligibility-paying for housing or food directly reduces SSI and Medicaid benefits, so trustees should consider restrictions that protect the beneficiary’s benefit status. Personal property memoranda listing specific gifts like jewelry, vehicles, or heirlooms should be distributed first, followed by cash and remaining assets according to the trust terms. Trustees must obtain signed receipts from beneficiaries for all distributions to protect against future claims that assets were never received.

Moving Forward with Confidence

These three responsibilities form the foundation of sound trust administration, but their execution often reveals complications that families don’t anticipate. Real estate transactions, multiple beneficiaries with competing interests, and tax implications specific to your state can transform what appears straightforward into a complex undertaking. Understanding these core duties positions you to recognize when professional guidance becomes necessary-and that’s where the next section addresses the common mistakes that slow families down and how to avoid them.

Common Mistakes Families Make During Trust Administration

Families commonly stumble at three critical junctures during trust administration, and each mistake cascades into delays, conflict, and unnecessary costs. Understanding where these errors occur positions you to avoid them-and recognizing when professional guidance becomes necessary.

Failing to Notify Beneficiaries Promptly

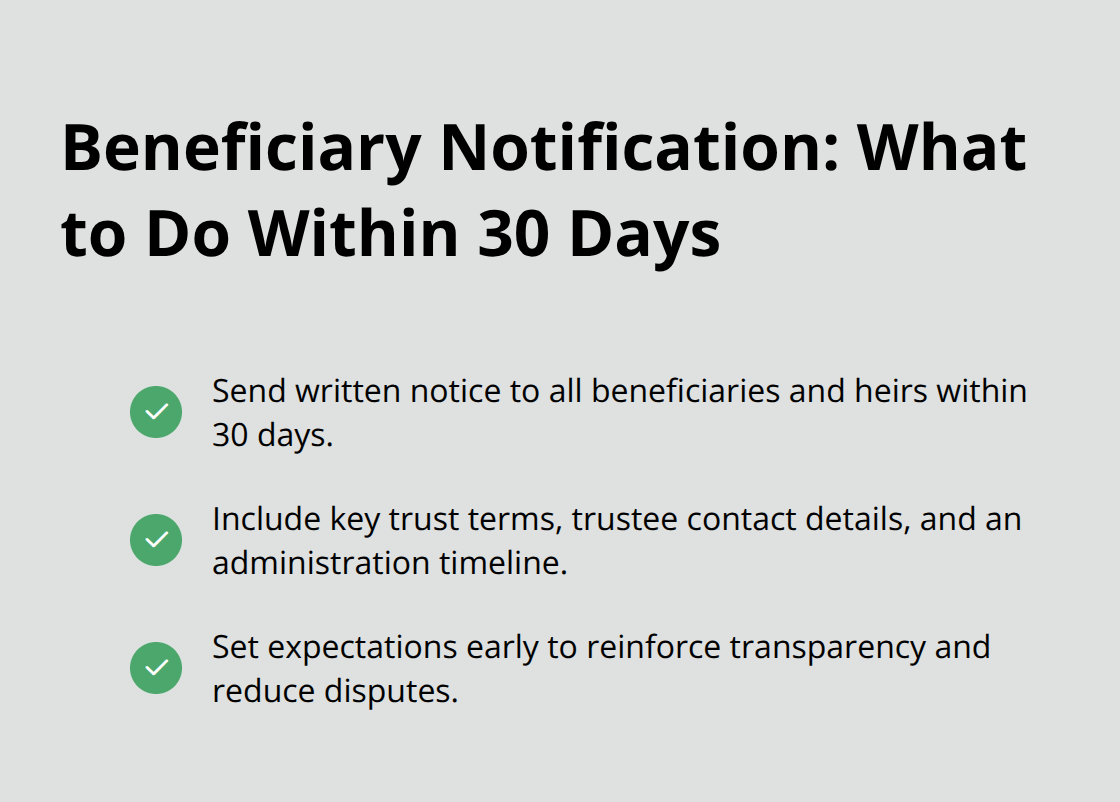

The first mistake is failing to notify beneficiaries within a reasonable timeframe after the settlor’s death. Many trustees assume they can handle everything quietly and inform beneficiaries only when distributions are ready, but state laws and trust documents typically require prompt notification. Indiana law, for example, expects trustees to provide beneficiaries with notice of the trust’s existence and their rights within specific timeframes. When beneficiaries discover months later that administration has been underway without their knowledge, suspicion and resentment follow-even if the trustee acted properly. Beneficiaries may question whether assets were mishandled, whether debts were paid fairly, or whether the trustee took unfair compensation. This notification gap transforms a straightforward administration into a contentious one.

Trustees should send written notice to all named beneficiaries and heirs within 30 days of the settlor’s death. This notice must provide the trust document’s key terms, contact information, and a timeline for administration. Clear communication at the outset prevents misunderstandings and demonstrates the trustee’s commitment to transparency.

Commingling Trust Assets with Personal Property

The second mistake is commingling trust assets with personal property or using trust funds for the trustee’s own expenses without clear documentation. A trustee who deposits trust funds into a personal checking account, pays personal bills from trust money, or borrows from the trust to cover household expenses destroys the legal separation that protects the trust’s integrity. The IRS scrutinizes these transactions during tax audits, and beneficiaries have legitimate grounds to challenge distributions if they suspect misuse.

A dedicated trust bank account with a separate federal tax ID costs minimal money to establish (typically $50 to $150) yet prevents this entire category of problems. Opening this account immediately after receiving the death certificate establishes a clear paper trail for every deposit and withdrawal. This single step protects both the trustee and the beneficiaries by creating an undeniable record of how trust funds were handled.

Missing Tax Deadlines and Filing Requirements

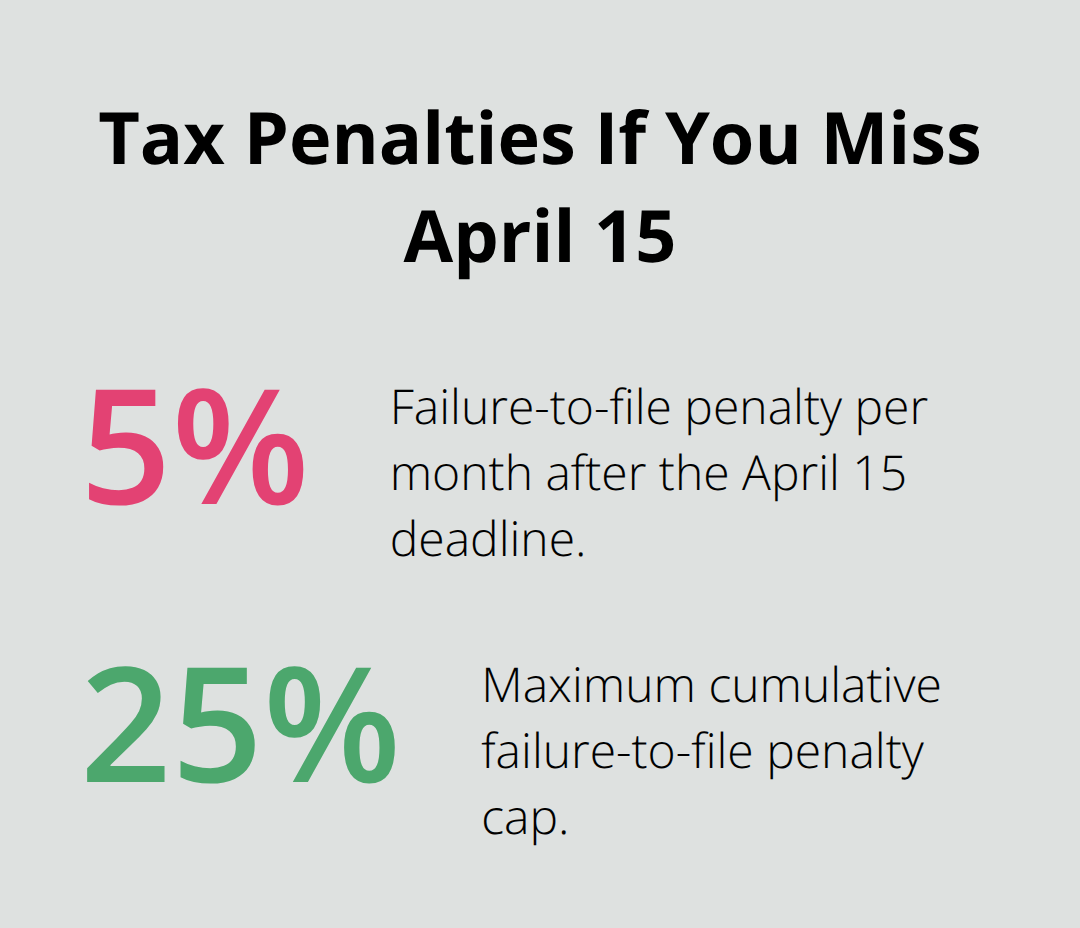

The third mistake is missing tax deadlines, which carry steep penalties and interest charges. The decedent’s final income tax return must file by April 15 following the year of death, and fiduciary income tax returns for the trust itself must file annually while the trust remains open. Many trustees don’t realize that investment income, rental income, and interest earned during administration create tax obligations separate from the decedent’s final return.

Missing the April 15 deadline triggers a failure-to-file penalty of 5 percent per month (up to 25 percent) plus interest accruing daily. A trustee who files three months late on a $50,000 tax bill faces penalties exceeding $7,500 before interest. Working with a CPA familiar with trust administration from the outset prevents these costly mistakes and ensures all filings meet deadlines.

A tax professional helps the trustee understand which income belongs to the decedent’s return versus the trust’s fiduciary return, preventing duplicate reporting or missed deductions.

Building a Foundation for Smooth Administration

These three mistakes are preventable with clear systems and professional guidance. Trustees who establish dedicated accounts, notify beneficiaries early, and engage a CPA before filing the decedent’s final return address the root causes of family disputes and administrative failures. Understanding common pitfalls that extend the process and how to avoid them transforms trust administration from a source of stress into a manageable process-and how we at Law Offices of Roshni T. Desai guide families through each phase.

How We Guide Families Through Trust Administration

Real Estate Complications and Property Transfers

Trust administration becomes significantly less stressful when families have professional guidance from the start, particularly when real estate, multiple beneficiaries, or blended family dynamics complicate the picture. One of the most common complications arises when a trust holds real estate that requires appraisal, transfer, or sale. Many trustees lack experience with property valuation, title transfers, or the paperwork that title companies and lenders demand. When a trust holds a family home worth $800,000 and three adult children are named beneficiaries, the trustee faces difficult decisions: should the home receive appraisal immediately or closer to distribution, who receives the home versus cash, and what happens if one beneficiary wants to keep the property while others need their share distributed?

Ms. Desai’s dual licensure as both an attorney and real estate professional directly addresses this challenge. Rather than hiring separate professionals for legal advice and property transactions, families work with a single point of contact who understands both the trust’s legal requirements and the practical mechanics of real estate transfers. This combination reduces delays caused by miscommunication between attorneys and real estate agents and eliminates the cost of coordinating multiple professionals. A family managing a $1.2 million estate with real estate holdings can expect to save $3,000 to $8,000 in professional fees simply by consolidating legal and real estate guidance under one knowledgeable advisor.

Blended Families and Multiple Trust Structures

Blended families and multiple trusts introduce a second layer of complexity that requires careful navigation. When a parent remarries and creates separate trusts for children from different marriages, or when a family holds assets across multiple trusts created at different times, trustees must track separate accounting requirements, different distribution schedules, and potentially conflicting interests among beneficiaries. A trustee managing a blended family situation where the deceased created one trust for adult children from a first marriage and a separate trust for a surviving spouse faces the immediate question of whether those trusts operate independently or whether assets flow between them.

State law, the trust documents themselves, and the family’s actual intentions may not align, creating confusion about which trustee controls which assets. Communication breakdowns escalate when beneficiaries from different family branches receive conflicting information about timelines or their expected distributions. Professional guidance consolidates these complex situations by coordinating across multiple trust documents, clarifying the legal relationships between them, and ensuring all beneficiaries receive consistent, accurate information about their specific rights. This prevents the scenario where one beneficiary believes distributions will arrive within six months while another learns the process may take two years, creating unnecessary suspicion that the trustee deliberately delays to benefit themselves.

Final Thoughts

Trust administration basics demand precision, documentation, and adherence to legal timelines that leave no room for guesswork. Families who attempt this process alone often discover too late that a missed deadline costs thousands in penalties, that commingling funds creates audit exposure, or that unclear communication with beneficiaries transforms a straightforward administration into years of family conflict. Professional guidance streamlines the entire process by consolidating the knowledge and systems that prevent these costly mistakes.

When a trustee works with an attorney and tax professional from the outset, the administration moves faster because deadlines receive tracking, documents stay organized, and beneficiaries receive clear, consistent communication about timelines and their rights. Real estate complications, blended family dynamics, and multiple trust structures become manageable challenges rather than sources of paralysis when someone with deep experience guides the decisions. We at Law Offices of Roshni T. Desai understand the specific pressures trustees face and offer free consultations with flexible scheduling-whether you prefer to meet at our office or in your home.

If you serve as a trustee or face trust administration decisions, contact Law Offices of Roshni T. Desai to discuss how we can guide your family through this process and take the first step toward confident, compliant trust administration.