Trust Administration Guide: Step‑by‑Step for Your Family

Being named a trustee is a significant responsibility. You’re managing assets, handling taxes, and distributing funds according to someone’s wishes-all while following strict legal requirements.

This trust administration guide walks you through each step of the process. We at Law Offices of Roshni T. Desai help trustees avoid costly mistakes and complete their duties correctly.

What Trust Administration Actually Requires

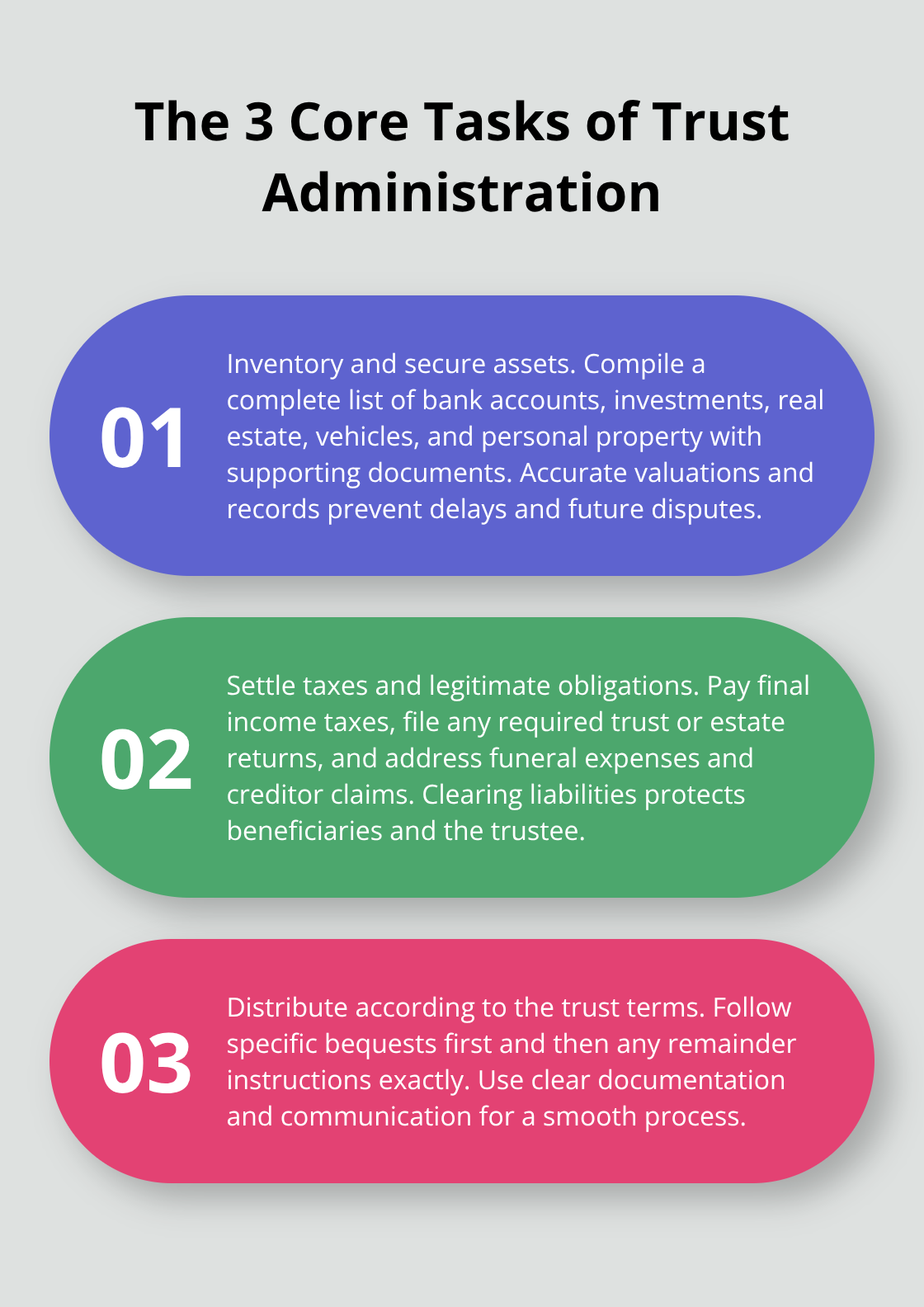

Trust administration means three concrete tasks that most trustees underestimate in scope and complexity. First, you locate and document every asset the trust holds-bank accounts, investment portfolios, real estate, vehicles, and personal property. This inventory phase demands accuracy because incomplete asset identification can delay distributions by months and create liability for the trustee. Second, you settle outstanding obligations before beneficiaries receive anything. This includes paying the decedent’s final income taxes, filing a trust income tax return if the trust generates income during administration, covering funeral expenses, and addressing any debts or claims against the estate. Third, you distribute remaining assets according to the trust document’s specific instructions, whether those are fixed amounts to named beneficiaries or discretionary distributions based on need.

Securing and Valuing Assets First

The inventory phase starts immediately after the decedent’s death. Gather the death certificate and obtain certified copies-you’ll need these to access accounts and notify institutions. Contact banks, investment firms, insurance companies, and the Social Security Administration to identify all accounts and benefits. For real estate and personal property, document current values with appraisals for significant assets like homes or collectibles; rough estimates create tax problems later. Create a detailed spreadsheet listing each asset, its location, account numbers, current value, and supporting documentation. This single document becomes your roadmap for the entire administration process. Many trustees delay this step or treat it casually, which creates confusion about what actually belongs to the trust and what doesn’t.

Managing Liabilities and Tax Obligations

Before distributing a single dollar to beneficiaries, you must identify and pay legitimate claims against the trust. This includes the decedent’s final income tax return, any estate tax returns if the estate exceeds federal thresholds, and the trust’s own income tax return for the administration period. You’ll also pay reasonable funeral expenses, outstanding debts, and valid creditor claims. Keep detailed receipts and records of every payment. The trustee’s biggest liability exposure comes from distributing assets without fully settling tax obligations-the IRS can pursue beneficiaries for unpaid estate taxes, and you personally bear responsibility for missing deadlines. California law gives creditors a specific window to file claims, typically four months from the decedent’s death, so you must notify known creditors and publish notice to unknown creditors in local newspapers. This sounds bureaucratic, but missing these steps means personal liability for unpaid taxes or creditor claims.

Distributing Assets According to the Trust Terms

Once liabilities are settled and taxes are paid, you distribute remaining assets exactly as the trust document specifies. Some trusts require specific bequests first-for example, a piece of jewelry to one beneficiary, a vehicle to another-before dividing the remainder. Others direct immediate equal distribution to all beneficiaries. Read the trust language carefully; if terms are ambiguous, consult an attorney before distributing. For complex estates with illiquid assets like real property or business interests, you may need to arrange an estate sale to convert assets to cash for fair distribution among beneficiaries. Throughout this process, maintain transparent communication with beneficiaries about timing, asset values, and distributions.

Why Mistakes Happen During These Steps

Trustees often underestimate how long asset identification takes or skip the formal appraisal process to save money, only to face IRS challenges later. Others rush distributions without confirming all tax obligations are settled, exposing themselves to personal liability. The complexity multiplies when trusts hold multiple property types, when beneficiaries live in different states, or when family dynamics create pressure to distribute quickly. These pressures and oversights lead directly into the common mistakes that derail trust administration-mistakes that create delays, disputes, and unnecessary costs for everyone involved.

Where Trustees Go Wrong

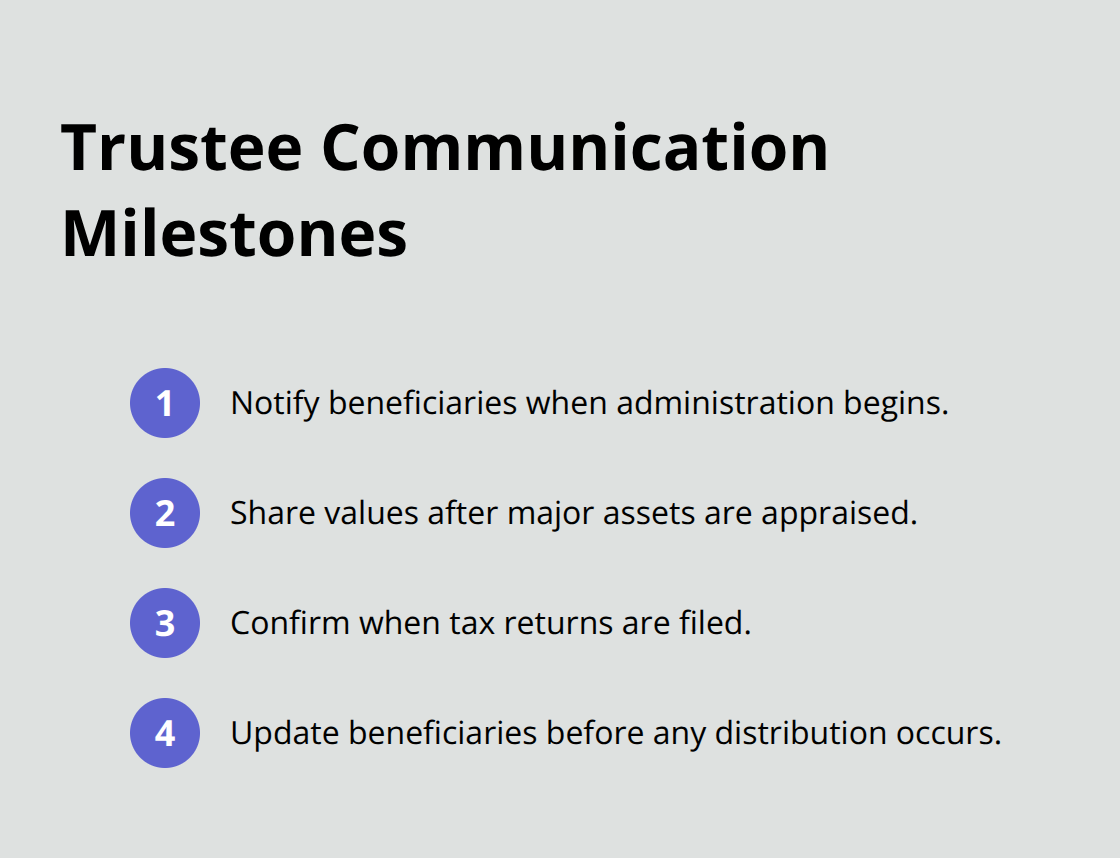

Trustees fail in three distinct ways, and most failures stem from avoidable decisions rather than impossible circumstances. The first failure is silence. Beneficiaries sit in the dark about what’s happening, when distributions will arrive, or why certain decisions were made. This creates suspicion, resentment, and often legal disputes that cost thousands in attorney fees. Beneficiaries need regular updates at key milestones: when the trustee begins administration, when major assets are valued, when tax returns are filed, and before any distribution occurs. A simple email explaining asset values and expected distribution timing prevents most conflicts.

Silence Creates Conflict

Communication gaps damage trust relationships faster than almost any other mistake. Beneficiaries who receive no updates assume the worst-that the trustee is hiding something, moving slowly on purpose, or taking money for themselves. These assumptions fuel resentment and legal action. A trustee who sends one email at the start of administration and another before distributions arrive eliminates most of this friction. The message doesn’t need to be lengthy; it needs to be honest and timely.

Mixing Trust Money with Personal Funds

The second failure is treating trust funds like personal money. Trustees mix trust assets with personal accounts, fail to document distributions clearly, or delay paying legitimate expenses because cash flow feels tight. The IRS scrutinizes these practices, and beneficiaries can sue if they discover mismanagement. Every trust transaction must be recorded separately, tracked in a dedicated accounting system, and supported by receipts. A trustee who opens a separate trust bank account and deposits all trust funds there immediately eliminates this risk entirely.

Missing Tax Deadlines

The third failure is missing tax deadlines. Trust income tax returns are due nine months after the decedent’s death in California. Estate tax returns, if required, have their own deadlines. Missing these dates triggers penalties, interest charges, and potential personal liability for the trustee. Many trustees don’t realize they’re personally responsible if the trust lacks sufficient funds to cover taxes-the IRS can pursue them directly. This liability exposure is real and substantial.

How Mistakes Compound

These mistakes compound quickly. A trustee who delays communication often also delays tax filings because they haven’t organized financial records. A trustee who mismanages assets typically hasn’t created proper documentation, making tax compliance nearly impossible. One error creates conditions for the next error, and soon the trustee faces multiple problems simultaneously. The solution is establishing systems from day one: create a communication schedule, open a dedicated trust bank account, hire an accountant or attorney to handle tax filings, and document every decision in writing.

The administrative work that creates most liability exposure is exactly where professional guidance makes the largest difference. Trustees who establish proper systems from the beginning avoid the cascading failures that turn a manageable task into a legal nightmare. Understanding these pitfalls is the first step-implementing safeguards is what separates smooth administrations from troubled ones.

How We at Law Offices of Roshni T. Desai Help Trustees Navigate Trust Administration

The mistakes outlined in the previous section-missed communication, mismanaged funds, and tax deadline failures-share a common root: trustees attempt administration alone without understanding California law’s specific requirements or the complex accounting and tax rules that govern the process. We at Law Offices of Roshni T. Desai work directly with trustees to prevent these failures from the start. Our approach centers on three practical interventions that address the exact pain points trustees face.

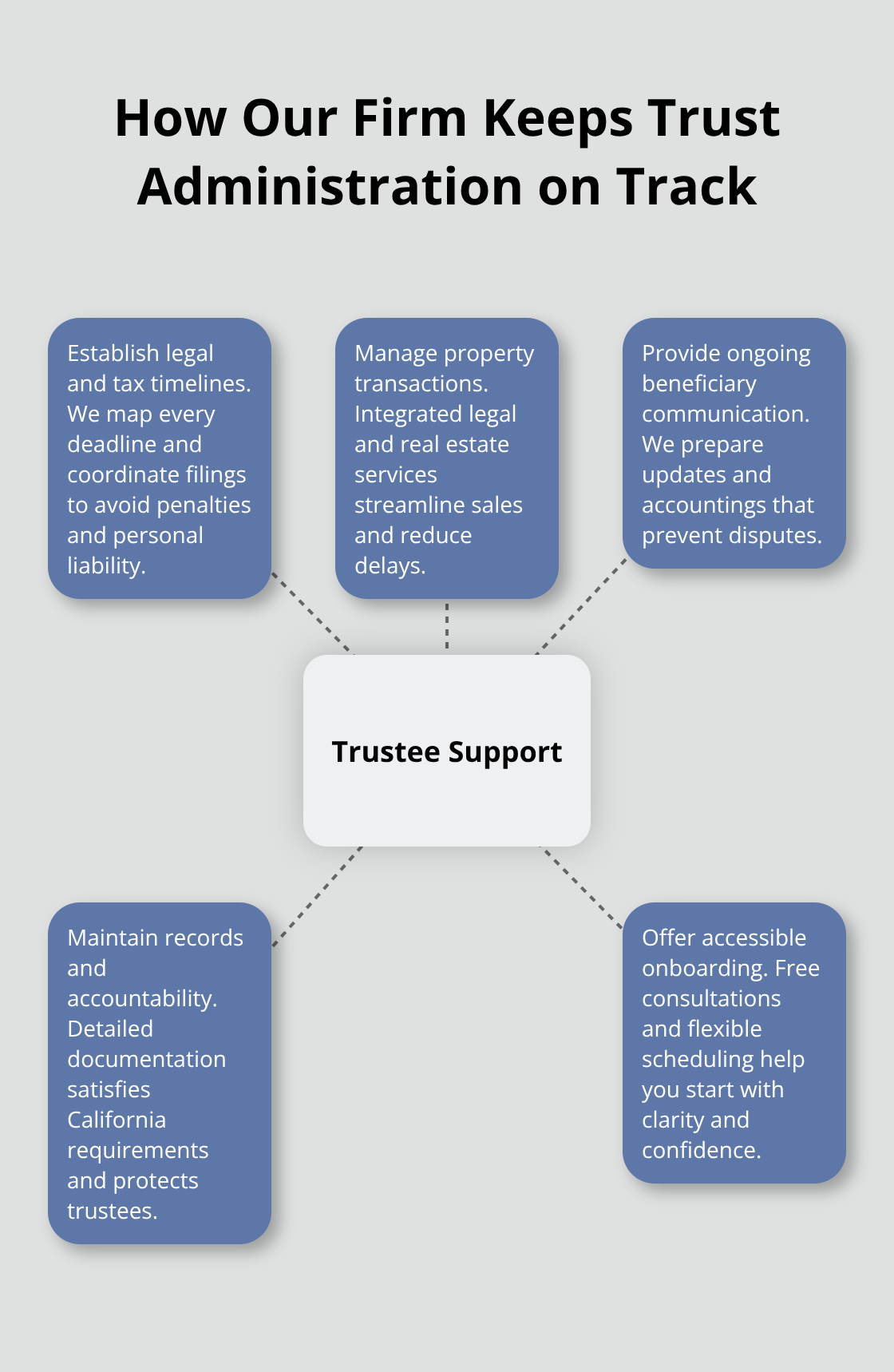

Establishing Legal and Tax Timelines

We create a legal and tax timeline specific to your trust, identifying every deadline that matters and establishing a system to meet them. The trust income tax return deadline in California is nine months after death-a single date that determines whether you face penalties and personal liability. We coordinate with accountants to ensure filings happen on time, every time. This structured approach transforms what feels like an overwhelming administrative burden into a manageable sequence of concrete steps.

Managing Property Transactions and Sales

Many trusts hold real estate or business interests that require professional management to sell fairly and efficiently. Our dual licensure as both attorneys and real estate professionals means we manage these transactions without the communication gaps and cost overruns that typically occur when trustees hire separate agents and lawyers. This integrated approach streamlines the process and reduces unnecessary complexity. Property sales that would otherwise consume months of a trustee’s time move forward with clear coordination between legal and real estate functions.

Providing Ongoing Administration Support

We provide ongoing administration support that keeps beneficiaries informed and protected throughout the process. We draft the initial communication to beneficiaries explaining the timeline and their rights, prepare detailed accountings of assets and distributions, and answer beneficiary questions that would otherwise create disputes. This proactive communication prevents the resentment and legal conflicts that emerge when beneficiaries sit in silence wondering what’s happening with their inheritance.

Maintaining Records and Accountability

The core service we provide is accountability and organization-two things trustees cannot easily create alone. We maintain detailed records of every asset, every payment, every distribution, and every decision, which protects you from future challenges and satisfies California’s strict accounting requirements. We also provide the knowledge needed to interpret ambiguous trust language before distributions happen, preventing costly mistakes that cannot be undone. If the trust directs discretionary distributions based on beneficiary need, we help you establish clear, defensible standards for those decisions and document your reasoning. If the trust holds multiple property types across different states, we coordinate the valuations, tax treatments, and distribution logistics that most trustees find overwhelming.

Getting Started with Professional Support

We offer free consultations that allow you to discuss your specific trust situation before committing to full administration support, and we offer flexible scheduling with home or office visits to accommodate your circumstances. The trustees who navigate trust administration most successfully are those who recognize early that trust administration is not a task you complete in your spare time-it requires systems, deadlines, professional coordination, and legal knowledge that most people lack.

Final Thoughts

Trust administration demands three core responsibilities that determine whether your family’s inheritance reaches beneficiaries smoothly or becomes entangled in delays and disputes. You must identify and value every asset the trust holds, settle all outstanding debts and tax obligations before distributions occur, and then distribute remaining funds exactly as the trust document specifies. Professional support transforms this trust administration guide into actionable steps that prevent the three mistakes derailing most administrations: failing to communicate with beneficiaries, mismanaging trust funds, and missing tax deadlines.

We at Law Offices of Roshni T. Desai have spent over 25 years helping trustees navigate this process with personalized guidance tailored to each family’s situation. Our dual licensure as both an attorney and real estate professional means we handle property transactions and sales without the coordination gaps that typically slow administrations. We establish communication systems that keep beneficiaries informed, maintain detailed accounting records that satisfy California’s strict requirements, and coordinate with accountants to meet every tax deadline.

If you’re managing a trust right now or have recently been named trustee, contact us for a free consultation. We offer flexible scheduling with home or office visits to fit your circumstances, and we can discuss your specific situation and show you how professional support protects your family and simplifies the administration process.