Trust Administration in Orange County, California: A Practical Guide for Owners

Trust administration in California involves managing assets, filing taxes, and communicating with beneficiaries-tasks that demand precision and knowledge of state law.

Many trust administrators in Orange County face confusion about their responsibilities and the legal requirements they must follow. We at Law Offices of Roshni T. Desai help administrators navigate this process smoothly, handling the paperwork and complexity so you can focus on what matters.

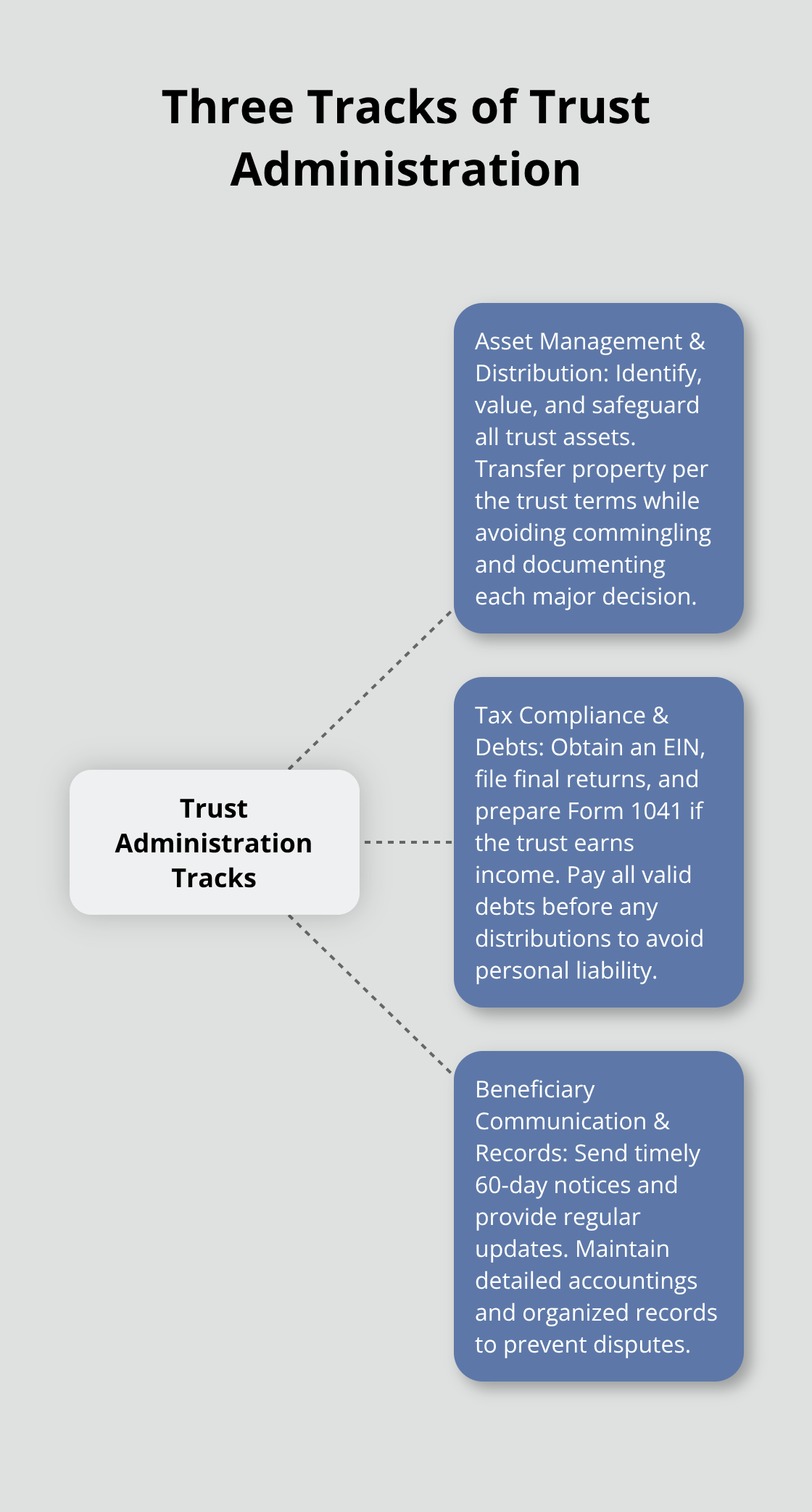

What Happens During Trust Administration

Trust administration starts the moment a trustee takes office and involves three simultaneous tracks that run throughout the entire process. The first track is asset management and distribution, which requires you to identify every asset the trust owns, value it accurately, and eventually transfer it to beneficiaries according to the trust document’s terms.

Managing Trust Assets in Orange County

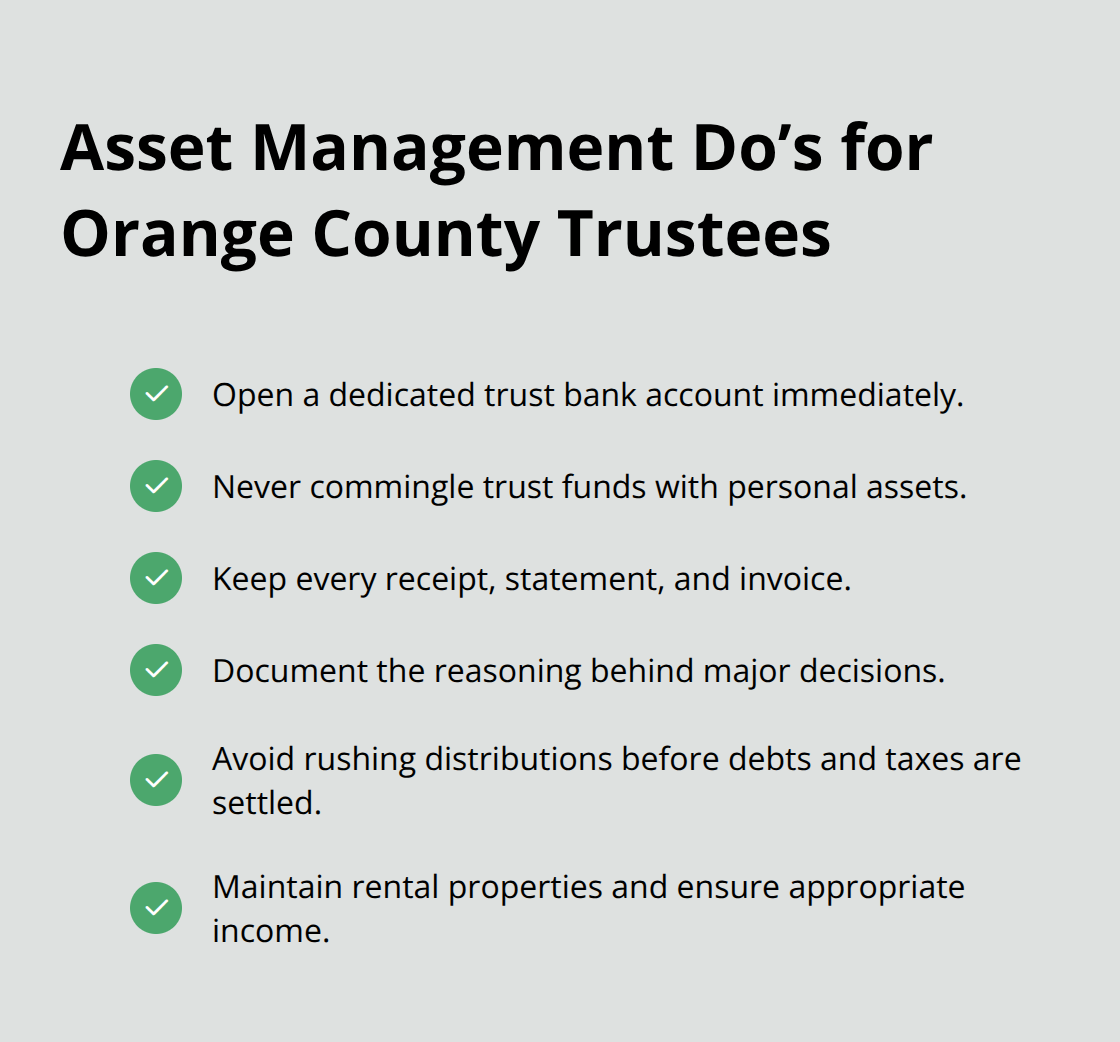

In Orange County, trust-held real property represents a significant portion of many estates, so you’ll need to decide whether to sell properties, retain them for beneficiaries, or transfer title directly. The California Probate Code requires trustees to act as a reasonably prudent investor, meaning you must manage investments with care and adjust strategies as market conditions shift. If the trust owns rental properties, you’re responsible for maintenance, tenant communications, and ensuring properties generate income appropriately.

Many administrators treat trust assets like personal funds, mixing them into personal bank accounts or making investment decisions without documentation. This creates liability and invites disputes. Instead, open a dedicated trust bank account immediately, keep every receipt and statement, and document the reasoning behind major decisions. Asset distribution typically takes 6 to 12 months in Orange County depending on complexity, but rushing distributions before settling all debts and taxes exposes you to personal liability.

Filing Taxes and Managing Obligations

The second track involves tax compliance and debt settlement, which many trustees underestimate in scope. You must obtain a federal Employer Identification Number for the trust, file final income tax returns for the deceased, and potentially file annual trust income tax returns on Form 1041 if the trust generates income during administration. California also imposes specific requirements like monitoring Proposition 19 property tax reassessment exclusions if the trust transfers real estate to beneficiaries.

Before you distribute a single dollar to beneficiaries, you must identify and pay all valid debts, file final tax returns, and settle any estate taxes owed. The California Probate Code gives creditors a limited window to file claims, and if you distribute assets before that window closes, you risk personal liability. Work with a CPA familiar with California trust taxation to avoid costly mistakes.

Communicating with Beneficiaries and Maintaining Records

The third track is beneficiary communication and record-keeping, which prevents disputes and protects you legally. California law requires you to notify beneficiaries within 60 days of your appointment, and that notification must be written and notarized. Maintain regular contact with beneficiaries about progress, major decisions, and timelines. Provide detailed accountings showing all transactions, investments, and distributions.

Keep both digital and physical copies of the original trust agreement, property deeds, bank statements, and all correspondence. Courts have consistently found that thorough documentation and transparent communication eliminate most disputes before they escalate to litigation. These three tracks-asset management, tax compliance, and beneficiary communication-operate simultaneously, and managing them effectively requires attention to detail and knowledge of California law. The challenges that arise during this process often stem from gaps in one or more of these areas, which is why understanding what obstacles you may face helps you prepare and respond appropriately.

Common Challenges Trust Administrators Face in Orange County

Trust administrators in Orange County encounter three recurring obstacles that derail timelines and create legal exposure if mishandled. Understanding these challenges helps you prepare and respond appropriately before problems escalate.

Navigating California Probate Code Requirements

The California Probate Code imposes strict fiduciary duties under sections 16000-16015, including loyalty to beneficiaries, impartiality between competing interests, and detailed record-keeping obligations. Many administrators operate informally, treating trust duties like personal money management, and this approach backfires when beneficiaries question decisions or when tax authorities examine trust records.

If you fail to maintain a separate trust bank account or commingle trust funds with personal assets, you create the appearance of self-dealing even if your intentions were sound. The California Probate Code requires you to account for every dollar-showing where money came from, how it was invested, and where it went. Trustees who lack organized systems often cannot produce these accountings when demanded, triggering beneficiary suspicion and potential litigation.

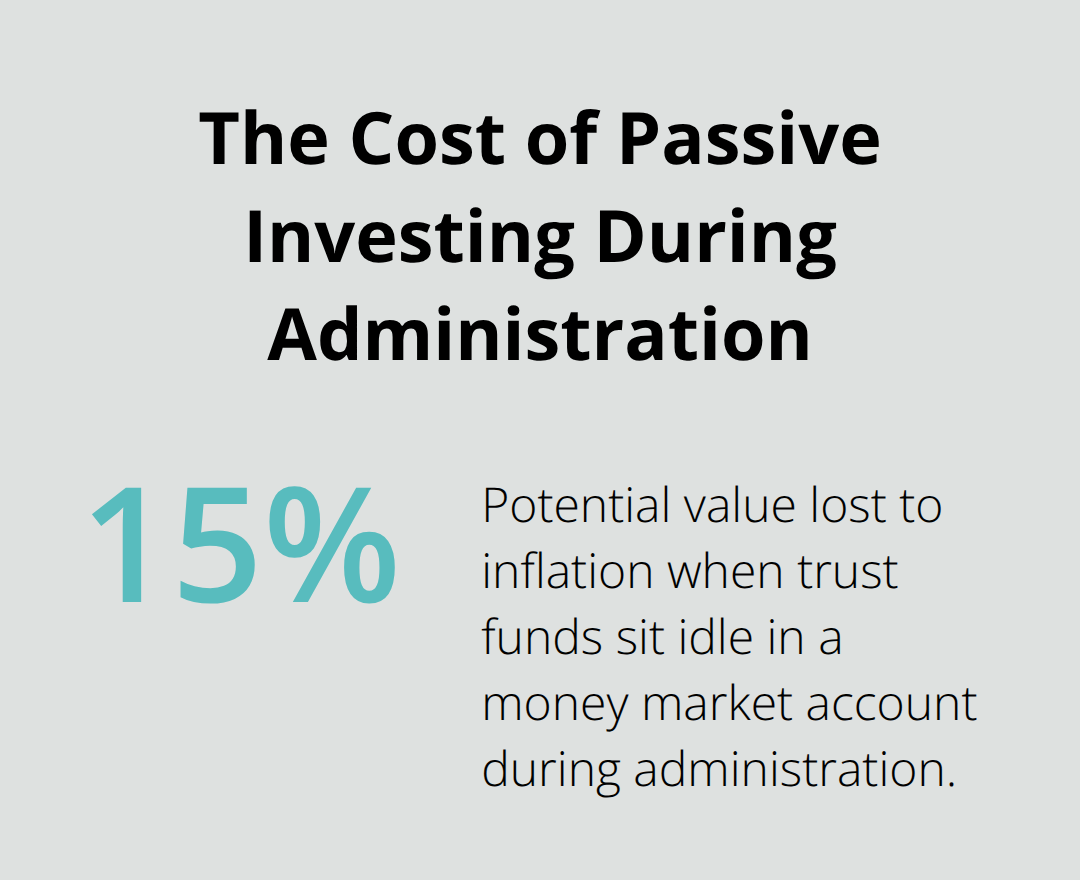

The Code also mandates that you act as a reasonably prudent investor, which means passive or outdated investment strategies expose you to liability claims that you failed to preserve trust value. Many administrators freeze trust investments during administration, assuming safety, when California law actually requires active management. A trust losing 15% to inflation while sitting in a money market account represents a breach of fiduciary duty, even though no active misconduct occurred.

Managing Beneficiary Disputes and Communication Gaps

Beneficiary conflict represents the most destructive obstacle that Orange County trust administrators face. Disputes between siblings, between surviving spouses and adult children, or between beneficiaries and trustees consume time, deplete trust assets through legal fees, and transform straightforward administrations into contested litigation lasting years.

Research on trust disputes shows that poor communication and perceived inequity drive most conflicts, not actual mismanagement. A trustee who distributes $500,000 to one sibling and $400,000 to another without explaining the reasoning invites accusations of favoritism, even if the trust document explicitly authorizes the difference. Transparency prevents most disputes, but many administrators avoid detailed communication fearing it will prompt questions. This silence backfires and creates the very disputes they hoped to avoid.

Handling Real Property and Complex Assets

Real property and complex assets represent substantial portions of Orange County estates given regional real estate values. A trustee holding rental properties must decide whether to sell, retain, or transfer them to beneficiaries-decisions that carry tax consequences, market timing risks, and ongoing management obligations.

If a property is underwater or generates negative cash flow, the trustee faces pressure from beneficiaries to sell immediately, yet selling at a loss may violate the fiduciary duty to preserve value. Capital gains taxes complicate matters further; transferring appreciated real estate to beneficiaries triggers capital gains liability that reduces distributions. Many administrators lack the financial knowledge to evaluate these tradeoffs and end up making reactive decisions rather than strategic ones.

Managing complex assets like closely held business interests, investment portfolios, or intellectual property requires specialized knowledge that most individual trustees do not possess. Poor decisions about these assets create subsequent liability claims and expose you to personal financial responsibility. These three obstacles-regulatory compliance, beneficiary relations, and asset complexity-often intersect, which is why many administrators benefit from professional guidance to navigate them effectively. We at Law Offices of Roshni T. Desai help trustees address these challenges head-on, providing the support and knowledge needed to move administration forward with confidence.

How Law Offices of Roshni T. Desai Supports Your Administration

Trust administration demands simultaneous attention to asset management, tax compliance, beneficiary relations, and regulatory requirements-a combination that overwhelms most individual trustees. We at Law Offices of Roshni T. Desai handle the legal complexity and paperwork so you avoid the costly mistakes that derail administrations and trigger litigation. Our approach focuses on three concrete areas where trustees struggle most.

Navigating California Probate Code Compliance

We guide you through California Probate Code compliance by preparing all required notices, accountings, and tax documentation in the correct format and timeline. California requires notifying beneficiaries within 60 days of your appointment using specific language and notarization standards; missing this deadline or using improper notice language invites challenges to your authority. We prepare these notices correctly the first time, eliminating delays and disputes.

The Probate Code also mandates detailed record-keeping and fiduciary accountability. We help you maintain organized systems that document every transaction, investment decision, and distribution. This documentation protects you from liability claims and demonstrates to beneficiaries that you acted within your authority and in their best interests.

Managing Tax Filings and Administrative Tasks

We handle the administrative burden that consumes months of your time. This includes obtaining the federal EIN for the trust, coordinating with the deceased’s final income tax filing, monitoring Proposition 19 property tax reassessment exclusions if real estate transfers to beneficiaries, and preparing Form 1041 trust income tax returns if the trust generates income during administration. We work directly with CPAs to align tax filings with trust distributions and beneficiary circumstances, reducing audit and penalty risk.

Real property transfers receive particular attention. We record the Affidavit of Death of Trustee, ensure title transfers correctly to beneficiaries or successor trustees, and address capital gains basis issues that affect tax liability. Our dual licensure as both attorney and real estate professional streamlines property sales and transactions, reducing costs, delays, and communication problems that typically arise when multiple professionals handle the same property.

Resolving Conflicts and Protecting Your Interests

We resolve conflicts before they escalate to litigation. When beneficiaries question distributions or dispute your decisions, we serve as a professional buffer, documenting the trust terms and the reasoning behind each decision in writing. Transparent communication reduces the emotional friction that drives disputes; our communications and detailed accountings demonstrate that you acted within your authority and in beneficiaries’ best interests.

We offer free consultations with flexible home or office visits, so you can discuss your specific administration challenges without commitment. Most administrations take 6 to 12 months, aligned with Orange County’s typical timeline, because proactive planning and professional coordination prevent the delays that extend administration indefinitely.

Final Thoughts

Trust administration in California demands precision across asset management, tax compliance, beneficiary communication, and regulatory obligations. Mistakes in any of these areas create cascading problems that extend timelines, deplete trust assets through legal fees, and transform straightforward administrations into contested litigation. The administrators who navigate this process successfully recognize when professional guidance prevents costly errors rather than adding expense.

The three obstacles outlined above-navigating California Probate Code requirements, managing beneficiary disputes, and handling complex assets-rarely appear in isolation. A trustee struggling with real property decisions while facing beneficiary questions about distributions needs coordinated support across legal, tax, and communication fronts. Individual effort applied piecemeal creates gaps that beneficiaries exploit, regulators scrutinize, and courts eventually address through litigation. Professional support reduces stress by removing the administrative burden that consumes months of your time and protects you from personal liability by ensuring every decision meets California requirements.

We at Law Offices of Roshni T. Desai provide personalized support tailored to your specific trust administration California challenges. Contact us to schedule your free consultation and move your administration forward with confidence.