Trust Administration Overview: From Setup To Settlement

Administering a trust involves managing assets, communicating with beneficiaries, and handling tax requirements from start to finish. The process can feel overwhelming without clear guidance on what each step entails.

We at Law Offices of Roshni T. Desai created this trust administration overview to walk you through the entire journey. You’ll learn what trustees actually do, what challenges arise, and how to move confidently toward final settlement.

What Trustees Actually Do From Day One

Trust administration starts the moment the grantor passes away or becomes incapacitated. Your first job is not strategic planning-it’s immediate triage. Within days, you need to locate the trust document, gather 8 to 12 certified death certificates from the county vital records office, and notify the Social Security Administration of the death. This prevents overpayments and keeps benefit checks from bouncing. Next, secure all physical assets, change locks if needed, and contact banks and financial institutions to freeze accounts until you can prove your authority as successor trustee.

Establish Your Legal Authority and Tax Identity

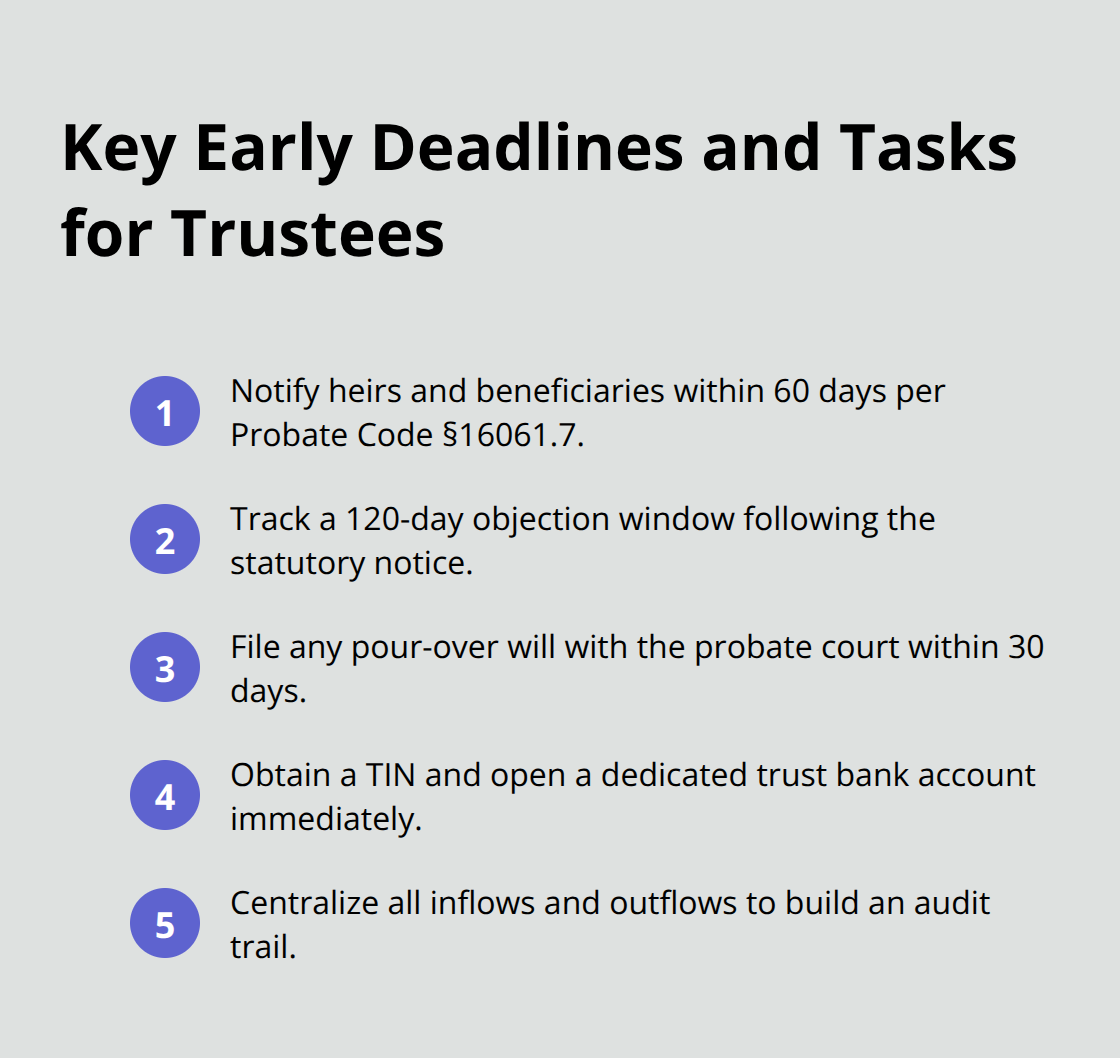

The IRS requires you to obtain a Taxpayer Identification Number for the trust itself, which you’ll use to open a dedicated trust bank account. This account becomes your central hub-all incoming funds and outgoing payments flow through it, creating an auditable trail that protects you from liability claims later. California Probate Code Section 16061.7 requires you to notify all legal heirs and beneficiaries within 60 days of the grantor’s death, providing them a copy of the trust document. This notice starts a 120-day window during which beneficiaries can object to your actions, so transparency from the start prevents disputes from festering. Many trustees skip this step thinking it saves time; it actually multiplies problems.

You must also file a pour-over will with the probate court within 30 days if one exists, even though it doesn’t avoid probate on its own-it captures any assets accidentally left outside the trust and directs them into it for proper distribution.

Create a Complete Asset Inventory and Valuation

Your second responsibility is inventory and valuation. You need to create a comprehensive list of every asset: real property, bank accounts, investment portfolios, life insurance policies, retirement accounts, vehicles, and personal property of value. For real estate, order a date-of-death appraisal immediately; this locks in the tax basis and can dramatically reduce capital gains taxes for beneficiaries. For community property in California, the death of one spouse can trigger a full step-up in basis for the surviving spouse, but only if you document it properly with qualified appraisals.

Set Up Your Accounting System and Pay Initial Obligations

You should open a trust accounting system-even a simple spreadsheet works for straightforward trusts, though accounting software like Quicken reduces errors if administration stretches beyond a few months. Track every receipt, invoice, and distribution. This documentation protects you if beneficiaries later challenge your decisions. Pay funeral and burial expenses first, then outstanding debts and taxes as they come due. If the grantor had an executor named in a separate will, stay in close contact to coordinate; the executor handles probate assets while you handle trust assets, and sometimes they overlap.

Transfer Real Property Into Your Name as Trustee

For real property held in the trust, file an Affidavit Change of Trustee with the county recorder to transfer title into your name as trustee. This step is critical if you plan to sell, refinance, or rent the property. Skipping it blocks these transactions entirely. Serving as a trustee comes with real responsibilities and tight deadlines, and missing even one procedural step can create legal problems. Once you complete this transfer and establish your accounting foundation, you’ll face the ongoing challenge of managing diverse assets while keeping beneficiaries informed-a balance that separates smooth administrations from contentious ones.

Where Trust Administration Runs Into Real Problems

Managing a trust’s assets while keeping beneficiaries informed and handling taxes creates friction points that catch most trustees off guard. The problem isn’t one single task-it’s juggling three competing demands at once. You preserve and grow assets, answer questions from people who have money at stake, and file paperwork that the IRS actually reads. Miss deadlines on any of these and your liability exposure grows fast.

Real Property Transfers and Valuation Challenges

Real property inside the trust complicates everything. If you need to sell a house or refinance a loan, title transfers take weeks, and if the property sits in a community property state, valuation errors cost beneficiaries thousands in unnecessary taxes. You must file an Affidavit Change of Trustee with the county recorder to transfer title into your name as trustee before any sale or refinance can proceed. This step blocks transactions entirely if you skip it. Obtain a date-of-death appraisal immediately to lock in the tax basis and reduce capital gains taxes for beneficiaries.

Investment Management and the Prudent Investor Standard

Investment accounts need active monitoring too. The prudent investor standard-a legal requirement in California-means you cannot leave money sitting in a savings account earning nothing. You must balance growth against risk in a way that makes sense for the beneficiaries’ timeline and needs. This requires either working with a financial advisor or educating yourself on asset allocation, which most trustees lack time for alongside everything else.

Tax Filings and Beneficiary Communication

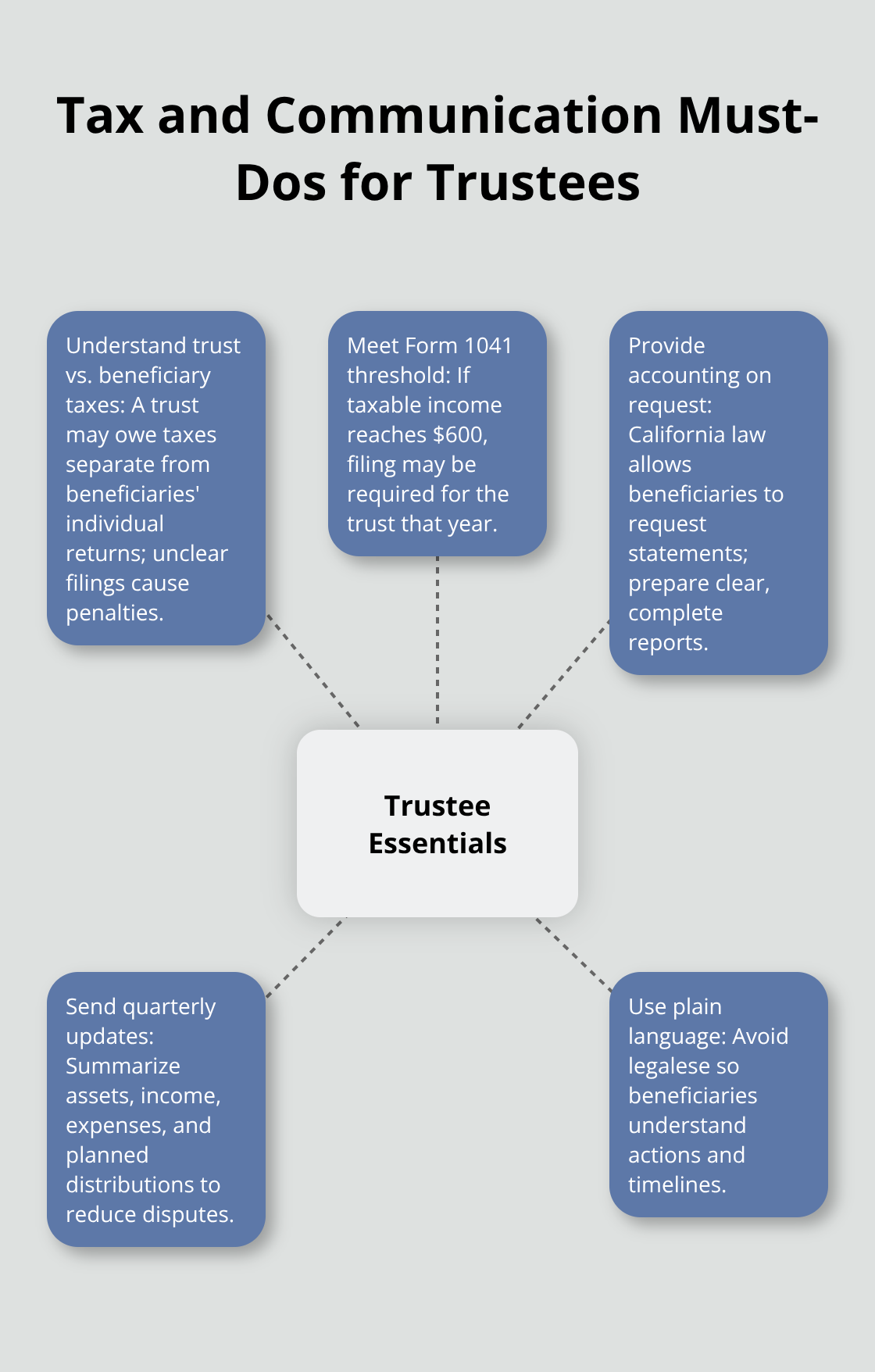

The IRS Form 1041 filing threshold sits at $600 of taxable income annually, but many trustees misunderstand that the trust itself may owe taxes separate from what beneficiaries owe individually. This confusion leads to incomplete filings and penalties.

California Probate Code requires you to provide accounting statements if beneficiaries request them, and many do-especially when they suspect you’re mismanaging funds or favoring one heir over another. Open communication prevents most disputes before they start. Send quarterly updates showing what assets you hold, what income came in, what expenses you paid, and when distributions will happen. Use plain language, not legalese.

Managing Conflict Before It Escalates

Beneficiary disputes destroy more trusts than bad investments ever will. When conflict emerges, mediation costs far less than litigation and preserves family relationships. For complex trusts with multiple properties, significant investments, or blended families, the coordination demands between estate taxes, income taxes, and property taxes demand professional guidance. The cost of early legal consultation almost always beats the cost of fixing problems after they spiral. These asset management and communication challenges set the stage for the final phase of trust administration-preparing your accounting, resolving outstanding obligations, and distributing what remains to beneficiaries.

Closing the Trust After All Debts and Assets Are Settled

Trust settlement demands precision because mistakes at the finish line create liability that follows you long after distributions end. Your final accounting is not optional paperwork-it’s your legal shield against future beneficiary claims.

Compile Complete Documentation Before Any Distribution

Before you distribute a single dollar, you must compile a complete record showing every asset the trust held, every dollar that came in, every expense paid, and how much remains for distribution. California Probate Code requires that beneficiaries can request a formal accounting, and if you cannot produce one, courts assume you mishandled funds. Start this documentation now, not at the end. Use a spreadsheet or accounting software to track date-of-death values, income received, expenses paid, and asset transfers. When you’re ready to distribute, calculate what each beneficiary receives based on the trust terms-some get fixed amounts, others get percentages, and some receive distributions only under specific conditions like reaching a certain age. Obtain written consent from beneficiaries before making any distribution if the trust allows it; this consent becomes proof you followed instructions correctly and prevents later disputes about whether they received what the grantor intended.

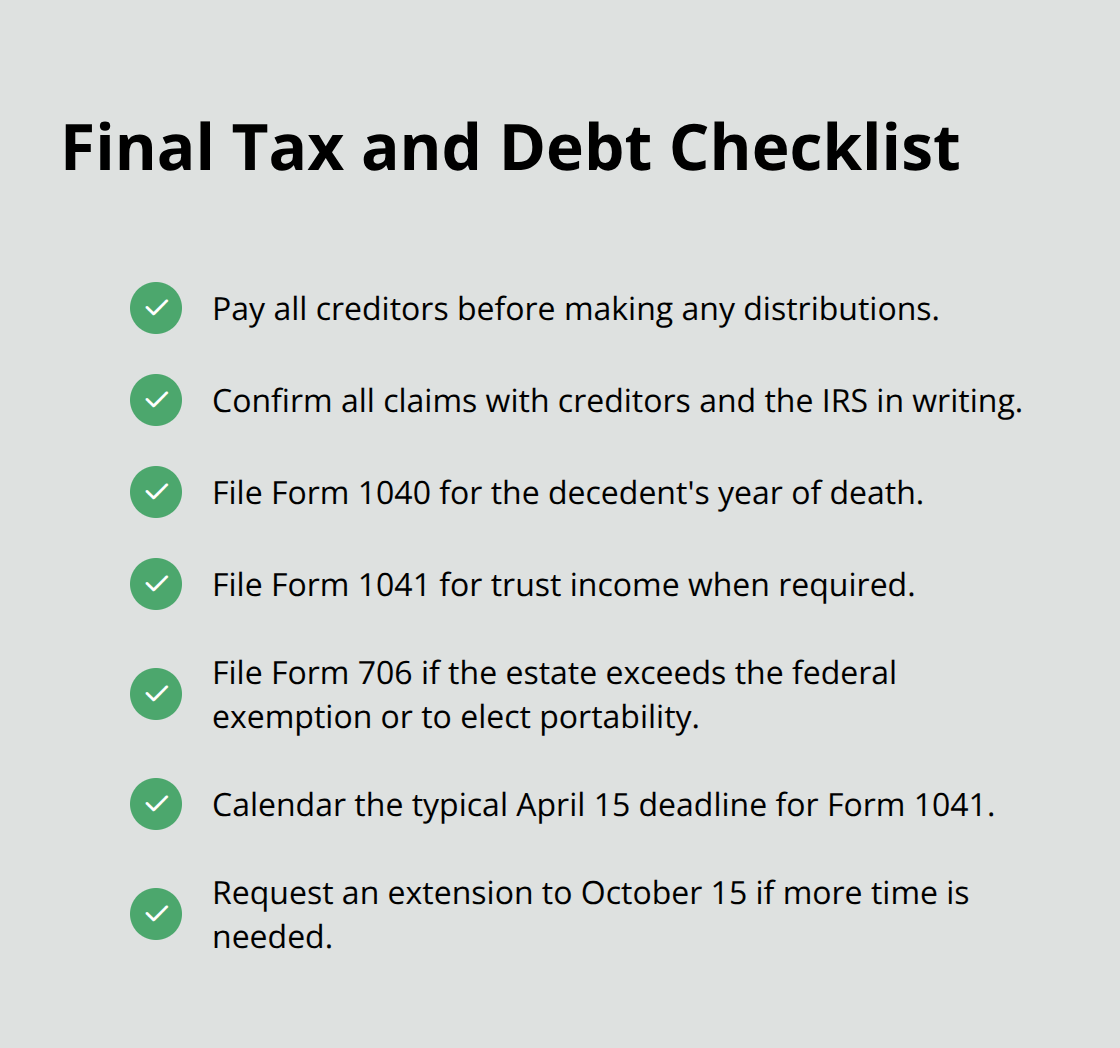

Settle All Debts and File Final Tax Returns

Resolve debts before distributions, not after. Contact creditors and the IRS to identify all outstanding claims against the estate, then settle them from trust assets. File final tax returns: Form 1040 for the year of death, Form 1041 for trust income, and Form 706 if the estate exceeds the federal exemption threshold to elect portability and allocate generation-skipping transfer tax. The IRS filing deadline for Form 1041 is typically April 15 of the following year, but you can request an extension to October 15 if needed.

Issue Final Statements and Execute Distributions

Once debts and taxes are paid and you’ve documented everything, issue a final statement to each beneficiary showing the date-of-death asset values, income earned, expenses paid, and the exact amount and timing of their distribution. Some beneficiaries receive distributions outright in a lump sum, while others receive staggered payments over months or years, and still others receive ongoing distributions from a subtrust if the grantor wanted to protect them from themselves or creditors.

Formally Terminate the Trust

After you distribute the final dollar and close all trust accounts, file a trust termination notice with the IRS using Form 1041 marked as final, then notify beneficiaries that the trust has ceased to exist. This closure protects you from future liability because your fiduciary duty ends once all assets are distributed and accounts are settled.

Address Conflicts Through Mediation

If conflicts emerge during settlement-a beneficiary claims you favored another heir or questions your valuations-mediation resolves most disputes faster and cheaper than litigation, preserving what remains of family relationships while protecting your reputation as trustee.

Final Thoughts

Trust administration from setup to settlement demands attention to detail, timely action, and honest communication with beneficiaries. The tasks you face-securing assets, filing tax returns, managing investments, and distributing property-are not optional, and missing deadlines or skipping procedural steps creates liability that can follow you for years. Success depends on establishing clear authority early, maintaining meticulous records throughout, and resolving all debts before distributions.

Real property transfers, investment management, tax filings, and beneficiary disputes are predictable challenges that most trustees encounter. The ones who navigate these smoothly document everything, communicate openly, and seek help when complexity exceeds their knowledge. Professional guidance matters most when real estate is involved, when the trust holds significant investments, or when beneficiaries show signs of conflict-an attorney can review your accounting, verify tax filings are complete and correct, and mediate disputes before they escalate to litigation.

We at Law Offices of Roshni T. Desai provide personalized estate planning and probate services across Southern California, including trust and probate administration. Contact us for a free consultation with flexible home or office visits to discuss your specific situation and receive guidance tailored to your trust administration overview and needs.