Why an Experienced Trust Administration Attorney Matters for Your Santa Ana, California Estate

Trust administration requires careful attention to detail and knowledge of California law. Many families in Santa Ana face costly mistakes when managing trusts without proper guidance.

At Law Offices of Roshni T. Desai, we help families navigate trust administration with clarity and confidence. An experienced trust administration attorney can protect your assets, satisfy tax requirements, and prevent disputes that drain your estate.

What Trust Administration Actually Requires

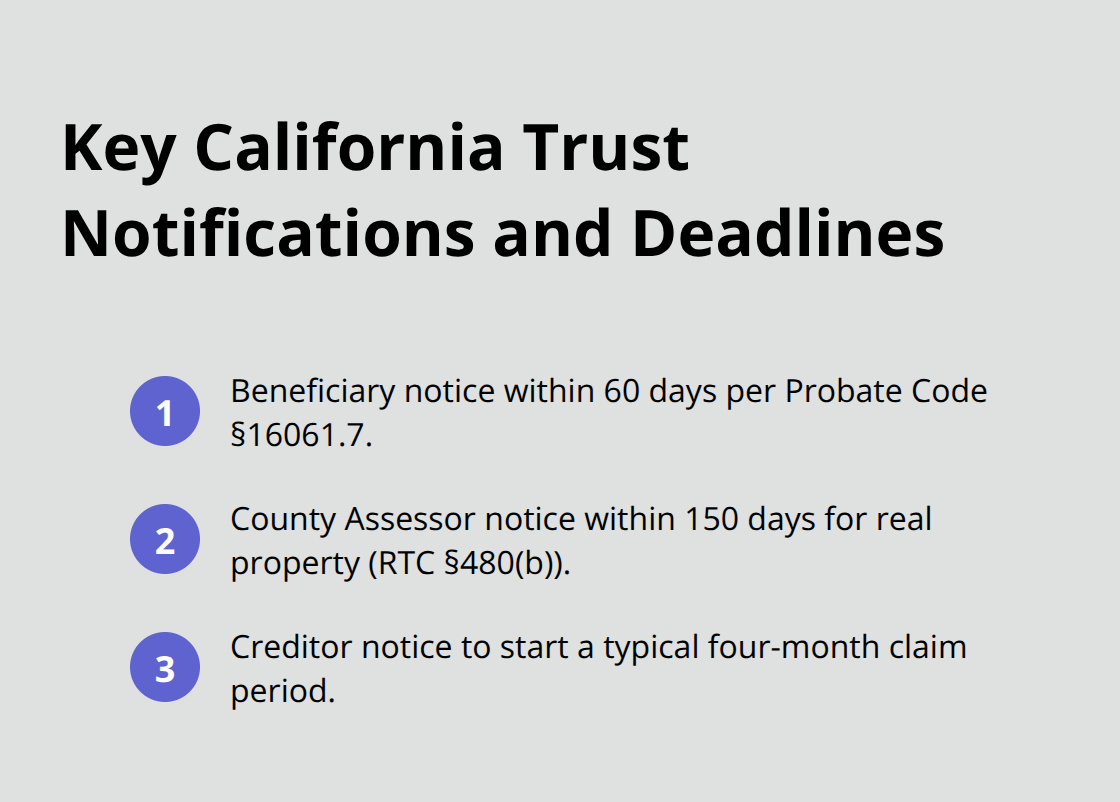

Trust administration in California involves three interconnected responsibilities that demand immediate attention after a settlor’s death. The trustee must identify and safeguard all trust assets within days of death, then notify beneficiaries and creditors within strict legal timeframes. California Probate Code Section 16061.7 requires written notice to beneficiaries within 60 days, including the settlor’s name, death date, trustee contact information, and the right to obtain a trust copy. Simultaneously, the trustee must notify the county Assessor within 150 days for any real estate held in trust, as required by Revenue and Taxation Code Section 480(b). Creditors must also receive notice so their claim period begins, typically within four months. Missing these deadlines creates immediate legal exposure and can trigger beneficiary lawsuits or costly penalties.

Managing Assets and Investments

Asset management requires the trustee to obtain current valuations, secure titles to properties in the trust’s name, and make prudent investment decisions. The trustee must prepare an inventory and appraise assets at the date of death to determine whether federal or state estate taxes apply and to support proper accounting. Real property should be rented or sold based on the trust’s terms, while liquid funds must be invested conservatively to generate reasonable returns without excessive risk. If assets are titled incorrectly or not in the trust’s name, the trustee may need to petition the court to include them under Probate Code Section 17200, which delays distribution and increases costs. Protecting assets from loss, theft, or depletion is a fiduciary duty that cannot be delegated away, even when hiring property managers or financial advisors.

Tax Obligations and Distributions

Tax responsibilities demand precise execution and timely filing. The trustee must file the settlor’s final income tax return for the year of death, obtain a new fiduciary tax ID number for the trust from the IRS, and file trust tax returns (IRS Form 1041) for any post-death income. California has no state estate tax, but federal estate taxes may apply to larger estates. The trustee must determine which debts and liabilities are valid, pay them from trust assets, and maintain detailed records of all transactions. Some trusts include multi-year distribution schedules that delay certain payments, requiring the trustee to hold and invest funds while managing tax consequences for beneficiaries. Missing tax deadlines results in penalties that compound quickly and reduce the inheritance available to beneficiaries.

Why Professional Guidance Prevents Costly Errors

These interconnected tasks create substantial risk when trustees attempt administration alone. A single missed deadline or mismanaged asset can expose the trustee to personal liability and trigger disputes with beneficiaries. The combination of California Probate Code requirements, IRS filing obligations, and state-specific property rules (including Proposition 19 considerations for real estate) makes professional guidance invaluable. Trustees who work with an attorney from the start avoid the costly mistakes that emerge later-mistakes that drain estate value and fracture family relationships. The next section examines the most common errors trustees make and how they damage estates.

Where Trust Administration Mistakes Happen Most

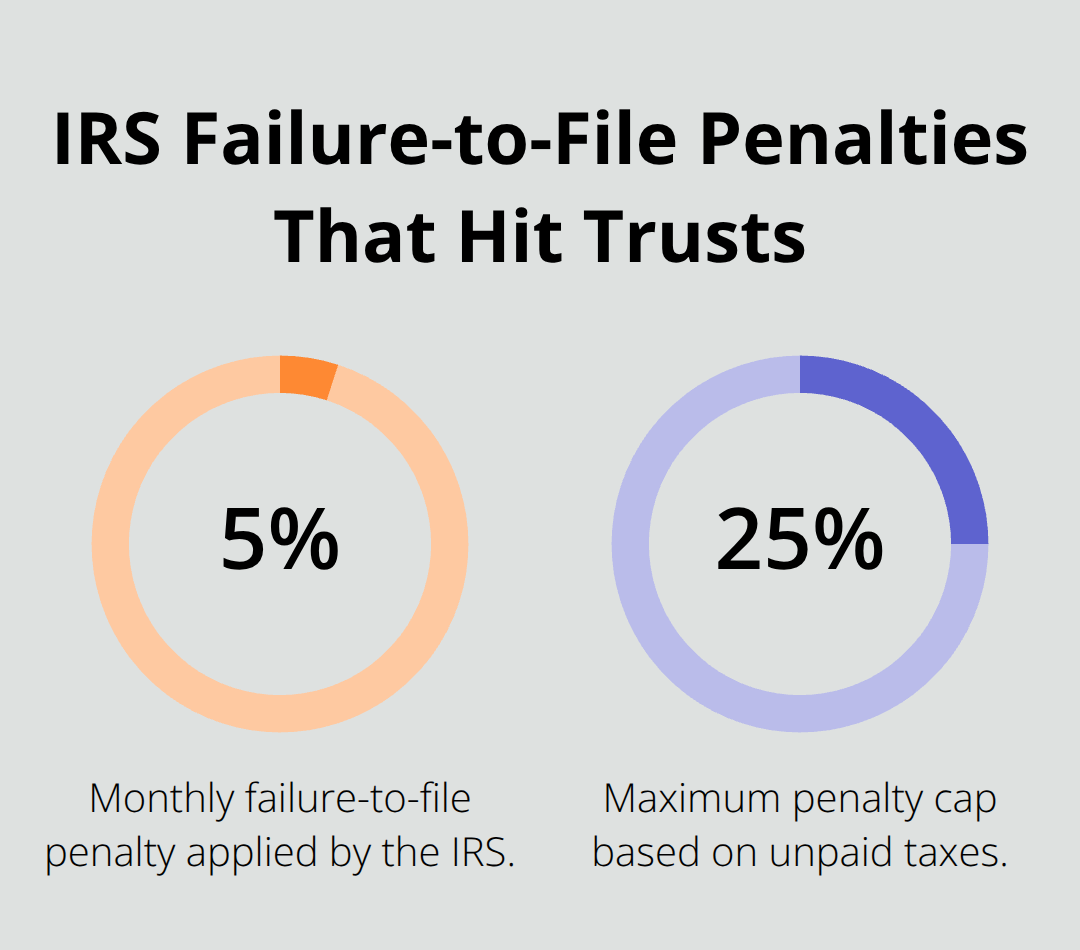

Trustees stumble at the exact moments when precision matters most. Tax filing deadlines arrive faster than expected, and the IRS does not grant extensions based on confusion or complexity. A trustee who misses the deadline for filing the settlor’s final income tax return faces immediate penalties that reduce the estate value available to beneficiaries. The Internal Revenue Service charges failure-to-file penalties of 5 percent per month, capping at 25 percent of unpaid taxes. When a trustee obtains a new fiduciary tax ID for the trust but fails to file IRS Form 1041 for post-death income, the trust itself faces penalties and interest that compound monthly.

California Probate Code Section 16061.7 requires written notice to beneficiaries within 60 days of death, yet many trustees send notices late or omit critical information like the trustee’s contact details or beneficiaries’ right to obtain a trust copy. Courts enforce these deadlines strictly, and late notice triggers beneficiary lawsuits that cost thousands in legal fees and damage family relationships permanently.

Tax Filing Deadlines Create Immediate Exposure

The IRS imposes strict timelines that trustees cannot negotiate or extend. A trustee who files the settlor’s final income tax return after the deadline incurs penalties that reduce what beneficiaries receive. The failure-to-file penalty of 5 percent per month (capping at 25 percent) applies automatically, with no exceptions for trustees who claim they were unaware of the requirement. When a trustee obtains a new fiduciary tax ID but fails to file IRS Form 1041 for post-death income, penalties and interest compound monthly on the trust’s account. These penalties accumulate faster than most trustees anticipate, and the IRS collects them from trust assets before distributions reach beneficiaries.

Notification Requirements Demand Precision and Speed

California Probate Code Section 16061.7 mandates written notice to beneficiaries within 60 days of death, and trustees who miss this deadline face legal consequences. The notice must include the settlor’s name, death date, trustee contact information, and the beneficiary’s right to obtain a copy of the trust document. Many trustees send notices late or omit one or more required elements, giving beneficiaries grounds to petition courts to compel proper notice and potentially remove the trustee. Courts have enforced these requirements strictly, treating late or incomplete notices as breaches of fiduciary duty. A trustee must also notify the county Assessor within 150 days for any real estate held in trust (Revenue and Taxation Code Section 480(b)), and creditors must receive notice so their claim period begins. Missing any of these notifications creates cascading legal exposure.

Asset Mismanagement Errors Cannot Be Reversed

Trustees create a second category of costly errors through improper asset handling. Some trustees fail to obtain current appraisals at the date of death, which distorts the estate’s tax basis and creates disputes with beneficiaries over valuation accuracy. Others leave real property titled in the settlor’s individual name instead of transferring it into the trust, forcing the trustee to petition the court under Probate Code Section 17200 to include the property. This petition delays distributions by months and adds court costs that reduce the inheritance. Trustees who invest liquid trust funds in high-risk or speculative securities violate their fiduciary duty to invest with reasonable care, and beneficiaries have grounds to sue for losses. A trustee who fails to notify the county Assessor within 150 days of death for real estate held in trust risks missed property tax deadlines and penalties under Revenue and Taxation Code Section 480(b). These errors compound because they interact with tax obligations and beneficiary rights in ways that create additional liability.

Beneficiary Accounting Delays Trigger Legal Action

Trustees who delay providing accountings to beneficiaries beyond the timeframes required by California law give beneficiaries legal grounds to petition courts to compel reporting and potentially remove the trustee. Beneficiaries have the right to request trust accountings, and if a trustee fails to provide one within 60 days of the request, courts can intervene. This delay signals to beneficiaries that the trustee may be mismanaging assets or hiding information, which escalates family conflict and increases the likelihood of litigation. The trustee’s failure to maintain detailed records of all transactions compounds the problem, as beneficiaries cannot verify that assets were managed properly or that distributions were calculated correctly.

The Interconnected Nature of Administration Errors

These mistakes share a common root: trustees assume they can handle administration alone, then discover too late that California law demands simultaneous attention to dozens of deadlines, regulatory filings, and notification requirements that interact in complex ways. A missed tax deadline affects the trust’s tax basis, which then impacts distributions to beneficiaries and creates accounting disputes. A delayed beneficiary notification can trigger litigation that freezes asset distributions and forces the trustee to defend actions in court. The combination of Probate Code requirements, IRS filing obligations, and state-specific property rules (including Proposition 19 considerations for real estate) creates a system where one error cascades into multiple problems. Trustees who work with an attorney from the start avoid these compounding mistakes and protect both the estate and their own liability. The next section explains how professional guidance helps trustees navigate these interconnected requirements and keep administration on track.

How We Help Santa Ana Trustees Navigate Administration

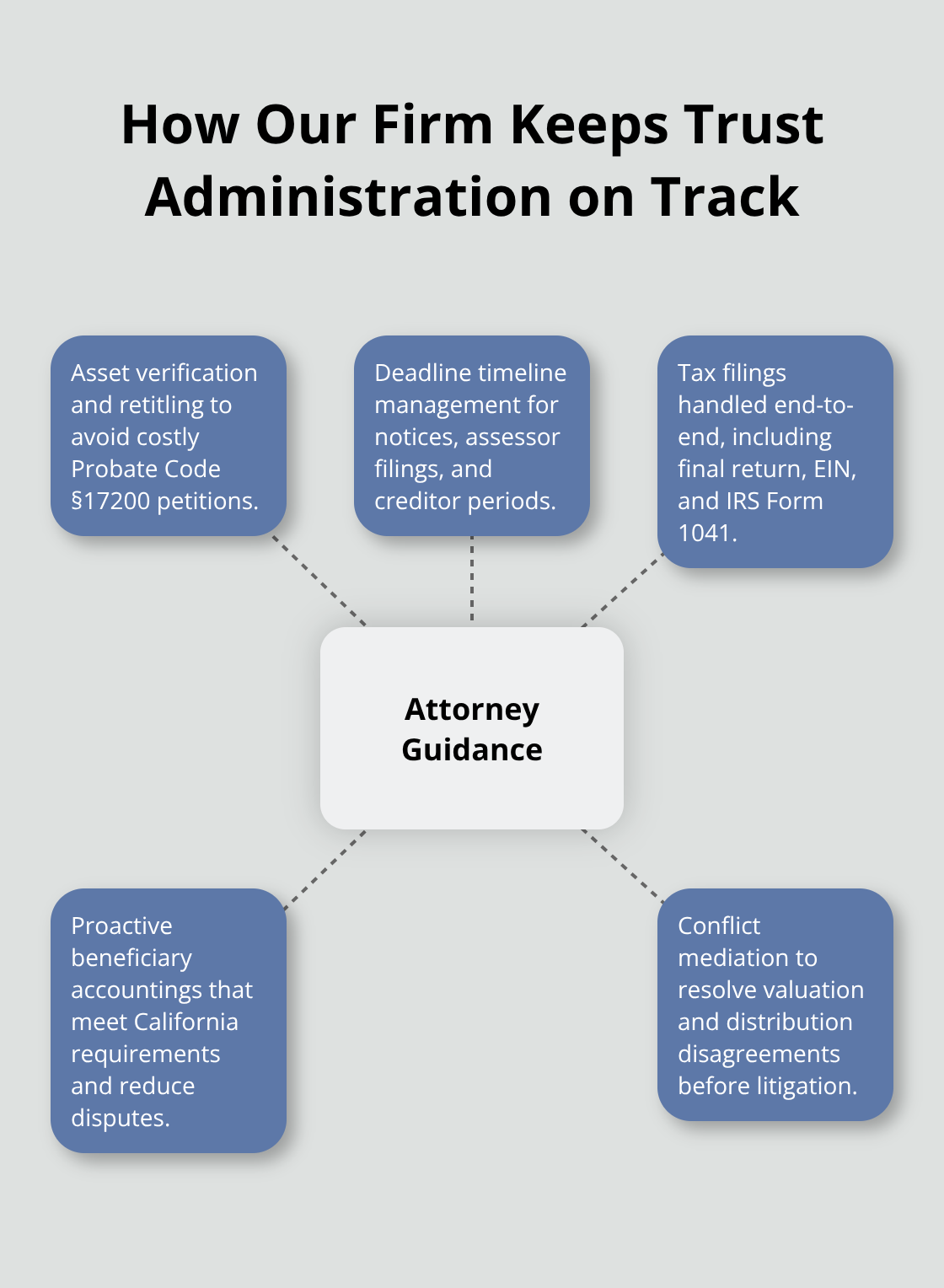

We at Law Offices of Roshni T. Desai work alongside trustees from the moment a settlor dies, moving through administration with a clear roadmap that prevents the cascading errors discussed above. The first step involves understanding exactly what assets exist and where they are titled. Many trustees discover too late that property sits in the settlor’s individual name instead of the trust, or that bank accounts lack proper beneficiary designations. We verify asset locations immediately, then work with county assessors, financial institutions, and title companies to transfer or retitle assets into the trust’s name. This prevents the costly court petitions under Probate Code Section 17200 that delay distributions by months.

Establishing Asset Values and Ownership

We coordinate with appraisers to establish accurate valuations at the date of death, which locks in the tax basis and eliminates disputes with beneficiaries over whether assets were valued fairly. Trustees often assume they can handle appraisals themselves, but professional valuations protect the estate from IRS challenges and give beneficiaries confidence that the trustee acted with care. We then create a master timeline for every deadline: the 60-day beneficiary notice under Probate Code Section 16061.7, the 150-day county assessor notification for real estate under Revenue and Taxation Code Section 480(b), the creditor notification period, and all tax filing deadlines. This timeline ensures nothing slips through the cracks.

Managing Tax Filings and Distributions

Tax obligations demand simultaneous attention to multiple filings, and this is where trustees face the steepest learning curve. We file the settlor’s final income tax return by the deadline, obtain the trust’s new fiduciary tax ID from the IRS, and file IRS Form 1041 for any post-death income the trust generates. We calculate which beneficiaries owe income taxes on distributions and prepare K-1 forms so beneficiaries can file their own returns accurately. For estates large enough to trigger federal estate taxes, we coordinate with tax professionals to determine whether the estate qualifies for portability or other federal benefits that reduce tax liability. We also manage the interaction between tax obligations and distributions-some trusts require the trustee to hold funds for multi-year distribution schedules, which means managing tax consequences for beneficiaries across multiple years.

Maintaining Records and Providing Accountings

We maintain detailed accounting records that satisfy California Probate Code requirements and give beneficiaries full visibility into how assets were managed and distributed. This documentation prevents the 60-day accounting disputes that trigger litigation. We handle beneficiary accountings proactively, sending detailed reports before beneficiaries request them and explaining the trustee’s decisions in plain language. This transparency eliminates the suspicion and conflict that typically arise when beneficiaries feel left in the dark.

Resolving Family Conflicts Before Litigation

When family conflict does emerge-disagreements over distribution timing, questions about asset valuations, or concerns about the trustee’s decisions-we mediate those disputes before they escalate into costly litigation. Many Santa Ana families avoid probate through living trusts but then face internal conflicts during administration that rival the cost of probate itself. We step in as a neutral voice to interpret the trust document, explain California law to frustrated beneficiaries, and guide the trustee toward decisions that satisfy everyone’s legitimate interests.

Final Thoughts

Trust administration in Santa Ana demands precision, timing, and knowledge of California law that most trustees cannot manage alone. Missed tax deadlines, delayed beneficiary notifications, and improper asset handling drain estate value and fracture family relationships in ways that are difficult to repair. An experienced trust administration attorney prevents these errors by establishing clear timelines, managing tax filings, and maintaining transparent communication with beneficiaries from day one.

Professional guidance saves money by avoiding penalties, court petitions, and litigation costs that quickly exceed the cost of hiring an attorney at the start. A trustee who works with legal counsel from the moment a settlor dies moves through administration efficiently, distributes assets on schedule, and protects themselves from personal liability. The time savings prove equally significant-trustees who handle administration alone spend months navigating deadlines and regulatory requirements, while professional guidance compresses the process and allows beneficiaries to receive their inheritance faster.

Santa Ana residents who have recently become trustees should act immediately and contact Law Offices of Roshni T. Desai to schedule a free consultation. Gather the trust document, death certificates, and a list of all assets the settlor owned before your first meeting. With experience in estate planning and trust administration across Southern California, we provide personalized guidance tailored to your family’s needs and help you navigate this complex process with confidence.