Small Business Trust Planning: Protecting Your Legacy and Cash Flow

Small business owners often overlook one critical reality: without proper planning, your business and personal assets face unnecessary taxes, delays, and public exposure after you’re gone.

Small business trust planning protects what you’ve built by keeping assets private, avoiding probate court, and reducing tax burdens on your family. At Law Offices of Roshni T. Desai, we’ve seen firsthand how the right trust structure makes the difference between a smooth transition and a financial nightmare for the next generation.

Why You Need Trust Planning Now

Probate Court Delays Cost Your Business Money

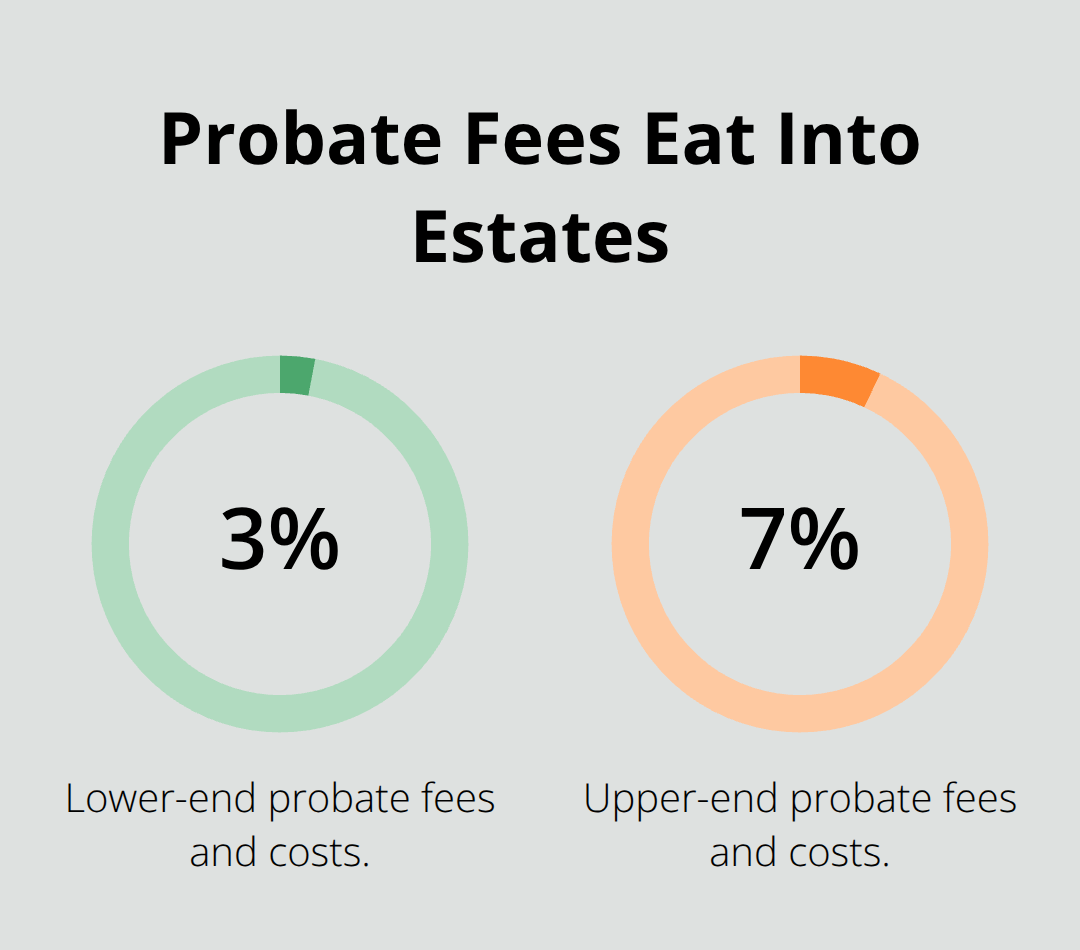

Probate court is where estates go to die-slowly and expensively. When a small business owner passes without a trust, their business and assets enter a public legal process that typically takes nine months to two years, depending on state complexity and whether heirs contest the will. During this time, the business sits in limbo. Employees wonder about their jobs. Customers question continuity. Vendors demand payment guarantees. Meanwhile, your family pays court fees, attorney fees, and executor fees that can consume 3 to 7 percent of the estate’s total value.

A revocable living trust eliminates probate entirely. You transfer ownership to the trust during your lifetime, allowing your chosen successor to step in immediately after your death without court involvement or public disclosure. This matters because every month of operational uncertainty costs money-lost clients, damaged vendor relationships, staff departures-costs that probate delays guarantee.

Privacy That Protects Your Business

Probate records are public. Anyone can walk into a courthouse and read exactly what you owned, what your business was worth, what debts you carried, and who inherited what. Competitors learn your financial details. Disgruntled customers or employees know your succession plan. Scammers target your heirs knowing their inheritance amounts.

A trust keeps all of this private. Trust documents and assets held in the trust never appear in public court records. Your business valuation, ownership structure, and succession arrangements remain confidential, giving your successor a clean start without public knowledge of the transition or inherited wealth. This privacy protection extends to your personal assets too-real estate, investments, bank accounts-all held privately within the trust rather than exposed in probate proceedings. For small business owners, this confidentiality translates directly to competitive advantage and security for your family.

Estate Taxes Don’t Have to Devastate Your Heirs

Federal estate tax applies to estates exceeding 13.61 million dollars in 2024, according to current IRS limits, but some states impose their own estate taxes at much lower thresholds. New York, for example, taxes estates over 6.94 million dollars. An irrevocable trust removes assets from your taxable estate permanently, reducing or eliminating estate tax exposure for your heirs.

The difference is substantial: a business valued at 5 million dollars could face hundreds of thousands in federal and state taxes without proper planning, forcing heirs to sell the business just to pay the bill. A properly structured trust plan prevents this forced liquidation. Additionally, trusts let you use lifetime gift tax exclusions strategically, transferring wealth to heirs during your life without triggering taxes. These strategies require coordination with your overall estate plan, but the tax savings alone justify professional guidance to structure the trust correctly from the start.

Understanding these three reasons-probate delays, privacy exposure, and tax liability-shows why trust planning matters. The next section explores the specific trust structures that protect small business owners and their families.

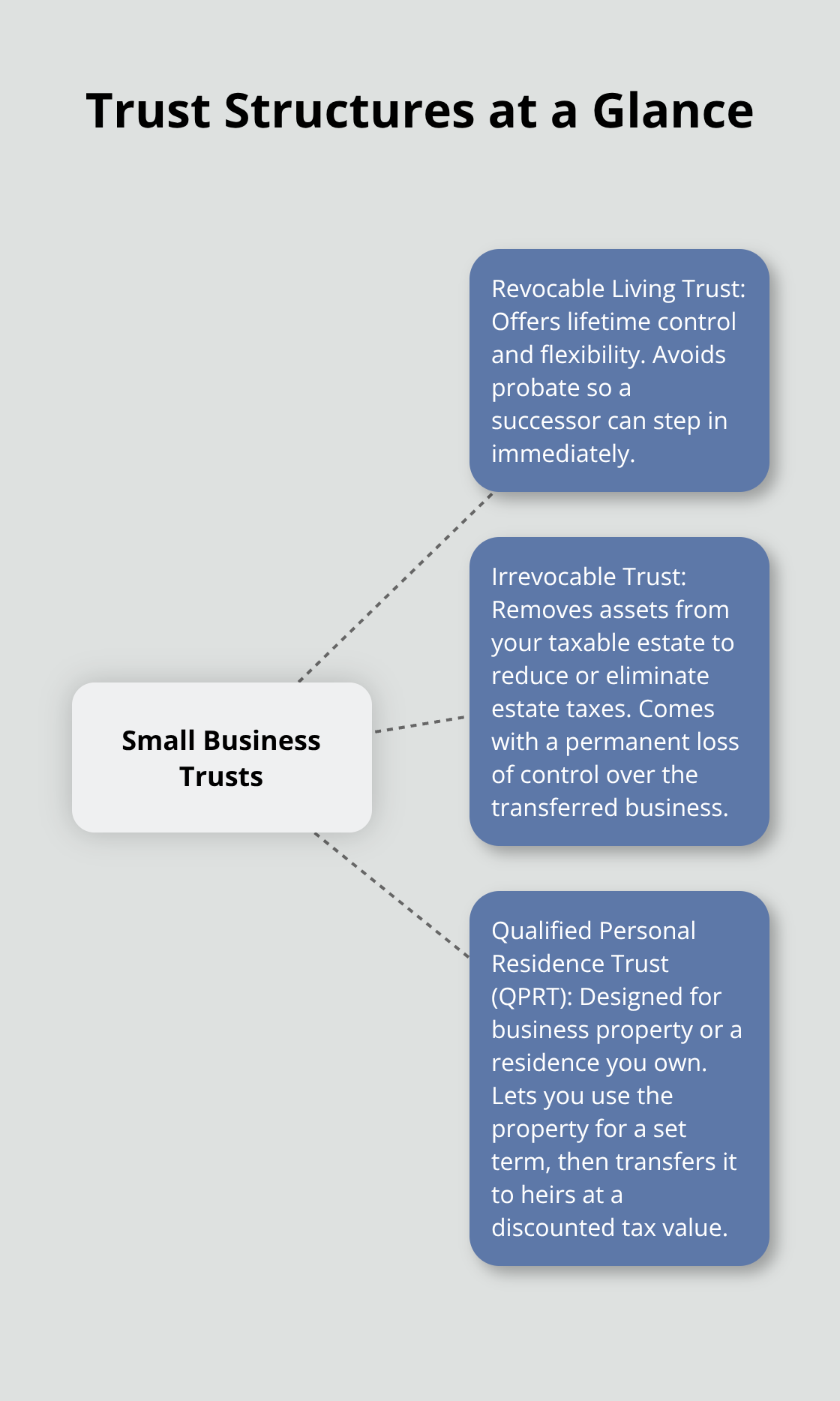

Which Trust Structure Fits Your Small Business

Revocable Living Trusts: Control and Flexibility

A revocable living trust gives you complete control during your lifetime while naming a successor trustee to manage the business immediately after your death or incapacity. You fund the trust by transferring business ownership to it while you’re alive, which means your chosen successor steps in without probate delays or court involvement. The critical advantage here is flexibility: you can amend the trust, remove assets, or change beneficiaries at any time. This matters for small business owners whose circumstances shift frequently.

If you bring in a partner, sell a division, or want to adjust how your children inherit the business, a revocable trust accommodates these changes without starting over.

The downside is minimal tax benefit-a revocable trust doesn’t reduce your taxable estate because you retain control, so federal and state estate taxes still apply. However, the probate avoidance and privacy protection alone justify this structure for most small business owners. Many business owners mistakenly think a revocable trust applies only to wealthy estates, but probate costs and operational disruption affect businesses of all sizes. A business valued at 1.5 million dollars still faces nine months to two years of court delays and 3 to 7 percent in fees, making a revocable trust practical regardless of your net worth.

Irrevocable Trusts: Tax Reduction at the Cost of Control

An irrevocable trust removes assets from your taxable estate permanently, which means those assets and their future growth avoid federal and state estate taxes entirely. This structure works best if your business is likely to appreciate significantly or if you’re approaching the federal estate tax threshold of 13.61 million dollars in 2024. The tradeoff is loss of control: once you transfer business ownership to an irrevocable trust, you cannot change your mind, retrieve the assets, or modify the terms.

For a small business owner, this demands absolute certainty about your succession plan and long-term vision. If your business faces market uncertainty or you might need to pivot, an irrevocable trust creates unnecessary rigidity. The permanent nature of this structure requires careful consideration before implementation.

Qualified Personal Residence Trusts: Real Estate Strategy

A qualified personal residence trust operates differently-it’s designed specifically for real estate. You transfer your business property or personal residence to the trust, retain the right to use it for a set term (typically 5 to 15 years), and then the property transfers to your heirs at a reduced tax value. This strategy works only if your business operates from property you own outright and you’re confident you won’t need to sell the property during the trust term.

The IRS calculates the gift tax based on the property’s value minus your retained use rights, resulting in substantial tax discounts. For example, a business property worth 3 million dollars might have a taxable gift value of only 1.5 million dollars after applying the discount, cutting your estate tax exposure in half. However, if you sell the property before the term ends or need to refinance, the strategy unravels and creates tax complications.

Choosing the Right Structure for Your Situation

Most small business owners benefit from starting with a revocable living trust, then layering in irrevocable strategies only after careful analysis of your business trajectory, tax exposure, and family circumstances. The right choice depends on your specific goals, business valuation, and willingness to accept restrictions on future control. Understanding these three structures positions you to make an informed decision about which approach protects your business most effectively. Working with a trust administration attorney ensures your plan aligns with California’s legal requirements and your long-term objectives. The next section addresses the common mistakes that undermine even well-intentioned trust planning efforts.

Common Mistakes Small Business Owners Make Without Trust Planning

Outdated Plans Undermine Your Legacy

Small business owners who fail to update their trust documents after major life changes essentially gamble with their legacy. Marriage, divorce, the birth of children or grandchildren, significant business growth, acquisition of new assets, or changes in tax laws all demand immediate updates to your trust structure. A trust drafted ten years ago does not reflect your current reality.

If you sold a division of your business but never updated the trust, your successor trustee inherits outdated instructions about assets that no longer exist. If you remarried without amending your trust, your new spouse may have no protection while your adult children from your first marriage receive everything, creating family conflict exactly when your family needs stability most. The IRS changes estate tax exemptions regularly-the 13.61 million dollar threshold in 2024 differs substantially from previous years, which means a trust designed under old tax rules may no longer serve your goals.

We at Law Offices of Roshni T. Desai recommend reviewing your trust every three to five years or immediately after any major life event. This is not optional maintenance; it is the difference between a plan that works and one that fails when it matters most.

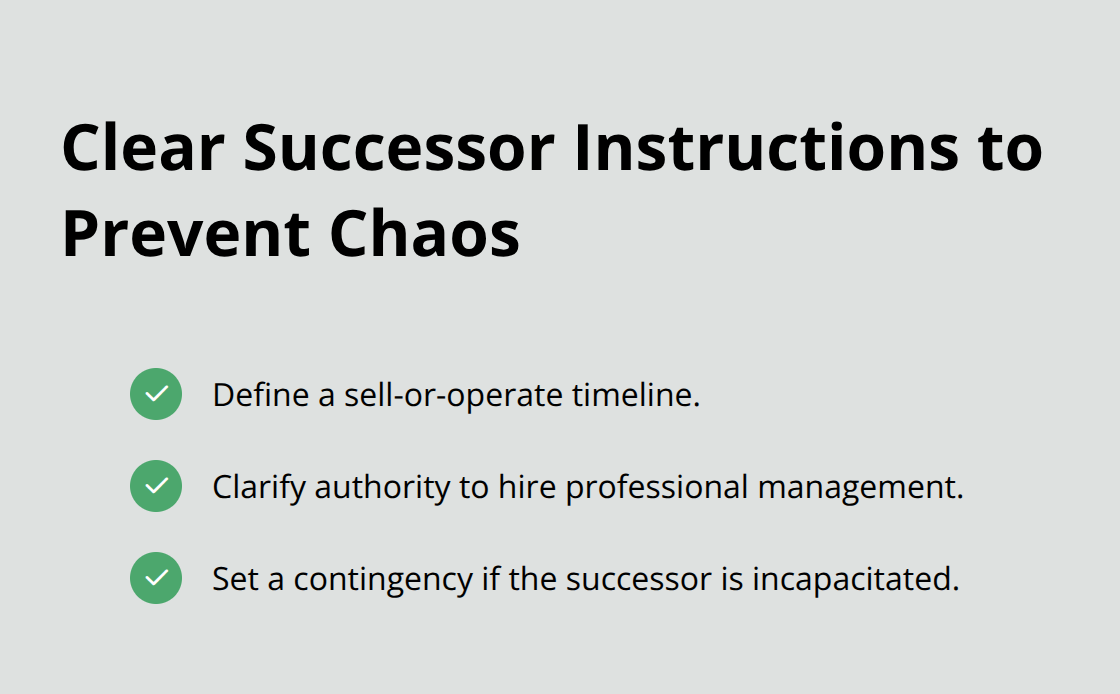

Unclear Successor Instructions Create Operational Chaos

Naming a successor without clarity about whether that person will own the business, manage it, or both creates dangerous ambiguity. Many business owners name their spouse as successor trustee, thinking this solves the problem, but spouses often lack industry knowledge, operational experience, or the temperament to lead a business through transition.

Your successor needs specific instructions: Should they sell the business immediately or operate it for five years before selling? Can they hire professional management or must they run it personally? What happens if they become incapacitated during their first year managing the company? Without these answers documented in your trust, your successor guesses.

Guessing during a business transition costs money through poor decisions, lost customers, and staff departures.

Assets Left Outside Your Trust Defeat the Entire Plan

Assets left without proper instructions create probate exposure even if you have a trust. If you own real estate outside your trust, hold accounts in your name alone, or maintain business interests that you never formally transferred to the trust during your lifetime, these assets bypass your trust structure entirely and enter probate.

Many small business owners fund a trust but never transfer the business ownership documents, leaving the business outside the trust protection they paid to create. This oversight happens frequently because business transfers require coordination with corporate governance documents and sometimes partner consent. The solution is straightforward: a trust only protects assets you actually place inside it. Documentation matters because incomplete funding undermines the entire strategy.

Final Thoughts

Small business trust planning accomplishes what no other strategy can: it protects your legacy while keeping your business operational and your family secure during the transition that matters most. Without a trust, your business enters probate court for nine months to two years, your assets become public record, and your heirs face estate taxes that may force them to sell the business just to pay the bill. A properly structured trust eliminates these outcomes entirely. The trust structures available-revocable living trusts for flexibility, irrevocable trusts for tax reduction, and qualified personal residence trusts for real estate-each serve different goals depending on your business size, growth trajectory, and family circumstances.

Early planning expands your options and control in ways that waiting cannot replicate. A business owner who plans at age 45 has far more flexibility than one who waits until age 65 when health concerns or market pressures force rushed decisions. The cost of professional guidance today is negligible compared to the cost of probate delays, tax exposure, or family disputes that poor planning creates. A trust only works if you fund it completely, update it regularly, and provide clear instructions to your successor about ownership, management, and decision-making authority.

We at Law Offices of Roshni T. Desai help small business owners structure trusts that fit their specific circumstances while protecting both legacy and cash flow. Your next step is straightforward: contact us to discuss your business and family goals. A qualified attorney will review your current situation, identify gaps in your planning, and recommend the trust structure that protects what you’ve built for the people who depend on it.