Living Trust Administration Steps: A Clear Path for Families

When a loved one passes away, administering their living trust can feel overwhelming. The living trust administration steps involve several key tasks, from locating assets to distributing funds to beneficiaries.

At Law Offices of Roshni T. Desai, we’ve guided countless families through this process. This guide breaks down each step so you understand what comes next.

What a Living Trust Is and Why Families Choose It

The Core Purpose of a Living Trust

A living trust is a legal document you create during your lifetime to hold and manage your assets, then transfer them to beneficiaries after you pass away-without going through probate court. Unlike a will, which becomes public record and requires court approval to distribute assets, a living trust keeps your financial details private and transfers property directly to the people you name. The American Bar Association defines the three core roles as grantor (you, the creator), trustee (the manager of assets), and beneficiary (the recipient). You typically serve as trustee while alive, maintaining full control over everything in the trust. When you become incapacitated or die, a successor trustee you’ve named steps in immediately to manage or distribute assets without delay. This avoids probate entirely-a process that in California takes 9 to 12 months or longer and costs thousands in court fees and attorney expenses.

Real Cost Savings and Privacy Benefits

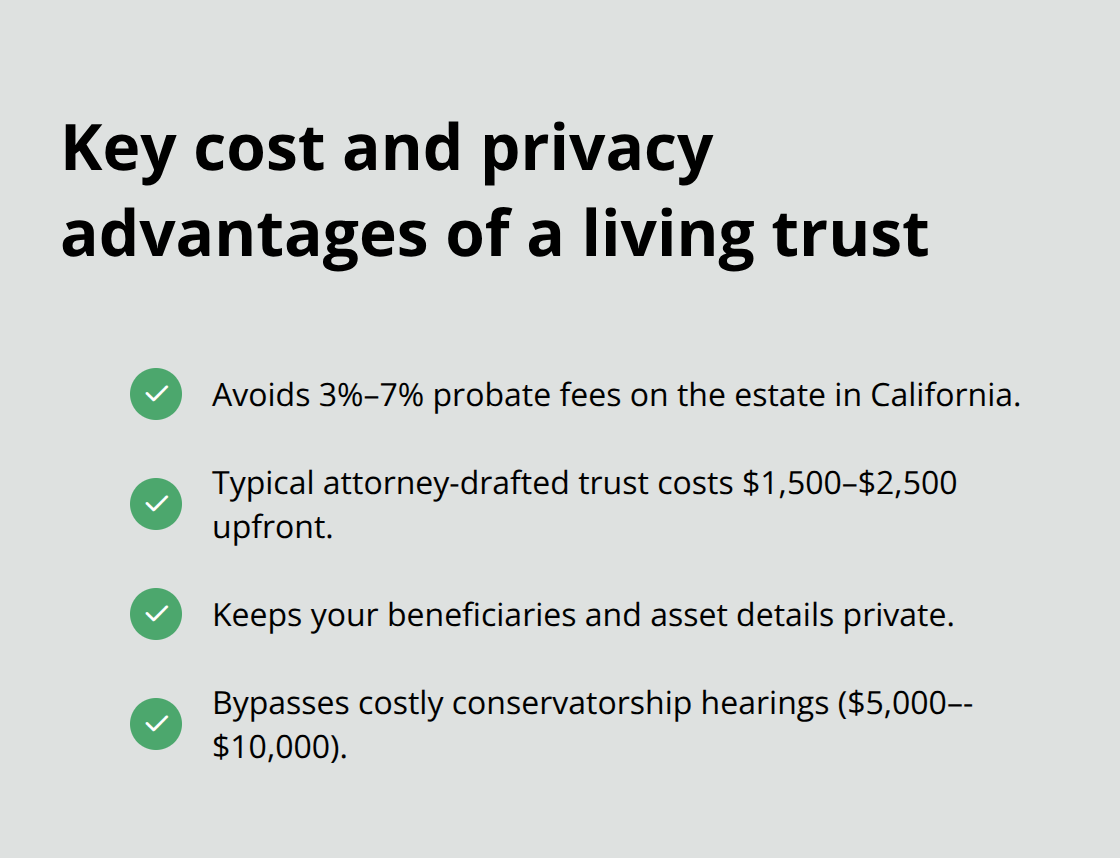

Families choose living trusts over wills for concrete reasons backed by real outcomes. Probate in California costs between 3% and 7% of the estate’s value, according to state bar data, making a $500,000 estate subject to $15,000 to $35,000 in probate costs alone.

A revocable living trust, which you can modify or revoke anytime, typically costs around $1,500 to $2,500 when drafted by an attorney-a one-time investment that saves far more later. Beyond cost, privacy matters: probate filings become public record, exposing your beneficiaries and asset details to anyone who searches court documents. A living trust administration stays completely private. Additionally, if you become mentally or physically unable to manage your affairs, a successor trustee named in your trust takes over immediately without a conservatorship hearing, which costs $5,000 to $10,000 and ties up assets in court for months.

The Non-Negotiable Step: Funding Your Trust

Proper funding-retitling assets into the trust’s name-determines whether your plan actually works. Many people create a trust but fail to fund it, leaving assets to pass through probate anyway. This mistake undermines otherwise solid plans. Assets must be retitled in the trust’s name (for example, “Jane Doe, Trustee of the Jane Doe Revocable Trust”) for the strategy to deliver its promised benefits. Without funding, your trust sits dormant while your estate still faces probate delays and public exposure.

Understanding these fundamentals prepares you for the actual administration steps that follow when a loved one passes away.

What Happens Right After Death

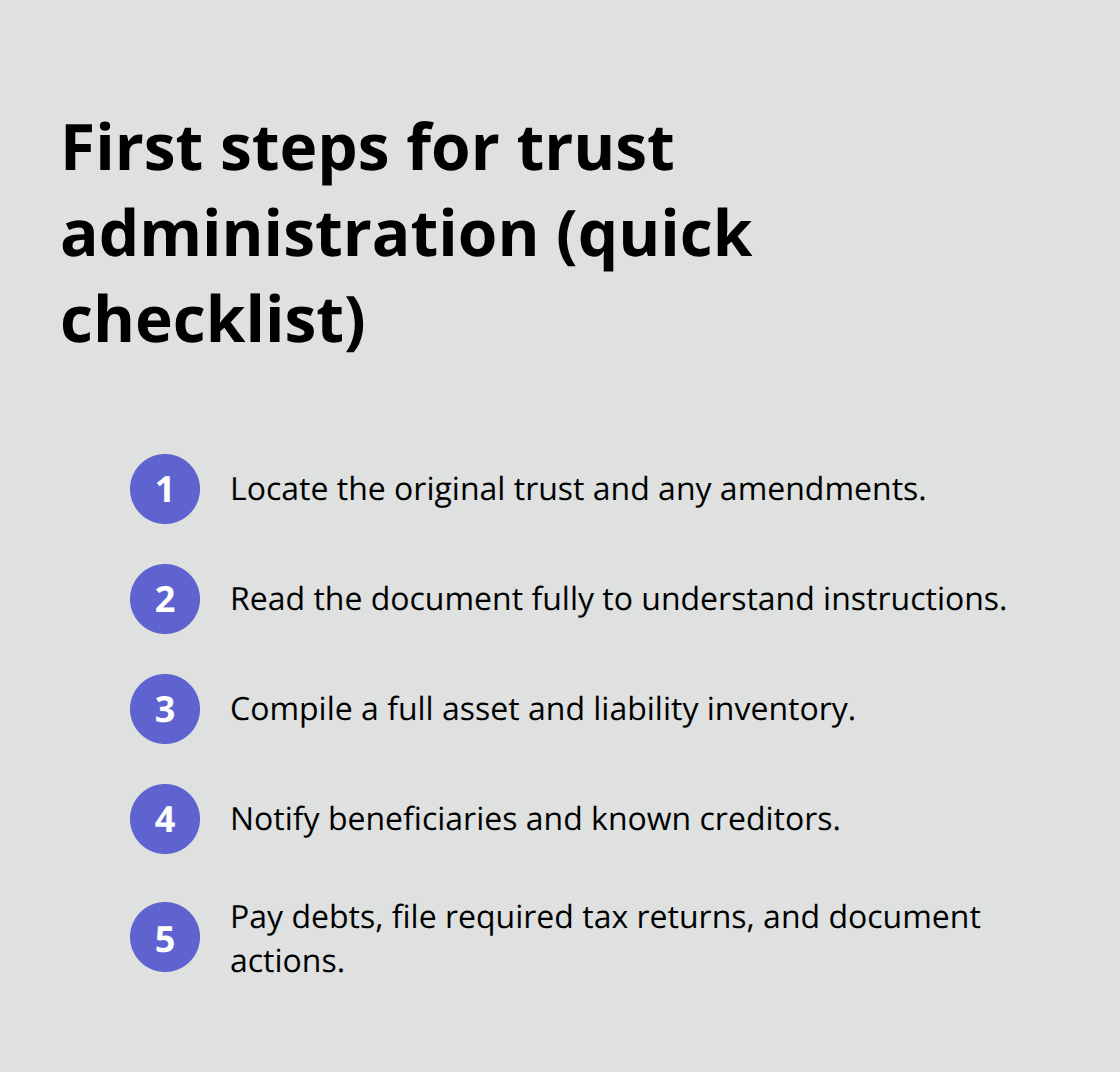

Locate and Understand the Trust Document

The first 48 to 72 hours after the grantor’s death demand immediate action. The successor trustee must locate the original trust document and any amendments, then read it thoroughly to understand exactly what instructions the grantor left behind. This document serves as your roadmap-without it, you administer blindly. Many families store originals in safe deposit boxes, home safes, or attorney offices. If the location isn’t obvious, contact the grantor’s bank, financial advisor, or the attorney who drafted it. Once found, read the trust multiple times to grasp distribution timelines, any conditions attached to bequests, and whether the trustee has discretion or must follow rigid instructions. Some trusts require distributions within 90 days; others allow longer timelines. Missing these deadlines exposes the trustee to liability claims from beneficiaries.

Create a Complete Asset and Liability Inventory

Next, create a comprehensive inventory of every asset titled in the trust’s name-real estate, bank accounts, investment portfolios, vehicles, and personal property. Contact each financial institution directly and request statements showing the trust as owner. Don’t rely on old statements; values change, and new accounts may exist.

For real estate, obtain current property tax assessments and appraisals if sales are planned. Simultaneously, identify all liabilities. Pull credit reports, check for mortgages, outstanding credit cards, and any loans against trust assets. This dual inventory (assets and debts) gives you the complete financial picture needed to administer properly.

Notify Beneficiaries and Creditors Within Legal Deadlines

California law requires the trustee to notify beneficiaries and known creditors within 60 days of the grantor’s death. Send formal written notice to all named beneficiaries and publish a notice in a local newspaper if required by the trust or state law. This notification period triggers a creditor deadline-typically creditors have four months from publication to file claims. These notifications protect the trustee by establishing a clear record of who knew what and when, reducing the risk of later disputes.

Pay Debts and File Tax Returns

Pay legitimate debts and taxes before distributing anything to beneficiaries. California requires estate and income tax returns if the trust generated income or held appreciated assets. The trustee must file a final individual income tax return for the grantor’s last year and potentially an estate tax return (Form 1041) for subsequent tax years. Work with a CPA or tax attorney experienced in trust administration; mistakes here cost thousands and create audit exposure.

Distribute Assets and Document Everything

After debts, taxes, and administration expenses are paid, distribute remaining assets exactly as the trust directs. If the trust names specific bequests-grandmother’s jewelry to Sarah, $50,000 to nephew James-distribute those first. Then distribute the remaining estate according to percentages or per stirpes provisions. Document every distribution with written receipts signed by beneficiaries. This protects the trustee from later claims that assets were mishandled. The entire process typically takes 6 to 12 months for straightforward estates, longer if real property sales or tax disputes arise.

These foundational steps set the stage for addressing the more complex challenges that often surface during administration-disagreements among beneficiaries, difficulty locating certain assets, and managing property transfers all demand careful attention and clear communication.

Common Challenges During Living Trust Administration

Beneficiary Disputes Derail Timelines and Relationships

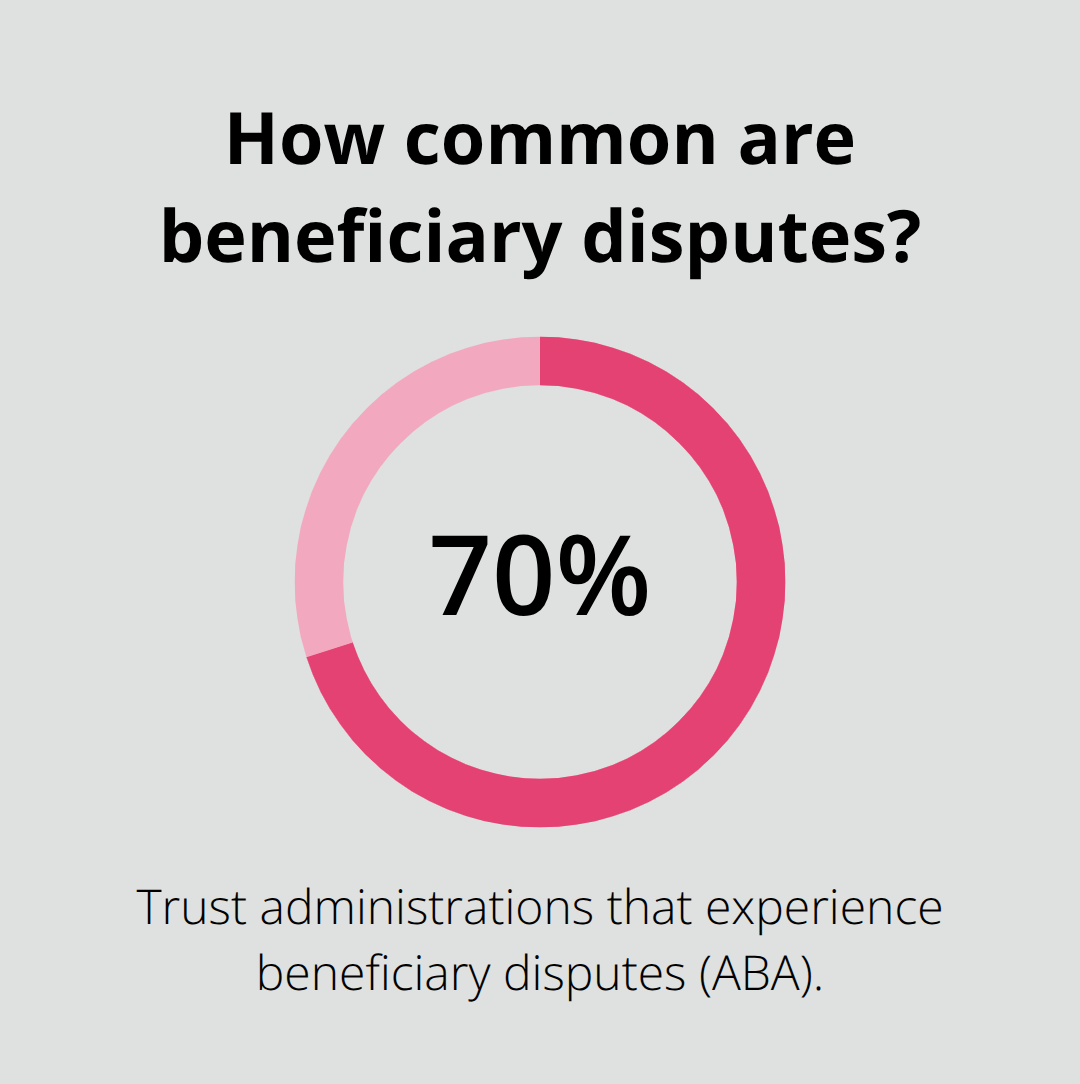

Beneficiary disputes surface in roughly 70% of trust administrations according to the American Bar Association, making conflict the single biggest reason administrations drag on past their expected timeline. These disputes rarely stem from vague language alone; they erupt when beneficiaries feel excluded from decisions, suspect the trustee favors other heirs, or disagree over how to value or sell assets.

The trustee bears the burden of proving fair dealing through transparent communication.

Send written updates to all beneficiaries at least quarterly, explaining what assets have been located, what debts were paid, and what timeline you’re following for distributions. If a beneficiary challenges a valuation or questions a trustee decision, address it immediately with documentation rather than silence. Silence breeds suspicion. For real estate appraisals, obtain written appraisals from licensed professionals and share them with beneficiaries; do not rely on estimates or casual valuations.

If beneficiaries genuinely disagree on whether to sell family property or distribute it in kind, mediation often costs far less than litigation and preserves family relationships. A mediator typically charges $200 to $400 per hour and can resolve disputes in one or two sessions; litigation costs tens of thousands and destroys trust within families.

Asset Location and Valuation Bottlenecks

Locating and valuing assets creates a second major bottleneck, especially when the grantor left incomplete records or held accounts at institutions that no longer exist. Pull credit reports for the deceased grantor to identify accounts you might have missed, then contact each institution directly and request statements as of the date of death. Digital asset discovery tools can help track online accounts and cryptocurrency holdings.

For valuations, never guess: obtain professional appraisals for real estate, collectibles, and business interests. The step-up in basis rule means assets receive a new valuation at the grantor’s death date, so accurate appraisals directly affect beneficiaries’ future tax liability. If you undervalue an asset, beneficiaries pay unnecessary capital gains taxes later; if you overvalue it, the estate may owe estate taxes it should not.

Real Property Transfers Demand Professional Handling

Real property transfers require careful deed preparation and county recording to avoid title defects that surface months or years later when a beneficiary tries to sell. Work with a title company or attorney experienced in trust property transfers; the cost of professional handling ($500 to $1,500 per property) prevents far costlier title disputes.

Tax Obligations and Fiduciary Returns

Tax obligations demand equal precision. The trust must file final income tax returns, potentially an estate tax return, and possibly fiduciary income tax returns for years of ongoing administration. California has no state estate tax, but federal estate taxes apply to estates exceeding $13.61 million in 2024 according to the IRS. If the trust holds appreciated assets, the trustee must understand step-up in basis rules to minimize tax burden.

A CPA familiar with trust administration costs $2,000 to $5,000 but prevents audit exposure and makes distributions happen tax-efficiently. Professional guidance addresses each of these challenges systematically-organizing documents, keeping beneficiaries informed, and handling tax obligations correctly-to keep administrations on track and costs reasonable.

Final Thoughts

Living trust administration steps demand careful attention to detail, clear communication, and precise handling of financial and legal obligations. Each phase-from locating the trust document to inventorying assets to notifying beneficiaries to paying debts and taxes to distributing remaining assets-requires accuracy. A single missed deadline, misvalued asset, or unclear beneficiary communication triggers disputes that cost thousands and damage family relationships irreparably.

Most families benefit from professional guidance during administration because trustees often lack experience with tax filings, property transfers, and California-specific rules governing trust administration timelines. A CPA or attorney familiar with trust administration prevents costly mistakes, keeps the process moving forward, and typically costs $2,000 to $5,000-far less than the expenses audit exposure, title defects, and litigation between beneficiaries create. We at Law Offices of Roshni T. Desai understand that trust administration happens during an emotionally difficult time and provide personalized support across Southern California.

Ms. Desai’s dual licensure as both an attorney and real estate professional streamlines estate property sales and reduces costs and delays that often plague administrations. We offer free consultations with flexible home or office visits, so you can discuss your situation without added stress. Contact us today to learn how we can guide your family through trust administration with clarity and compassion.