Discretionary Trust Administration: Guidelines for Executors and Trustees

Serving as an executor or trustee comes with real legal responsibilities that many people underestimate. Discretionary trust administration requires careful attention to beneficiary needs, asset management, and strict compliance with state laws.

At Law Offices of Roshni T. Desai, we’ve seen trustees struggle with the practical side of their role-from documentation mistakes to missed deadlines. This guide walks you through the essential steps to administer a discretionary trust correctly.

What Discretionary Trusts Actually Give You

A discretionary trust places assets under the control of a trustee who decides how and when to distribute money or property to beneficiaries. Unlike a will that passes assets directly, a discretionary trust gives the trustee flexibility to respond to each beneficiary’s actual circumstances. As a beneficiary, you have no automatic right to distributions-the trustee determines what you receive based on the trust’s terms and your needs. This structure protects assets from creditors, reduces taxes through strategic timing, and keeps distribution decisions private. The trustee holds legal title to everything inside the trust, meaning beneficiaries cannot access assets without the trustee’s approval. This separation of ownership and benefit makes discretionary trusts powerful for multi-generational planning. Some trusts can last up to 125 years, allowing families to build wealth across multiple generations while maintaining control over how that wealth gets used. The trustee’s job is not to act as a personal accountant but to make reasoned decisions about distributions that serve the trust’s stated purpose and reflect each beneficiary’s genuine situation.

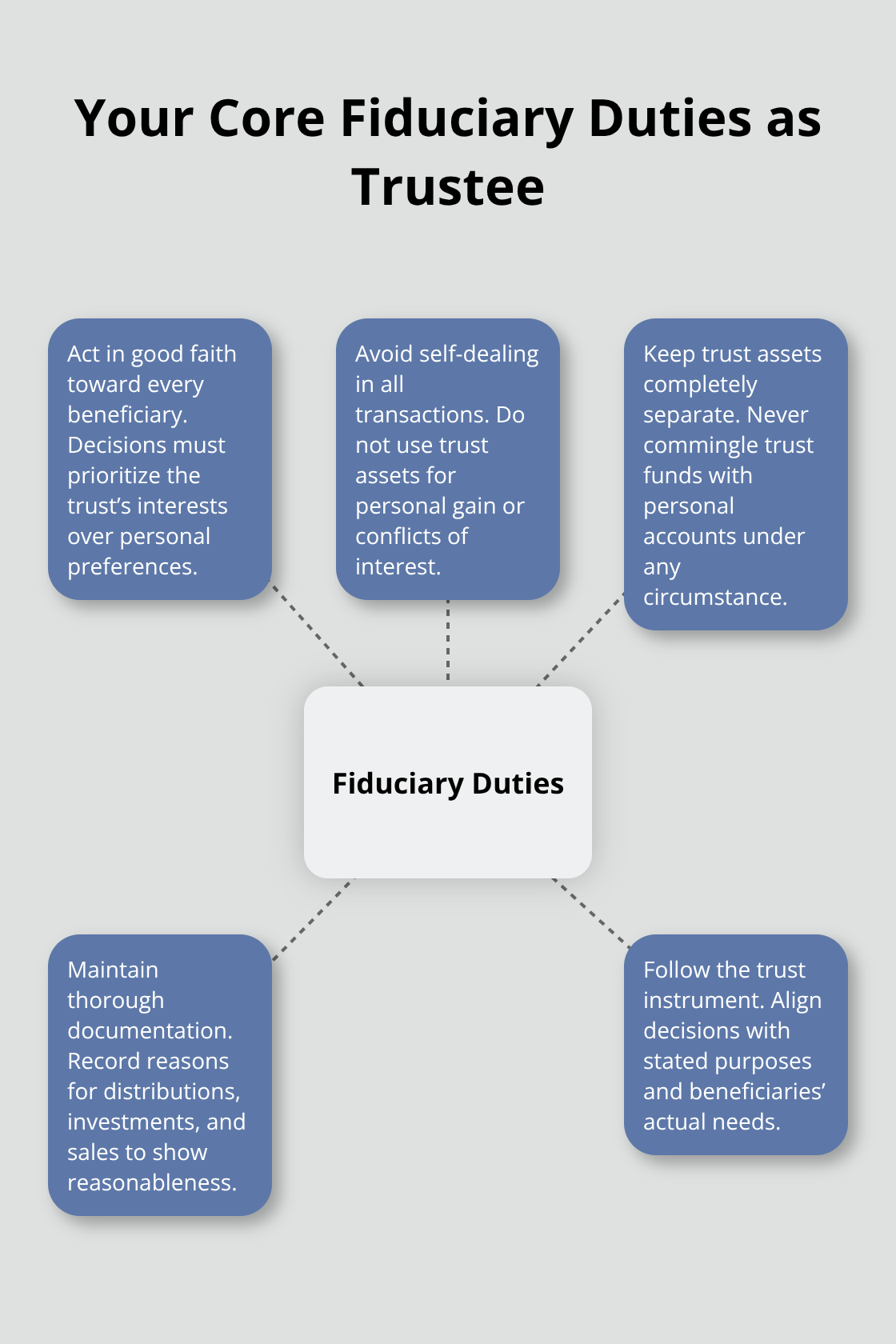

Your Core Fiduciary Duties

You owe fiduciary duties to all beneficiaries, not just the ones you like or the ones asking for money. This means acting in good faith, avoiding self-dealing, and keeping trust assets completely separate from your personal finances. Courts consistently hold that commingling trust money with your own accounts violates this duty, even if you eventually repay it. You must document every decision you make about distributions, investments, or asset sales-this documentation protects you if a beneficiary later challenges your judgment.

How Florida Law Bounds Your Discretion

Florida law requires trustees to exercise discretion reasonably and with proper attention to the settlor’s intent, according to cases like Wallace v. Julier and Hoppe v. Hoppe. Many trustees assume they have absolute power to do whatever they want, but Florida courts have rejected this interpretation repeatedly. Your discretion is bounded by the trust’s purpose and by the requirement that you act in good faith. If the trust specifies distributions for education or health care, you cannot redirect those funds to something else.

Creating a Record That Protects You

Keeping contemporaneous notes about why you made each distribution decision -what the beneficiary’s needs were, what other income they had, how the distribution aligned with the trust’s goals-creates a clear record that shows reasonableness and protects you from liability claims. This documentation becomes especially important when distributions involve substantial amounts or when multiple beneficiaries have competing interests. The next section covers how to evaluate beneficiary needs and circumstances in a way that supports both fair decisions and solid record-keeping.

Managing Trust Assets and Making Distributions

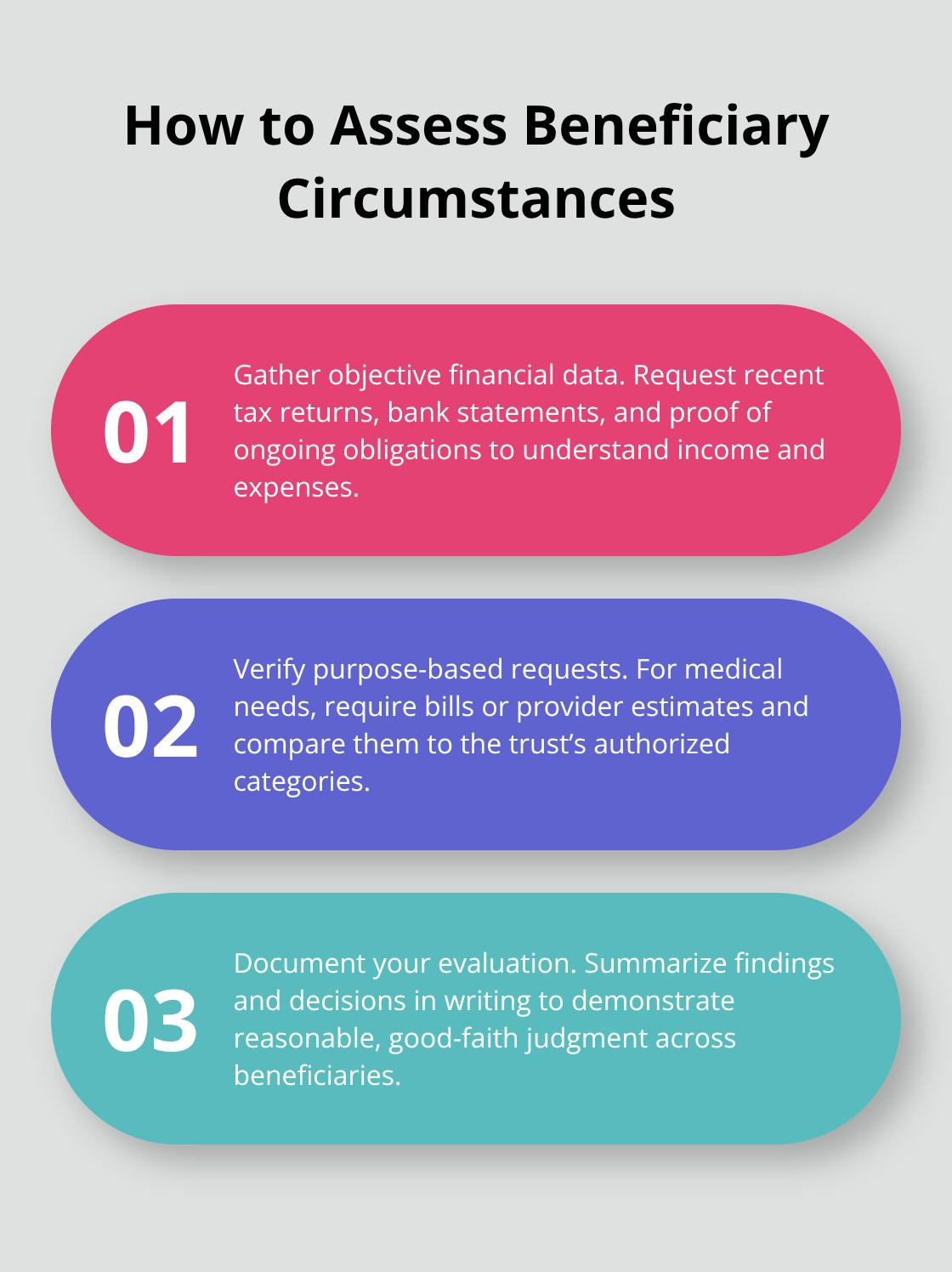

Assess Beneficiary Circumstances Before You Distribute

Evaluating what each beneficiary actually needs takes more than reading the trust document once. You need a clear picture of their income, expenses, health status, education goals, and other financial resources before you decide whether to distribute money. A beneficiary earning $150,000 annually has different needs than one who is unemployed or disabled.

Start by requesting recent tax returns, bank statements, and documentation of any ongoing support obligations. If a beneficiary claims they need funds for medical care, ask for medical bills or provider estimates rather than accepting vague requests. This approach protects you because it shows you applied reasonable judgment based on concrete facts. Courts reviewing trustee decisions look for evidence that you investigated circumstances rather than making arbitrary choices. Document these conversations in writing, either through email confirmations or brief notes dated and filed with trust records.

Handle Competing Beneficiary Requests Fairly

When multiple beneficiaries compete for distributions, your documentation becomes your defense against claims that you favored one person over another. The trust’s language matters too: if it authorizes distributions for health, education, maintenance, or support, you cannot stretch those categories to cover every request. A distribution for a vacation fails the maintenance standard, but one for medical treatment succeeds. If the trust gives you absolute discretion without limiting language, you have more flexibility, but Florida courts still require that you act in good faith and consider all beneficiaries’ interests, not just the loudest voices.

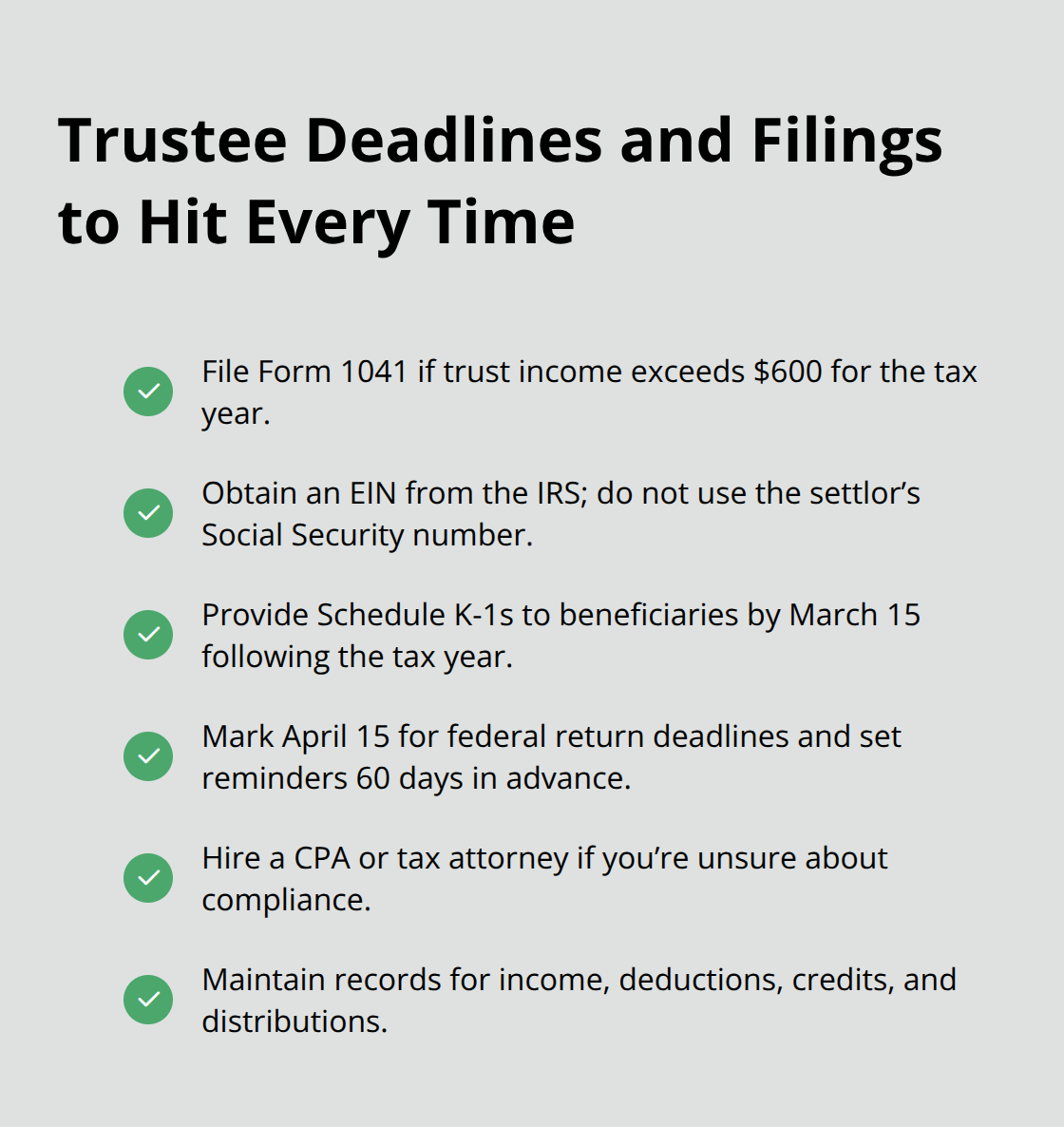

File Tax Returns and Obtain the Right Identification Number

Tax reporting obligations demand accuracy because mistakes trigger IRS penalties and can delay estate closure. You must file a fiduciary income tax return on Form 1041 if the trust earned income above $600 during the tax year, and you need an Employer Identification Number from the IRS rather than using the deceased settlor’s Social Security number. Each beneficiary who receives a distribution gets a Schedule K-1 showing their share of income, deductions, and credits, and you must provide these by March 15 following the tax year. Capital gains, dividend income, and interest earned inside the trust flow through to beneficiaries on their K-1s, affecting their personal tax liability.

Coordinate Asset Distributions with Tax Consequences

If you distribute appreciated assets to beneficiaries, those distributions may trigger capital gains tax consequences, so coordinate timing with a tax professional to minimize the overall tax hit. State inheritance taxes and local property taxes also apply in some cases, particularly if the trust holds real estate across multiple states. Many trustees fail to obtain a federal tax identification number promptly, causing filing delays and penalties. Obtain the EIN within 30 days of your appointment and keep it with your other trust records. Distributions made within two years after the settlor’s death receive more favorable tax treatment under some circumstances, so timing matters significantly.

Verify All Obligations Are Met Before Final Distributions

You should never distribute assets without confirming that all debts, taxes, and administration expenses have been paid or adequately reserved. Distributing the final assets before the last tax return is filed leaves you personally liable for unpaid taxes. These tax and distribution decisions set the stage for understanding the mistakes that derail many trustees-and how to sidestep them entirely.

Where Trustees Go Wrong and How to Stay on Track

Communicate Early and Often With Beneficiaries

Trustees fail most often not from lack of good intentions but from poor communication habits and incomplete asset management. The single biggest mistake is silence-trustees who avoid talking to beneficiaries until problems surface. When beneficiaries hear nothing for months, they assume the worst, question your judgment, and sometimes hire attorneys to investigate your conduct. Send a written summary within 30 days of your appointment outlining your role, the trust’s terms, and when beneficiaries can expect updates. Schedule quarterly check-ins, either in writing or by phone, to discuss distributions, asset performance, and any changes to beneficiary circumstances. This transparency prevents misunderstandings and shows you act deliberately rather than arbitrarily. If you must decline a distribution request, explain your reasoning in writing so the beneficiary understands your decision was based on the trust’s language and their actual needs, not personal preference.

Get Professional Appraisals for All Significant Assets

Asset valuation errors create the second major problem. Many trustees postpone obtaining professional appraisals for real estate, vehicles, art, or collectibles, thinking they can estimate value themselves or rely on tax assessments. This approach backfires when beneficiaries later dispute whether assets were valued fairly or when the IRS questions your valuations for tax reporting. Obtain written appraisals from qualified professionals for any asset worth more than $5,000, and keep those appraisals with your trust records. For real estate, hire a licensed appraiser rather than relying on Zillow or county records. For tangible personal property like jewelry or antiques, use a professional appraiser with relevant credentials. These costs typically run 0.5 to 1 percent of asset value but protect you from liability and provide documentation that withstands scrutiny.

Meet Every Deadline Without Exception

Missing deadlines is equally damaging-tax returns due by April 15, beneficiary statements by March 15, and trust accountings by court-ordered dates create hard deadlines that trigger penalties and sanctions if missed. Set calendar reminders for every deadline at least 60 days in advance, and if you lack confidence in tax compliance, hire a CPA or tax attorney to handle fiduciary returns. The cost of professional help is far less than penalties, legal fees from disputes, or personal liability for unpaid taxes.

Final Thoughts

Discretionary trust administration requires attention to detail, clear communication, and a willingness to seek professional help when you need it. The three core mistakes we covered-silence with beneficiaries, poor asset valuation, and missed deadlines-are entirely preventable if you establish systems from day one. Document your decisions, maintain separate accounts, and treat all beneficiaries fairly based on their actual circumstances and the trust’s stated purpose.

Florida law bounds your discretion more than you might think, so understanding the trust document and the settlor’s intent matters as much as having broad authority. Tax compliance alone involves multiple filings, identification numbers, and beneficiary statements that trip up people without accounting backgrounds. Asset appraisals, investment decisions, and distribution timing all have tax consequences that ripple through years of administration.

Your role as trustee is not to become a tax accountant or investment manager, but to act reasonably, document your choices, and know when to bring in professionals who can. We at Law Offices of Roshni T. Desai work with trustees and executors throughout Southern California to handle these complexities, from trust administration to property transactions related to trust assets. If you are managing a discretionary trust and feel uncertain about any step, contact us to discuss your situation and get the guidance you need to move forward with confidence.