California Revocable Trust Attorney: What to Expect in Estate Planning

A revocable trust is one of the most practical tools for managing your California estate without the delays and costs of probate. Many people create these trusts but then make critical mistakes that undermine their benefits.

At Law Offices of Roshni T. Desai, we help clients understand what a California revocable trust attorney can do for them and how to avoid the pitfalls that derail estate plans. This guide walks you through what to expect when working with us and how to build a trust that actually works for your situation.

What a Revocable Trust Actually Does for You

How Probate Costs and Delays Affect Your Estate

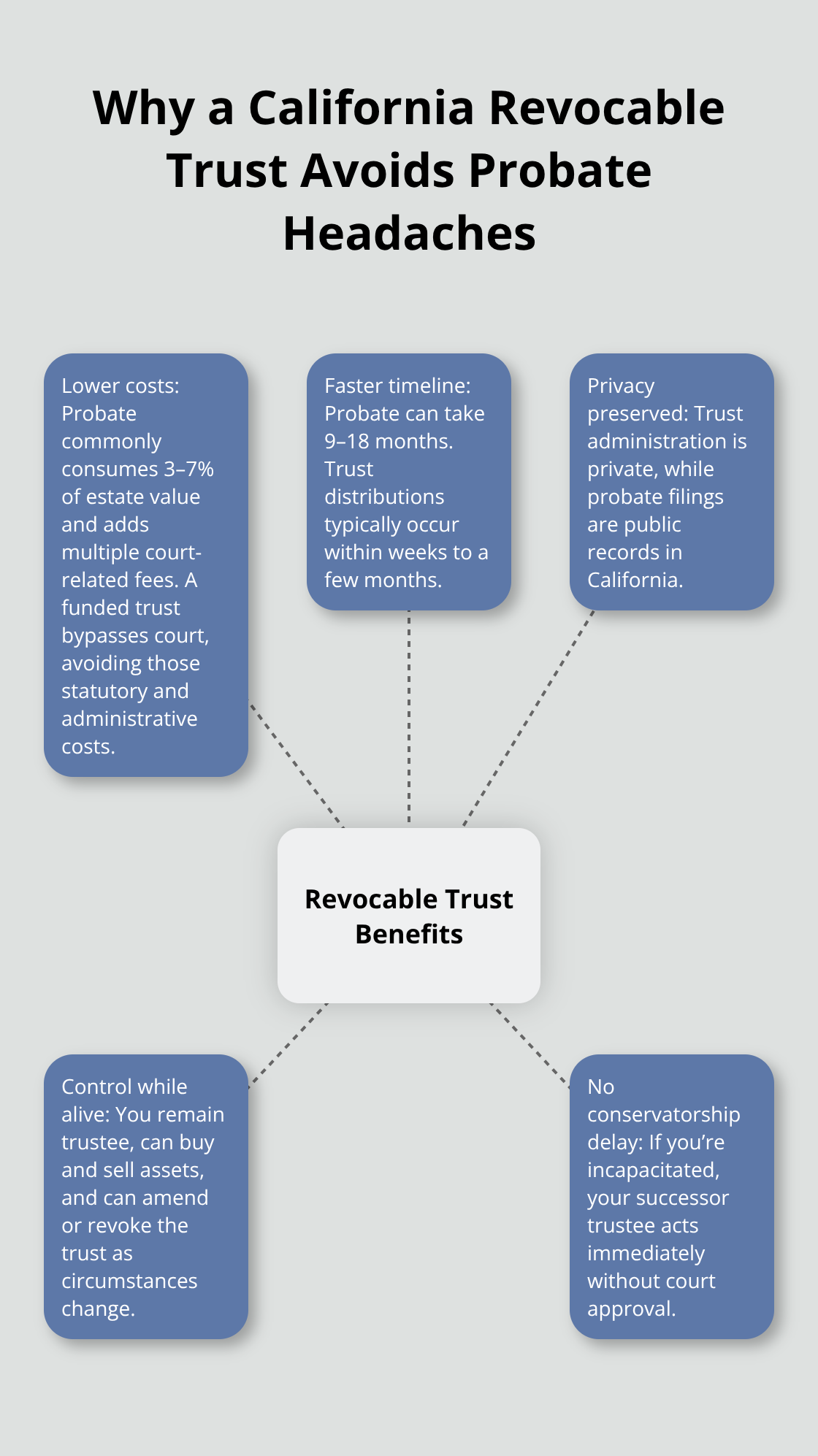

A revocable trust in California holds the title to your assets so those assets pass to your beneficiaries without probate. That core function matters because probate in California typically costs between 3 and 7 percent of your estate value. For a $1 million estate, you face roughly $46,000 in statutory attorney and executor fees alone, plus court filing fees starting around $435, publication costs between $200 and $500, and probate referee fees of about 0.1 percent of appraised assets. The process also stretches for 9 to 18 months, during which your beneficiaries wait for distributions.

A fully funded revocable trust sidesteps all of that. When you transfer real property, bank accounts, and investments into the trust during your lifetime, those assets belong to the trust, not to you personally. When you die, your successor trustee distributes them according to your written instructions without court involvement, typically within weeks to months. The California probate threshold stands at $208,850 as of April 1, 2025, so estates above that amount generally need either probate or a funded trust to avoid it.

Maintaining Control While You’re Alive

You remain the trustee while you’re alive and able, meaning you keep full authority over your assets and can buy, sell, or refinance property held in the trust. You can also amend or revoke the trust entirely at any time if your circumstances change-a marriage, a new child, a business sale, or a shift in your goals. That flexibility stands as a genuine advantage over irrevocable structures. The trust also protects you if you become unable to manage your finances due to illness or injury. Your successor trustee steps in immediately without needing court approval for a conservatorship, which would otherwise tie up your finances in a public court process.

Tax Treatment and the Stepped-Up Basis Advantage

A revocable trust is tax-neutral during your lifetime. The IRS treats you as the owner of trust assets on your personal tax return, so no separate tax filing requirement or loss of the stepped-up basis benefit occurs. Married couples receive particular value under California community property law. That double step-up in basis can be significant: a home now worth $1.2 million steps up to that value on the first spouse’s death, potentially eliminating capital gains tax on appreciated assets. The trust becomes irrevocable at your death, and your successor trustee then administers it according to your terms, which cannot be changed after that point.

Understanding these three functions-probate avoidance, lifetime control, and tax efficiency-forms the foundation for why a revocable trust works. The next step involves learning what happens when you actually sit down with an attorney to build one.

Working With a California Revocable Trust Attorney

What Happens During Your Initial Consultation

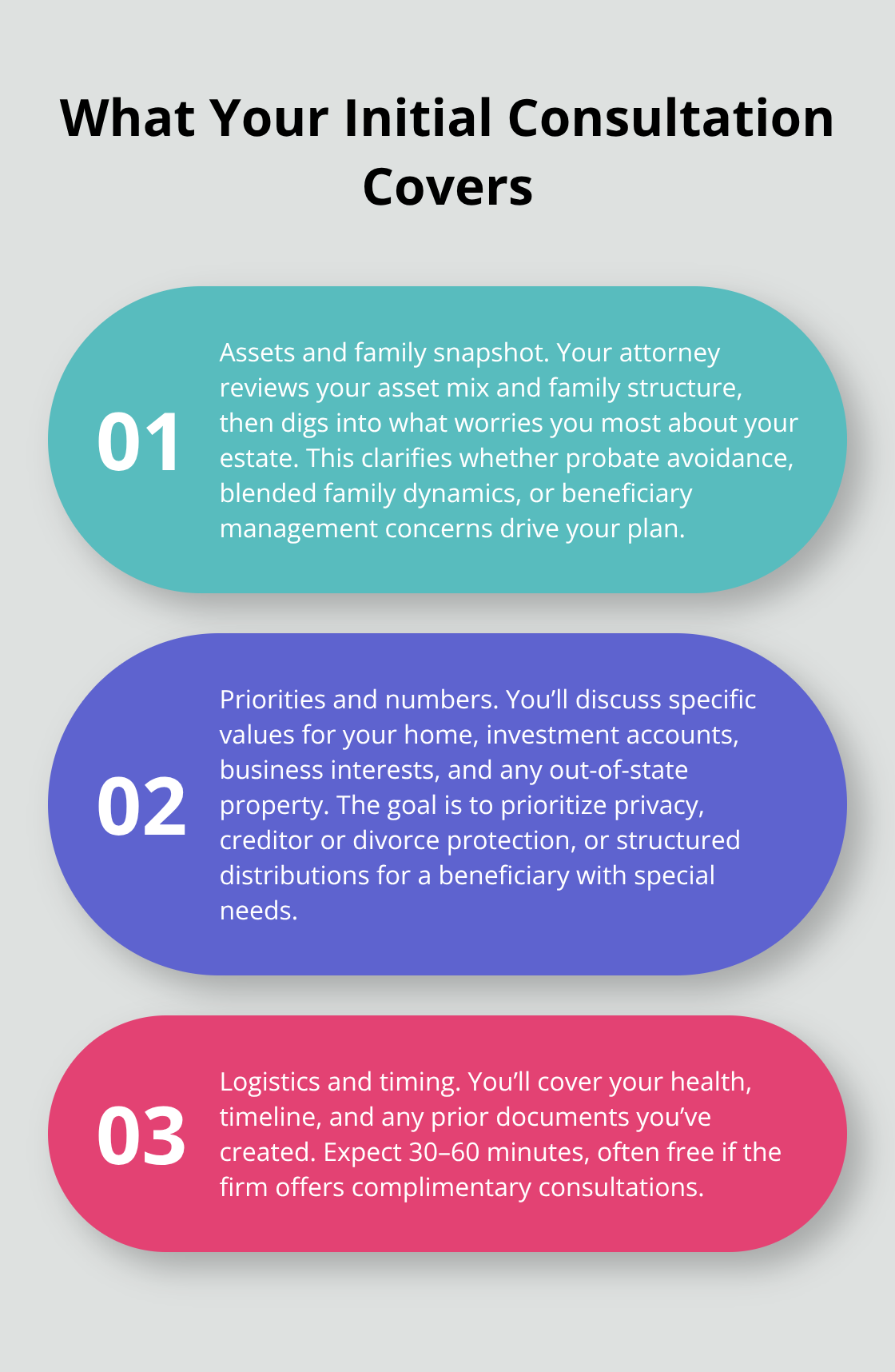

Your first meeting with a trust attorney shapes everything that follows. During the initial consultation, the attorney will ask detailed questions about your assets, family structure, and what worries you most about your estate. This isn’t generic questioning-it’s designed to uncover whether probate avoidance is your primary goal, whether you have blended family concerns, or whether you’re worried about a beneficiary’s ability to manage money responsibly.

Prepare to discuss real numbers: the value of your home, investment accounts, business interests, and any property outside California. Many people assume the attorney will know what matters most, but you need to articulate it clearly. Some clients prioritize keeping their estate private; others want to protect assets from a child’s creditors or divorce; still others need to structure distributions over time for a beneficiary with special needs.

The attorney will also ask about your health, your timeline, and whether you’ve already created documents elsewhere. This conversation typically lasts 30 to 60 minutes and often costs nothing if the firm offers free consultations.

Drafting Your Trust and Supporting Documents

Once you’ve decided to move forward, the attorney drafts your trust document along with supporting papers-a pour-over will, a durable power of attorney, and an advance healthcare directive. A professionally drafted package typically costs between $2,500 and $5,000 and includes everything you need to execute a complete plan.

The trust document itself lays out who serves as trustee during your life, who steps in as successor trustee after your death or incapacity, how assets distribute to beneficiaries, and any special conditions you want in place. This is where precision matters enormously. Vague language or omitted terms about remarriage or survivorship can fuel disputes later, so the attorney will work to ensure your instructions are clear and legally sound.

Funding Your Trust: The Step That Makes It Work

Roughly one in three trusts reviewed are not fully funded, which defeats the entire purpose of avoiding probate. Funding means retitling assets into the trust’s name-transferring real property through a deed recorded with the county, changing bank and brokerage accounts to the trust’s name, and reassigning business interests.

Retirement accounts like IRAs and 401(k)s typically stay in your name with the trust named as contingent beneficiary, since moving them into the trust can trigger unwanted tax consequences. Your attorney will provide a funding checklist and coordinate with title companies or financial institutions to ensure each asset transfers correctly.

After funding is complete, many attorneys offer verification services to confirm the trust holds what it should. This step separates a trust that actually works from one that sits dormant and fails when needed most. Once your trust is funded and your supporting documents are in place, the real protection kicks in-and that’s when understanding what happens next becomes important.

Common Mistakes People Make With Revocable Trusts

The Unfunded Trust Problem

The gap between creating a trust and actually funding it destroys more estate plans than any other single mistake. Roughly one in three trusts reviewed are not fully funded, meaning the assets you intended to protect still sit in your personal name and will drag through probate anyway. This happens because people focus on the legal document itself and overlook the mechanical work of retitling property. A trust sitting empty is worthless-it’s like buying insurance and never paying the premium.

Funding requires concrete steps: you record a new deed to transfer real estate into the trust with the county recorder’s office, call your bank to retitle savings and checking accounts, contact your brokerage to move investment accounts, and reassign any business interests or partnership stakes. Each financial institution has its own forms and timeline, which is why many people abandon the process halfway through. The cost to fund a trust is minimal-deed recording typically runs $10 to $300 depending on your county, notary fees around $2 to $15-but the inconvenience feels substantial.

Without verification, you won’t know until after your death whether the trust actually holds your assets, at which point it’s too late to fix the problem. A funding checklist and direct coordination with title companies and financial institutions can eliminate confusion and ensure each asset transfers correctly.

Outdated Trusts Miss Life’s Changes

Life happens: you marry, divorce, have children, sell a business, inherit money, or watch your net worth shift dramatically. Many people assume their 10-year-old trust still reflects their current wishes, but it doesn’t. Tax law changes too-the federal estate tax exemption sits at $15 million per individual in 2026, but that exemption sunsets in 2027 without Congressional action, meaning your plan may need adjustment before then.

You should review your trust every three to five years and update it whenever major events occur. Failing to do so means your trust might name an executor who’s now estranged, designate a beneficiary who no longer exists, or hold assets in a way that triggers unnecessary taxes. The cost of updating a trust is far less than the cost of fixing problems after death.

Tax Planning Opportunities You Can’t Afford to Miss

A revocable trust itself provides no tax savings during your lifetime, but married couples can structure their trust to capture the double step-up in basis under California community property law. If you own appreciated assets like real estate worth significantly more than you paid for it, that step-up can eliminate capital gains tax on the first spouse’s death (a home now worth $1.2 million steps up to that value on the first death, potentially erasing capital gains tax entirely).

Without proper structuring, you lose this benefit permanently. This tax planning opportunity requires attention at the outset, not after your trust is already in place. An attorney can help you understand whether your situation qualifies for this advantage and how to position your assets to capture it.

Final Thoughts

A revocable trust in California works only when three things happen together: it’s drafted with precision, it’s funded completely, and it’s updated when your life changes. Skip any one of these steps and your trust fails to deliver the probate avoidance and privacy you expected. The unfunded trust sits dormant, the outdated trust misses tax opportunities or names beneficiaries who no longer fit your wishes, and the poorly drafted trust creates confusion that your successor trustee must untangle after your death.

A California revocable trust attorney prevents these failures by asking the right questions during your initial consultation to understand what actually keeps you up at night-whether that’s protecting assets from creditors, structuring distributions for a beneficiary with special needs, or capturing the stepped-up basis advantage for appreciated property. They draft documents with the precision that prevents disputes later and provide a funding checklist that coordinates with financial institutions to transfer your assets into the trust. They flag tax planning opportunities like the double step-up in basis that married couples can capture under California community property law, potentially eliminating capital gains tax on appreciated assets worth hundreds of thousands of dollars.

The cost of professional guidance-typically $2,500 to $5,000 for a complete package-is negligible compared to the $46,000 in probate costs alone on a $1 million estate or the months of delay your beneficiaries face while waiting for distributions. We at Law Offices of Roshni T. Desai offer free consultations to discuss your situation and answer questions about whether a revocable trust fits your goals. Contact us to schedule your consultation and take the first step toward an estate plan that protects your family and preserves your legacy.