Executors Estate Planning: Building a Solid Plan for Loved Ones

Most people put off estate planning because they don’t understand what it involves. The truth is, executor estate planning isn’t complicated-it’s about making deliberate choices now so your family doesn’t face confusion and financial strain later.

At Law Offices of Roshni T. Desai, we’ve seen firsthand how a solid plan protects what matters most. This guide walks you through the essential steps to build one.

Understanding the Role of an Executor

What an Executor Actually Does

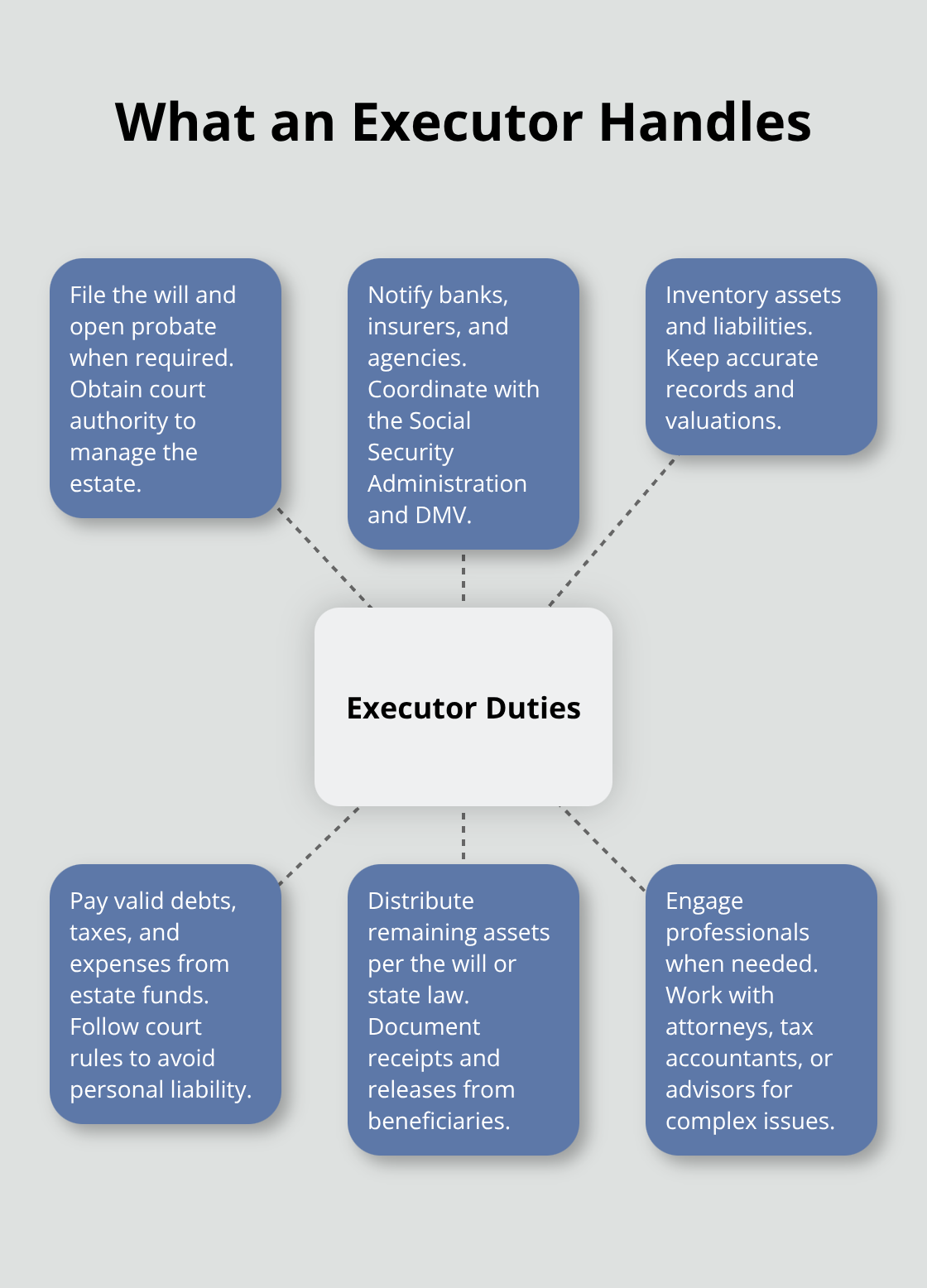

An executor administers your estate after you pass away. They handle everything from obtaining death certificates to distributing assets to beneficiaries. According to Cornell Law and Justia, the executor carries a fiduciary duty-a legal obligation to act in the best interest of your estate and beneficiaries, not themselves. This role carries real responsibility. If you die with a will, the executor files it with the probate court and petitions for authority to manage your affairs. They notify financial institutions, insurers, and government agencies like the Social Security Administration and DMV. They inventory all assets and liabilities, settle debts and taxes from estate funds, and ultimately distribute what remains according to your wishes.

The executor is often called a personal representative. In many states, a beneficiary can serve in this role-though that arrangement can create tension if other heirs feel their interests aren’t protected. When selecting an executor, prioritize trustworthiness, organizational ability, financial know-how, and conflict-resolution skills, not just family relationships.

Timeline and Complexity

The probate timeline varies dramatically depending on estate complexity. Simple estates settle in under a year, while more complex ones take several years, according to NOLO. During this time, your executor must appear in probate court, file inventories using court-approved forms, and handle disputes if beneficiaries contest the will.

Assets held in a living trust bypass probate entirely. The trustee manages the trust without court involvement, which speeds up settlement and protects privacy. This distinction matters significantly when you plan your estate structure.

Challenges Executors Face

Common obstacles include locating hard-to-find assets, managing family conflicts over distribution, and avoiding personal liability for unpaid taxes. The executor’s workload is substantial-they juggle deadlines, paperwork, legal requirements, and emotional family dynamics simultaneously. Many executors benefit from consulting professionals like estate planning attorneys, tax accountants, or financial advisors (whose fees typically come from estate assets). If your executor fails to perform duties, beneficiaries can petition the court to remove them and appoint a replacement.

The complexity of these responsibilities underscores why your estate plan must clearly define not just who serves as executor, but also what documents and instructions they’ll need to act effectively.

What Documents Your Estate Plan Must Include

The Foundation: Why a Will Alone Falls Short

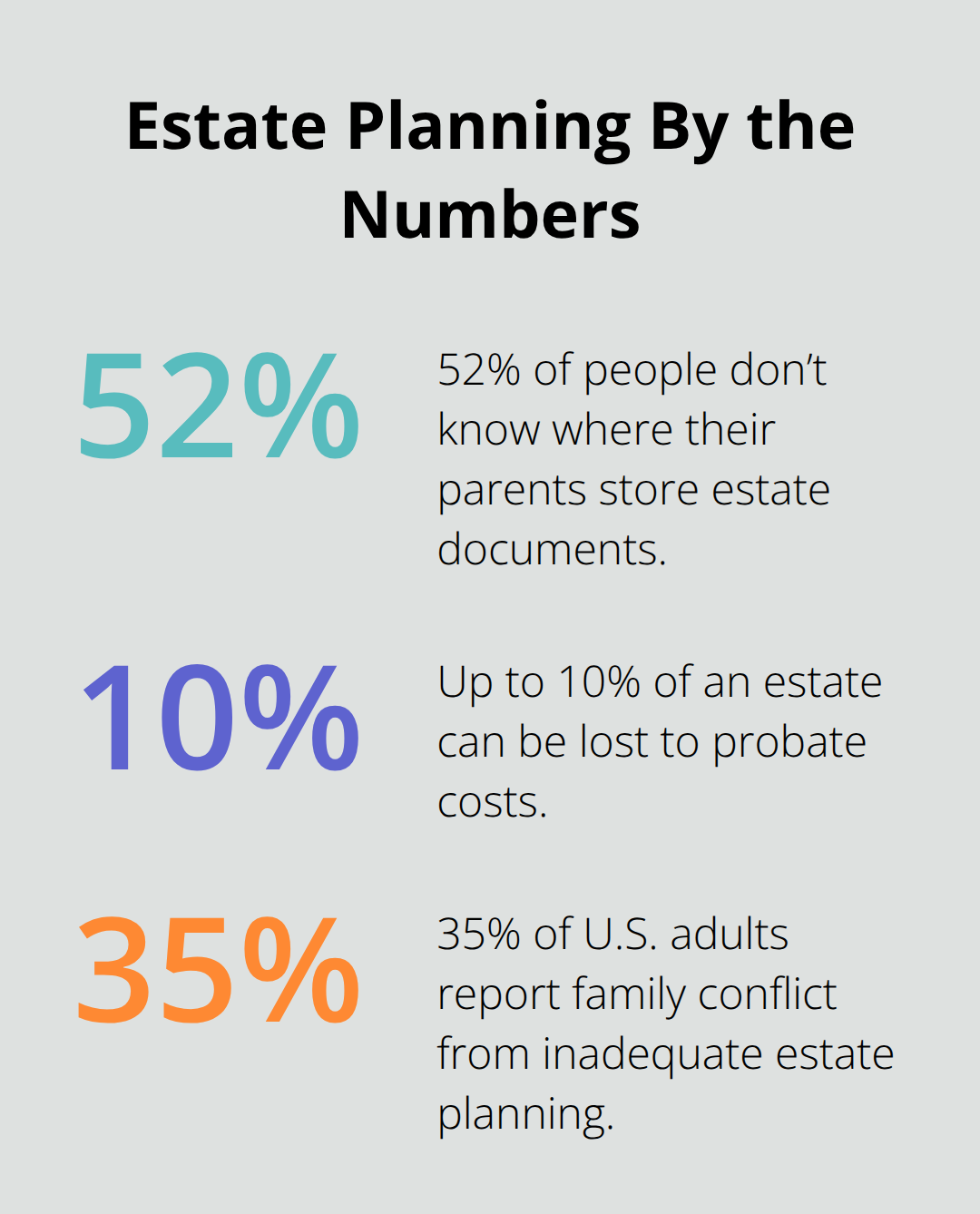

Your estate plan starts with a will, but that document alone leaves critical gaps. A will only controls assets in your name at death and requires probate court approval, which takes months or years and costs up to 10% of your estate according to Vanilla research. The real protection comes from layering multiple documents that work together. Without this foundation, your executor cannot act effectively, and your family faces unnecessary delays and expenses.

Living Trusts and Asset Protection

A living trust holds your major assets and bypasses probate entirely, letting your successor trustee distribute property immediately after you pass away without court involvement. This matters most if you own property in multiple states or have substantial assets, since each out-of-state property would otherwise require separate probate proceedings. The trustee manages the trust without court involvement, which speeds up settlement and protects privacy. This distinction matters significantly when you plan your estate structure.

Powers of Attorney: Control Before and After

Powers of attorney are equally vital but often overlooked. A financial power of attorney lets someone manage your accounts and property if you become incapacitated before death, while a healthcare power of attorney designates who makes medical decisions if you cannot. Without these documents, your family faces court-ordered guardianship proceedings that cost thousands of dollars and eliminate your control over who decides your care. An advance healthcare directive goes further by documenting your specific treatment preferences for end-of-life scenarios, so your medical team and family know your wishes without guessing.

Beneficiary Designations and Account Management

Beneficiary designations on retirement accounts, life insurance policies, and payable-on-death bank accounts override your will entirely, which means outdated designations can send money to an ex-spouse or deceased person instead of your intended heirs. According to Vanilla, 52% of people don’t know where their parents store estate documents, creating chaos when they’re needed most. Your executor cannot act effectively without knowing where these documents live. The practical approach is gathering everything into one secure location with clear instructions.

Organizing and Maintaining Your Documents

Create a detailed asset inventory listing all assets (bank accounts, investments, real estate, vehicles, life insurance), liabilities (mortgages, credit cards, loans), and account numbers. Include funeral or memorial preferences and consider prepaying arrangements to spare your family that burden during grief. Store originals in a home safe or safe-deposit box and share the location with your executor and attorney. Digital storage with secure login details works for copies, but originals need physical security. Life changes demand immediate updates. Marriage, divorce, retirement, financial growth, or the birth of children should all trigger a review of your entire plan, since outdated documents can contradict your current wishes and create legal confusion. Annual reviews at minimum work best, particularly if tax laws or your circumstances shift significantly. Without this layered approach, your executor faces impossible obstacles, your family endures probate delays, and your assets may distribute contrary to your actual wishes-which is why the next step involves understanding how to protect your family through strategic planning decisions.

How to Protect Your Wealth and Reduce What Your Family Loses

Three Major Threats to Your Estate

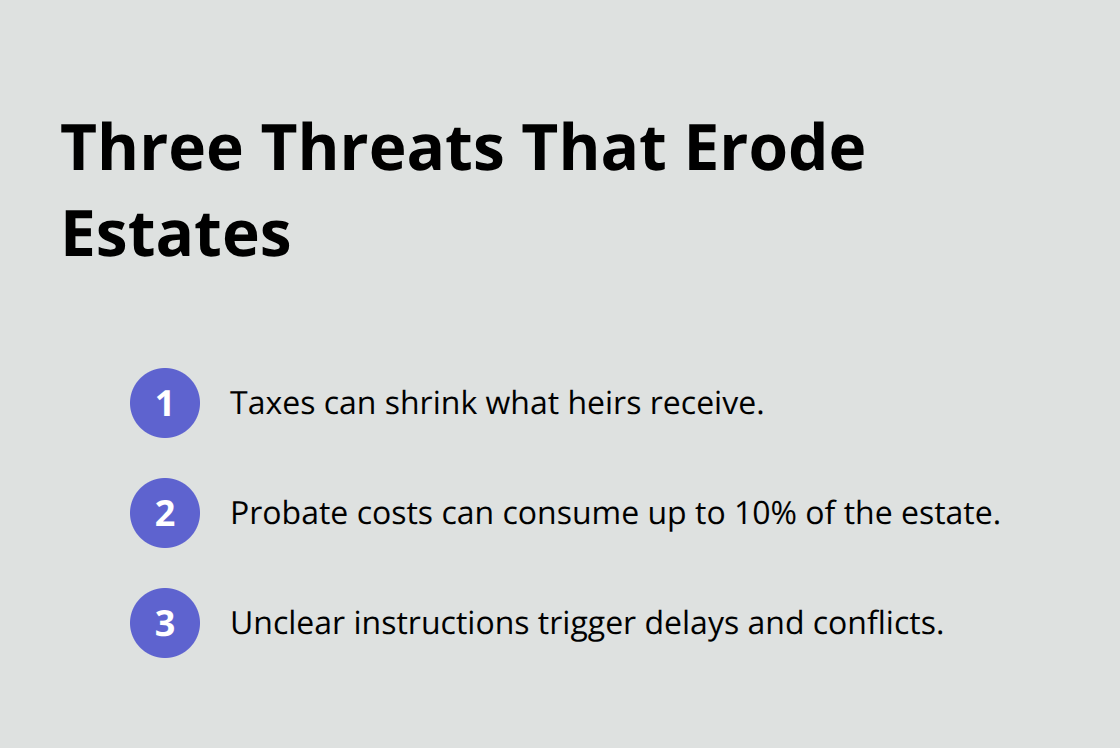

Your estate faces three major threats after you pass away: taxes that shrink your legacy, probate costs that can consume up to 10 percent of everything you own according to Vanilla research, and unclear instructions that force your executor to make guesses about your intentions. The good news is that each threat has a direct solution, and most require nothing more than decisions you make today.

Understanding Tax Exposure and Planning Strategies

Tax planning starts with understanding what actually gets taxed. Federal estate taxes only apply to estates exceeding 13.61 million dollars in 2024, so most families avoid federal tax entirely. However, state-level estate taxes and inheritance taxes hit much lower thresholds in some jurisdictions, and even modest estates face capital gains taxes on inherited property if beneficiaries sell assets shortly after receiving them.

The three-year rule presents a specific tax strategy worth understanding: transfers you make within three years of death get pulled back into your taxable estate, so moving assets outside this window preserves tax advantages for your heirs. Strategic gifting during your lifetime reduces your taxable estate while you see your loved ones benefit from the money directly. Life insurance structured properly can cover estate taxes without forcing your executor to sell family property or business assets to pay the bill.

Avoiding Probate Delays and Costs

A living trust funded with your major assets bypasses probate court entirely, which eliminates the court fees, attorney costs, and months of waiting that drain your estate. According to NOLO, probate can stretch across multiple years for complex estates, during which time your beneficiaries cannot access their inheritance and your executor shoulders substantial administrative burden.

If you own property in multiple states, a living trust avoids the expense and complexity of separate probate proceedings in each state by consolidating everything under one trustee’s management. This single document structure prevents your family from facing repeated court filings and legal fees across different jurisdictions.

Creating Clear Instructions to Prevent Family Conflict

Clear instructions matter as much as the documents themselves. Your executor cannot distribute assets wisely without knowing your specific wishes about who receives what, when they receive it, and under what conditions. A detailed letter of intent accompanying your will and trust prevents disputes over heirloom distribution and clarifies your reasoning behind unequal bequests, which heads off family conflict before it starts.

Beneficiary designations on retirement accounts and life insurance must match your current wishes, since outdated designations override your will regardless of what you actually wanted. According to Vanilla research, 35 percent of U.S. adults report that family conflict arose from inadequate estate planning, and most of that conflict stems from confusion about what the deceased actually intended. Your executor cannot act effectively without knowing where documents live and what your specific intentions are for each asset.

Final Thoughts

Building a solid executor estate planning strategy requires more than downloading templates online. The documents matter, but the real protection comes from decisions you make now about who manages your affairs, how assets transfer to your heirs, and what instructions guide those decisions. Without professional guidance, gaps emerge that cost your family thousands in probate fees, create family conflict over unclear intentions, and delay access to inheritance during grief.

We at Law Offices of Roshni T. Desai understand that estate planning feels overwhelming when you handle it alone. Over 25 years, we have helped families across Southern California navigate wills, living trusts, powers of attorney, and probate administration with straightforward guidance that explains your options in plain language. Ms. Desai’s dual background as both an attorney and real estate professional means we streamline property-related transactions within your estate, reducing costs and delays that typically bog down administration.

Schedule a free consultation with Law Offices of Roshni T. Desai to discuss your circumstances, your assets, and your concerns about what happens after you’re gone. We offer flexible home or office visits so you can meet on your terms. Your family deserves clarity, not confusion, and your executor needs instructions, not guesswork.