Probate Tax Considerations: What It Means for Your Estate

Probate tax considerations often catch families off guard, especially when they realize how much of an estate can go to taxes instead of heirs. At Law Offices of Roshni T. Desai, we’ve seen firsthand how proper planning makes the difference between preserving wealth and watching it disappear.

This guide walks you through the taxes that apply to estates, the mistakes people make, and the strategies that actually work to protect your assets for the people you care about.

What Taxes Actually Apply to Your Estate

Three Tax Obligations That Catch Families Off Guard

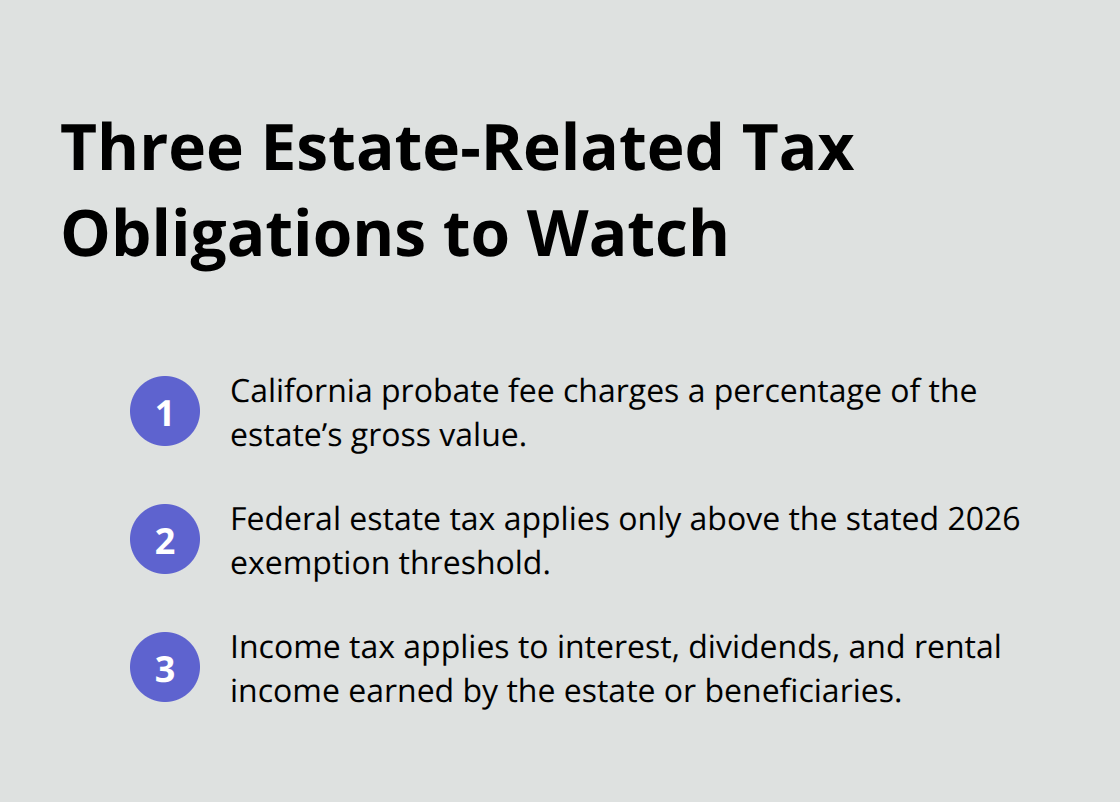

Probate in California triggers three separate tax obligations that most people never anticipate until it’s too late. The first is the California probate fee, which isn’t technically a tax but functions like one-the court charges a percentage of the estate’s gross value, starting at 4% for the first $15,000 and decreasing incrementally for larger estates. For a $500,000 estate, you face roughly $13,000 in probate fees alone. Second is the federal estate tax, which applies only to estates exceeding $15 million in 2026 according to IRS guidance, though this threshold drops significantly after 2025 unless Congress acts. Third is income tax on assets the estate produces after death-interest, dividends, and rental income all remain taxable to the estate or beneficiaries.

California itself has no state estate or inheritance tax, which is a genuine advantage compared to states like Oregon with $1 million exemptions or Maryland with both estate and inheritance taxes. This regional difference shapes how much your heirs ultimately receive.

The Stepped-Up Basis Rule Changes Everything

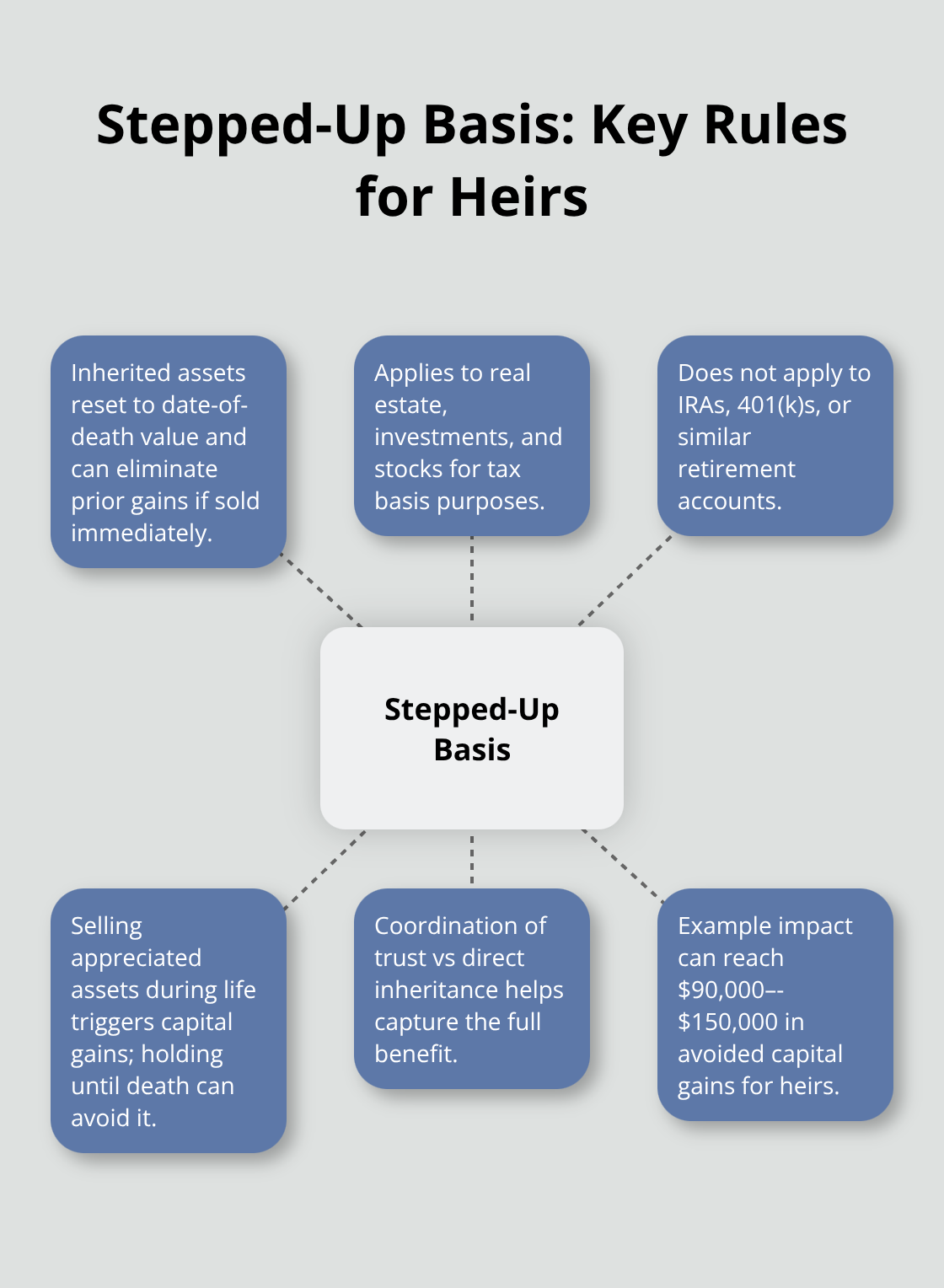

The real trap most families fall into is overlooking the stepped-up basis rule, which gives inherited assets a new valuation at the date of death. If your parent bought a house for $200,000 and it’s worth $800,000 when they die, your heir receives that $800,000 valuation as their starting point-meaning if they sell immediately, no capital gains tax applies to that $600,000 increase. This advantage applies to real estate, investments, and stocks; it does not apply to IRAs, 401(k)s, or retirement accounts, which retain their original tax-deferred status and create a completely different tax problem for heirs.

How Your Estate’s Size Determines What You Actually Owe

Estate value is the deciding factor in whether your family pays taxes at all. Estates under $15,000 in Virginia avoid probate tax entirely-anything larger triggers that 10-cent-per-$100 rate. In California, the probate fee structure means a $100,000 estate pays roughly $1,300, while a $1 million estate pays approximately $14,000. The federal exemption of $15 million per person in 2026 sounds generous until you factor in that rising home values and investment accounts can push ordinary middle-class estates over state thresholds faster than expected.

A married couple with a $3 million home, $500,000 in retirement accounts, and $700,000 in investments sits at $4.2 million-still below the federal limit but potentially exposed to state taxes in jurisdictions with lower thresholds. The math matters because taxes are calculated on the gross estate before any deductions, meaning debts, mortgages, and administration costs don’t reduce the tax base.

Asset Titling and Beneficiary Designations as Your First Defense

Property held in joint tenancy with survivorship or accounts with named beneficiaries bypass probate entirely and avoid these fees. This is why proper titling of assets and beneficiary designations function as your first line of defense. Delaying planning decisions costs real money; the difference between a family that acts now and one that waits five years could easily exceed $10,000 to $50,000 depending on asset growth and tax law changes.

Understanding these three tax layers and how your estate’s size triggers them sets the foundation for the strategies that actually reduce what your heirs owe. The next section walks you through the specific approaches that work-from trusts to gifting strategies to leveraging federal exemptions-so you can move forward with confidence.

How to Cut Probate Taxes Down to Size

Revocable Living Trusts: The Foundation of Tax-Efficient Planning

Revocable living trusts stand as the single most effective tool for California families because they accomplish what probate fees prevent: complete bypass of court involvement and the 4% fee structure that costs $13,000 on a $500,000 estate. When you fund a revocable living trust properly-meaning you retitle real estate, brokerage accounts, and other assets into the trust’s name during your lifetime-those assets transfer directly to beneficiaries at death without touching probate. You create the trust document, transfer ownership of assets into it, and name yourself as trustee while you’re alive and able to manage everything. At death, your successor trustee distributes assets according to your instructions, typically completing the process within weeks rather than the months or years probate demands. California law allows you to maintain complete control and modify the trust anytime before death, making this approach far less restrictive than people assume.

The tax advantage compounds because avoiding probate also means avoiding the income tax on assets the estate would generate during a lengthy probate timeline-a hidden cost that can add thousands more depending on account balances and dividend income. Working with a trust administration attorney can compress your timeline from 18 to 24 months down to six months or less by coordinating appraisals, tax filings, and asset transfers efficiently.

Annual Gifting: Transferring Wealth Tax-Free

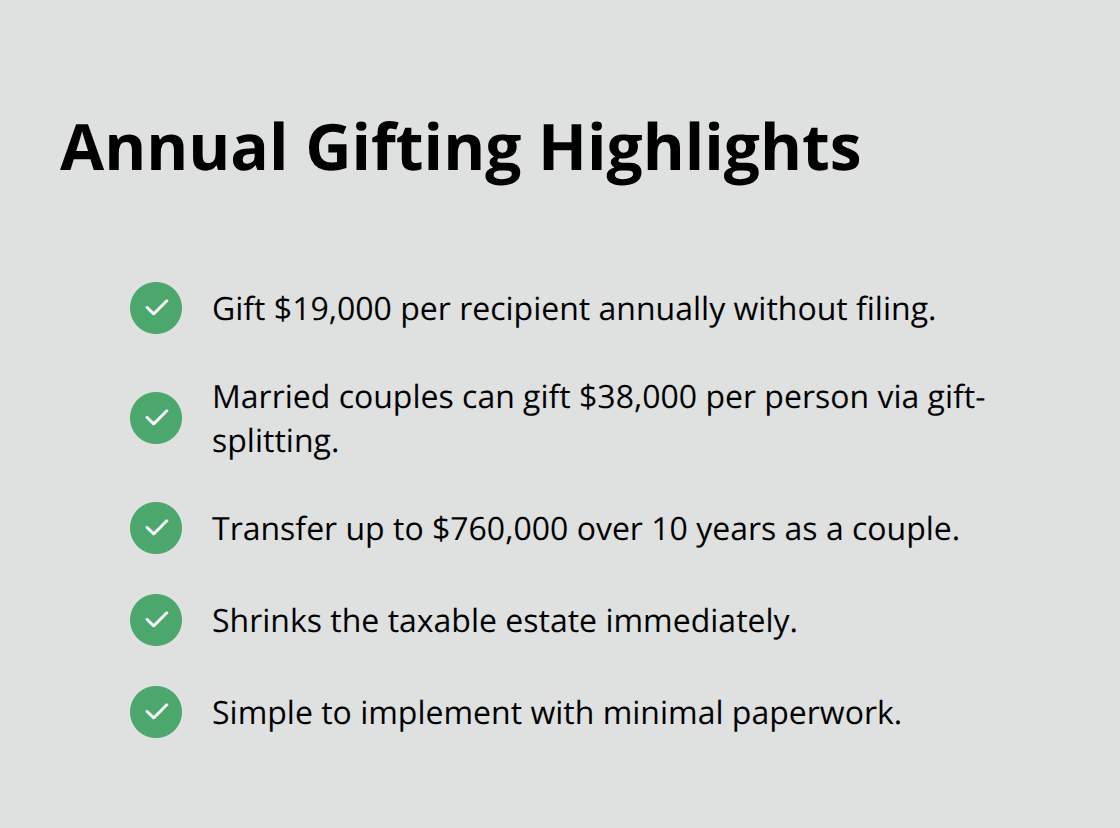

Lifetime gifting strategies work alongside trusts to permanently reduce what gets taxed at death. The IRS allows you to gift $19,000 per recipient annually without filing paperwork or reducing your lifetime exemption, and married couples can double this to $38,000 per person per year through gift-splitting. Over a decade, a married couple can transfer $760,000 to children tax-free, which means that money grows outside the taxable estate and never triggers federal estate tax.

This approach requires no complex paperwork and produces immediate results in shrinking your taxable estate.

Education Savings and Accelerated Gifting Options

For education funding specifically, 529 plans offer an accelerated gifting option under IRS rules: you can contribute up to $95,000 per beneficiary using a five-year election without gift tax, letting you front-load education savings while shrinking estate value. The SECURE 2.0 Act, effective in 2024, added another option-you can now transfer up to $35,000 from a 529 plan into a Roth IRA for the beneficiary after 15 years of account ownership, combining education savings with tax-free retirement growth. These tools let you accomplish multiple goals simultaneously: funding education, reducing your estate, and building tax-free retirement accounts for the next generation.

Charitable Giving as an Estate Reduction Strategy

Charitable giving delivers similar estate reduction benefits: assets left to qualified charities are deducted from your gross estate dollar-for-dollar, and donations made during life can generate immediate income tax deductions while lowering the estate’s taxable value. This strategy works particularly well for families with substantial charitable interests because it aligns your values with your tax planning.

When These Strategies Matter Most

The federal exemption of $15 million per person in 2026 sounds enormous until you calculate that a married couple with substantial real estate, investment accounts, and retirement savings can easily approach or exceed $4 million to $5 million-still below the federal threshold but enough to justify strategic gifting that reduces what’s left for taxation if circumstances change or Congress alters exemption amounts after 2025. These strategies also protect your family if state-level tax laws shift or if your estate grows faster than you anticipated. The next section addresses the mistakes families make when they fail to implement these approaches and what happens when tax planning gets delayed.

Mistakes That Cost Families Thousands

Underestimating Your Estate’s Growth and Tax Exposure

The gap between knowing you should plan and actually planning creates the biggest financial damage. Most families understand trusts and gifting exist, but they operate under false assumptions that delay action until circumstances force rushed decisions. One of the most expensive mistakes is assuming that because California has no state estate tax, you don’t need to worry about taxes at all. This reasoning ignores federal estate tax thresholds and overlooks that your estate value climbs faster than you realize through home appreciation and investment growth. A $2 million estate today becomes $3 million in eight years if property values rise 5% annually and investment accounts compound at historical averages. At that point, your taxable estate sits dangerously close to thresholds in states with lower exemptions if you own property outside California, or it approaches the federal limit if Congress doesn’t extend the current $15 million exemption past 2025. Families who assume they’re too small to worry about taxes often discover during probate that they owed significant amounts they never anticipated.

Missing the Stepped-Up Basis Opportunity

The second critical mistake involves treating the stepped-up basis rule as passive rather than as an opportunity to structure your estate strategically. Many people know inherited assets receive a new valuation at death, but they fail to coordinate which assets should transfer through trusts versus which ones your heirs should inherit directly to capture this advantage. Selling appreciated assets during your lifetime triggers capital gains tax immediately, while holding them until death lets heirs inherit at stepped-up value with no tax consequence. The difference is substantial: if you hold appreciated stock worth $600,000 more than you paid for it, selling it yourself means capital gains tax on that $600,000 at your long-term rate, potentially $90,000 to $150,000 depending on your income bracket. Your heirs inherit the same stock at stepped-up basis and owe nothing if they sell immediately.

This rule doesn’t apply to retirement accounts like IRAs or 401(k)s, which remain tax-deferred and create the opposite problem for heirs who face income tax on withdrawals.

The Cost of Waiting Until It’s Too Late

Waiting to address these decisions until a few months before death or after diagnosis guarantees you miss these opportunities entirely. Rushed planning under time pressure produces costly mistakes that lock in inefficient tax outcomes for decades. The mistake isn’t holding appreciated assets; it’s failing to coordinate your strategy while you still have time to modify it. Understanding how trust administration works helps you address these decisions while you can still adjust your approach, preventing the tax inefficiencies that rushed planning creates. Your estate’s structure determines whether your heirs capture stepped-up basis advantages or whether they inherit accounts that trigger immediate income tax obligations-a distinction that costs tens of thousands of dollars depending on your asset composition.

Final Thoughts

The probate tax considerations you face depend entirely on decisions you make now, while you still control the outcome. Waiting for a crisis or relying on generic advice costs families tens of thousands of dollars in unnecessary taxes and delays. We at Law Offices of Roshni T. Desai understand that estate planning feels overwhelming when you’re juggling work, family, and daily responsibilities, which is why personalized guidance makes the difference between a plan that actually protects your wealth and one that sits incomplete on your to-do list.

Creating a tax-efficient plan requires coordinating multiple moving pieces: trust structure, asset titling, beneficiary designations, gifting strategies, and retirement account treatment all interact to determine what your heirs ultimately receive. A professional who understands California probate law, federal estate tax rules, and your specific asset composition can identify opportunities you’d miss on your own. The stepped-up basis advantage, annual gifting limits, and trust funding strategies only work if you implement them correctly and coordinate them with your overall financial picture.

Your estate strategy isn’t static-property values change, tax laws shift, family circumstances evolve, and your financial situation grows or contracts over time. Regular reviews every three to five years catch these changes before they create problems, and taking action now preserves options you lose by waiting. Contact Law Offices of Roshni T. Desai to discuss your probate tax considerations and move forward with confidence.