Living Trust Administration: Keep Your Family’s Assets in Sync

A living trust administration requires careful attention after you pass away. Without proper management, families often face missed deadlines, tax complications, and costly mistakes.

We at Law Offices of Roshni T. Desai help families navigate this process smoothly. This guide walks you through what happens to your trust and how to avoid the pitfalls that derail many families.

What Happens After Your Living Trust Takes Effect

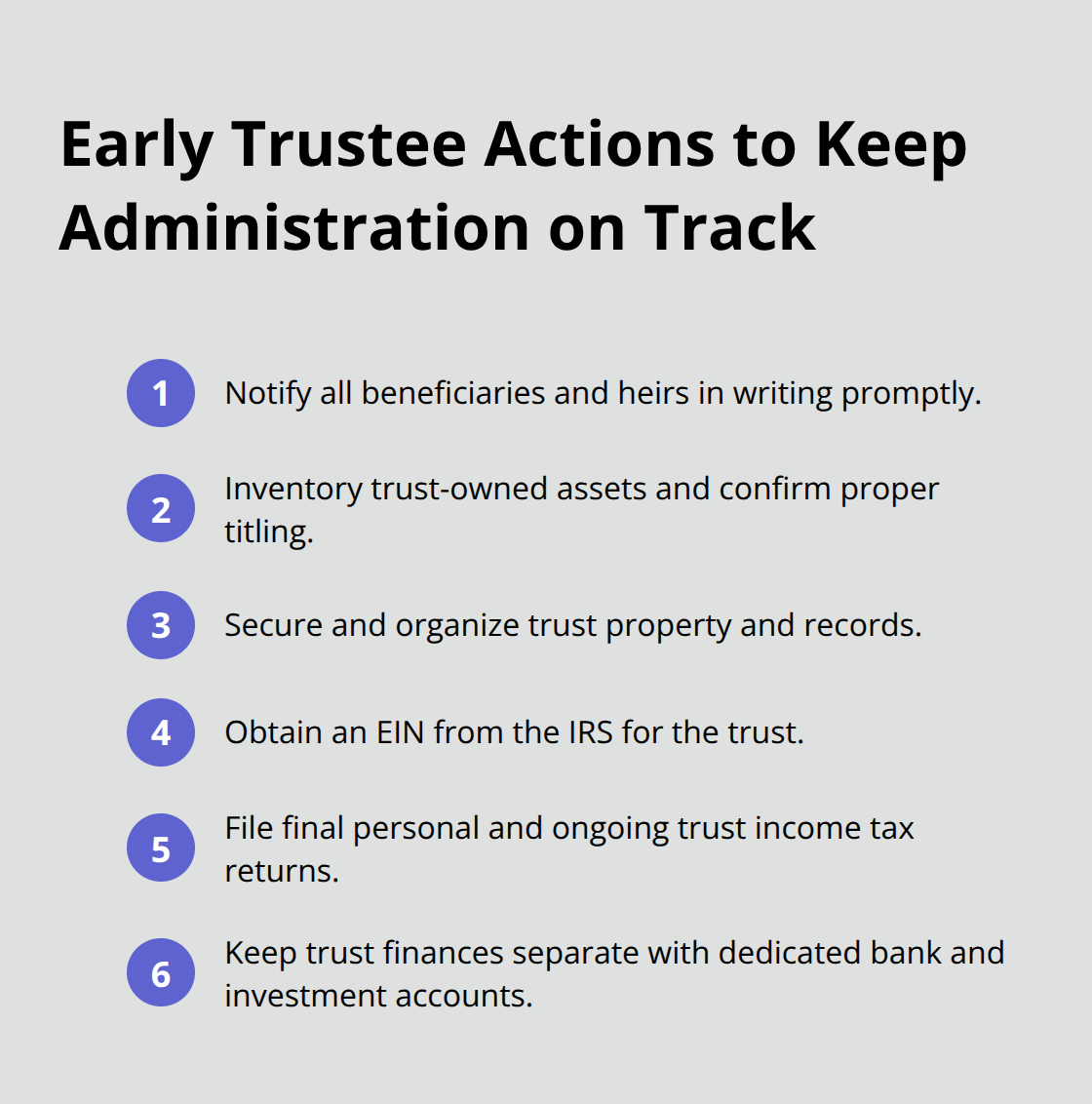

When you pass away, your living trust immediately becomes irrevocable, meaning no one can change its terms. The successor trustee you named steps into control without waiting for court approval-this is the core advantage that separates trusts from wills. Your successor trustee’s first job is to notify all beneficiaries and heirs that the trust has become irrevocable and that they need to know what comes next.

This notification must happen promptly; delays create anxiety and breed suspicion among family members.

Identifying and Inventorying Trust Assets

The trustee inventories everything the trust owns by identifying which assets were properly transferred into the trust during your lifetime and which assets remain outside it. This distinction matters enormously because assets not titled in the trust’s name may still require probate, defeating part of the trust’s purpose. According to the American Bar Association, the most common and costly mistake families make is creating a trust but failing to fund it-signing the document means nothing if your house, bank accounts, and investment portfolio still sit in your personal name.

Handling Tax Obligations and Deadlines

Your successor trustee must obtain a tax identification number from the IRS and file final income tax returns for you personally, plus ongoing trust tax returns if the trust generates income. These deadlines are strict; missing them triggers penalties and interest that reduce what beneficiaries ultimately receive. The trustee cannot distribute assets to beneficiaries until these tax obligations are addressed and documented.

Managing Assets and Settling Debts

Your trustee now controls all trust-held property and must keep it organized and secure. The trustee collects your mail from your residence and files a change-of-address to uncover any debts, creditors, or liabilities you may have left behind. The trustee pays your final bills, outstanding debts, and any taxes owed from trust assets before distributing anything to beneficiaries.

Establishing Fair Market Values for Distribution

For assets of significant value, the trustee often orders appraisals to establish fair market values-this step is critical if beneficiaries are supposed to receive equal amounts but the trust holds a mix of real estate, securities, and personal property. If you designated specific percentages rather than specific assets to different beneficiaries, the trustee must know exact values to divide everything fairly. The trustee operates without court supervision in most cases, which keeps the process private and typically faster than probate, but this freedom also means the trustee bears full responsibility for accuracy and compliance. Once the trustee completes these foundational steps, the actual distribution process begins-and this is where many families encounter their second major challenge.

Where Trust Administration Goes Wrong

Notifying Beneficiaries Promptly Prevents Family Conflict

Trust administration crumbles when families delay notifying beneficiaries. The trustee must send written notice to all beneficiaries and heirs as soon as the trust becomes irrevocable-California law requires this notification to happen promptly. Many families wait weeks or months, thinking they will communicate once everything is organized. This silence breeds resentment and suspicion. Beneficiaries who do not hear from the trustee assume something is hidden or mismanaged, even when the trustee is working diligently behind the scenes. A straightforward letter explaining the trustee’s role, timeline expectations, and next steps prevents most family conflict. Failing to notify quickly transforms a straightforward administration into a minefield of hurt feelings and legal demands.

Keeping Trust Finances Separate From Personal Accounts

Mixing personal and trust finances is the second major failure point. The trustee must maintain separate bank accounts and investment accounts for the trust-never commingling trust money with the trustee’s personal funds or other estates. When a trustee deposits trust income into a personal checking account or uses a personal credit card for trust expenses, the IRS views this as sloppy record-keeping at best and fraud at worst. The trustee cannot prove which transactions belonged to the trust versus personal spending, which invites audit risk and beneficiary lawsuits. More practically, this sloppiness makes it impossible to file accurate tax returns. The trust’s income tax return requires a clear accounting of all trust revenues and expenses; muddled accounts prevent the trustee from completing this filing correctly. If the trustee collected $15,000 in rental income but spent trust money on personal bills, no one can untangle what actually belongs to the trust. The IRS can assess penalties on unreported income, and beneficiaries can sue the trustee for breach of fiduciary duty. Opening a dedicated trust bank account costs nothing and takes thirty minutes. Not doing it costs thousands in corrections, penalties, and legal fees later.

Tax Deadlines Are Non-Negotiable

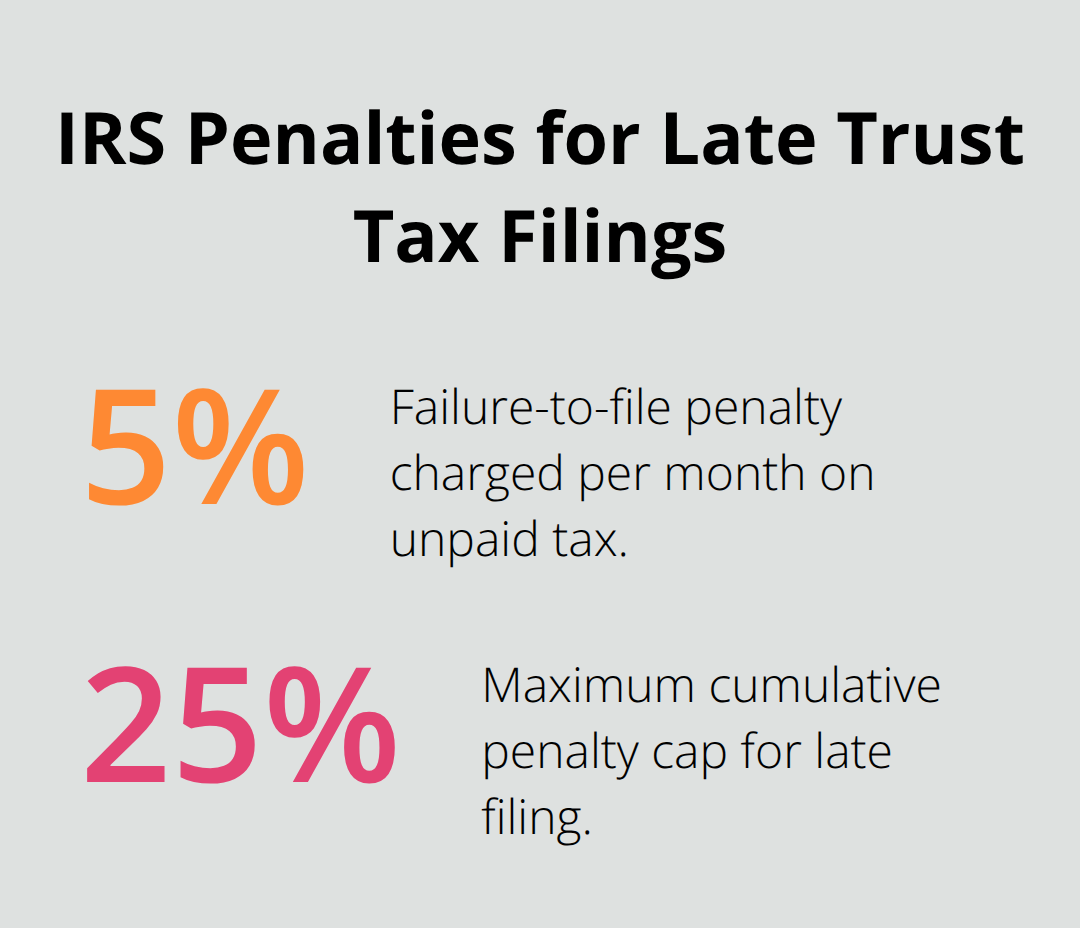

Tax filing deadlines for trusts operate on strict calendars with no flexibility. The trustee must obtain an EIN from the IRS within sixty days of the grantor’s death, file the final personal income tax return by April 15 of the following year, and file the trust’s income tax return by April 15 if the trust generates income during the administration period. Missing these deadlines triggers automatic penalties-the IRS assesses a failure-to-file penalty of five percent per month up to twenty-five percent of the unpaid tax, plus interest that compounds daily. A trustee who misses the trust’s tax filing deadline by three months faces penalties that can exceed what a beneficiary receives in distribution.

These deadlines do not wait for the trustee to feel ready or for family disagreements to resolve. The trustee should contact a CPA or tax professional immediately after the grantor’s death to map out the filing calendar. Waiting until summer to address taxes guarantees missed deadlines and unnecessary penalties that reduce what beneficiaries ultimately receive from the estate.

Moving Forward With Professional Support

The complexity of trust administration-from asset inventories to tax filings to beneficiary distributions-demands coordination across multiple professionals. A trustee attempting to navigate these steps alone often stumbles on one or more of these common mistakes. We at Law Offices of Roshni T. Desai work with families to handle the trustee duties, manage beneficiary communications, and address tax and legal compliance issues that trip up so many families. The next section walks through how professional guidance transforms trust administration from a source of family stress into a manageable process.

How Professional Guidance Transforms Trust Administration

Trust administration involves three interconnected responsibilities that most families cannot manage alone: handling the trustee’s fiduciary duties while managing assets, communicating with beneficiaries about timelines and distributions, and meeting tax filing requirements that carry automatic penalties for missed deadlines. A trustee who attempts this work independently often succeeds at one task while failing at another-for example, distributing assets to beneficiaries on schedule but neglecting to file the trust’s income tax return, which then triggers IRS penalties that reduce what beneficiaries ultimately receive.

The Coordination Problem Trustees Face Alone

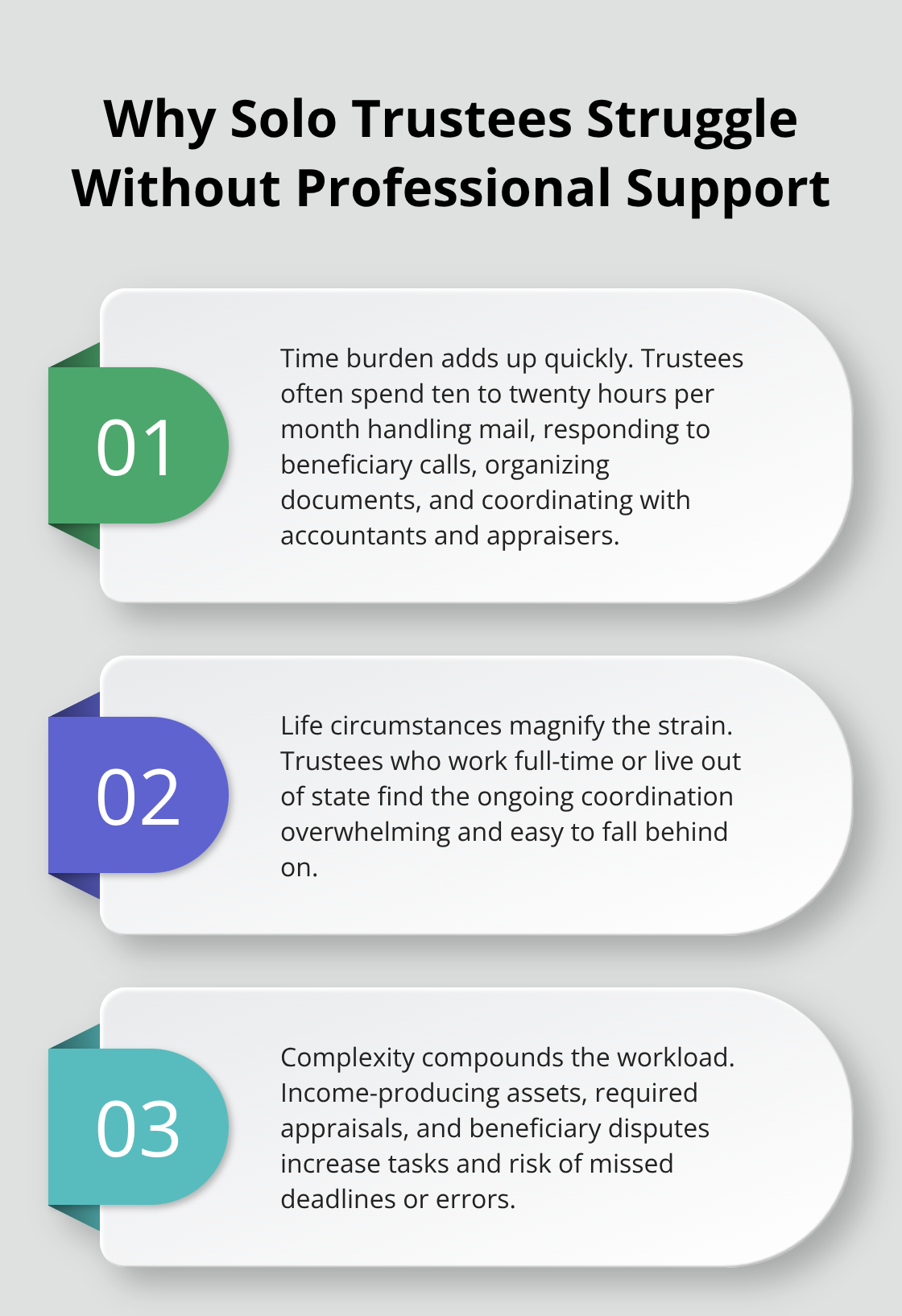

The coordination problem is real. The trustee must inventory assets, establish fair market values through appraisals, obtain a tax identification number from the IRS, file final personal income tax returns and ongoing trust tax returns, maintain separate trust bank accounts, notify beneficiaries in writing, answer beneficiary questions about distributions, settle debts and taxes, and finally distribute assets according to the trust terms. Each step has specific deadlines and legal requirements. Trust administration requires careful attention to detail and knowledge of California’s specific legal requirements. Filing the trust’s income tax return late triggers penalties of five percent per month up to twenty-five percent of unpaid tax, plus daily compounding interest. Distributing assets before debts and taxes are settled exposes the trustee to personal liability if creditors later come forward.

Why Trustee Duties Demand Professional Support

The practical reality is that trustee duties demand constant attention across months or sometimes years, especially if the trust holds real estate, investment accounts, or ongoing business interests. A trustee managing this work alone typically spends ten to twenty hours per month on administration tasks-reviewing mail, responding to beneficiary calls, organizing documents, and coordinating with accountants and appraisers. For families where the trustee also works full-time or lives out of state, this burden becomes overwhelming. The workload compounds when the trust generates income, requires property appraisals, or involves disputes among beneficiaries about distributions.

How Professional Coordination Reduces Stress

Professional guidance transforms trust administration by creating a clear administration timeline, coordinating with CPAs and tax professionals to meet every filing deadline, maintaining proper documentation for IRS and beneficiary review, and guiding the trustee through each distribution decision so nothing falls through the cracks. We at Law Offices of Roshni T. Desai work with families to handle these responsibilities directly or work alongside the trustee to divide the workload. We maintain the trust’s separate bank accounts and investment accounts, prepare detailed accountings that show exactly where every dollar came from and where it went, communicate with beneficiaries on a regular schedule so they understand what is happening and when distributions will arrive, coordinate with tax professionals to file returns on time, and address any creditor claims or tax disputes that arise.

What Families Experience With Professional Support

This approach keeps the trustee informed and involved without requiring the trustee to manage every detail. Families often report that having this support transforms their experience from months of stress and confusion into a manageable process where they know exactly what to expect and when. The trustee no longer juggles competing deadlines or worries about missing a filing requirement that triggers penalties. Beneficiaries receive regular updates instead of silence, which prevents the resentment and suspicion that derail so many administrations. The trust’s assets remain properly documented and separate from personal finances, which protects the trustee from liability and simplifies the final accounting to beneficiaries.

Final Thoughts

Living trust administration protects your family’s financial stability when a trustee manages assets properly, meets tax deadlines, and keeps beneficiaries informed throughout the process. A trustee working alone often misses critical filing requirements or delays notifications, which triggers penalties and resentment that reduce what your family ultimately receives. Professional support transforms this complex coordination into a manageable process where deadlines stay on track, documentation remains organized, and beneficiaries understand exactly what to expect.

The difference between smooth administration and costly chaos comes down to whether the trustee has guidance navigating asset management, beneficiary communications, and tax compliance together. We at Law Offices of Roshni T. Desai help families establish clear timelines, meet every filing deadline, and maintain proper documentation so your living trust administration works as intended. Contact us to schedule a free consultation and discuss how we can support your family’s financial stability through proper trust administration planning.