Proactive Trust Administration Attorney: Preventing Problems Before They Arise

Trust disputes drain families emotionally and financially. Most of these conflicts stem from preventable issues like unclear documents, poor communication, and inadequate planning.

We at Law Offices of Roshni T. Desai believe that working with a proactive trust administration attorney before problems emerge saves families thousands in litigation costs and preserves relationships. This guide shows you how.

What Derails Trust Administration

Vague trust language creates immediate problems when trustees execute distributions. A trust that says “distribute to beneficiaries in the trustee’s sole discretion” without defining what triggers distributions or how much each person receives invites conflict. Trustees second-guess their own decisions, beneficiaries question every action, and what should take months stretches into years of back-and-forth arguments. The Florida Trust Code requires trustees to provide accountings to beneficiaries, but vague instructions make those accountings hard to defend. Original documents often lack specifics on whether a beneficiary’s disability affects their share, whether distributions happen at certain ages, or what happens if a beneficiary dies before receiving their inheritance. These gaps force trustees to make judgment calls that feel arbitrary to family members watching from the sidelines. The cost of clarifying one ambiguous clause through mediation or litigation routinely exceeds several thousand dollars-money that should have gone to beneficiaries instead.

Trustee Actions That Trigger Disputes

Mismanagement occurs when trustees fail to separate personal finances from trust assets, fail to keep detailed records of transactions, or fail to invest trust money prudently. A trustee who deposits trust funds into a personal checking account violates fiduciary duty, even if they intend no wrongdoing. A trustee who avoids communicating with beneficiaries about distributions, tax filings, or account performance plants seeds for suspicion. Orange County Superior Court Probate Division data shows trust litigation is common in Southern California, with many cases stemming from trustee inaction rather than intentional misconduct. The trustee simply did not understand their obligations under California Probate Code rules or failed to document their decisions. Beneficiaries then challenge distributions they perceive as unfair, request accountings the trustee cannot produce, or discover that tax obligations went unpaid. Once litigation starts, both sides spend money fighting rather than resolving the underlying problem.

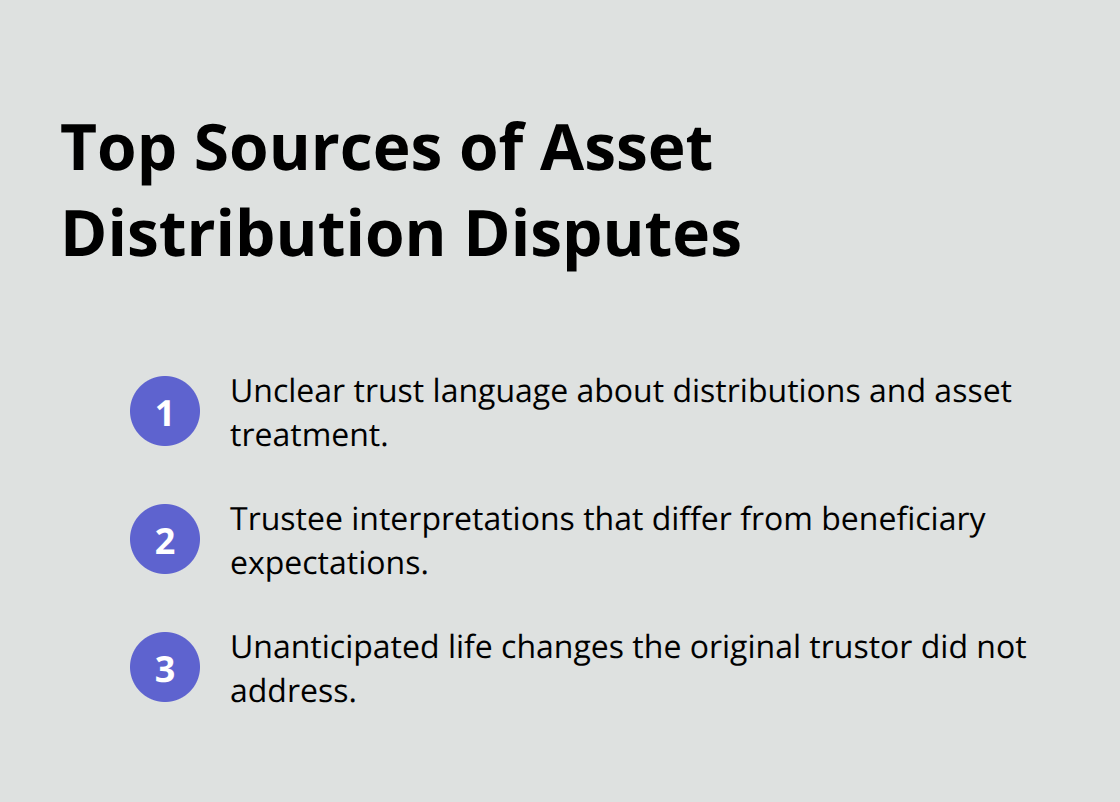

Asset Distribution Disagreements

Disagreements over who gets what stem from three sources: unclear language in the trust document, trustee interpretation that differs from what beneficiaries expected, and life changes the original trustor did not anticipate. A trust written twenty years ago may not address digital assets, cryptocurrency holdings, or significant real estate appreciation.

The trustor may have intended equal distribution among three children but never specified whether equal means equal dollar amounts or equal percentages of the estate. When one child received help with a home down payment during the trustor’s lifetime, should that count against their inheritance? The trust document does not say. These gaps force conversations that feel accusatory even when everyone acts in good faith. Beneficiaries who feel shortchanged hire attorneys, request formal accountings, and sometimes file court challenges. The administration process halts while the dispute plays out. Families fracture over money that should have gone according to clear, written instructions from the start.

These preventable problems-from vague language to poor trustee communication to unaddressed life changes-form the foundation of most trust disputes. The next section shows how proactive legal guidance stops these issues before they damage families and drain trust assets.

How Proactive Legal Guidance Stops Trust Problems

Vague trust documents breed conflict because they force trustees to interpret the trustor’s wishes without clear guidance. A trust attorney reviews your existing documents for gaps before problems surface. They identify where language about distributions, asset management, or beneficiary eligibility leaves room for disagreement. When a trust says nothing about what happens if a beneficiary faces financial hardship or divorce, the trustee has no framework for decisions. A proactive attorney adds specificity: they define distribution triggers, clarify how life changes affect inheritance, and address assets the original trustor never contemplated when the trust was drafted.

Regular reviews every three to five years catch problems early. Life events like remarriage, business sales, significant property appreciation, or changes in tax law all create gaps between what the trust says and what actually needs to happen. California Probate Code requires trustees to follow the trust’s terms precisely, but vague terms make compliance impossible. An attorney helps you amend the trust before administration begins, saving thousands in mediation or litigation costs later.

Selecting Trustees Who Understand Their Obligations

The trustee you choose determines whether administration runs smoothly or descends into conflict. Too many families name someone based on family loyalty without considering whether that person understands financial management, tax obligations, or communication. A trustee who cannot separate personal finances from trust assets, who delays providing accountings to beneficiaries, or who makes investment decisions without documenting their reasoning violates fiduciary duty under California law.

An attorney helps you identify trustee candidates who have the discipline and organization the role demands. They also establish proactive oversight mechanisms: regular check-ins with the trustee, annual accountings provided to beneficiaries, and documentation standards that prevent disputes. If you name a corporate trustee or a family member, that person needs written guidelines about their responsibilities. An attorney creates a trustee instruction letter that spells out expected timelines for distributions, how often accountings should be provided, and what records the trustee must maintain. This prevents the common problem where a well-meaning trustee simply does not understand what beneficiaries are entitled to know.

Creating Accountings That Beneficiaries Understand

Beneficiaries challenge trustee actions when they feel kept in the dark. Open communication channels prevent suspicion from taking root. A trustee who provides annual accountings showing exactly where trust money went, what distributions were made, and what taxes were paid removes the mystery that fuels disputes. California Probate Code mandates accountings, but many trustees provide bare-bones reports that raise more questions than they answer.

An attorney helps trustees create accountings that beneficiaries actually understand: clear descriptions of assets, explanations of investment performance, itemized expense deductions, and distributions listed by date and amount. Trustees should also communicate proactively about decisions. If the trustee decided to hold assets in certain investments rather than sell them, explain why. If distributions will be delayed due to tax filings or creditor claims, tell beneficiaries the timeline upfront. This prevents beneficiaries from imagining the worst and filing formal requests for information or court challenges.

Establishing Communication Schedules That Build Confidence

Trustees who establish regular communication schedules demonstrate competence and good faith throughout administration. Quarterly or semi-annual updates (depending on the trust’s complexity) keep beneficiaries informed without overwhelming them with information. These updates should address account performance, pending distributions, and any decisions the trustee made since the last report.

Proactive communication also addresses concerns before they escalate into formal disputes. When a beneficiary questions a distribution decision or investment choice, the trustee responds promptly with documentation and reasoning. This responsiveness signals that the trustee takes their fiduciary duties seriously and welcomes scrutiny. Beneficiaries who feel heard and informed are far less likely to hire attorneys or file court challenges, allowing the trust administration to proceed efficiently toward the next phase of distributions and final settlement.

What Records Trustees Must Keep and Why

Trustees who maintain meticulous records eliminate the primary source of beneficiary suspicion: the inability to verify where money went and why. A trustee’s detailed accounting should document every transaction from day one, including asset valuations at the time the trust became irrevocable, investment purchases and sales with dates and amounts, all distributions to beneficiaries with dates and purposes, fees paid to professionals, tax filings submitted, and expenses deducted from the trust. Without this documentation, even an honest trustee cannot defend their decisions when a beneficiary questions a distribution or investment choice. Florida Trust Code requires trustees to provide accountings to beneficiaries, but the law does not specify how detailed those accountings must be, leaving room for conflict. A trustee who keeps only bank statements and investment statements without explanatory notes creates a paper trail that looks suspicious even when nothing improper occurred.

The solution is straightforward: establish a record-keeping system before administration starts. Many trustees use spreadsheets or accounting software to track every transaction in real time rather than scrambling to reconstruct records months later. When a beneficiary requests documentation, the trustee produces organized, dated records that show exactly how trust assets were managed and distributed.

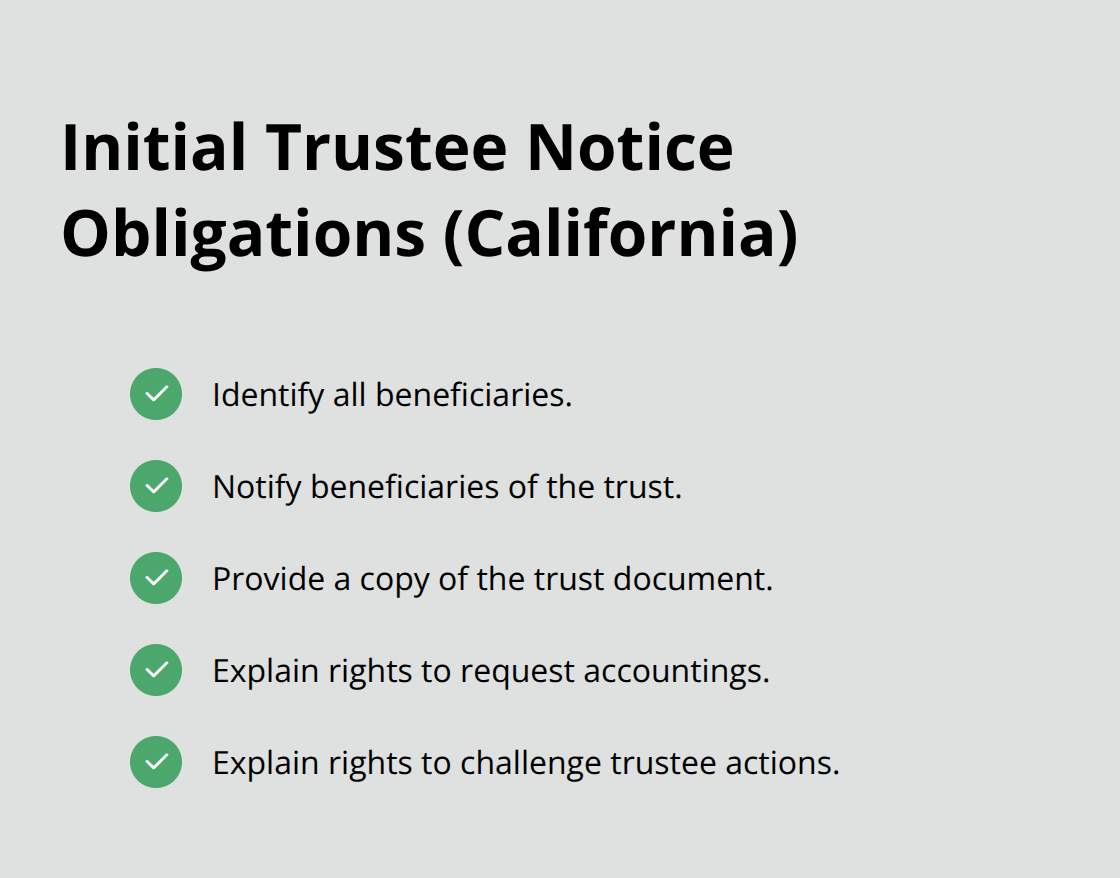

State Laws Require Specific Actions at Specific Times

Trust administration operates under strict timelines set by state law, and missing a deadline triggers costly problems. California Probate Code imposes specific notice requirements that trustees must follow within days or weeks of the trustor’s death. Trustees must identify all beneficiaries, notify them of the trust, provide a copy of the trust document, and explain their rights to request accountings and challenge trustee actions.

Failure to provide proper notice gives beneficiaries grounds to challenge the trustee’s authority or sue for damages.

Tax filing deadlines are equally unforgiving. A trustee who misses the deadline for filing the deceased trustor’s final income tax return or the trust’s first fiduciary income tax return exposes themselves to penalties and interest, reducing the assets available for distribution. Some trustees assume they can file these returns themselves, but trust tax returns involve complicated calculations around income recognition, distribution deductions, and fiduciary deductions that require professional guidance.

The Florida Trust Code and California Probate Code both mandate that trustees follow the trust’s terms exactly, which means understanding what the document requires at each stage of administration. A trustee who delays distributions because they misunderstood the distribution timeline, or who distributes assets prematurely because they did not read the document carefully, violates their fiduciary duty. The practical approach is to have an attorney review the trust document and create a written timeline of required actions, notification deadlines, tax filing dates, and distribution schedules. This prevents the common mistake where a trustee handles some tasks correctly but misses others because they did not realize the trust document required them.

Tax Planning Protects Assets Before Distribution

Trusts created during the trustor’s lifetime often carry income tax consequences that trustees overlook until it is too late to address them efficiently. A revocable living trust does not generate income taxes during the trustor’s life because the trustor is still the owner, but the moment the trustor dies and the trust becomes irrevocable, the trust becomes a separate taxpaying entity. Income earned by trust assets after death gets taxed either to the trust or to the beneficiaries who receive distributions, depending on how the trustee manages cash flow.

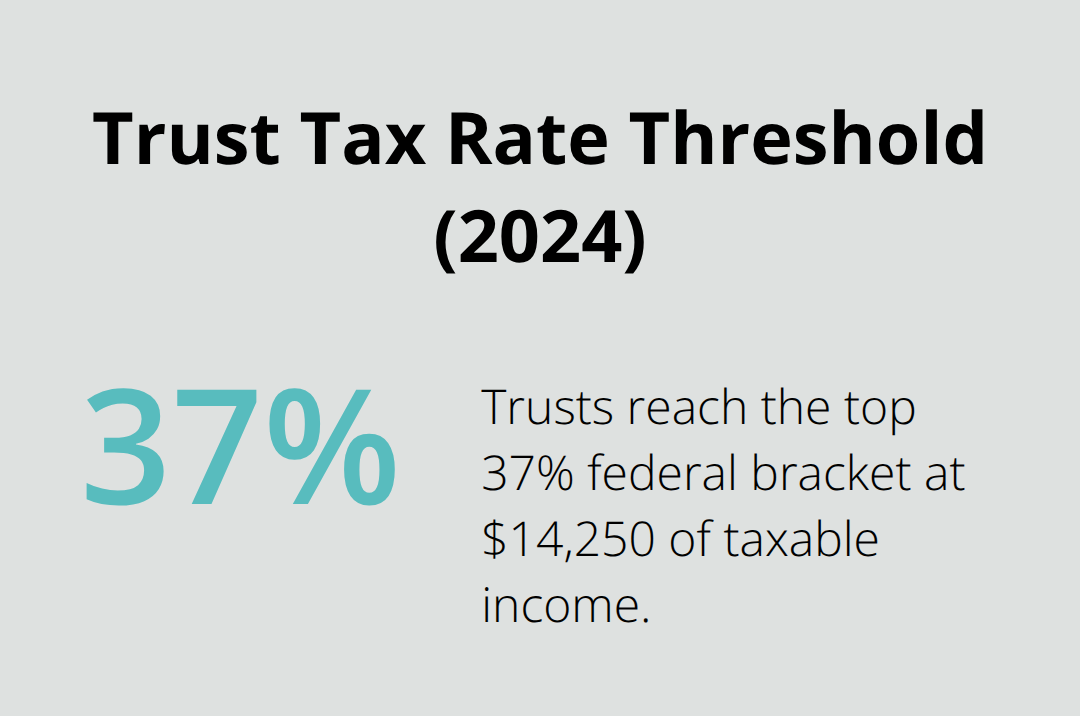

A trustee who distributes income to beneficiaries in the year it is earned shifts the tax burden to those beneficiaries, which may be efficient if they are in lower tax brackets. A trustee who retains income in the trust pays taxes at trust rates, which reach the highest federal rate of 37 percent at just $14,250 of taxable income as of 2024.

This means retaining income in the trust is almost always inefficient from a tax perspective.

The solution requires coordination between the trustee and a tax professional before distributions start. The trustee should work with an accountant or tax attorney to calculate the trust’s taxable income for the year, determine which beneficiaries are receiving distributions, and decide whether distributing income to beneficiaries makes sense. Some trusts also own businesses, real estate, or retirement accounts that trigger additional tax complications. A trustee who inherits a business through the trust must decide whether to continue operating it, sell it, or wind it down-each choice carries different tax consequences. A trustee who discovers the trust is the beneficiary of an IRA or 401k needs guidance on required minimum distributions, which changed significantly under recent federal law. These decisions require professional input, and the cost of getting them right is far less than the tax bill that results from mistakes.

Final Thoughts

Trust disputes cost families tens of thousands of dollars in legal fees and court costs while stretching administration from months into years. A proactive trust administration attorney identifies gaps in your documents before they become disputes and establishes systems for record-keeping, communication, and compliance that prevent the misunderstandings fueling conflict. They help trustees understand their fiduciary obligations, create accountings that beneficiaries trust, and coordinate tax planning so distributions happen efficiently without unexpected tax bills.

We at Law Offices of Roshni T. Desai help families across Southern California avoid trust problems through personalized estate planning and probate services. Ms. Desai’s dual licensure as an attorney and real estate professional means we streamline estate-related property transactions, reducing costs and delays that complicate administration. We provide compassionate guidance during what is often a difficult time, helping families navigate trust administration with confidence rather than fear.

Contact Law Offices of Roshni T. Desai for a free consultation and discuss your trust and administration concerns in a setting that works for you. We offer flexible home or office visits across Southern California, so you can review your documents and see exactly how proactive planning prevents the costly disputes that damage families. Reach out today to take the first step toward protecting your family’s future.