Trust Administration Asset Management: A Practical Playbook

Trust administration asset management requires clear systems and professional guidance to protect beneficiaries and preserve wealth. Many trustees struggle with the competing demands of investment decisions, tax planning, and beneficiary communication.

We at Law Offices of Roshni T. Desai have seen firsthand how the right strategies and processes transform trust administration from overwhelming to manageable. This playbook walks you through practical approaches that work.

What Trustees Actually Do With Trust Assets

The Critical First 90 Days

Trust administration isn’t abstract-it’s about controlling real assets, managing cash flow, and making decisions that directly affect beneficiaries’ financial security. A trustee’s job starts the moment the trust becomes active, whether due to the grantor’s incapacity or death. The first 90 days matter most. You must formally accept the role in writing, locate the original trust document and any amendments, gather death certificates if applicable, and identify every asset: bank accounts, brokerage statements, real estate deeds, life insurance policies, business interests, and even digital assets. This inventory phase takes time but prevents costly mistakes later. Open a separate trust bank account and obtain an EIN from the IRS so trust finances stay completely separate from your personal money. Many trustees fail here and mix funds, which creates audit risk and makes it harder to prove you acted with care.

Investment Management and Asset Protection

The Prudent Investor Rule requires you to act with care, skill, and caution-no guesses, no gambles. You must diversify investments, avoid concentration in a single stock or property, and regularly review performance against appropriate benchmarks. If you manage real estate, update insurance immediately, maintain the property, and retitle assets into the trust’s name to protect against loss. Your fiduciary duties are non-negotiable: loyalty means the trust’s interests come before yours, prudence means you research decisions and seek professional help when needed, and impartiality means you balance the needs of current beneficiaries against future remainder beneficiaries fairly.

Documentation, Valuation, and Tax Compliance

Documentation serves as your shield. You must record every asset, expense, and decision and keep them separate from personal finances. California law requires an annual accounting, and you need signed receipts from beneficiaries for distributions to create a clear paper trail. Many trustees underestimate the complexity of tax compliance. You will file the decedent’s final income tax return, the trust’s Form 1041 with the IRS, and potentially state fiduciary returns. Asset valuations matter enormously-real estate, collections, and business interests require professional appraisals to establish defensible values for tax reporting and distribution. Settle debts and final medical bills before distributing anything to beneficiaries, and communicate timelines clearly so expectations are set from the start.

Building Your Professional Team

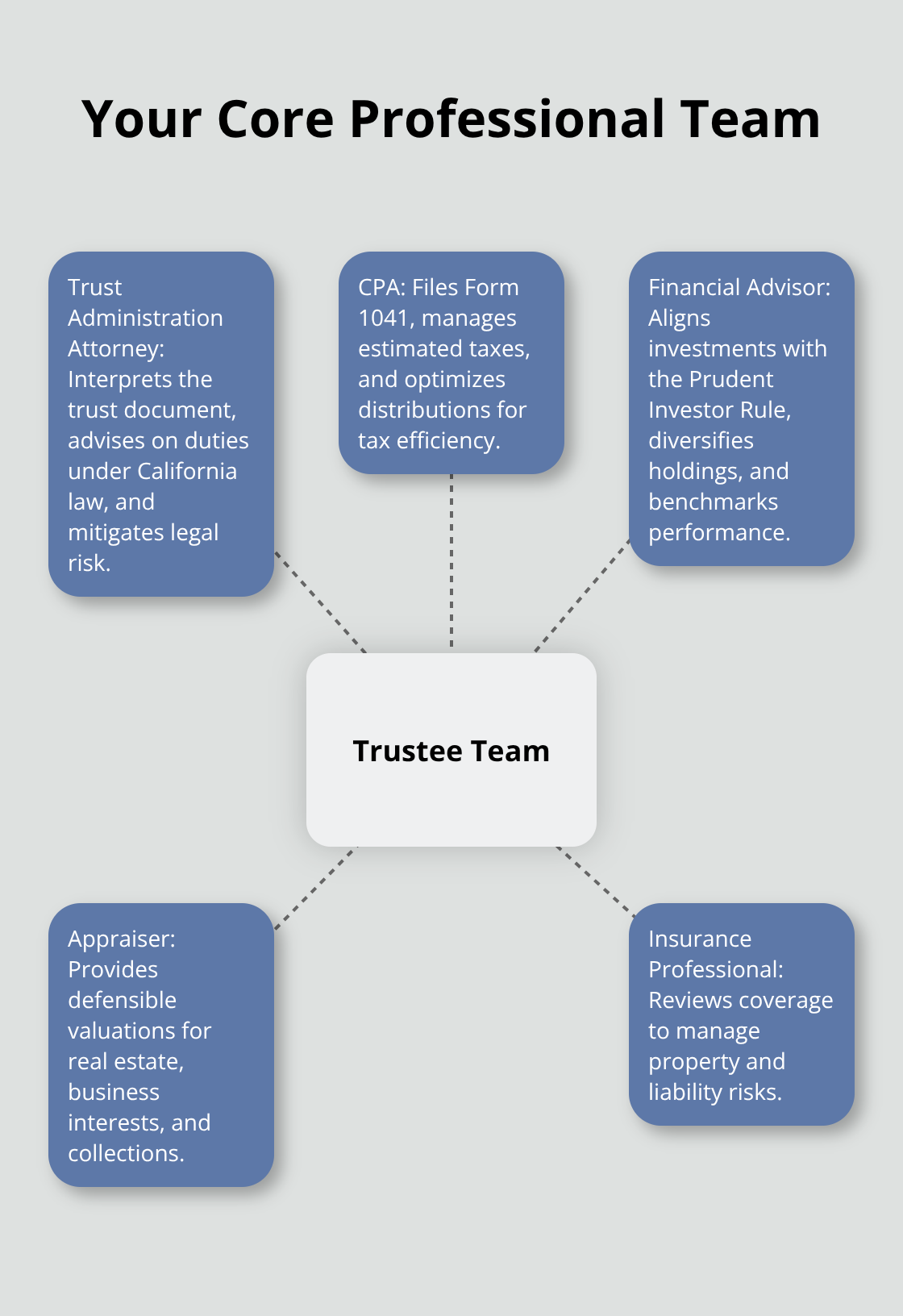

Most trustees assemble a professional team early: a trust administration attorney, a CPA familiar with trust taxation, and a financial advisor aligned with the Prudent Investor Rule. The trust pays these fees, not you personally. Handling this alone almost always costs more in errors and missed opportunities than professional guidance would have cost upfront. The complexity of managing investments, distributions, and tax obligations demands coordinated support. When you work with professionals who understand trust law and tax strategy, you protect both the trust’s assets and your own liability as trustee. This foundation of professional guidance and clear systems positions you to handle beneficiary communications and requests effectively-the next critical area where many trustees stumble.

Building a Diversified Portfolio and Managing Risk in Trust Assets

Diversification as Your Foundation

Trust asset management succeeds or fails based on investment decisions made during the first year. The Prudent Investor Rule demands that you diversify holdings across asset classes, geographies, and time horizons rather than concentrating wealth in a single stock, bond, or property. A trustee who holds 60 percent of trust assets in one company stock violates this standard, even if that company is historically stable. Concentration creates unnecessary risk and exposes you to liability claims from beneficiaries.

Start by developing an Investment Policy Statement that defines the trust’s risk tolerance, time horizon, liquidity needs, and spending obligations. This document becomes your roadmap and protects you if beneficiaries later question your decisions. If the trust requires $40,000 annually for distributions but holds only illiquid real estate, you have a mismatch that demands immediate correction through asset sales or refinancing.

Valuation and Performance Benchmarking

Real estate valuations require professional appraisals every three to five years, not estimates. Business interests need formal valuation using income approach or comparable sales methods, not guesswork. For investment portfolios, benchmark performance against appropriate indices-a balanced fund should track the S&P 500 and bond indices, not beat them wildly or underperform significantly.

Many trustees fail because they chase returns or hold outdated positions inherited from the grantor without reassessing suitability for current beneficiary needs. You must actively review whether each holding still serves the trust’s purpose and the beneficiaries’ interests.

Tax-Efficient Distribution Planning

Tax efficiency separates competent trust administration from careless administration. California and federal tax law allow you to control when income flows to beneficiaries and when capital gains are realized, creating planning opportunities that reduce the overall tax burden. Distributing income to beneficiaries in lower tax brackets costs less than retaining it in the trust, where higher rates apply.

If the trust generates $50,000 in dividend income and a beneficiary sits in the 22 percent federal bracket while the trust sits in the 37 percent bracket, distributing that income saves roughly $7,500 in federal taxes alone. Conversely, you realize large capital gains in low-income years and spread them across multiple years to reduce the likelihood of pushing beneficiaries into higher brackets. Form 1041 and Schedule K-1 reporting tie directly to these distribution decisions, so coordination with your CPA is non-negotiable.

Documentation and Record-Keeping Systems

Documentation serves as your legal protection. You record every asset purchase and sale with dates, cost basis, and fair market value at acquisition. You maintain receipts from all beneficiary distributions signed and dated by the recipient. You create a separate trust accounting file that lists assets by category, tracks income deposits, records expenses paid, and notes distributions made each month.

California law requires annual accountings, and courts can surcharge trustees who fail to maintain clear records. Digital asset management deserves equal attention-cryptocurrency, online bank accounts, and digital brokerage platforms must be tracked with the same rigor as physical property. A trustee who loses track of a Bitcoin wallet containing significant value faces beneficiary claims for negligence. You open a dedicated trust bank account and investment account in the trust’s name, never in your personal name, and maintain them separately from day one. This separation protects both the trust and you personally if disputes arise.

Moving Forward With Beneficiary Communications

These investment and tax strategies work only when beneficiaries understand what you’re doing and why. Clear communication about your diversification approach, distribution timing, and performance benchmarks prevents misunderstandings and builds trust. The next section covers how to handle beneficiary requests and set expectations that align with your asset management decisions.

Professional Support and Beneficiary Alignment

Assembling Your Professional Team Early

Trustees who hire the right professionals early stop most trust administration problems before they start. A trustee managing significant assets without a CPA, attorney, and financial advisor risks beneficiaries’ money and personal liability. The trust pays these fees from its assets, not from your pocket, so cost should never prevent you from securing professional help. A trust administration attorney reviews your duties under California law, confirms you understand the trust document’s requirements, and protects you from misinterpreting vague language. A CPA handles Form 1041 filing, calculates estimated tax payments, and identifies distribution strategies that minimize the overall tax burden across the trust and beneficiaries. A financial advisor aligned with the Prudent Investor Rule manages the portfolio, ensures proper diversification, and benchmarks performance against appropriate indices so you can defend your investment decisions later. Assemble this team within the first 30 days of accepting the trustee role. The cost of coordinated professional guidance averages 0.5 to 1.5 percent of trust assets annually for smaller trusts and drops significantly for larger estates, while mistakes from acting alone can cost multiples of that amount.

Communicating With Beneficiaries Effectively

Beneficiary communication determines whether your administration succeeds or fails. Send written notice to all beneficiaries within 30 days of the trust becoming active, clearly stating your role, the trust’s assets, and what to expect in the coming months. Silence breeds suspicion and disputes, so transparency matters more than avoiding questions. Provide annual accountings showing every asset, all income received, every expense paid, and every distribution made. When a beneficiary requests information, respond within two weeks with specific documents or explanations rather than vague answers. Document these conversations in writing and keep copies in your trust file.

Handling Beneficiary Requests and Disputes

When a beneficiary requests an early distribution or challenges your investment decisions, listen carefully and explain your reasoning with reference to the trust document and the Prudent Investor Rule. Set clear timelines upfront: distributions happen on specific dates, appraisals take 30 to 45 days, and tax returns file by the April deadline. If a beneficiary becomes hostile or demands actions that violate the trust terms, consult your trust administration attorney immediately rather than negotiating alone. This approach protects both the trust and your position as trustee.

Final Thoughts

Trust administration asset management succeeds when you act decisively in the first 90 days, hire professionals immediately, and document everything from the start. The trustees who avoid costly mistakes separate trust finances from personal money, file complete tax returns, and communicate transparently with beneficiaries. Courts surcharge trustees who mix accounts or fail to maintain records, and beneficiaries remove trustees who create suspicion through silence.

If you have just accepted a trustee role, prioritize the first 90 days: formally accept in writing, locate all documents, inventory every asset, open separate accounts, and hire a trust administration attorney, CPA, and financial advisor. If you already administer a trust, audit your current practices against the Prudent Investor Rule and California law by reviewing your investment diversification, confirming your tax filings are complete, and assessing whether your beneficiary communications remain transparent and timely. Address any gaps now rather than waiting for a beneficiary to challenge your decisions.

We at Law Offices of Roshni T. Desai provide personalized guidance on trust administration, investment strategy, and beneficiary communications tailored to your specific situation. Contact us for a free consultation if you need support navigating trust administration or want to review your current approach.