Probate Asset Inventory: Comprehensive Listing for Estate Tax and Distribution

A probate asset inventory is one of the most overlooked steps in estate administration, yet it directly impacts how much your heirs actually receive. Missing even one account or undervaluing property can trigger tax problems and family disputes that take years to resolve.

We at Law Offices of Roshni T. Desai have seen estates lose thousands because families failed to document everything properly from the start. This guide walks you through exactly what belongs on your inventory and how to avoid the costly mistakes we see repeatedly.

What Actually Belongs in Your Probate Inventory

Real estate, bank accounts, and jewelry are obvious-but most families miss 30 to 40 percent of what should be listed. The inventory isn’t just a nice-to-have document; Florida probate rules require it within 60 days of appointment, and incomplete inventories directly delay distributions to heirs and trigger tax complications. Start with real property first, then move systematically through financial accounts, and finally capture personal property that holds actual value.

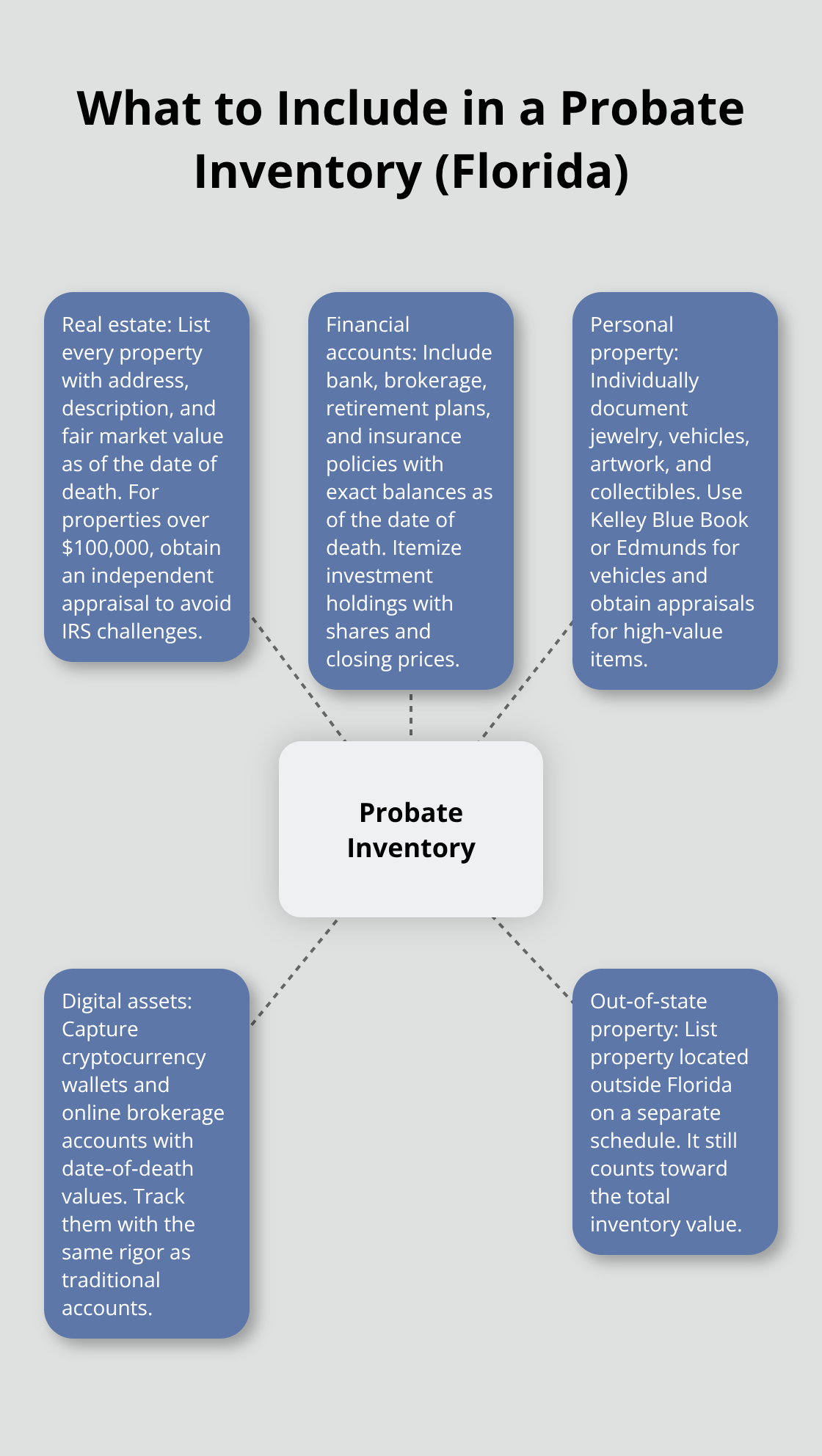

Real Estate and Property Holdings

Every piece of real estate the decedent owned must appear on the inventory, regardless of whether it carries a mortgage or significant value. Include the street address, a clear property description, and the fair market value as of the date of death-not the listing price or what you hope to sell it for. For Florida homestead property, you need to determine whether it qualifies for exemption, which requires a judicial determination and affects how creditors can claim against the estate. Non-exempt Florida real estate gets listed separately with its own valuation. Property located outside Florida goes on a separate schedule but still counts toward the total inventory value. Vacant land, rental properties, and commercial holdings all belong here. The valuation method matters: use county tax assessments as a starting point, but for properties worth over $100,000, obtain an independent appraisal rather than guessing. This protects the estate from IRS challenges and provides beneficiaries with documented proof of how values were determined.

Financial Accounts and Investment Holdings

Bank accounts, brokerage accounts, retirement plans, and insurance policies must all appear on the inventory with their account balances as of the date of death. Collect statements from every institution-checking, savings, money market, CDs, investment accounts, IRAs, and 401(k) plans. Include the institution name, account type, last four digits of the account number, and the exact balance. Many families overlook payable-on-death accounts and retirement benefits with named beneficiaries; these bypass probate but still require documentation in the inventory. If the decedent held stocks, bonds, or mutual funds, list the number of shares and the closing price on the date of death, not the current price. Investment accounts with multiple holdings should be itemized separately to avoid confusion during distribution. Digital assets like cryptocurrency wallets and online brokerage accounts are frequently forgotten but represent real value-track these with the same rigor as traditional accounts.

Personal Property That Holds Real Value

Household goods, furniture, and clothing can be grouped into categories with an estimated total rather than listing every item, but jewelry, collectibles, vehicles, and artwork require individual attention. For vehicles, record the year, make, model, VIN, and fair market value using Kelley Blue Book or Edmunds-don’t rely on what the family thinks it’s worth. Jewelry worth more than $500 per piece should be professionally appraised; smaller items can be grouped. Antiques, art, firearms, and collectibles with secondary market value need appraisals too. Obtain multiple estimates for high-value items and keep documentation of how each value was determined. Many estates have overlooked valuables in safety deposit boxes, storage units, or home safes-conduct a thorough physical search and don’t skip this step. Once you’ve identified and valued all assets, the next challenge is avoiding the mistakes that derail most inventories during the documentation process.

Common Mistakes When Creating a Probate Asset Inventory

Undervaluing Assets Costs Your Estate Thousands

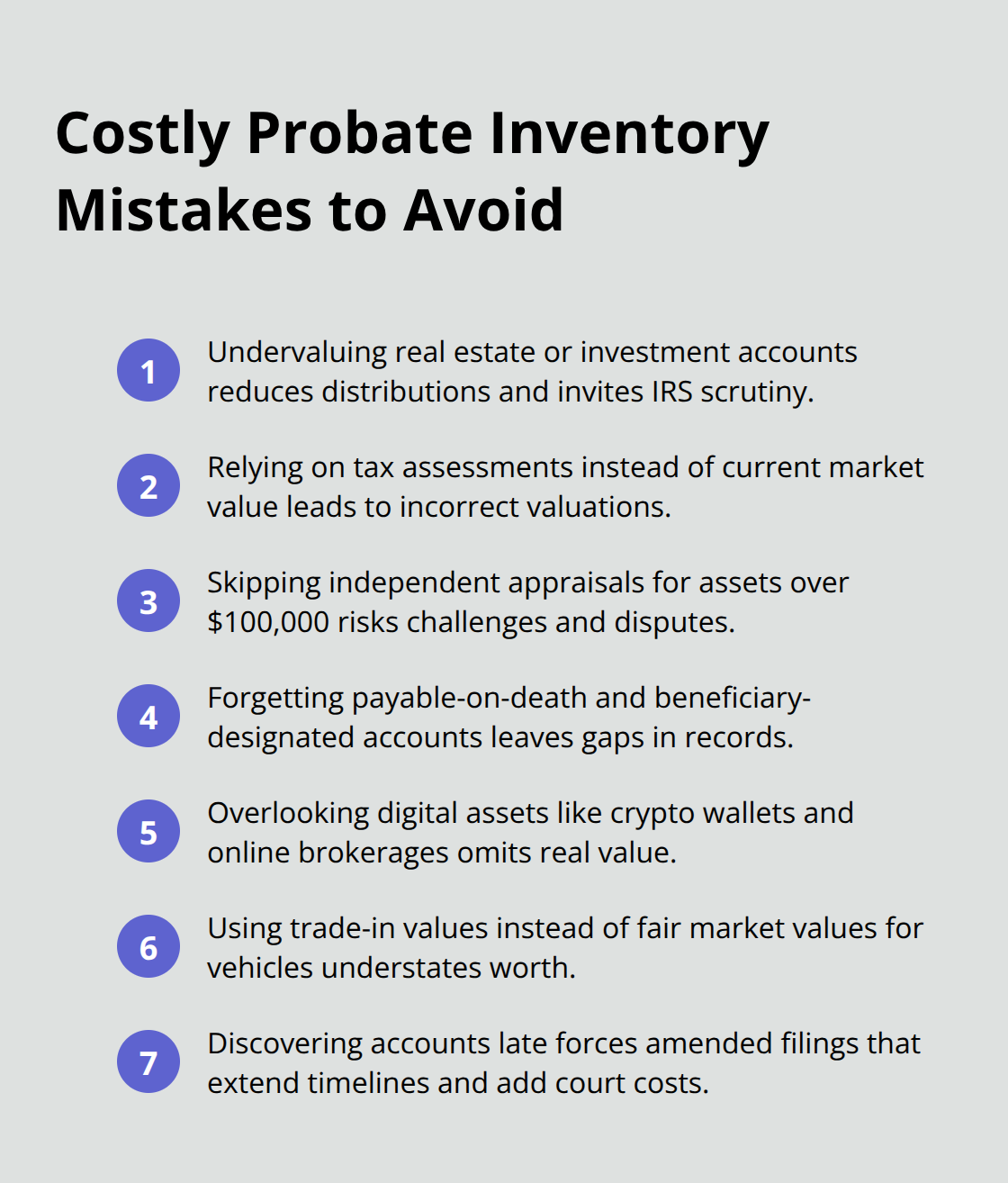

The gap between what families think they own and what actually appears on the inventory creates problems that ripple through the entire probate process. Undervaluation ranks as the single most costly mistake-when a $250,000 investment account gets listed at $180,000 or a rental property is valued at county tax assessment rather than current market rate, the estate pays unnecessary taxes and heirs receive less than they should. The IRS challenges undervalued estates regularly, and once questioned, the burden falls on the personal representative to prove the original valuation was accurate. This is why independent appraisals matter for anything worth over $100,000. For vehicles, using Kelley Blue Book’s fair market value rather than trade-in value can mean the difference between $15,000 and $22,000 on a single car.

The valuation date itself is critical-use the fair market value as of the date of death, not the date you create the inventory three months later. Markets move, and using current prices inflates or deflates the estate value incorrectly.

Hidden Accounts Slip Through the Cracks

Bank statements arriving at the deceased’s address often sit unopened for weeks, meaning accounts continue accruing interest or fees without anyone’s knowledge. Safety deposit boxes frequently contain cash, securities, or jewelry that families never discover because they didn’t know the box existed. Check the decedent’s mail for six months before and after death, request account statements from all financial institutions where the person had relationships, and review tax returns from the past three years to identify investment accounts and retirement plans. Digital assets create a particularly blind spot-cryptocurrency wallets, online brokerage accounts, PayPal balances, and domain names with resale value vanish from most inventories because executors don’t think to search for them. Request the decedent’s digital asset list from their financial advisor or accountant, search email for account confirmations and statements, and check password managers if you have access.

Digital Assets Represent Real Money

Online accounts hold substantial value that most families overlook entirely. Cryptocurrency stored in digital wallets, domain names with established traffic or resale value, and social media accounts with monetized followings all represent estate assets. Many executors skip these accounts because they assume digital property has no value or they don’t know where to look. Start by searching the decedent’s email for account confirmations, password reset notifications, and statements from cryptocurrency exchanges or online brokers. Check whether the decedent maintained a list of passwords or digital assets-many financial advisors now ask clients to document this information. If you find cryptocurrency, obtain a current valuation from the exchange where it was held as of the date of death. Domain names can be valued through domain appraisal services or by checking comparable sales on marketplaces. Social media accounts with commercial value (YouTube channels, Instagram accounts with sponsorships) should be documented with their current follower counts and any revenue streams they generate.

Amended Filings Create Delays and Extra Costs

Many families discover forgotten accounts months after the inventory closes, requiring amended filings that delay distributions and trigger additional court costs. Each amendment filed with the probate court extends the timeline for closing the estate and increases administrative expenses. The personal representative bears responsibility for accuracy, and incomplete inventories can expose them to liability claims from beneficiaries who receive less than they should have. Conduct a thorough search before submitting the initial inventory rather than rushing through the process. This upfront effort prevents the costly corrections that follow incomplete documentation. Once you’ve identified all assets and avoided these common pitfalls, the next step involves creating a systematic process that captures everything accurately and produces documentation the probate court will accept without question.

How to Build Your Documentation System

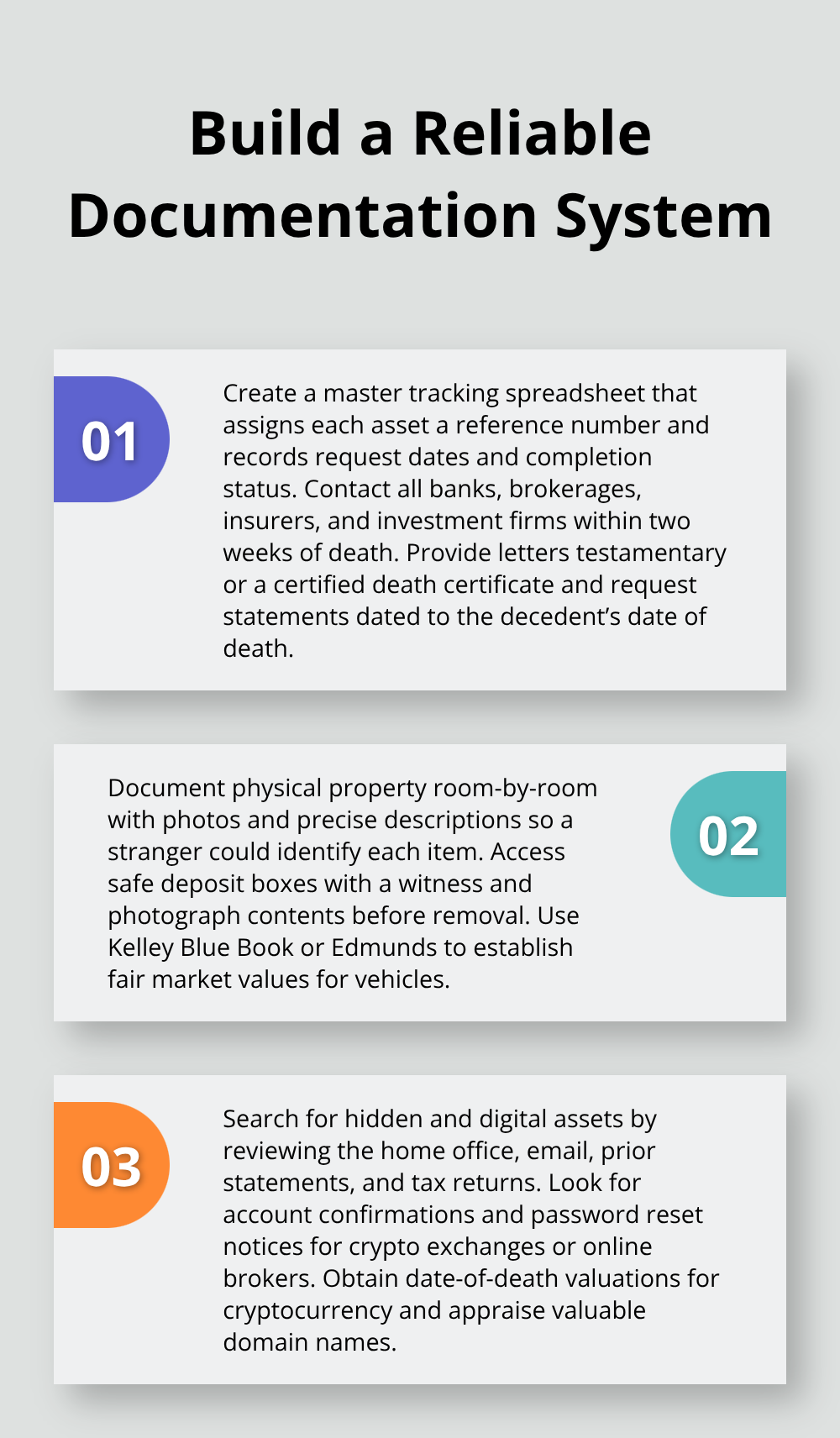

Create a Master Tracking Spreadsheet

A master spreadsheet prevents duplicate requests and catches gaps before they become problems. Assign each asset a reference number, note the institution or location, record the date you requested information, and mark completion once documentation arrives. This single document becomes your control center for the entire inventory process. Contact every bank, brokerage, insurance company, and investment firm where the decedent held accounts within the first two weeks after death.

Provide letters testamentary or a certified death certificate along with your request, and ask specifically for account statements dated to the decedent’s death. Many institutions require this formal documentation before releasing information.

Request six months of prior statements as well, since account transfers or changes made shortly before death sometimes reveal overlooked assets or uncover fraudulent activity. Create a separate folder for each institution’s documents and cross-reference them in your spreadsheet so nothing gets lost in the administrative shuffle. This organizational approach transforms what could be a chaotic process into a manageable system that produces results.

Document Physical Property Systematically

A systematic room-by-room inspection of the home, storage units, safe deposit boxes, and anywhere else the decedent maintained belongings uncovers assets that paper trails miss. Take photographs of high-value items and note condition details that affect resale value. Jewelry, firearms, art, and collectibles require individual documentation with descriptions precise enough that a stranger could identify each piece. Don’t rely on memory or family recollections about what exists or where it’s stored.

Contact the bank to access any safe deposit boxes and bring a witness when you open them. Document everything inside with photos before removing anything. For vehicles, gather the title documents and use Kelley Blue Book’s fair market value tool to establish baseline values rather than relying on what family members think the cars are worth. This methodical approach prevents valuable items from slipping through the cracks.

Search for Hidden and Digital Assets

The decedent’s home office, email, and financial records often contain evidence of overlooked accounts, safety deposit boxes, or digital assets. Look for statements, bills, or account confirmations that reference institutions you haven’t yet contacted. Many people maintain accounts at multiple brokers or banks specifically to organize different types of investments, and these secondary accounts frequently escape initial attention.

Cryptocurrency stored in digital wallets, domain names with established traffic or resale value, and social media accounts with monetized followings all represent estate assets that most families overlook entirely. Search the decedent’s email for account confirmations, password reset notifications, and statements from cryptocurrency exchanges or online brokers. Check whether the decedent maintained a list of passwords or digital assets-many financial advisors now ask clients to document this information. If you find cryptocurrency, obtain a current valuation from the exchange where it was held as of the date of death. Domain names can be valued through domain appraisal services or by checking comparable sales on marketplaces.

Organize Documentation for Court Submission

Each document you collect serves a specific purpose in the probate process and must be organized for easy retrieval. Maintain a chronological record of when you requested information, when institutions responded, and what documentation you received. This trail protects you if questions arise about the completeness of your search. Cross-reference all documents in your master spreadsheet so the probate court can verify that your inventory matches the supporting evidence you’ve collected.

Professional valuation becomes the final step that protects your inventory from IRS scrutiny and ensures beneficiaries receive accurate distributions based on actual fair market values rather than guesses or outdated assessments.

Final Thoughts

A complete probate asset inventory protects your estate from tax complications, family disputes, and unnecessary delays that cost thousands in administrative fees and lost distributions. When you document every asset systematically, obtain proper valuations, and maintain organized records, the probate court processes your estate faster and beneficiaries receive what they’re entitled to without question. The difference between a thorough inventory and a rushed one often determines whether your heirs spend months waiting for distributions or receive their inheritance within a reasonable timeframe.

Florida law requires you to file your probate asset inventory within 60 days of appointment, and missing this deadline creates immediate problems with the court. Once filed, you’ll respond to any questions the probate judge raises about valuations or missing assets, then proceed with paying creditors’ claims and distributing remaining assets according to the will or state law. This process moves smoothly only when your initial inventory is accurate and complete.

We at Law Offices of Roshni T. Desai help personal representatives navigate probate asset inventory preparation and administration for families across Southern Florida who want to avoid costly mistakes. Contact us to schedule your free consultation and take the first step toward protecting your estate.