Executor Probate Responsibilities: Duties You Must Know

Being named an executor comes with real legal obligations that many people don’t fully understand until they’re already in the role. The decisions you make-from managing assets to filing taxes-directly affect whether beneficiaries receive their inheritance on time and whether the estate avoids costly legal problems.

We at Law Offices of Roshni T. Desai have seen executors face serious consequences for missing deadlines or overlooking key responsibilities. This guide breaks down the executor probate responsibilities you need to know, the mistakes to avoid, and when to bring in legal support.

What an Executor Actually Does

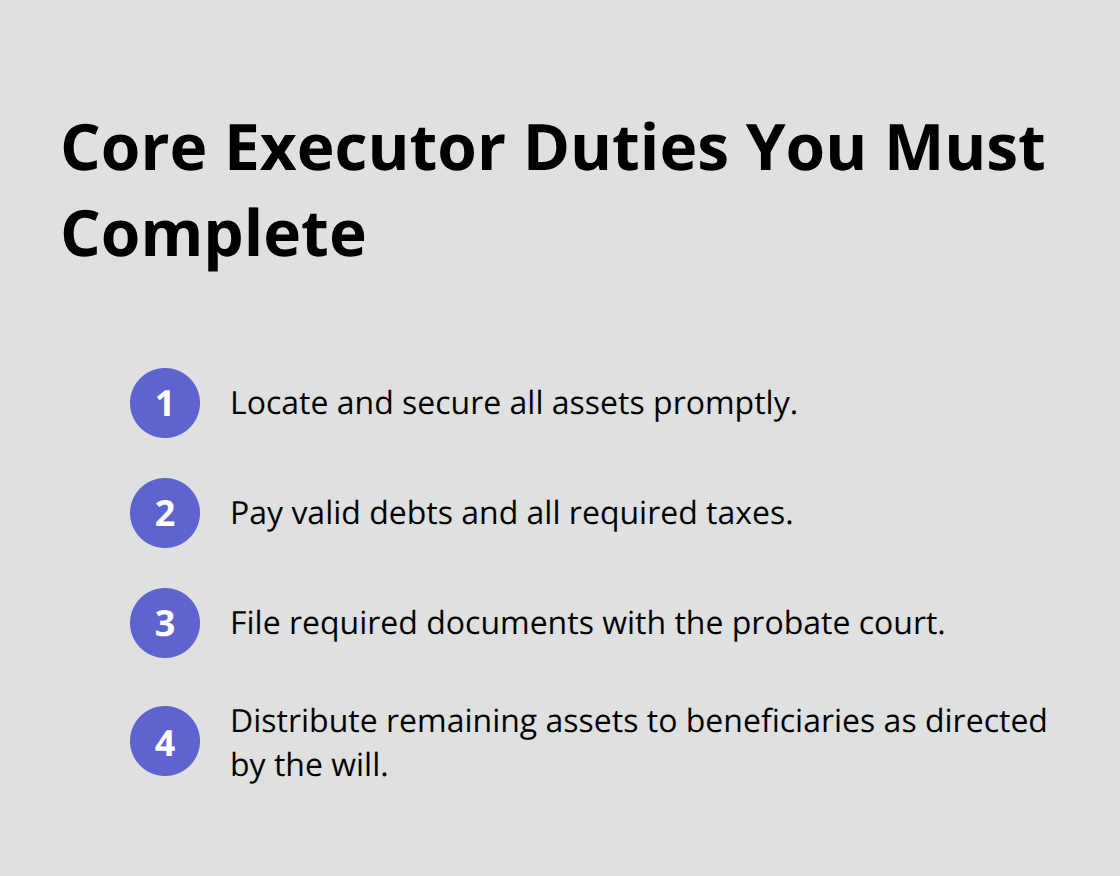

An executor is the person appointed by a court or named in a will to manage a deceased person’s estate during probate. Your role isn’t ceremonial-it’s a legal position with fiduciary duties that can expose you to personal liability if you fail to act properly. According to Forbes and Cornell Law’s Legal Information Institute, executors must locate and secure assets, pay debts and taxes, file required documents with the court, and distribute what remains to beneficiaries. The probate court supervises this process, which means your actions are subject to legal scrutiny.

Many executors underestimate the time commitment involved. Simple estates settle in under a year, but complex ones with multiple properties, business interests, or family disputes routinely take three to five years. You’ll open an estate bank account, track every expense, maintain detailed records, and communicate regularly with beneficiaries and creditors. Mismanaging funds, missing tax deadlines, or making unauthorized distributions exposes you to personal liability for losses.

Administrator vs. Executor: Understanding the Legal Distinction

The terms executor and administrator are often used interchangeably, but they have a key difference. An executor is named in the will and chosen by the deceased before death. An administrator is appointed by the probate court when there is no will or when the named executor cannot serve. Both roles carry identical legal responsibilities-managing assets, paying debts, filing taxes, and distributing property.

The administrator’s appointment typically takes longer because the court must follow intestacy laws to identify heirs and determine distribution. This added step delays the settlement process by months. Whether you’re an executor or administrator, you face the same fiduciary duty to act in the estate’s and beneficiaries’ best interests. Beneficiaries can petition the court to remove an executor or administrator who fails to perform their duties, and in some states, beneficiaries themselves serve as executors, which is common in family-run estates.

Why Your Responsibilities Matter More Than You Think

Understanding your executor duties protects the estate from costly mistakes and protects you from personal liability. A single missed deadline-like failing to file federal or state estate tax returns within nine months of death-triggers penalties, interest charges, and audits that drain estate assets. According to Justia, executors must obtain multiple certified copies of the death certificate (typically at least ten) because banks, insurers, creditors, and government agencies each require original or certified copies.

Neglecting to notify creditors promptly results in claims against the estate after you’ve already distributed assets to beneficiaries, leaving you personally responsible for repaying those amounts. The probate process demands organization, attention to deadlines, and knowledge of tax law and estate administration procedures. If your estate involves real property, multiple states, business interests, or significant assets, the complexity increases dramatically and professional guidance becomes essential to avoid costly errors.

The next section walks through the core duties that form the foundation of executor responsibilities and shows you exactly what actions you must take at each stage.

What Executors Must Actually Do With Assets and Money

Locate and Secure Every Asset

The moment you’re appointed executor, your first responsibility is locating and securing every asset the deceased owned. This includes bank accounts, investment portfolios, real estate deeds, vehicles, insurance policies, and personal property. According to Forbes, you must obtain multiple certified copies of the death certificate-at least ten-because each financial institution, creditor, and government agency requires originals or certified copies before releasing information or transferring accounts.

Open an estate bank account immediately in the estate’s name, not your personal account. This single step protects you from personal liability and creates a clear audit trail for every dollar that moves. Deposit all estate funds into this account and pay all ongoing expenses-mortgage payments, utilities, property taxes, insurance premiums-from it. Many executors make the critical mistake of using their own accounts temporarily, which blurs personal and estate finances and invites tax complications and beneficiary disputes.

Create a Detailed Asset Inventory

You must create a detailed inventory of all assets with estimated values. Some assets require professional appraisal, particularly real estate, business interests, and valuable personal property like jewelry or art. Illinois law, for example, requires probate when estate assets exceed $100,000, which means proper valuation determines whether your estate avoids probate entirely through smaller estate procedures. Document everything with photographs, receipts, and professional appraisals that you keep on file.

Identify and Pay All Debts and Taxes

Paying debts and taxes comes next and drains most executors’ time. You must identify all outstanding debts-credit cards, medical bills, mortgages, car loans-and notify creditors of the death. State law typically gives creditors a window to file claims, often four months from the date you publish notice in a local newspaper.

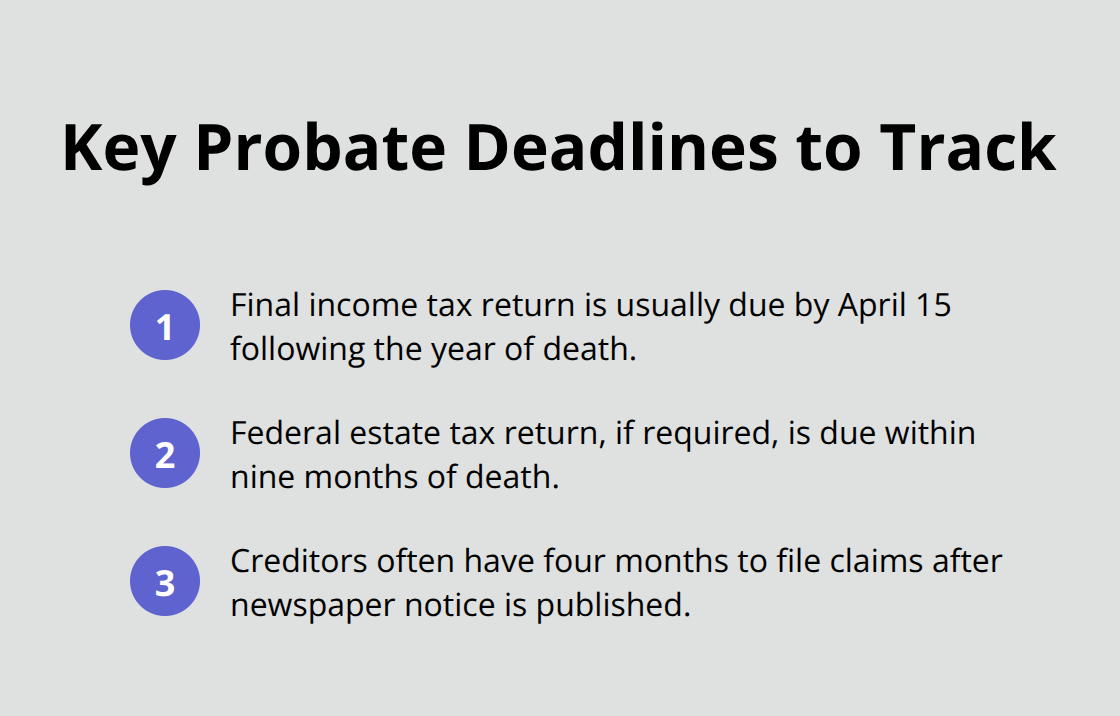

Federal and state income tax returns for the deceased are due within the normal filing deadline, usually April 15 following the year of death. Estate tax returns, if required, are due within nine months of death according to federal law. Missing this deadline triggers automatic penalties and interest that reduce assets available for beneficiaries.

If your estate involves property in multiple states or significant assets, hire a tax professional immediately; the cost of professional guidance is paid from estate funds, not your pocket.

Distribute Assets and Document Everything

After all debts and taxes are settled, you distribute remaining assets to beneficiaries according to the will’s terms. This is where detailed record-keeping becomes your legal shield. Keep receipts from every beneficiary confirming they received their inheritance. Some states require written acknowledgment; others accept simple signed receipts. Track the date of distribution, the asset description, and the beneficiary’s signature. If disputes arise later-and they often do in family estates-your documentation proves you acted correctly and protects you from personal liability claims.

Maintain organized files throughout the entire process with copies of all court filings, tax returns, bank statements, and correspondence with beneficiaries and creditors. This documentation also supports your compensation claim if state law permits executor fees. The complexity of managing these financial and legal responsibilities often exceeds what most executors anticipate, which is why understanding the common pitfalls that derail estates becomes your next critical step.

Where Executors Go Wrong

Missing Tax Deadlines Costs Thousands

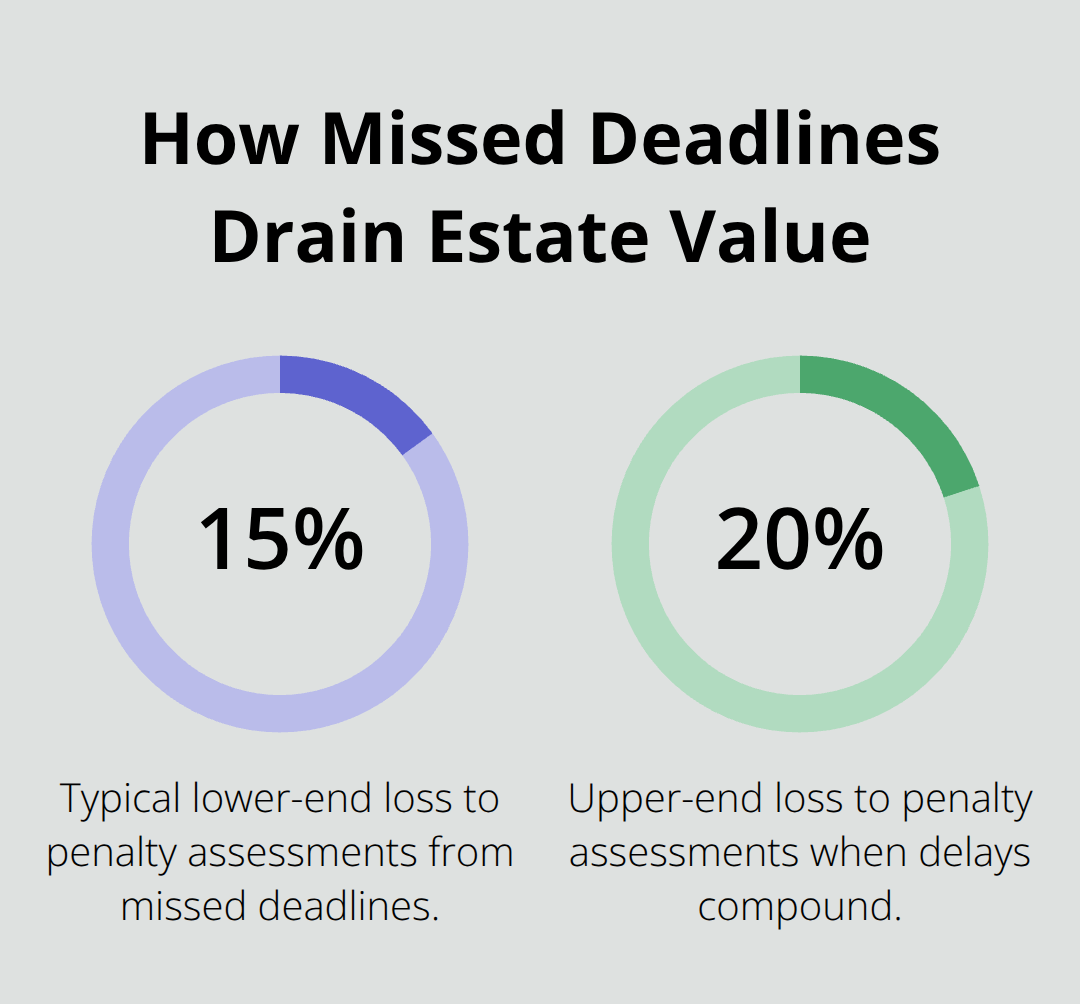

The most expensive executor mistakes happen silently, months into the probate process, when deadlines pass or documents sit unfiled. Tax returns for the deceased are due by April 15 following the year of death, and estate tax returns must be filed within nine months of death according to federal law. Missing either deadline triggers automatic penalties and interest that compound monthly, draining thousands from the estate before beneficiaries receive anything. Estates lose 15 to 20 percent of their value to penalty assessments that could have been avoided with a single phone call to a tax professional. The IRS doesn’t care about your circumstances-the penalty clock starts the moment the deadline passes.

State taxes add another layer of complexity. Pennsylvania, for example, offers a three-month prepayment discount on inheritance tax, meaning executors who file early save money directly for beneficiaries. Most executors don’t know this discount exists and pay full rates months later. Hire a tax professional immediately after the death occurs, not after you’ve already missed deadlines. Their fees come from estate funds, not your pocket, and they pay for themselves through penalty avoidance alone.

Mixing Personal and Estate Money Creates Legal Exposure

The second critical mistake is mixing estate money with personal finances. You must open an estate bank account immediately-this step is non-negotiable. Many executors deposit funds into their own accounts temporarily for convenience, which creates an audit trail nightmare if the IRS questions distributions. This approach also exposes you to personal liability if beneficiaries claim you misappropriated funds.

Every dollar must move through the estate account with documentation. Pay all bills (mortgage, utilities, property taxes, insurance) from this account and keep receipts. The moment you settle the estate too quickly without proper documentation, you lose your legal protection. Beneficiaries can challenge distributions years later if they suspect mismanagement, and without receipts proving you paid debts, taxes, and legitimate expenses, you become personally responsible for losses.

Notifying Creditors and Beneficiaries on Time Prevents Liability

Courts have ruled that executors who distribute assets before all creditors are notified must repay those amounts personally. Illinois law gives creditors four months to file claims after you publish notice in a newspaper, and skipping this step or distributing before the window closes is a costly error. Beneficiaries must also receive timely written notice of the estate’s existence and their inheritance rights.

Neglecting these notifications doesn’t just create family conflict-it exposes you to removal by the court and personal liability for losses caused by your delay. Document everything: dates you sent notices, which beneficiaries and creditors received them, copies of the actual notices, and proof of delivery. This documentation is your legal shield when disputes arise.

Final Thoughts

Executor probate responsibilities demand attention to detail, strict adherence to deadlines, and clear communication with beneficiaries and creditors. Missing even one of these core duties-locating assets, paying debts and taxes, maintaining records, or distributing inheritances-triggers penalties, family disputes, or personal liability that follows you long after the estate settles. The time you invest in understanding these obligations upfront prevents costly mistakes that drain estate assets and damage family relationships.

Complex estates involving multiple properties, business interests, or beneficiaries in different states require professional guidance from the start. If your estate exceeds $100,000 in assets, involves real property in multiple states, or includes a family business, an attorney and tax professional protect both the estate and your personal interests through penalty avoidance and tax optimization. Waiting until problems arise costs significantly more than getting guidance at the beginning.

We at Law Offices of Roshni T. Desai understand the weight of executor probate responsibilities and the stress that comes with managing a deceased person’s affairs while grieving. Contact us for a free consultation to discuss your estate’s specific needs and learn how we can support you in fulfilling your duties correctly and efficiently.