Probate Closing Procedures SoCal: Final Steps to Settlement

Probate closing procedures in Southern California involve specific court requirements and timelines that many families find overwhelming. The final steps toward settlement demand careful attention to documentation, asset distribution, and debt resolution. We at Law Offices of Roshni T. Desai guide clients through each phase to reach closure efficiently.

This guide walks you through what to expect and how to navigate the process successfully.

How Long Does Probate Take in Southern California

The Timeline Reality for SoCal Estates

Probate timelines in Southern California range from nine months for straightforward estates to two or three years for complex cases involving multiple properties, business interests, or beneficiary disputes. The mandatory four-month creditor claims period under California Probate Code Section 9100 sets a floor-even simple estates cannot close faster than roughly six months due to waiting periods, court notices, and administrative steps. Large counties like Los Angeles, San Diego, and Orange County experience heavier court dockets, pushing hearing dates out 45 to 60 days, which compounds delays throughout the process.

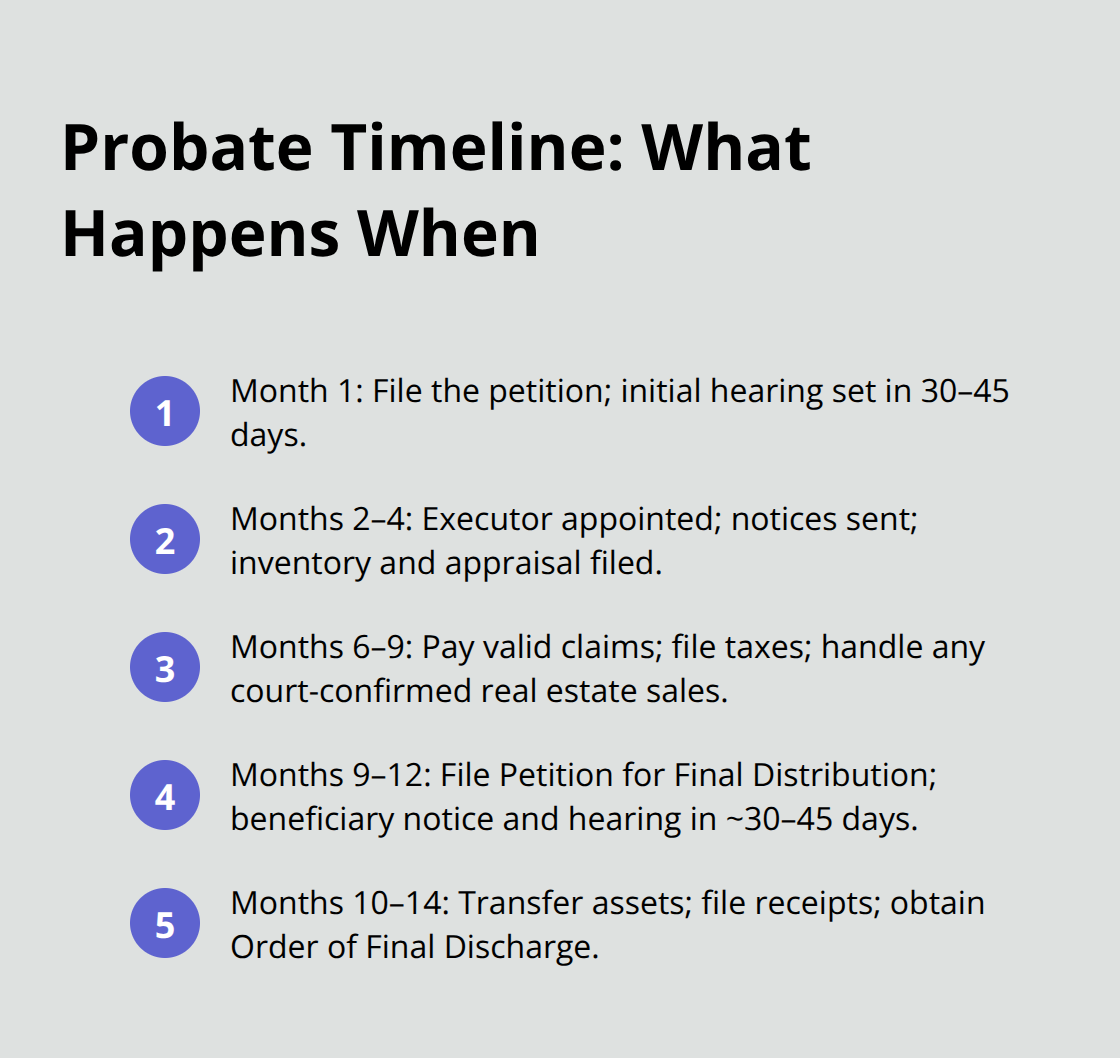

Month One: Filing and Initial Court Hearing

Month one involves filing the Petition for Probate using Judicial Council Form DE-111 with a filing fee around $435. The court schedules a hearing 30 to 45 days after you submit the petition. This initial filing sets the entire timeline in motion and establishes the estate’s official opening date.

Months Two Through Four: Appointment and Asset Marshaling

Month two brings the probate hearing where the court appoints the executor or administrator and issues Letters Testamentary or Letters of Administration. You should obtain 5 to 10 certified copies immediately for banks, title companies, and government agencies. The executor files the Duties and Liabilities of Personal Representative form to formally accept the role, and a probate bond may be required depending on the will or beneficiary consent.

Months two through three see creditor notification and asset marshaling begin. The executor mails Notice of Administration to known creditors and publishes notice in a local newspaper, triggering the four-month claim window. Official notices must be mailed by a neutral third party, not the executor, to create a sworn proof of service record and prevent later objections. Months three through four require filing the Inventory and Appraisal within four months of appointment; non-cash assets often need a probate referee valuation costing roughly 0.1 percent of gross estate value.

Months Six Through Twelve: Claims, Taxes, and Final Distribution

Months six through nine focus on paying valid claims, filing final tax returns, and handling any real estate sales that require court confirmation. Federal estate tax considerations matter here-estates exceeding the 2024 federal exemption of $13.61 million must file Form 706 and wait for IRS processing, which delays final distribution significantly.

Months nine through twelve involve filing the Petition for Final Distribution with a full accounting and proposed distribution. Beneficiaries receive notice and have the right to object, with a hearing scheduled about 30 to 45 days after filing. If probate runs longer than a year, a status report explaining delays must be filed.

Months Ten Through Fourteen: Asset Transfer and Discharge

Months ten through fourteen complete the process after court approval. Assets transfer to beneficiaries, you collect receipts and file them with the court, and the court issues an Order of Final Discharge, formally ending the executor’s duties and requiring real estate deeds to be recorded. Once you understand these timelines, the next critical step involves gathering and preparing the specific documents the court demands before it will approve your final distribution.

Required Documents and Court Filings for Probate Closure

The Petition for Final Distribution: Your Court Roadmap

The court will not approve your final distribution without specific documents proving you have administered the estate properly. The Petition for Final Distribution stands as the centerpiece-this filing tells the court you have paid all valid debts, resolved all claims, and are ready to distribute remaining assets to beneficiaries. California Probate Code Section 11640 sets the condition: debts must be paid or adequately provided for before the court will close the estate. You file this petition using Judicial Council Form DE-350, and it must include a complete accounting showing every dollar that entered and left the estate, a narrative report detailing your administration work, and a detailed list of each asset remaining for distribution.

Building Your Final Accounting: The Foundation of Court Approval

The accounting is not optional-it is the foundation the court uses to verify you have followed the law. Courts in Los Angeles, Orange, San Diego, Riverside, and San Bernardino counties see accounting errors constantly. Common mistakes include failing to distinguish principal from income, omitting sale costs for real property, and providing vague asset descriptions. For real property sales, show the gain on sale as the difference between the gross sale price and the appraised value; include all costs of sale in the disbursements section. If you are distributing to minors, include their birthdates and guardian information. If the estate involved independent administration under the Independent Administration of Estates Act, state the transactions undertaken and attach relevant findings.

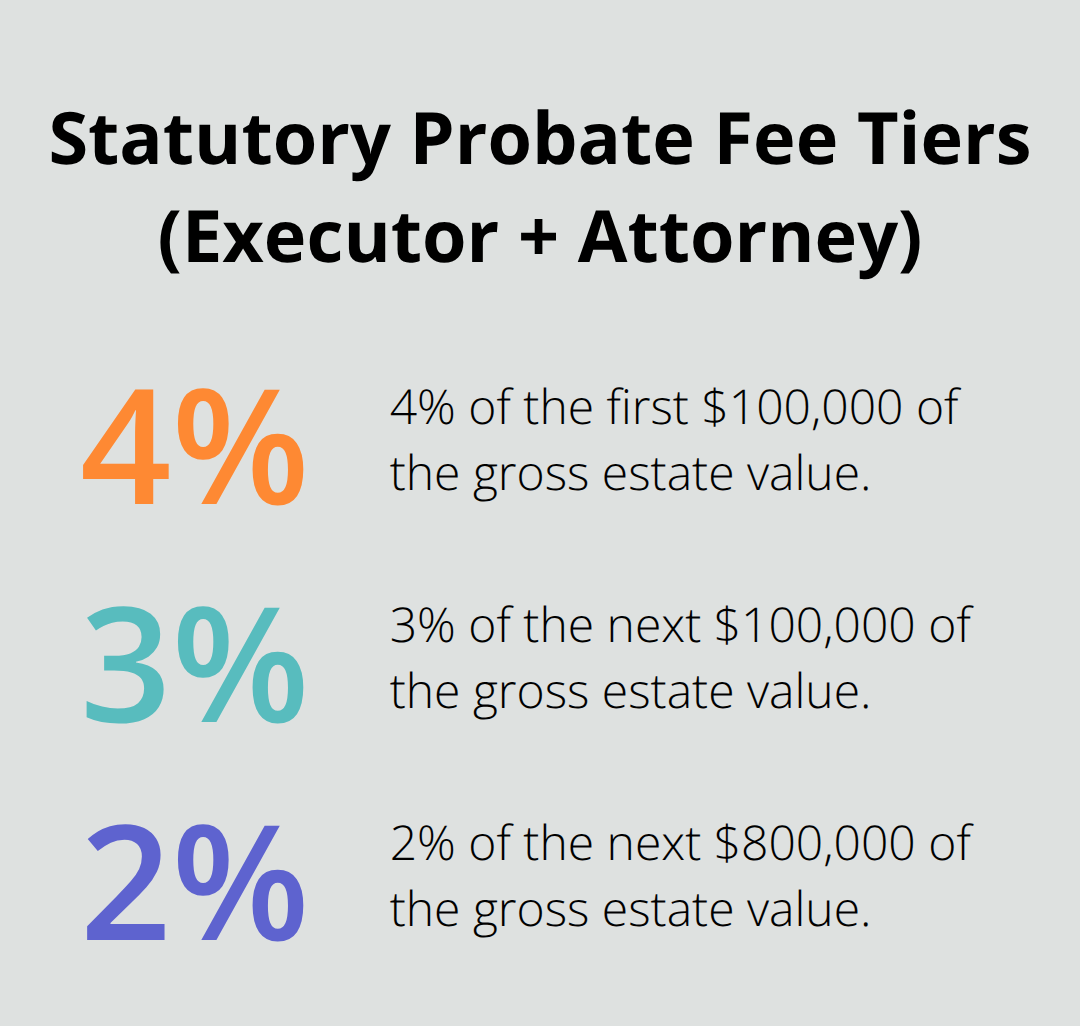

Your final accounting must include two critical schedules: the Schedule of Receipts and the Schedule of Disbursements. Receipts must show the nature, source, and date of each asset received; distinguish between principal and income; and list gains and losses on separate schedules. Disbursements must itemize every expense paid from the estate, including funeral costs, court fees, attorney fees, executor fees, and creditor payments. Under California Probate Code Section 10810, statutory fees for both the executor and attorney are calculated on the gross estate value: four percent of the first $100,000, three percent of the next $100,000, two percent of the next $800,000, one percent of the next $9,000,000, and 0.5 percent above that. A $1 million estate incurs approximately $46,000 in total statutory fees split between executor and attorney, not counting other costs.

Notice Requirements and Beneficiary Communication

The Notice of Hearing using Form DE-120 must reach all beneficiaries and interested parties at least 15 days before the hearing-this is not a suggestion but a statutory requirement. A proof of service by mail must be filed with the probate filing clerk showing exactly when and how each notice was sent. If all beneficiaries sign written waivers acknowledging receipt of assets or waiving the accounting, the court may waive a full accounting. This approach saves time and reduces fees, but waivers must be signed before the petition is filed.

Recording and Final Discharge: Closing the Estate

Once the court approves your petition and issues the Judgment of Final Distribution, you must obtain certified copies, collect signed receipts from each beneficiary, and record the judgment for any real property in the county where that property is located. The Franchise Tax Board may require a clearance certificate if the estate exceeds $1,000,000 and assets distribute to nonresidents. Only after all distributions are complete and receipts are filed can you file the Affirmation of Final Discharge to formally end your fiduciary duties and obtain the court’s order releasing you from liability. With these documents filed and approved, you move into the practical work of actually transferring assets and settling any remaining obligations to beneficiaries.

Settling Debts and Distributing Assets to Beneficiaries

Payment Priority and Reserve Accounts

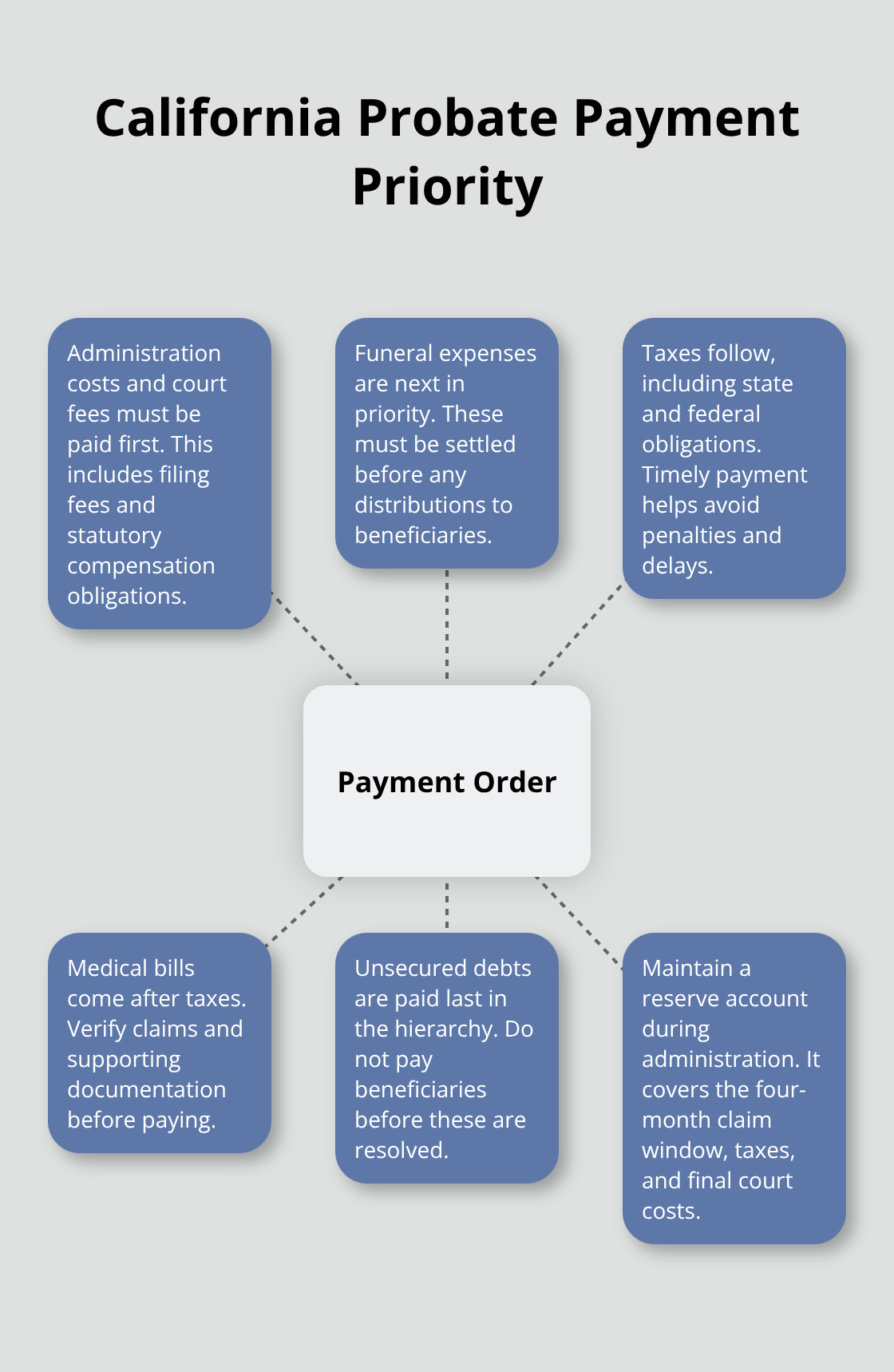

California Probate Code prioritizes payments strictly: probate administration costs and court fees come first, then funeral expenses, followed by taxes, medical bills, and finally unsecured debts. If the estate runs short on liquid funds, you cannot skip creditor payments to pay beneficiaries-doing so exposes you to surcharge liability, meaning the court can hold you personally responsible for the shortfall. You must establish a separate reserve account immediately after receiving Letters of Administration; this account holds funds to cover the mandatory four-month creditor claim window, outstanding taxes, and final court fees before any distribution occurs.

For a $1 million estate, you should expect approximately $23,000 in attorney fees and $23,000 in executor fees alone under California’s statutory fee schedule, plus court costs averaging $2,000 to $5,000 depending on your county.

Tax Clearance and Federal Estate Considerations

Federal estate tax returns must be filed for estates exceeding $13.61 million in 2024; the IRS processing delay can extend your timeline by six months or longer. You should not distribute assets until you receive IRS clearance if your estate approaches this threshold. Real property sales complicate matters further-all sale proceeds flow through escrow to cover debts, taxes, and fees before beneficiaries receive anything. You must coordinate payoff statements from lienholders at least 30 days before closing to prevent delays. Under the Garn-St. Germain Act, heirs are protected from due-on-sale clauses triggered by death, so mortgages can be assumed or paid from sale proceeds without acceleration. You still need written confirmation from each lender that no acceleration will occur once you notify them of the death.

Property and Asset Transfers

You must collect signed receipts from each beneficiary and file them with the court before you can obtain your final discharge. For real property, you must record the Judgment of Final Distribution in the county recorder’s office where the property sits; if property spans multiple counties, you must record in each one. Bank accounts and investment accounts transfer through beneficiary designation forms provided by the financial institution-you should not attempt to transfer these yourself without guidance from the institution, as improper transfers can trigger tax consequences or create title problems. If you are distributing to minors, you must establish a blocked account or guardianship arrangement; never transfer assets directly to a minor’s name. The Franchise Tax Board requires a clearance certificate if your estate exceeds $1 million and assets distribute to nonresidents, so you should request this certificate at least 60 days before your final distribution hearing.

Resolving Beneficiary Disputes

Disputes among beneficiaries surface most often when the will is ambiguous, when one beneficiary claims a lifetime gift should reduce their inheritance, or when beneficiaries disagree on property valuations. California Probate Code Sections 21135 and 6409 address these issues-ademption by satisfaction covers lifetime gifts that may reduce a bequest, and advancements cover gifts the deceased intended as early distributions against inheritance. You must resolve these questions before filing your petition for final distribution; if beneficiaries cannot agree, the court will decide at the final distribution hearing, which adds 60 to 90 days to your timeline. You should document all beneficiary communications in writing and obtain written acknowledgment of distributions to prevent later claims of fraud or mismanagement.

Final Thoughts

Probate closing procedures in Southern California demand precision and knowledge of court rules that vary between counties. Missing a filing deadline, omitting a schedule from your accounting, or failing to notify a beneficiary can delay closure by months and expose you to personal liability. A $1 million estate carries roughly $46,000 in statutory fees alone, and errors compound those costs through extended administration and potential surcharge claims.

We at Law Offices of Roshni T. Desai have guided families through probate closing for over 25 years across Los Angeles, Orange, San Diego, Riverside, and San Bernardino counties. Our firm prepares your final accounting, files your petition for final distribution, coordinates with the court, and guides you through asset transfers and discharge. We handle the practical details: obtaining Franchise Tax Board clearance, recording deeds, collecting beneficiary receipts, and filing your affirmation of final discharge.

Questions often arise after probate settlement closes about tax reporting, trust administration, or elder law planning for other family members. Contact Law Offices of Roshni T. Desai for a free consultation with flexible home or office visits so you can discuss your situation without pressure.