Probate Property Tax Planning: Smarter Strategies for California Estates

California property owners face a harsh reality: when you pass away, your heirs often face immediate property tax reassessment that can dramatically increase their tax burden. Proposition 13 protections disappear, and without proper planning, your family could lose significant wealth to taxes.

We at Law Offices of Roshni T. Desai have helped countless California families reduce this tax hit through smart probate property tax planning. This guide walks you through proven strategies that work within California’s unique tax system.

What Happens to Property Taxes When You Die

Reassessment at Death: The Proposition 13 Cliff

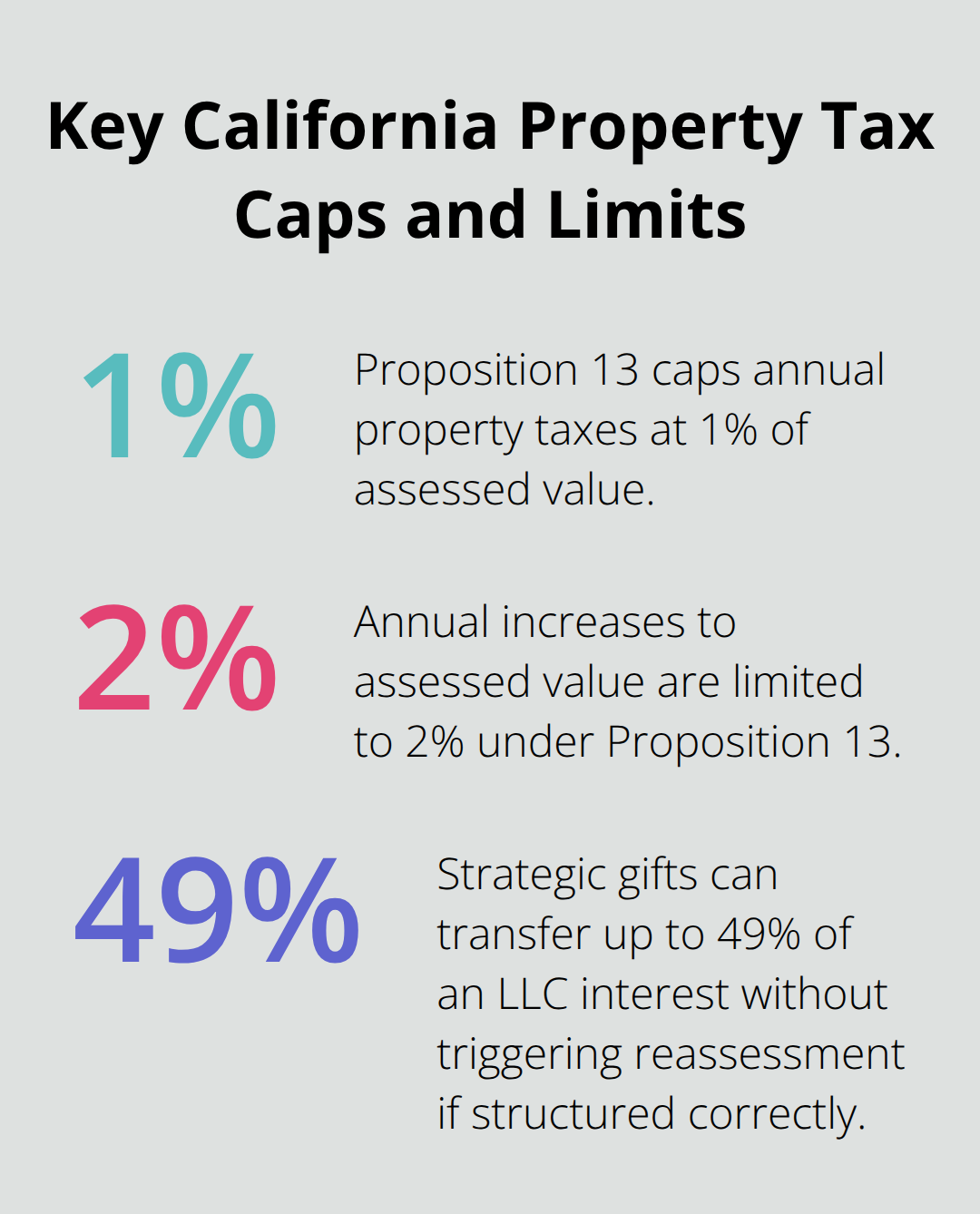

Death triggers California’s harshest property tax reality: reassessment. Under Proposition 13, passed in 1978, property taxes stay capped at 1% of assessed value with annual increases limited to 2%, but this protection vanishes the moment you pass away. The county assessor treats your death as a change of ownership and resets your home’s assessed value to current market value on the date of death. For a home purchased decades ago for $300,000 and now worth $1.5 million, your heirs suddenly face taxes based on $1.5 million instead of the original purchase price plus accumulated 2% annual increases-roughly $12,000 per year in additional property taxes compared to what you were paying.

How Proposition 19 Changed the Rules

Proposition 19, which took effect February 16, 2021, eliminated most parent-to-child property transfer protections that existed before. Previously, you could transfer nearly any property to your children without triggering reassessment, but now only your principal residence qualifies for a limited exclusion. Your child must occupy it as their primary residence within one year of your death and continue living there to claim this benefit.

Non-primary residences, rental properties, and commercial real estate face full reassessment at market value when inherited.

The exclusion itself caps at $1,044,586 for transfers between February 16, 2025 and February 15, 2027 according to California Board of Equalization guidance, with the amount adjusting yearly for inflation. If your home exceeds this cap, the excess gets added to the taxable base, reducing the tax benefit significantly. A home worth $1.5 million with a $300,000 original purchase price means the excess ($455,414) adds to the child’s tax burden, creating a higher taxable value than the full exclusion would suggest.

Common Mistakes That Trigger Reassessment

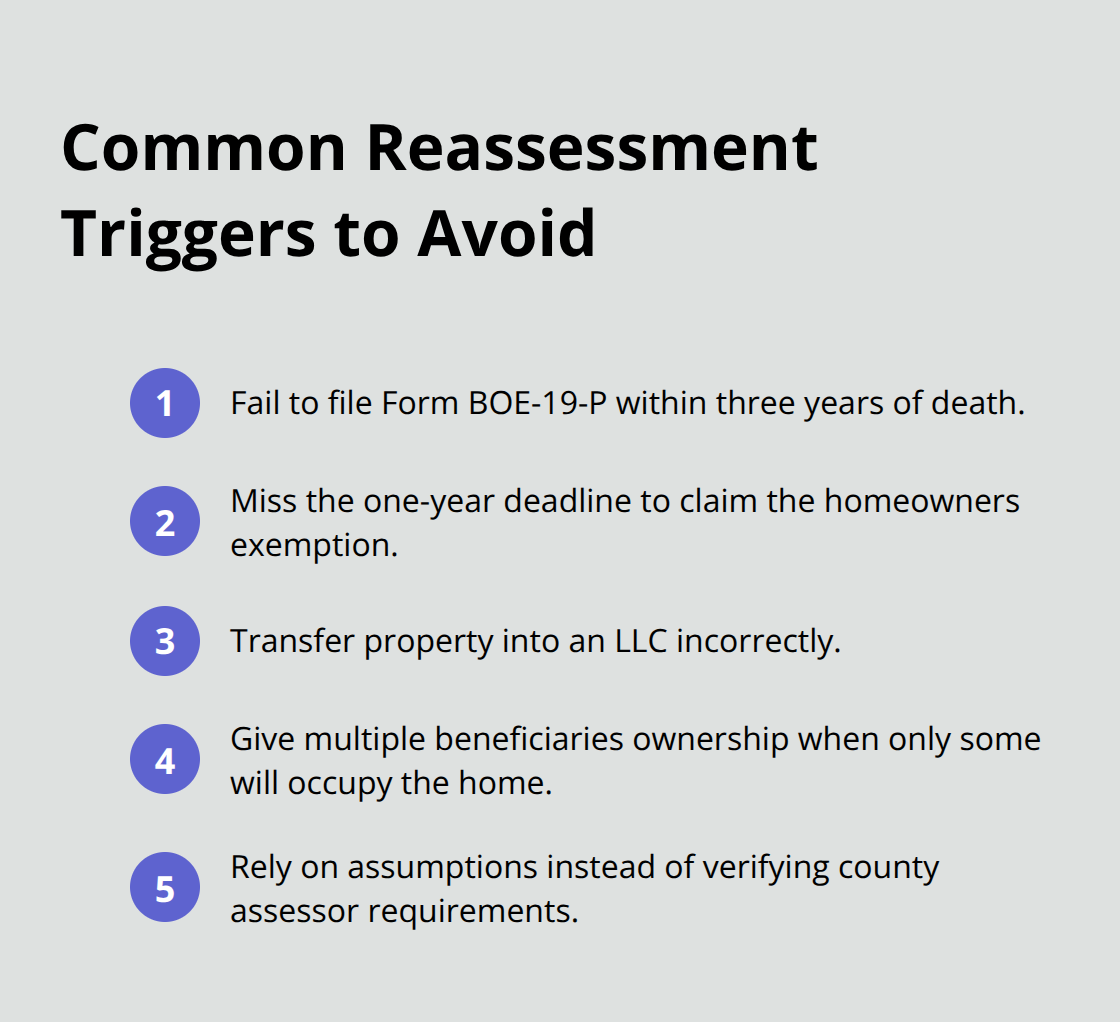

Reassessment during probate often results from preventable errors. Failing to file the required Form BOE-19-P within three years of death costs you the exclusion entirely. Missing the one-year deadline to claim homeowners exemption after transfer also eliminates protection. Placing property into an LLC incorrectly or having multiple beneficiaries where only some occupy the home creates complications that assessors scrutinize closely. These mistakes are expensive and often irreversible, which is why understanding the mechanics now prevents your heirs from inheriting a crushing tax burden later.

The path forward requires careful coordination between your estate plan and property tax strategy. Understanding which assets qualify for protection and which ones face reassessment determines whether your family preserves wealth or watches it disappear to taxes.

How to Protect Your Property From Reassessment

The Living Trust: Your Foundation for Tax Protection

The revocable living trust stands as the most reliable tool to prevent probate and preserve your Proposition 13 tax base, but only when you properly fund it with your real property. A living trust alone accomplishes nothing; you must transfer the deed to the trust’s name to gain protection. When your home sits in the trust rather than your individual name, the county assessor does not treat your death as a change of ownership. Your heirs then inherit the property at your original assessed value rather than current market value. This single step saves your family tens of thousands in annual property taxes. A home purchased for $400,000 and now worth $2 million avoids reassessment if held in a funded trust, keeping your heirs’ tax bills based on roughly $500,000 in assessed value instead of $2 million.

The catch appears frequently: many people create a trust but never transfer the title, leaving the property in their individual name. This defeats the entire purpose. We at Law Offices of Roshni T. Desai observe this mistake repeatedly, and it costs families dearly.

Claiming the Parent-Child Exclusion Under Proposition 19

Proposition 19’s parent-child exclusion offers a second layer of protection if your principal residence qualifies, but the rules demand strict compliance and the exclusion amount matters significantly. Your child must move into the home as their primary residence within one year of your death and file Form BOE-19-P with the county assessor within three years to claim the benefit. The exclusion caps at $1,044,586 for transfers through February 15, 2027, according to California Board of Equalization guidance.

If your home’s market value exceeds this cap plus your original purchase price, the excess becomes part of your child’s taxable base. A $2 million home with a $300,000 original cost means the child’s taxable value jumps to roughly $1,344,586 instead of the full $2 million, still delivering meaningful savings but less than the exclusion alone suggests. Timing matters critically: if your child delays occupancy beyond one year or fails to file the homeowners exemption within that first year, the exclusion vanishes entirely. The three-year filing window for Form BOE-19-P provides some cushion, but waiting invites mistakes and creates unnecessary risk.

Protecting Non-Primary Residences and Rental Properties

Non-primary residences and rental properties receive no Proposition 19 protection; they face full reassessment at market value when inherited. For these assets, different strategies apply. Structuring ownership through an LLC often preserves the Proposition 13 base and avoids triggering reassessment when interests transfer to heirs. The mechanics are complex, and professional guidance during your lifetime prevents your family from inheriting both property and a tax disaster.

The next section explores how to coordinate these strategies with federal tax planning and work with professionals who understand both state and federal implications of your choices.

Advanced Tax Strategies for High-Value California Estates

The Stepped-Up Basis Advantage at Death

For California estate owners with substantial property holdings, the stepped-up basis rule represents one of the most powerful tax advantages available at death. When you pass away, your heirs inherit property at its fair market value on the date of death, not at your original purchase price. If you bought a rental property for $600,000 and it appreciates to $1.8 million by the time you die, your heirs inherit it with a $1.8 million basis. Should they immediately sell the property, they owe capital gains tax only on appreciation after your death, not the $1.2 million gain that occurred during your lifetime. For a $1.2 million unrealized gain, this step-up eliminates roughly $180,000 to $240,000 in federal capital gains taxes depending on their tax bracket. This benefit applies automatically to all property in your estate, making it far more valuable than any lifetime gifting strategy for assets that will appreciate significantly before your death.

Strategic Lifetime Gifting for Federal Tax Reduction

This does not mean you should ignore lifetime gifting for high-value estates. Strategic gifts before death reduce your taxable estate and can shrink the amount subject to federal estate taxes if your net worth exceeds roughly $13.61 million according to 2024 federal exemption levels. The federal exemption drops substantially in 2026 unless Congress extends current law, potentially falling to around $7 million per person. For estates approaching these thresholds, gifting appreciating assets like LLC interests in real property during your lifetime accomplishes two goals: it removes future appreciation from your taxable estate, and it can preserve California property tax protections if structured correctly.

Transferring up to 49 percent of an LLC holding a rental property to your children over several years keeps any single child below the 50 percent ownership threshold that would trigger reassessment, while also removing that property’s future appreciation from your federal taxable estate. A property worth $2 million today that appreciates to $3 million by your death saves your estate roughly $150,000 in federal taxes if you gifted just the appreciating portion during your lifetime.

Coordinating Federal and State Tax Planning

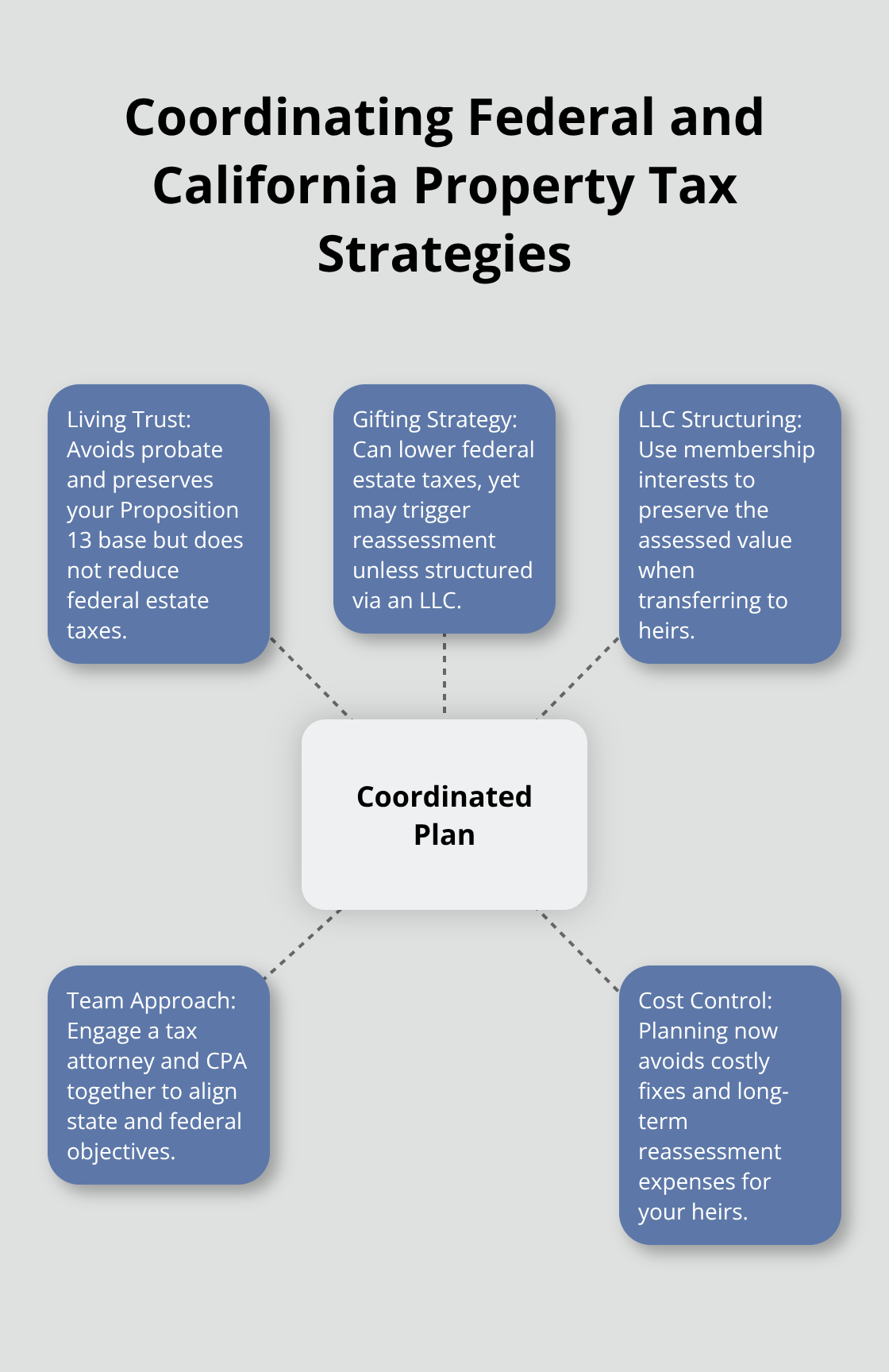

Coordinating these federal and state strategies requires understanding how each affects the other. A living trust prevents probate and protects your Proposition 13 base, but it does not reduce your federal taxable estate for estate tax purposes. Gifting reduces federal estate taxes but can trigger California property tax reassessment if not structured carefully through an LLC. Working with a tax attorney and a CPA together, rather than separately, ensures your plan achieves both goals without creating unintended consequences.

The cost of fixing a poorly designed strategy after your death often exceeds the cost of planning correctly beforehand. A misstep in LLC structuring might cost $5,000 to $10,000 in professional fees to correct, while the reassessment consequences could cost your heirs $50,000 to $100,000 or more in additional property taxes over time. We at Law Offices of Roshni T. Desai recommend this coordinated approach because the interaction between state and federal rules creates complexity that demands careful attention from the start.

Final Thoughts

Probate property tax planning in California demands attention to detail and timing. The strategies outlined in this guide-funding your living trust, claiming parent-child exclusions under Proposition 19, structuring non-primary residences through LLCs, and coordinating federal stepped-up basis rules with state tax protections-work together to preserve your family’s wealth. A single mistake, like failing to file Form BOE-19-P within three years or missing the one-year occupancy deadline, costs your heirs tens of thousands in unnecessary taxes.

Your next step involves honest assessment of your current situation. Do you own multiple properties across California? Is your estate approaching federal tax thresholds? Are your beneficiaries clear about occupancy plans for inherited homes? These questions determine which strategies apply to your family, and many California estate owners discover gaps in their plans only after death, when options narrow and costs multiply.

We at Law Offices of Roshni T. Desai understand the intersection of California property tax law and estate planning because we work with families navigating these exact decisions. Contact Law Offices of Roshni T. Desai today to schedule your free consultation and take control of your family’s financial future.