Trust Accounting Basics: A Clear Roadmap for Heirs

Inheriting assets through a trust can feel overwhelming, especially when you’re trying to understand what’s happening with your money. Trust accounting basics matter because they show you exactly where your funds are, how they’re being managed, and when you’ll receive distributions.

At Law Offices of Roshni T. Desai, we’ve seen heirs struggle with confusing statements and unclear fee breakdowns. This guide walks you through what trust accounting actually is and what rights you have as a beneficiary.

What Trust Accounting Actually Means

Trust accounting is a financial report that tracks every dollar moving in and out of a trust after someone dies. It shows the trust’s opening balance, all income received, every expense paid, distributions to beneficiaries, investment gains or losses, and the closing balance. This isn’t optional paperwork-California Probate Code Section 16062 requires trustees to provide annual accountings to beneficiaries, and some trusts demand more frequent reports. The trustee documents everything with precision because beneficiaries have a legal right to see exactly how their inheritance is being managed.

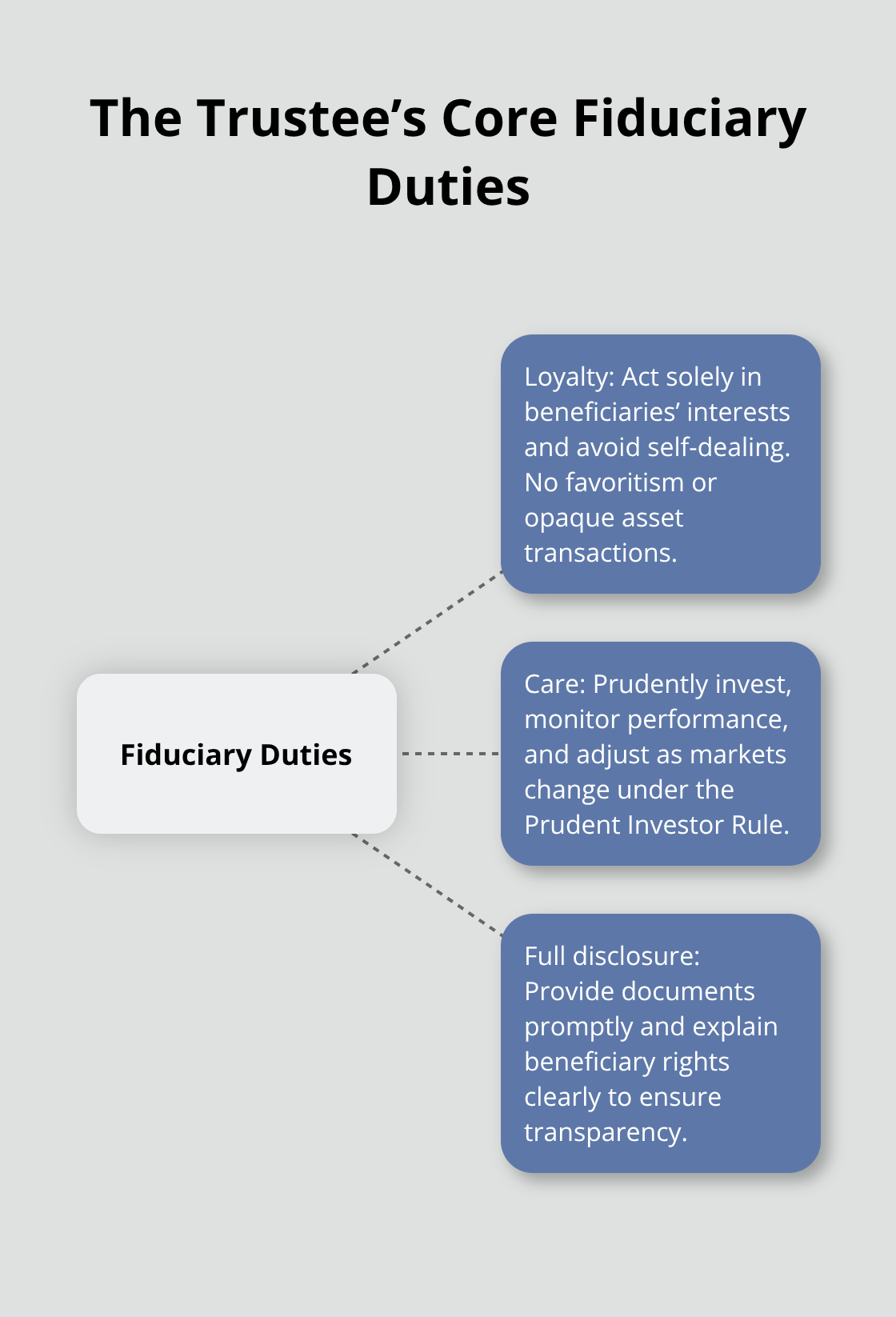

The Three Fiduciary Duties That Drive Disclosure

Fiduciary duty under California law rests on three core obligations: loyalty, care, and full disclosure. Loyalty prohibits the trustee from borrowing from the trust, buying or selling assets without full transparency, or favoring one beneficiary over another. Care requires the trustee to monitor investments and adjust them as market conditions shift, following what’s called the Prudent Investor Rule. Full disclosure is where trust accounting comes in-the trustee must provide beneficiaries with copies of relevant trust documents and explain their rights clearly.

When a trustee fails at any of these duties, beneficiaries can challenge the accounting in probate court. This process involves gathering evidence, organizing documents, and potentially filing a formal petition. Breaches of fiduciary duty carry serious consequences: the trustee can be removed and forced to repay mismanaged funds.

Comparing Accountings to Bank Statements

When you receive a trust accounting, compare it directly to the trust’s actual bank statements. Look for deposits, withdrawals, and transfers that match what the accounting claims. If a distribution appears in the accounting but not on the bank statement, that signals potential errors or worse. Check that distributions follow the trust terms exactly-if the trust specifies income goes to one person and principal to another, verify that’s what happened.

Unexplained charges or transactions that don’t fit the trust’s provisions deserve immediate attention. Cross-checking statements catches discrepancies early and prevents disputes from escalating into costly litigation.

Taking Action When You Spot Problems

If you spot discrepancies, start by asking the trustee directly for clarification. If the trustee cannot explain the issue satisfactorily, contact a trust attorney or financial advisor who can interpret the statements and guide your next steps. Professional advisors (accountants, financial planners, and trust attorneys) provide essential support in understanding complex statements, ensuring tax compliance, and protecting your rights.

Engaging professionals helps transform confusion into clarity. These advisors demystify the accounting and safeguard assets for future generations. The complexity of trust accounting makes professional guidance invaluable-especially when questions arise about what should be included in statements or whether you can demand more frequent accountings under California law and your trust’s specific terms.

Key Components of Trust Account Statements

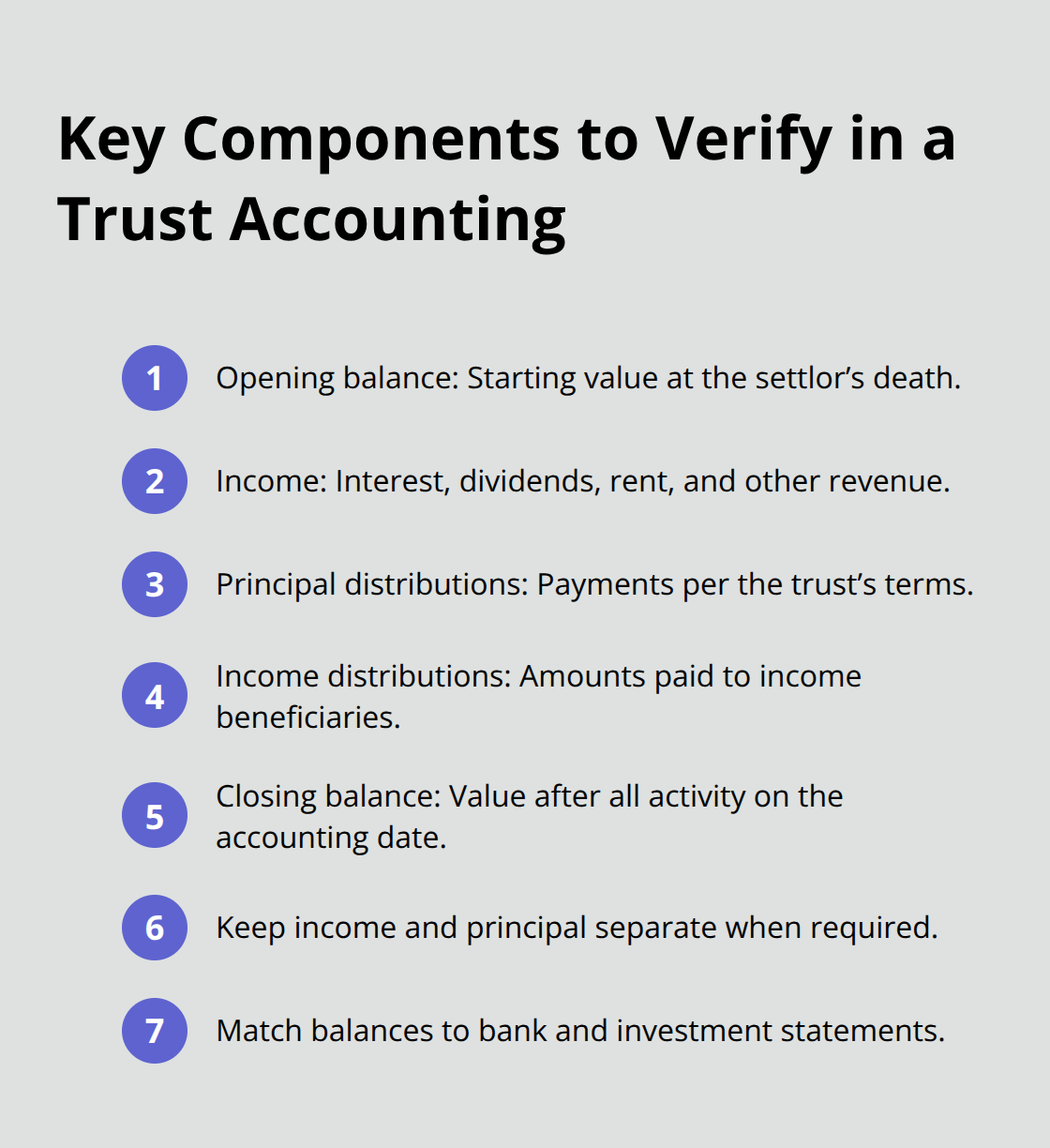

Trust accountings break down into three main sections that directly affect your money. The opening balance shows what the trust held when the settlor died-this is your starting point for understanding whether assets have grown or shrunk. Income includes everything the trust earned: interest from bank accounts, dividends from stocks, rent from rental properties, and any other revenue sources. Principal distributions are withdrawals paid to beneficiaries according to the trust terms, while income distributions go to income beneficiaries specifically.

The closing balance reflects the trust’s value after all activity, and this number should match the trust’s actual bank and investment account balances on the accounting date. When you review your statement, verify that income and principal stayed separate if your trust requires it-mixing them signals mismanagement or violation of trust language.

Identifying Legitimate and Questionable Fees

Trustee compensation is the most common fee, and California law allows reasonable compensation based on the work involved and the trust’s size. A trustee managing a $500,000 trust with straightforward distributions typically charges 0.5% to 1% annually, while a $2 million trust with complex investments might run 1% to 1.5%. This means a $1 million trust could legitimately cost $5,000 to $15,000 per year in trustee fees alone. Beyond trustee compensation, accounting fees from CPAs preparing trust tax returns typically range from $1,500 to $3,500 annually depending on complexity. Investment management fees, if the trust uses a professional manager, usually run 0.5% to 1.5% of assets under management. Every fee must appear in the accounting with clear explanation-vague line items like miscellaneous charges or administrative fees without detail are red flags. Ask the trustee to itemize what professional services were provided and why. If a trustee charged $8,000 in fees to manage a straightforward $300,000 trust with minimal activity, that’s excessive and worth challenging. California Probate Code Section 16062 requires transparency on compensation, so demand specificity.

Matching Asset Values to Market Reality

The accounting lists every asset the trust holds with its value as of the accounting date. Real estate should show an appraised value or recent market assessment-if the property hasn’t been professionally valued in over two years and the trust still lists a stale 2022 appraisal, push for an updated valuation. Stocks and mutual funds must reflect actual market prices on the date the accounting was prepared, not old cost basis figures. Bank account balances should match statements to the penny. If the trust holds a business interest or rental property, the trustee must provide documentation of how that value was determined. Request the source of every valuation rather than accepting round numbers without backup. An accounting that shows a commercial building valued at exactly $500,000 for three consecutive years despite market changes needs explanation. These valuations matter because they determine how much each beneficiary ultimately receives and whether the trustee is being truthful about trust performance. Missing valuations or outdated appraisals suggest the trustee isn’t monitoring the trust properly under the Prudent Investor Rule.

Spotting Red Flags in Your Statement

Unexplained charges or transactions that don’t fit the trust’s provisions deserve immediate attention. Cross-check the accounting against the trust’s actual bank and investment statements-look for deposits, withdrawals, and transfers that match what the accounting claims. If a distribution appears in the accounting but not on the bank statement, that signals potential errors or misappropriation. Vague descriptions of expenses, missing documentation for large transactions, or fees that seem disproportionate to the trust’s size all warrant questions. When you spot discrepancies, start by asking the trustee directly for clarification. If the trustee cannot explain the issue satisfactorily, contact a trust attorney or financial advisor who can interpret the statements and guide your next steps. Professional advisors provide essential support in understanding complex statements, ensuring tax compliance, and protecting your rights. Engaging professionals transforms confusion into clarity and safeguards assets for future generations.

Common Issues Heirs Face with Trust Accounting

Heirs frequently encounter three concrete obstacles when reviewing trust accountings: trustees who provide vague documentation that leaves questions unanswered, disagreements over what fees are reasonable and what distributions should have been made, and accountings that arrive months or years late. These aren’t minor annoyances-they directly affect your money and your ability to verify that the trustee follows the law. Vague documentation happens when a trustee submits an accounting with line items like administrative costs or professional fees without itemization, forcing you to guess what work was actually performed and why it cost that amount. A trustee might charge $5,000 for accounting services without specifying whether a CPA prepared tax returns, reconciled accounts, or both. When you ask for details, some trustees respond with defensiveness rather than clarity, which signals either incompetence or intentional obfuscation. California Probate Code Section 16062 requires trustees to provide transparent accountings, so vague descriptions violate the law.

Disputes Over Distributions and Fees

Disputes with the trustee typically emerge over three issues: unexplained delays in distribution, suspicious fees or expenses, or evidence that the trustee interpreted trust terms differently than you would. A trust might specify that income goes to a surviving spouse while principal goes to adult children, but the trustee decides to retain income for reinvestment without clear authorization. That decision directly reduces what the spouse receives and increases what remains for later distribution. Similarly, fee disputes explode when a trustee charges 1.5% annually on a $2 million trust (roughly $30,000 per year) without justifying why that rate applies when the trust requires minimal active management. Many heirs accept whatever fees appear on the accounting simply because they don’t understand what’s reasonable-but California law requires those fees to be proportionate to the work performed and the trust’s complexity.

Delays in Receiving Statements and Payments

Delays in receiving statements and payments represent a major problem and often indicate disorganization or deliberate foot-dragging. California law requires trustees to provide annual accountings within a reasonable timeframe after the trust year ends, but some trustees take six months or longer to produce them. During that delay, beneficiaries cannot verify distributions, cannot detect errors, and cannot plan their finances with certainty.

A beneficiary waiting for a principal distribution that should arrive within months might face financial hardship while the trustee procrastinates. Delays compound when the trustee hasn’t yet paid final taxes, settled creditor claims, or resolved unclear trust language-but these delays should be communicated proactively, not hidden until the beneficiary demands answers.

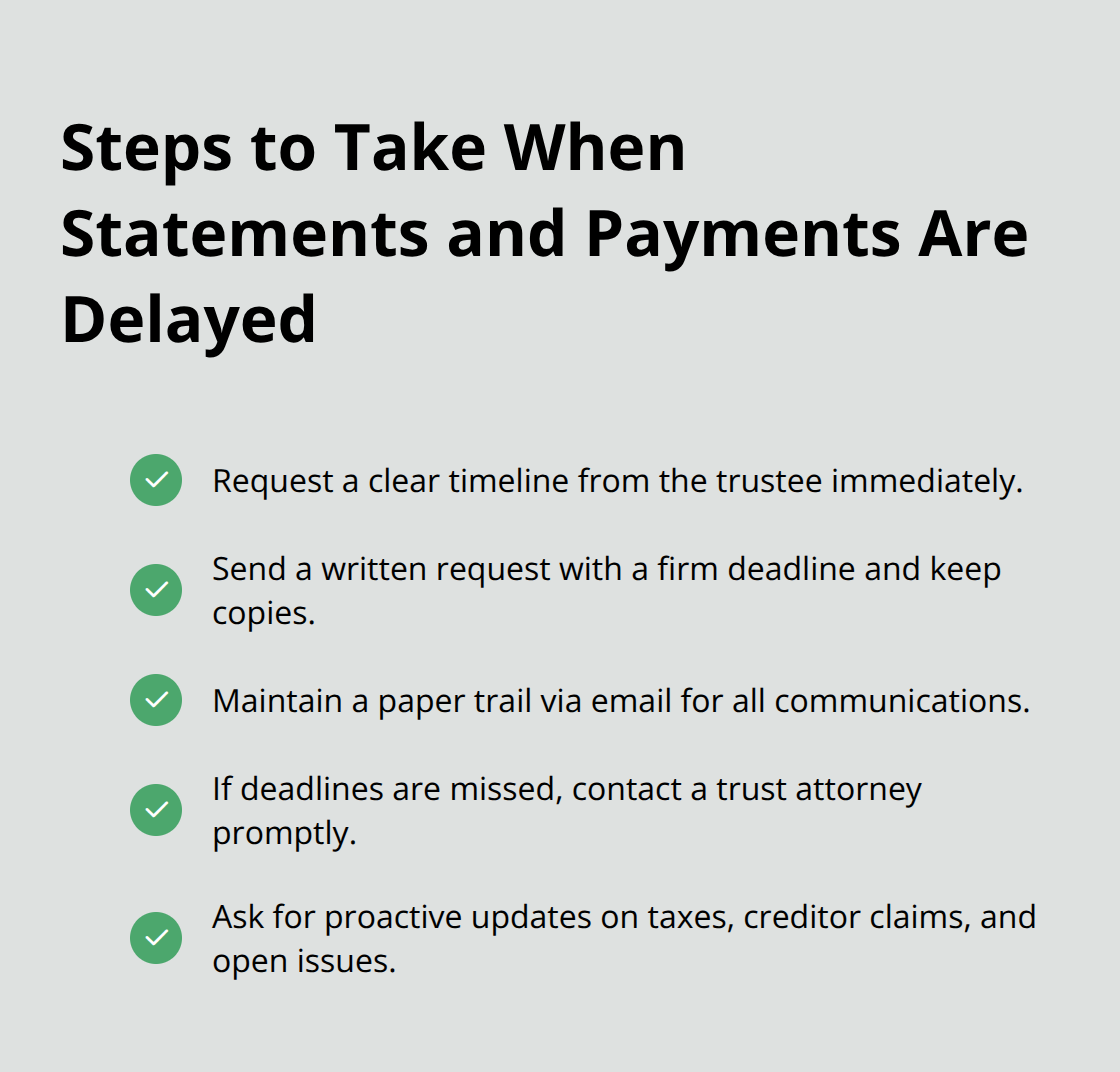

Taking Action Against Delays and Vague Documentation

If you receive an accounting more than four months after the trust year ends without prior explanation, push back immediately and request a timeline for when you’ll receive payment. Some trustees also delay providing statements because they’ve made questionable transactions and hope beneficiaries won’t notice. When you spot delays, send a written request for the accounting and specify a deadline-email works fine and creates a paper trail. If the trustee misses that deadline, contact a trust attorney because the law is clearly on your side. Delays also prevent you from catching errors early; an accounting delivered 18 months late makes it harder to reconstruct what actually happened and whether the trustee made mistakes. The longer you wait, the colder the trail becomes and the harder it is to prove wrongdoing if you need to challenge the accounting in probate court.

Unclear Documentation and What It Reveals

Unclear documentation happens when a trustee submits an accounting with line items like administrative costs or professional fees without itemization. This forces you to guess what work was actually performed and why it cost that amount. A trustee might charge $5,000 for accounting services without specifying whether a CPA prepared tax returns, reconciled accounts, or both. When you ask for details, some trustees respond with defensiveness rather than clarity, which signals either incompetence or intentional obfuscation. California Probate Code Section 16062 requires trustees to provide transparent accountings, so vague descriptions violate the law. Request itemized invoices from any professional the trustee hired and ask the trustee to explain exactly what services those professionals performed. If the trustee cannot or will not provide this documentation, that refusal itself is a red flag that warrants legal attention.

Final Thoughts

As a beneficiary, California law grants you concrete rights. You can demand trust accountings within a reasonable timeframe, understand exactly how your inheritance is being managed, and challenge any accounting that doesn’t add up. The trustee cannot hide behind vague documentation or delay payments indefinitely. Understanding trust accounting basics empowers you to verify that the trustee follows the law and protects your interests.

You should not accept confusing statements or questionable fees without pushback. Ask direct questions first, request itemized invoices, demand explanations for unexplained charges, and cross-check statements against actual bank records. Many trustee errors stem from disorganization rather than intentional wrongdoing, and direct communication often resolves issues quickly. When direct communication fails or when you spot serious discrepancies, a trust attorney can interpret complex statements, identify potential breaches of fiduciary duty, and advise whether you have grounds to challenge the accounting in probate court.

We at Law Offices of Roshni T. Desai understand that trust administration creates stress for heirs already dealing with loss. If you’re uncertain about an accounting you’ve received or need help understanding your rights, contact us for a free consultation. We serve Southern California and offer flexible home or office visits to make this process easier for you.