Trust Administration and Real Estate: Streamlining Property Transfers

Selling property held in a trust involves far more complexity than a standard real estate transaction. Timing delays, conflicting beneficiary interests, and tangled documentation create obstacles that most trustees aren’t prepared to handle.

We at Law Offices of Roshni T. Desai have seen how trust administration and real estate challenges intersect-and how the right approach removes friction from the entire process. This guide walks you through the problems trustees face and the practical solutions that actually work.

Why Trust Administration Complicates Property Sales

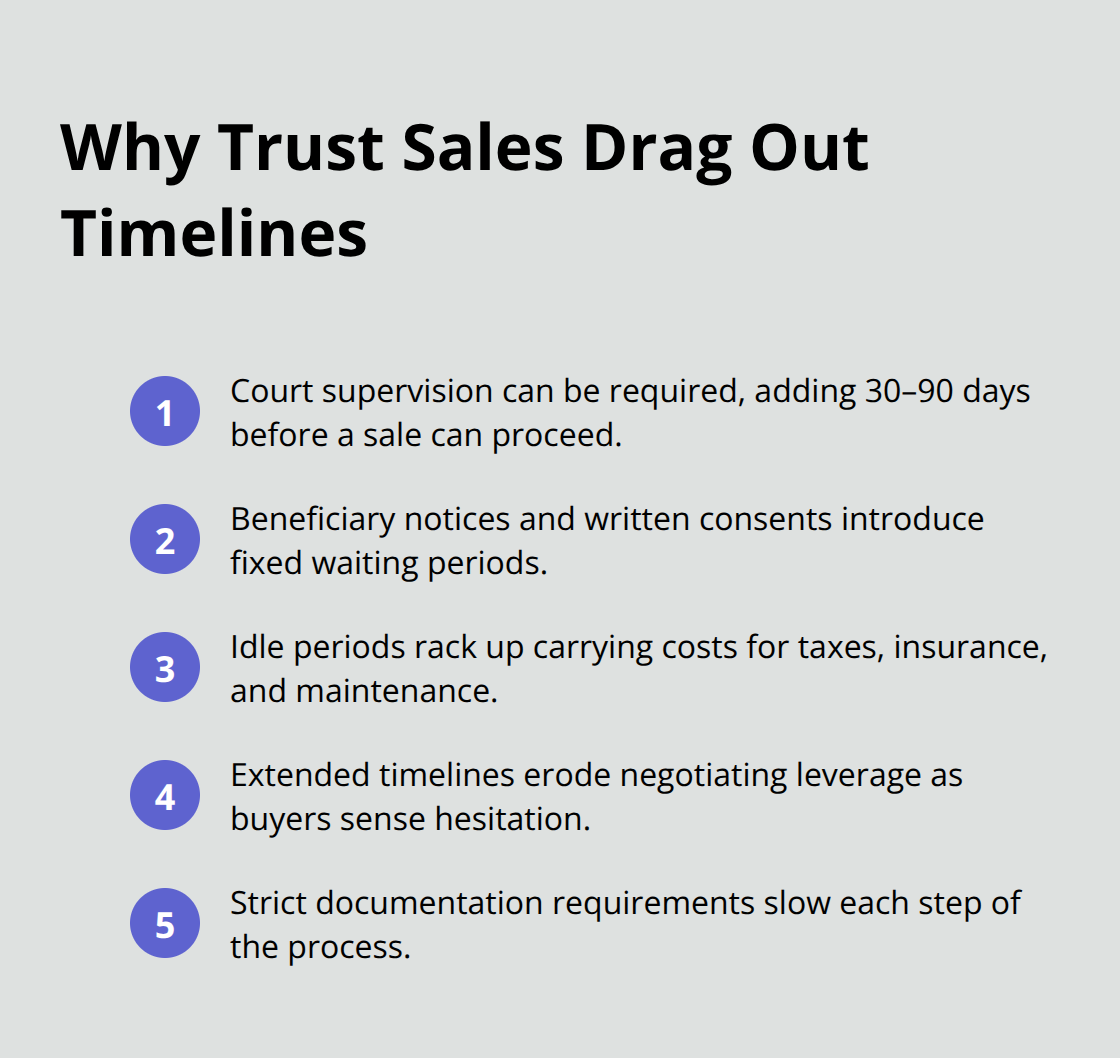

Trust property sales take longer than standard real estate transactions because multiple legal and administrative requirements collide. Probate trustees must wait for court approval in many states before selling trust-held real estate, and this approval process alone can stretch 30 to 90 days depending on jurisdiction and whether beneficiaries object. In New York, where court-supervised probate is mandatory, trustees cannot move forward without judicial sign-off on the sale price and terms. Even in non-judicial states, trustees face strict timelines for notifying beneficiaries, gathering consent signatures, and documenting every step. The property itself often sits idle during this waiting period, accumulating carrying costs like property taxes, insurance, and maintenance that drain the estate. Trustees lose negotiating leverage because buyers sense hesitation when closing timelines stretch beyond the typical 30 to 45 days.

Documentation Creates a Bottleneck

The paperwork required to sell trust property is substantially heavier than a standard home sale. Trustees must produce the original trust document with signature pages, proof of trustee appointment, a death certificate if the grantor is deceased, beneficiary identification and consent forms, and a chain-of-title search showing how the property entered the trust. Title companies often require an affidavit of trust to confirm the trustee’s authority without revealing the full trust contents to the public. If the property has a mortgage, the lender must approve the sale and may require the loan to be paid off at closing, which creates a dependency on sale proceeds. Missing or incomplete documents force delays of weeks or months while trustees hunt through old files or request certified copies from courts. Banks and title companies will not proceed until every document is verified, and they rarely give trustees the benefit of the doubt. This gatekeeping is intentional-it protects lenders and title holders from liability-but it transforms a straightforward transaction into a document assembly project that most trustees are unprepared to manage.

Beneficiary Conflicts Block Progress

When a trust holds real estate, multiple beneficiaries often have competing interests in how and when that property sells. One beneficiary may want the house kept as a family home, while another demands immediate sale to access their inheritance. A child who grew up in the house may value it emotionally, while a financial beneficiary sees only a non-performing asset. State law requires trustees to notify all beneficiaries of the intended sale, and in some cases, beneficiaries can object or petition the court to block the transaction if they believe the trustee is acting improperly. These disputes are not academic-they force trustees to hire attorneys, file court motions, and sometimes hire appraisers to defend the sale price. The process can add three to six months to a timeline that should take two months. Trustees caught between warring beneficiaries often freeze, afraid that any decision will trigger litigation.

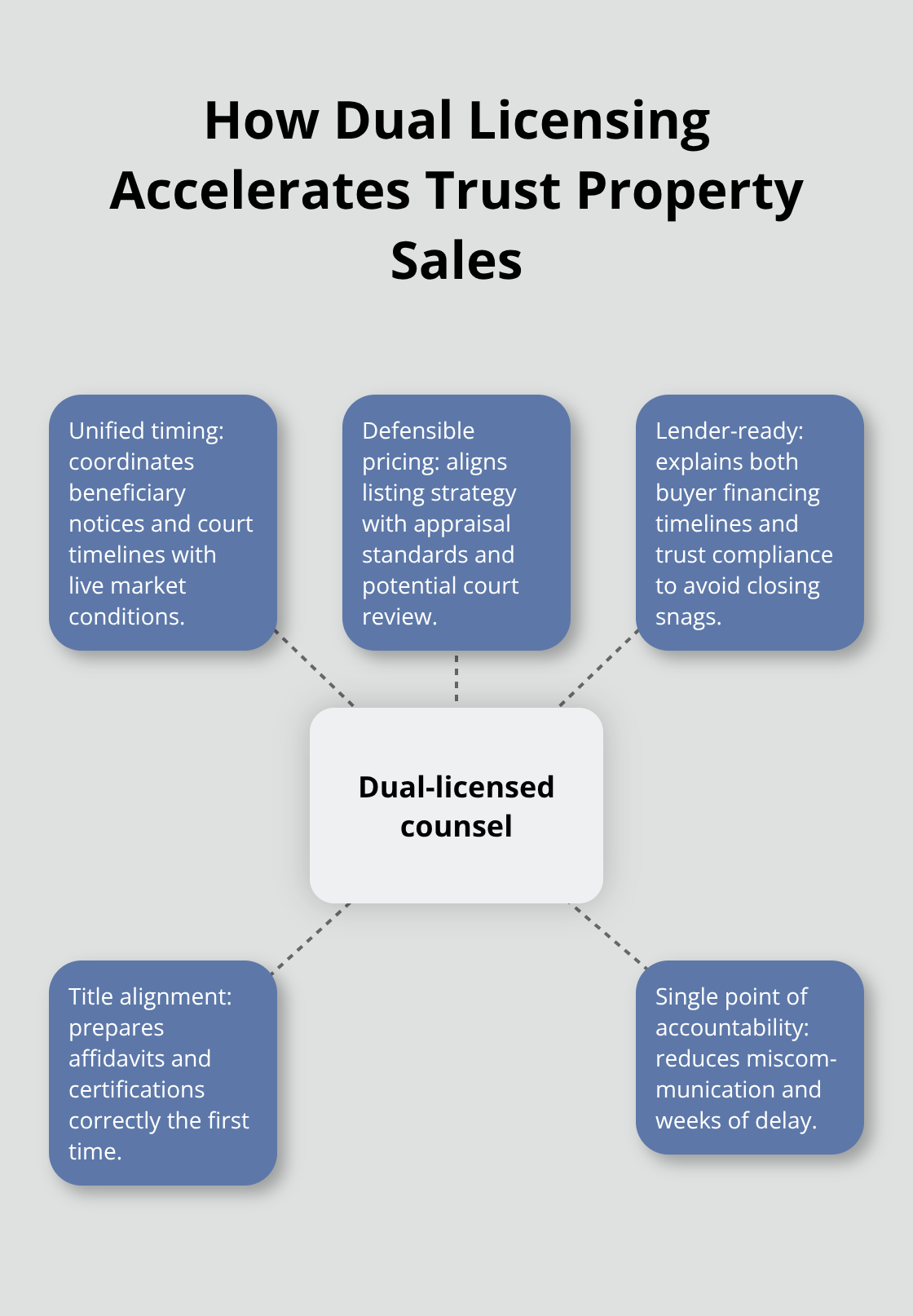

Why Dual Knowledge Matters

The intersection of trust law and real estate practice creates a gap that most professionals cannot bridge. Attorneys understand the fiduciary obligations and court requirements, but they often lack real estate market knowledge. Real estate agents understand buyer behavior and pricing, but they cannot navigate trust administration rules or beneficiary consent requirements. This separation forces trustees to coordinate between two separate professionals, each operating from incomplete information. Miscommunication between legal and real estate teams causes delays, missed deadlines, and conflicting advice about sale strategy. A professional with dual licensure as both an attorney and real estate practitioner can address trust administration requirements and market realities in a single conversation, eliminating the back-and-forth that consumes weeks. This integrated approach prevents conflicts from derailing sales and keeps the transaction moving forward.

How Dual Licensing Bridges Legal and Real Estate Gaps

When a trustee needs to sell trust property, legal requirements and real estate realities collide and create inefficiency. An attorney focused on fiduciary duties may advise waiting for court approval or gathering additional documentation, unaware that the local real estate market is cooling and buyers are disappearing. A real estate professional focused on finding buyers may push toward a quick sale without understanding that beneficiary consent forms are missing or that state law requires specific notice periods before the property can be listed. These professionals operate from different playbooks, and the trustee becomes a translator trying to coordinate two separate teams that speak different languages. The gap between legal compliance and market timing costs trustees money and months.

A professional holding both attorney and real estate licenses eliminates this disconnect. When someone advises on timing, they account for beneficiary notification deadlines and court timelines while simultaneously understanding current market conditions in your area. This integrated knowledge prevents the common mistake of timing a sale for legal convenience rather than buyer demand.

Separate Teams Create Predictable Delays

Trustees working with separate legal and real estate teams face problems that dual licensure prevents. A separate attorney may require three weeks of documentation assembly before authorizing a real estate listing, during which the market window closes. A separate agent may propose a listing price without understanding that the trustee must later justify that price in court filings or to skeptical beneficiaries, creating liability if the property sells below what a professional appraisal suggested.

Lender Coordination Requires Integrated Knowledge

The coordination gap also affects negotiations with lenders. When a mortgage encumbers the trust property, the lender needs assurance that the sale complies with trust law and that proceeds will properly pay down the loan. An attorney alone cannot explain the buyer’s financing timeline; a real estate agent alone cannot explain the lender’s trust administration requirements. A dual-licensed professional addresses both concerns in conversations with the lender, preventing last-minute complications at closing.

Title Insurance and Documentation Alignment

Title companies often flag trust-held properties as higher risk and demand affidavits, trust certifications, or additional documentation. A professional understanding both title insurance requirements and trust law can prepare these documents correctly the first time, avoiding the delays that come from back-and-forth corrections. This alignment matters because title companies will not move forward until every document satisfies their standards, and they rarely give trustees the benefit of the doubt.

The practical outcome is measurable: trustees working with a single integrated professional report faster timelines and lower legal costs compared to those coordinating separate teams. These efficiency gains matter most when beneficiary disputes threaten to derail the sale entirely, which is exactly the problem we address in the next section.

Common Problems Trustees Face When Selling Trust Property

Trust property sales trigger tax obligations that trustees often underestimate, and the reporting requirements vary depending on whether the property sits inside or outside the probate estate. When a trustee sells trust-held real estate, the trust itself may owe capital gains tax on the appreciation between the date the grantor died and the date of sale. The stepped-up basis rule provides relief here-property held in a trust at death receives a new cost basis equal to its fair market value on the date of death, which eliminates capital gains tax on appreciation that occurred during the grantor’s lifetime. However, any appreciation after death remains taxable. A property worth $500,000 on the grantor’s death date that sells for $550,000 six months later triggers a $50,000 capital gain subject to trust-level income tax at rates as high as 37 percent, depending on trust income and state tax law. The trustee must file a federal income tax return for the trust, report the sale on Schedule D, and coordinate with a tax professional to understand the tax impact and plan for distributions that account for capital gains liability. State-level reporting varies significantly-New York requires trustees to file fiduciary income tax returns and may assess state capital gains tax on top of federal liability, while California imposes state income tax at rates up to 13.3 percent. Trustees who fail to file these returns face penalties and interest that compound quickly. Beneficiaries also face tax consequences because distributions of sale proceeds may trigger income tax reporting requirements, and the trustee must provide each beneficiary with a Schedule K-1 showing their share of trust income.

Tax Planning Before the Sale Closes

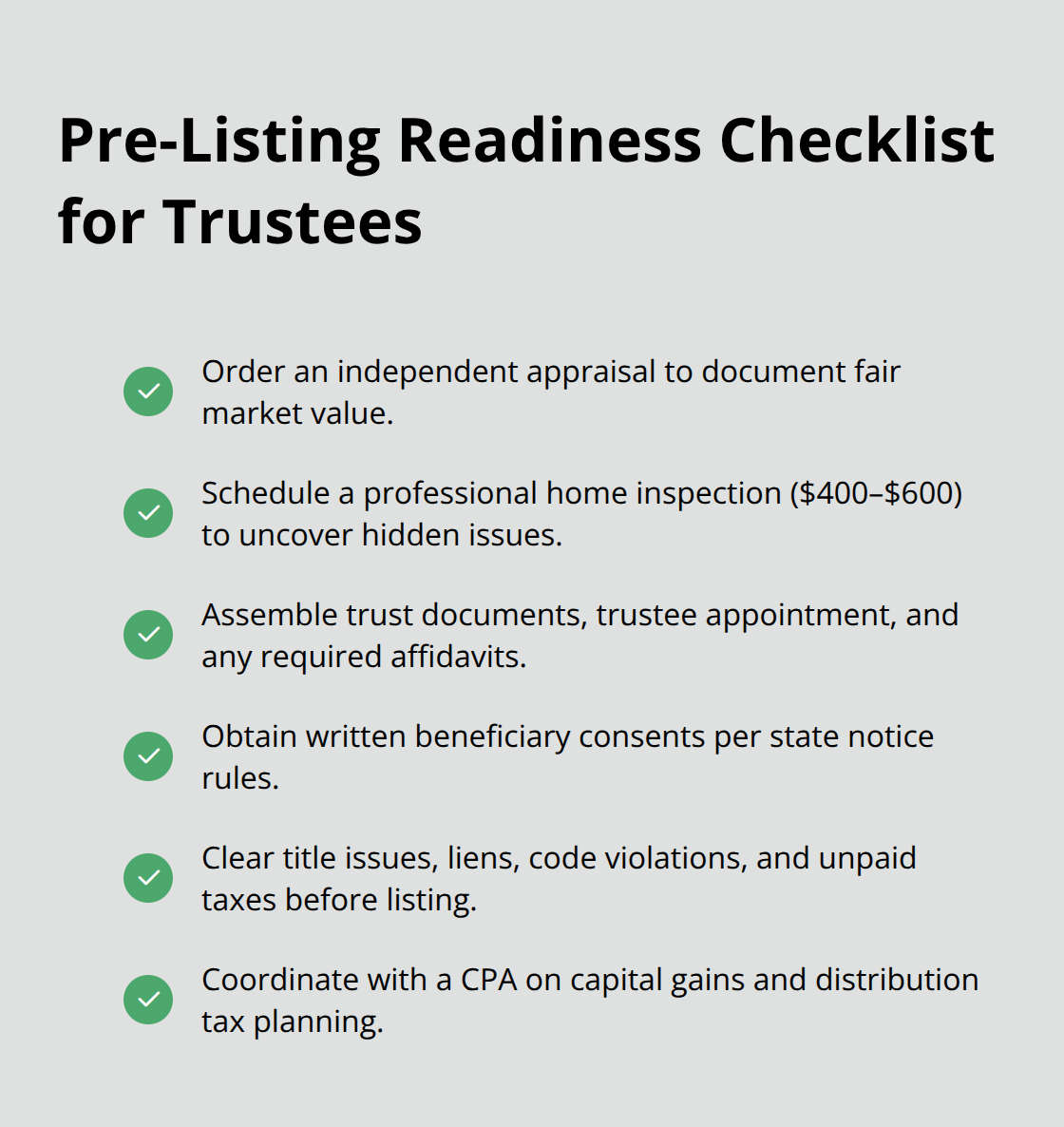

A trustee cannot simply deposit sale proceeds into a trust account and distribute them to beneficiaries without understanding the tax implications. The capital gains liability can consume 20 to 40 percent of the sale proceeds depending on appreciation and state taxes, which means a $500,000 sale may net only $300,000 to $400,000 after taxes. Trustees should coordinate with a CPA or tax attorney before listing the property to model different sale scenarios and understand how timing affects the tax bill. Some trustees benefit from spreading distributions across two tax years to keep trust income below thresholds that trigger higher tax rates, while others face immediate tax liability regardless of timing. The key is planning ahead rather than discovering tax liability after the sale closes.

Beneficiary Disputes Over Sale Price and Timing

Beneficiary disputes over property sales represent the most common reason trust property transactions stall or fail entirely. When multiple beneficiaries exist, at least one will disagree with the trustee’s decision to sell, and state law typically requires the trustee to notify all beneficiaries of the intended sale, which creates an opportunity for objections. A beneficiary who believes the trustee is selling too cheaply, selling at the wrong time, or violating the trust document’s intent can petition the court to block the sale or force a new appraisal. These disputes often hinge on property valuation-a trustee may hire an appraiser who values the property at $475,000, but a beneficiary’s independent appraisal shows $510,000, creating a $35,000 gap that feels material to heirs waiting for their inheritance. The trustee’s fiduciary duty requires acting in the beneficiaries’ best interest, which means documenting that the sale price is fair and that the decision to sell serves the trust’s purpose. Without this documentation, a beneficiary can challenge the sale in probate court, forcing the trustee to hire an attorney and defend the transaction-a process that costs $5,000 to $15,000 and delays closing by months. The practical solution is to obtain an independent appraisal before listing and to document in writing why the trustee decided to sell at that particular time. If beneficiaries object, the trustee should consult an attorney immediately rather than proceeding unilaterally.

Property Condition Assessments Prevent Surprises

Property condition assessments and valuations also create friction because the property’s actual condition often differs from what beneficiaries expect. A house that appears well-maintained on the exterior may have hidden structural, electrical, or plumbing issues that reduce its market value significantly. A professional home inspection typically costs $400 to $600 and reveals these problems before the trustee lists the property. This inspection serves two purposes: it prevents the trustee from being blindsided by buyer inspections later, and it creates documentation that justifies a lower sale price if serious defects exist. Beneficiaries are less likely to dispute a sale price when the trustee can point to a professional inspection report showing foundation cracks, roof deterioration, or HVAC system failure.

Title companies also require clear title before closing, which means the trustee may need to address code violations, unpaid property taxes, or mechanics’ liens that accumulated before the grantor’s death. Clearing these issues costs money but prevents deal collapse at closing.

Final Thoughts

Trust administration and real estate transactions demand coordination across legal compliance, market timing, and beneficiary management. Trustees who navigate these challenges alone face delays that stretch timelines from months into years, documentation gaps that halt closings, and tax surprises that consume significant portions of sale proceeds. The problems are real, but the right approach solves them.

Streamlined trust property transfers require integrated knowledge that accounts for timing, documentation accuracy, tax planning, and beneficiary concerns before they escalate. Market windows close while trustees wait for court approval or assemble documents, documentation must satisfy title companies and lenders on the first submission, capital gains liability can reduce net proceeds by 20 to 40 percent if not planned ahead, and beneficiary disputes become preventable when trustees document decisions and obtain independent appraisals. We at Law Offices of Roshni T. Desai address trust administration and real estate challenges through dual licensure as both an attorney and real estate professional, which eliminates the communication gaps that plague trustees coordinating separate teams and allows us to handle tax scenarios, documentation preparation, and beneficiary concerns before they create expensive delays.

Contact Law Offices of Roshni T. Desai for a free consultation if you are managing estate property or facing a trust-related real estate transaction. We offer flexible scheduling with home or office visits across Southern California and can walk you through the specific challenges your property presents.