Trust Administration for Families: Coordinating Assets Across Generations

Trust administration for families involves far more than simply distributing assets. When a trustee takes on this role, they’re managing legal obligations, tax considerations, and the competing interests of multiple generations simultaneously.

At Law Offices of Roshni T. Desai, we’ve seen how poor coordination between trustees and beneficiaries creates unnecessary conflict and expense. This guide walks you through the practical steps that protect family wealth and prevent costly mistakes.

What Trustees Actually Do

Trust administration starts the moment a trustee accepts the role. The work begins immediately after obtaining the death certificate. California law requires trustees to notify all legal heirs and beneficiaries within 60 days of death, providing key information about the trust and a copy of the trust document itself, as governed by Penal Code Section 16061.7. This notification triggers a critical clock: beneficiaries have 120 days to challenge the trust, or 60 days from receiving the trust copy, whichever comes later. Failure to send this notice correctly means the clock may never start, leaving the trustee exposed to challenges years down the road and creating potential personal liability.

The Initial 40-Day Period and Asset Inventory

The trustee must wait a minimum of 40 days after death before beginning formal administration in California, giving time to gather financial records and coordinate with the decedent’s accountants and financial advisors. During this period, the trustee’s first major task is creating a comprehensive inventory of all assets, including bank accounts, retirement accounts, real estate, life insurance proceeds, investments, and personal property like jewelry or art. Obtaining title to assets requires notifying financial institutions of trustee status and providing required documentation. For real property, filing an Affidavit of Change of Trustee with the county recorder enables refinancing, sale, or transfer. If retirement accounts or life insurance name the trust as beneficiary, the trustee must contact providers immediately because these assets carry significant tax consequences when distributed into a trust rather than directly to individual beneficiaries.

Setting Up the Trust’s Financial Structure

The trustee obtains a Tax Identification Number for the trust and opens a dedicated estate or trust bank account to consolidate investments and track income separately from personal funds. This separation is not optional-it forms the foundation for accurate accounting and tax filing. The trustee files a final individual income tax return for the decedent (Form 1040) and a fiduciary income tax return for the trust itself (Form 1041) once the trust becomes irrevocable upon death. For married couples, Form 706 may be filed to elect portability of the federal estate tax exemption and allocate generation-skipping transfer tax, which in 2025 stands at up to 13.99 million dollars per individual according to the IRS.

Valuation and Tax Basis Planning

Obtaining date-of-death values for all assets and securing appraisals for real property establishes accurate tax bases and asset values. In community property states like California, a surviving spouse receives a step-up in basis on all community property, which significantly reduces capital gains taxes if the trustee later sells appreciated assets. The trustee maintains annual trust accounting, whether informal or formal, documenting all assets, income received, and distributions made. Beneficiaries can request a formal accounting under state law, and transparency here prevents disputes later.

Timing Distributions and Resolving Obligations

Distributions occur only after all debts, taxes, and administrative expenses are fully resolved, which typically takes several months to a year depending on complexity. The trustee’s careful attention to these financial and legal requirements protects beneficiaries from unexpected tax bills and ensures assets transfer smoothly. Yet managing these obligations becomes significantly more complicated when families hold diverse assets across multiple states or when beneficiaries have competing interests in how and when they receive distributions.

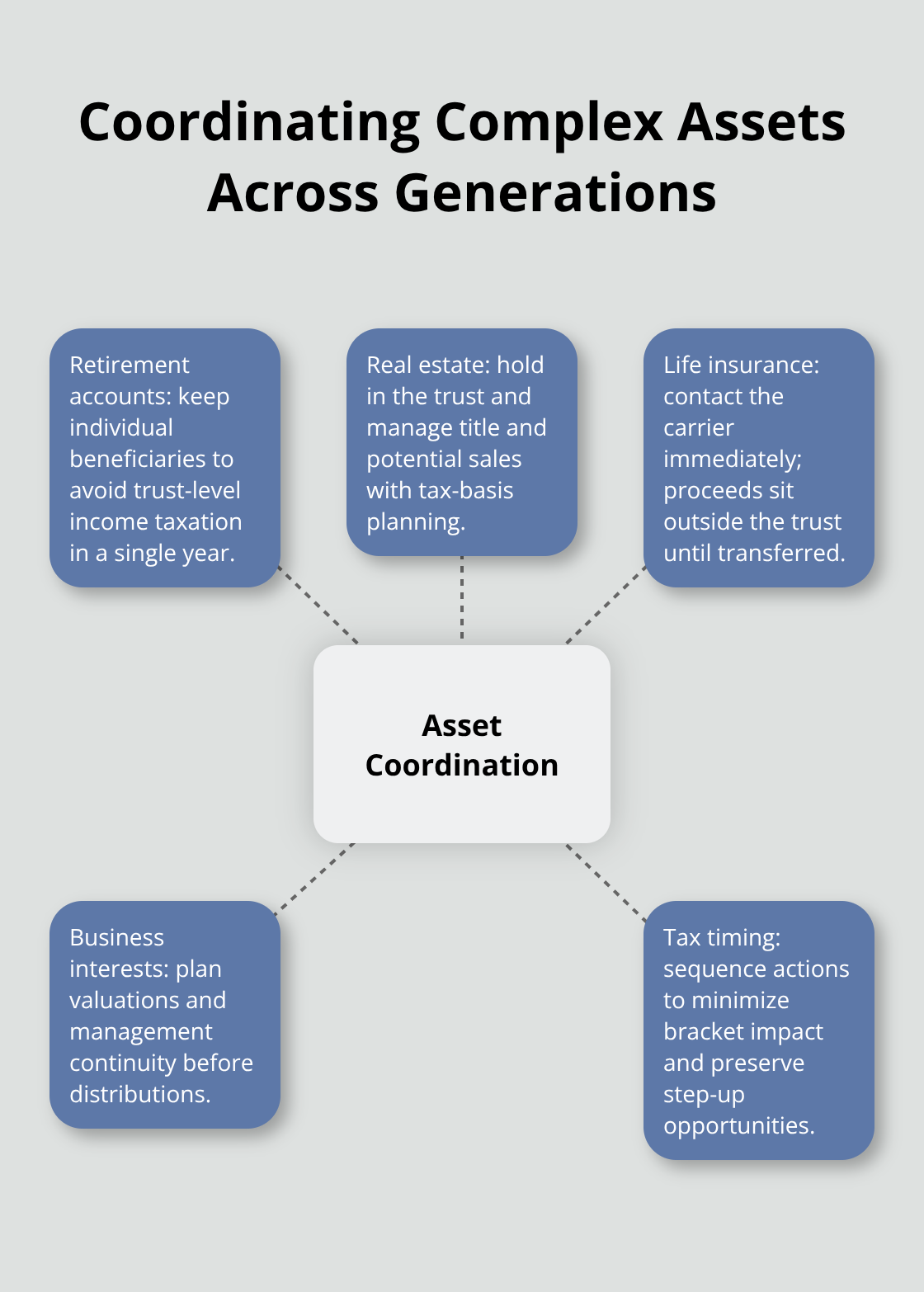

Coordinating Assets Across Multiple Generations

Multi-generational wealth transfer requires more than following a checklist. Families with assets spread across real estate in different states, retirement accounts with outdated beneficiary designations, and closely-held business interests face coordination challenges that most trustees underestimate. The Federal Reserve reported that U.S. household net worth reached record levels in 2025, driven largely by corporate equity holdings, which means many families now manage significantly more complex asset portfolios than previous generations. When these assets must transfer smoothly to children and grandchildren, poor coordination creates delays, unnecessary taxes, and family tension that can persist for years.

Mapping Assets and Understanding Tax Consequences

The first step is mapping exactly what needs to transfer and when. Retirement accounts like IRAs and 401(k)s cannot simply flow into a trust without triggering immediate tax consequences. If the trust becomes the named beneficiary instead of individual heirs, the entire account becomes taxable income to the trust in a single year, potentially pushing the trust into the highest federal tax bracket. Individual beneficiaries should remain named on retirement accounts, with the trust holding other assets like real estate and investments. For life insurance proceeds, the trustee must contact the insurance company immediately after death because these funds sit outside the trust until properly transferred. Delaying this contact costs beneficiaries months of lost investment returns on proceeds that should already be working for them.

Structuring Distributions for Different Family Members

Beneficiaries rarely have identical needs or timelines. A 25-year-old child may need immediate access to education funding while an elderly parent requires reliable monthly income and a grandchild needs assets protected until age 30. The trust document should specify how distributions address these different circumstances rather than treating all beneficiaries equally. Dynasty trusts, designed to hold assets for multiple generations, accomplish this by keeping wealth in a single governing structure while the trustee makes distributions based on individual needs and circumstances. The trustee maintains control over investments and asset management across generations, preventing beneficiaries from making poor decisions with inherited money while still supporting their legitimate needs.

Leveraging Step-Up in Basis for Tax Savings

When a surviving spouse exists, the situation becomes more complex. In California, community property law gives the surviving spouse a step-up in basis on all community property owned at death, meaning capital gains taxes on appreciated assets disappear entirely if the trustee sells those assets soon after death. Separate property receives no step-up for the surviving spouse unless specific tax elections are made on Form 706. This distinction alone can save families hundreds of thousands of dollars if the trustee understands the difference and acts accordingly. The trustee should coordinate with a tax professional before selling any appreciated assets to confirm whether a step-up applies and whether timing the sale immediately after death provides tax advantages.

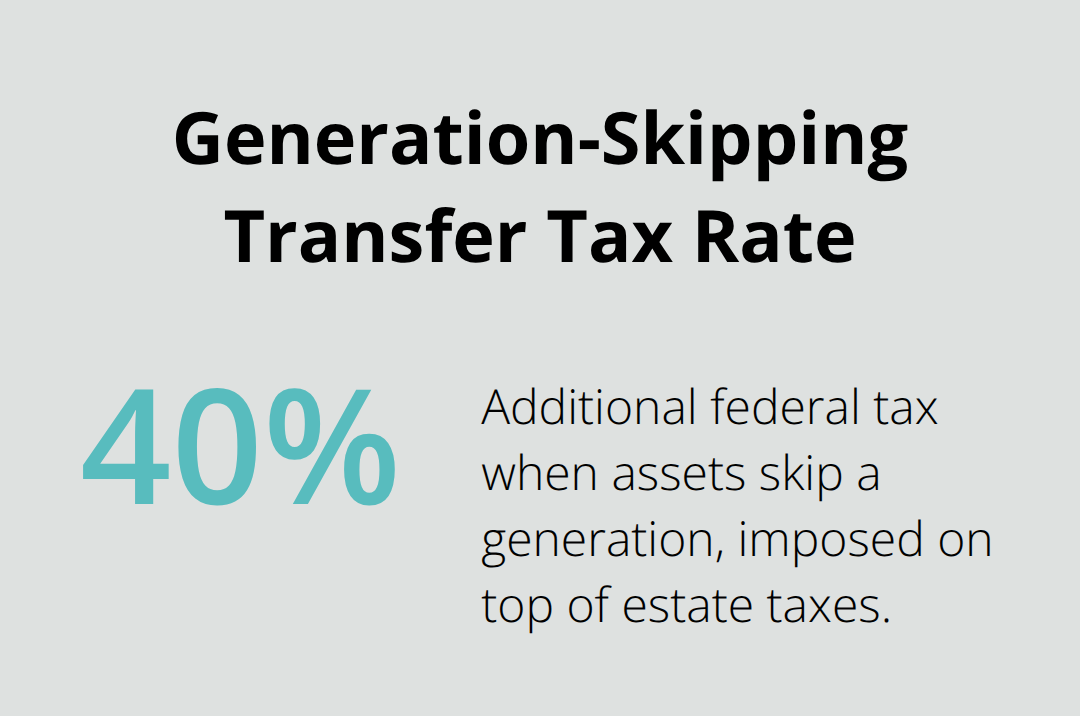

Allocating Generation-Skipping Transfer Tax Exemptions

Generation-skipping transfer tax represents a hidden cost that families often discover too late. When assets skip a generation-for example, when grandparents leave money directly to grandchildren rather than to their adult children first-the IRS imposes an additional 40% tax on top of regular estate taxes. In 2025, the federal estate tax exemption stands at 13.99 million dollars per individual according to the IRS, but generation-skipping transfer tax has its own separate exemption that does not carry over between spouses.

A married couple with a 27.98 million dollar estate can leave assets tax-free to children, but if they want to benefit grandchildren as well, the trustee must carefully allocate generation-skipping transfer tax exemptions across the trust structure. Failing to do this during the initial administration phase means the family loses the exemption permanently. Form 706, the federal estate tax return, must be filed even when no estate tax is owed, specifically to elect portability of exemptions and allocate generation-skipping transfer tax exemptions to particular trusts or bequests.

Coordinating With Professional Advisors Before Distributions Begin

Families should hold a structured meeting with their trustee, tax professional, and financial advisor before distributions begin. This meeting maps out the exact sequence of distributions, identifies which assets carry tax consequences, and confirms that the trust document actually permits the distribution strategy the family wants to pursue. Many families discover that their trust language restricts the trustee’s flexibility, forcing distributions that create unnecessary taxes or fail to address real family needs. Revisiting the trust document early in administration, rather than after distributions have already caused problems, prevents expensive mistakes and keeps family relationships intact. These coordination efforts set the stage for addressing the communication and management challenges that emerge once distributions actually begin.

Where Trust Administration Actually Falls Apart

The Communication Gap Between Trustees and Beneficiaries

Trustees and beneficiaries operate in fundamentally different worlds. The trustee sees the work: tracking assets across bank statements, filing tax returns, managing appraisals, coordinating with accountants. Beneficiaries see only silence and then a distribution check months later, wondering where their money went and whether the trustee made the right decisions. This gap between effort and visibility creates the single largest source of conflict in trust administration.

When a trustee waits nine months before making the first distribution, beneficiaries assume incompetence or theft rather than understanding that the trustee was legally required to resolve all debts and taxes first. The trustee should send written updates every 60 days explaining what work occurred during that period, what remains outstanding, and when distributions will likely occur. This transparency costs nothing but prevents the resentment that festers when beneficiaries feel excluded from information.

Many trustee-beneficiary conflicts escalate into expensive litigation simply because no one communicated clearly about timelines and obligations. A trustee who explains the 40-day waiting period, the tax filing requirements, and the appraisal process upfront transforms beneficiary expectations from frustration to understanding.

Valuation Problems That Expose Trustees to Liability

Asset valuation creates a second layer of problems that trustees consistently underestimate. When a family holds real estate in multiple states, retirement accounts with unclear beneficiary designations, privately held business interests, and investment accounts, determining accurate values for each asset becomes a specialized task requiring coordination across multiple professionals.

A trustee who values a piece of commercial real estate at $800,000 based on a quick online estimate, then later discovers the actual appraised value is $1.2 million, has created a massive tax problem for beneficiaries and exposed themselves to liability for negligence. Professional appraisals for real property must occur within the first 90 days of administration to establish accurate date-of-death values for tax basis calculations.

For business interests, the trustee should hire a business valuation firm to determine fair market value rather than guessing based on prior year tax returns. Retirement accounts present a different problem: many trusts were created decades ago with outdated beneficiary designations naming the trust itself as beneficiary, which triggers immediate income taxation of the entire account value. The trustee must contact the retirement account provider immediately to understand whether the beneficiary designation can be changed and what tax consequences exist. Failing to address this within the first 60 days of administration means the family loses months of opportunity to restructure distributions tax-efficiently.

Disputes Rooted in Perceived Unfairness

Disputes between beneficiaries rarely stem from disagreement about trust language itself. Instead, they emerge when one beneficiary perceives that another beneficiary received preferential treatment, timing advantages, or asset distributions that seemed unfair. A trustee who distributes $50,000 to one child for education funding but tells another child to wait six months for their distribution creates legitimate anger about apparent favoritism.

The trust document may permit this discretionary distribution, but the trustee failed to explain the reasoning or the timeline to the other beneficiary. Beneficiaries with conflicting interests require explicit communication about how the trustee interprets the trust language and what distributions each beneficiary can expect. This conversation should occur in writing within the first 120 days of administration, before distributions begin.

When distributions benefit some beneficiaries more substantially than others, the trustee should document the specific trust language justifying each distribution decision and provide copies to all beneficiaries. Families who address these communication challenges early avoid the pattern where one beneficiary files a lawsuit challenging the trustee’s decisions, forcing all other beneficiaries to spend $30,000 to $100,000 defending the administration in court. Prevention through transparency costs far less than litigation after conflict has already erupted.

Final Thoughts

Trust administration for families succeeds when trustees act with transparency, plan ahead, and recognize when professional guidance prevents costly mistakes. Asset coordination requires professional input from tax advisors and financial professionals before distributions begin, since retirement accounts, life insurance proceeds, real property, and business interests each carry different tax consequences and timing considerations. A trustee who maps these assets and their tax implications with professional guidance avoids the expensive mistakes that emerge when distributions trigger unexpected tax bills or miss opportunities for step-up in basis planning.

Families who invest time upfront in clear communication and proper coordination avoid the disputes and delays that consume far more time and money later. The trustee should establish a communication schedule, sending written updates every 60 days that explain completed work, outstanding obligations, and realistic distribution timelines. Beneficiaries who understand why distributions take nine months rather than three weeks accept the process rather than question the trustee’s competence, and generation-skipping transfer tax exemptions must be allocated during the initial administration phase, not after distributions have already occurred.

We at Law Offices of Roshni T. Desai provide personalized trust and probate administration services across Southern California, helping families navigate trust administration for families with clarity and precision. Contact us for a free consultation to discuss your specific situation and the steps that protect your family’s interests.