Trust Administration Guidance: Clear Roadmap for Executors and Trustees

Serving as a trustee or executor means handling significant financial and legal responsibilities. We at Law Offices of Roshni T. Desai know that many people in this role feel overwhelmed by the complexity.

This trust administration guidance walks you through each step, from understanding your duties to distributing assets correctly. You’ll learn what mistakes to avoid and how to stay on track with deadlines and legal obligations.

What Trust Administration Actually Involves

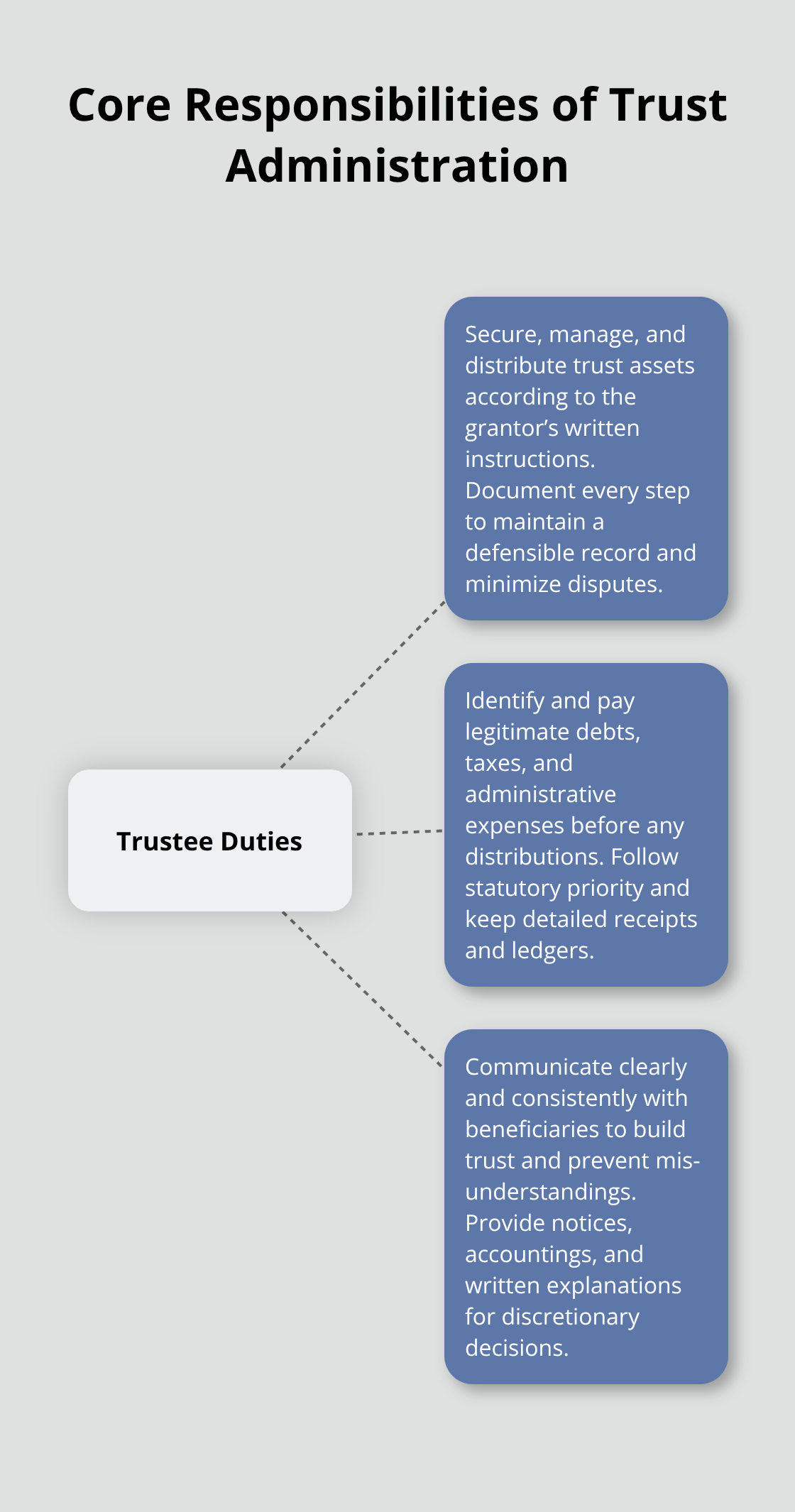

Trust administration is the operational side of estate planning-it’s where the document becomes action. After a grantor passes away or a successor trustee steps in, the trustee takes on three interconnected responsibilities that demand precision and attention to detail. The first involves identifying, securing, and eventually distributing trust assets according to the grantor’s written instructions. The second requires paying legitimate debts, taxes, and administrative costs before any beneficiary receives a penny. The third demands clear, honest communication with beneficiaries throughout the process, which prevents misunderstandings that can spiral into expensive disputes. These three areas overlap constantly, and mistakes in one area create problems in the others.

Securing and Managing Trust Assets

Your first job is to locate and secure every asset titled in the trust’s name. Real estate, investment accounts, bank deposits, and business interests must all be identified and their values determined as of the date of death or succession. Create a comprehensive inventory immediately-this isn’t just paperwork, it’s your legal protection. Open a dedicated trust bank account in the trust’s name to keep trust money separate from personal funds; mixing them together is one of the fastest ways to trigger beneficiary lawsuits and personal liability claims. For assets with fluctuating values like stocks or rental properties, obtain professional appraisals rather than guessing. Many trustees postpone this step thinking they’ll handle it later, but delays cost money through missed investment opportunities and create gaps in documentation that beneficiaries will question. Once you understand what you’re managing, follow any investment guidelines the trust document specifies. The prudent investor rule requires you to balance current income needs with preserving principal for future beneficiaries, which means reckless or overly conservative decisions both create liability.

Handling Debts and Taxes Before Distributions

Before distributing a single dollar to beneficiaries, you must identify and pay the grantor’s debts, final income taxes, and trust-related expenses. Contact the Social Security Administration, Department of Veterans Affairs, and life insurance companies to understand what benefits or proceeds are available. File the decedent’s final federal income tax return by April 15 and state returns according to your state’s deadline-missing these dates triggers penalties that reduce the estate’s value. If the trust generates income during administration, file a fiduciary return with the IRS. Pay creditor claims in the order state law requires, and maintain detailed records of every payment. Some trustees try to distribute assets quickly to avoid this work, but distributing money before paying legitimate debts exposes you to personal liability if creditors later pursue claims. The trust document controls the timing of distributions, not your preference for speed.

Building Trust Through Transparent Communication

Beneficiaries deserve timely information about what’s happening with their inheritance. Provide written notice of the trust’s terms, your contact information, and their rights within a reasonable timeframe after the grantor’s death or succession. Send annual accountings showing all income received, expenses paid, and distributions made. If beneficiaries request information about specific assets or transactions, respond promptly with documentation. Transparency costs almost nothing and prevents the suspicion that breeds litigation. Many trustees avoid communication because they fear questions, but silence guarantees conflict. When beneficiaries feel informed and respected, they’re far less likely to challenge your decisions later. This is especially important if the trust gives you discretion over distributions-explain your reasoning in writing, not just verbally.

These three responsibilities form the foundation of sound trust administration. The mistakes trustees make most often stem from overlooking one of these areas or treating them as separate tasks rather than interconnected duties that shape each other.

Common Mistakes Trustees and Executors Make

The gap between understanding trust administration in theory and executing it correctly is where most trustees stumble. Many trustees inherit the role without formal training, relying on family members’ vague assurances that they’ll figure it out as they go. This approach guarantees mistakes. The most damaging errors fall into three categories, and each one creates cascading problems that are expensive and time-consuming to fix.

Treating Fiduciary Duties as Optional Guidelines

The first mistake is treating fiduciary duties as optional guidelines rather than legal obligations with real consequences. A fiduciary duty means you must act in the beneficiaries’ best interests, not your own, and you must follow the trust document precisely even when you disagree with the grantor’s choices. Many trustees rationalize small deviations-using trust funds to cover a family member’s medical bill, investing trust money in a relative’s business, or delaying a distribution because they think the timing is wrong. These actions expose you to personal liability. A beneficiary can sue you individually to recover misused funds, and your homestead, retirement accounts, and personal savings become targets. Courts don’t accept good intentions as a defense; they examine whether your actions matched the trust document and state law.

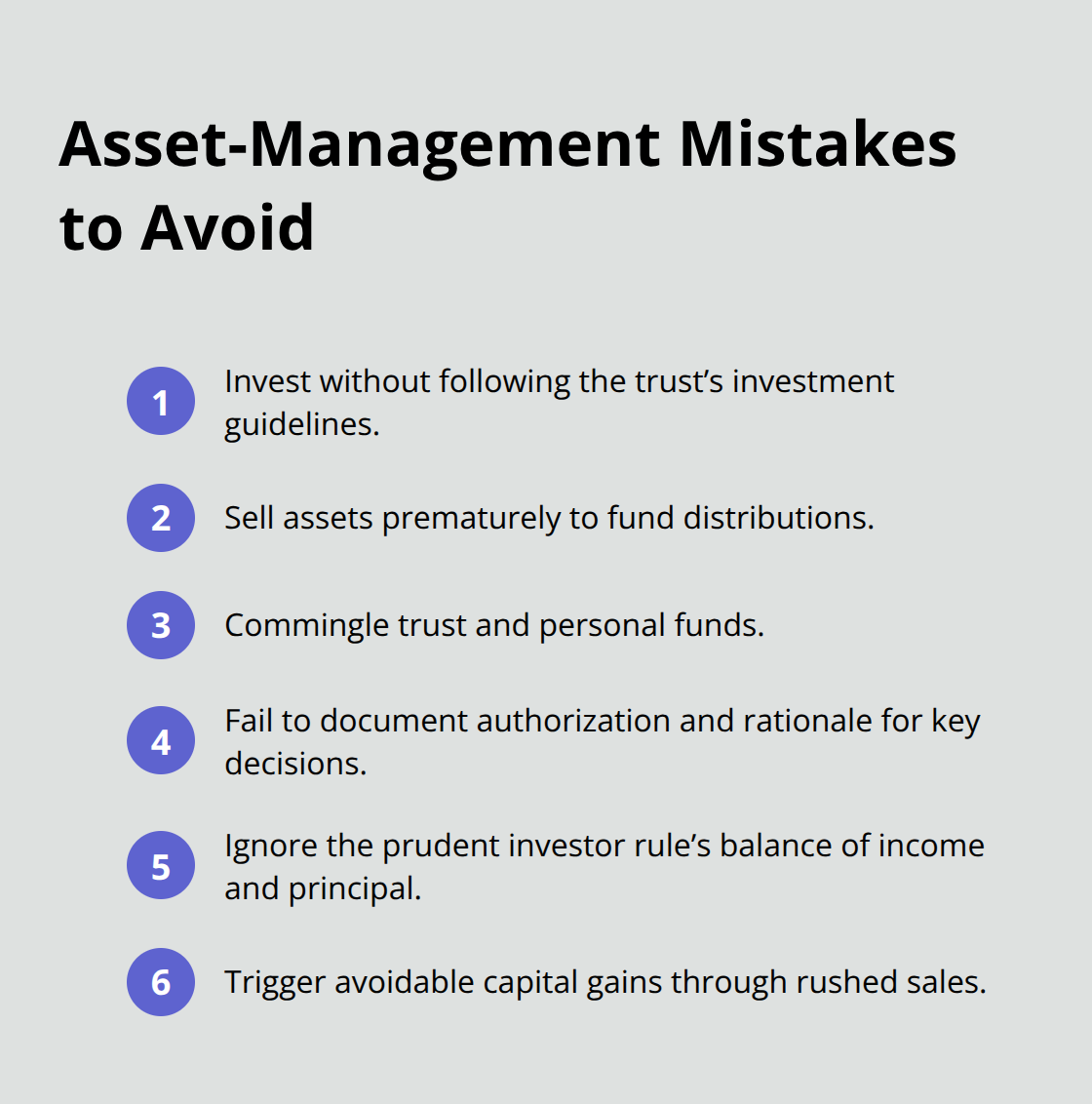

Making Asset Management Decisions Without Documentation

The second mistake involves asset management decisions that lack documentation or authorization. Some trustees invest trust money without understanding the trust’s investment guidelines or the prudent investor rule, which requires balancing current income needs with preserving principal for future beneficiaries. Others sell assets too quickly to pay distributions, triggering unnecessary capital gains taxes that reduce the estate’s value. A few trustees commingle trust assets with personal funds, which destroys the clear record-keeping that protects you if questions arise later. This separation of funds is not optional-it’s a foundational requirement that prevents beneficiaries from questioning whether you diverted money for personal use.

Missing Critical Deadlines and Postponing Distributions

The third mistake is postponing critical deadlines-filing tax returns, notifying beneficiaries, paying creditors, or making required distributions. Delays on federal income tax returns trigger penalties that compound monthly. Missing state deadlines for beneficiary notices creates legal violations that beneficiaries can cite in lawsuits. Postponing distributions without legitimate reason signals to beneficiaries that something is wrong, fueling suspicion and conflict. The trustee’s job demands speed on administrative tasks and deliberation on discretionary decisions, not the opposite.

These three categories of mistakes share a common thread: they all stem from either misunderstanding your legal obligations or failing to document your decisions. Understanding what you must do and why you must do it is the first step toward avoiding these pitfalls. Avoiding common pitfalls keeps you on track and protects both the trust and your personal liability.

How to Start Trust Administration the Right Way

Start by gathering every document related to the trust and the grantor’s finances. Locate the original trust agreement, any amendments or codicils, the death certificate (obtain at least five certified copies), bank statements, investment account statements, property deeds, insurance policies, and tax returns from the past three years. Review your trust document word-for-word to identify any directed trustee language, modification procedures, and distribution rules. The second and third readings reveal investment restrictions, distribution timelines, and special instructions that shape every decision you’ll make. If the trust language is unclear, write down the specific passages that confuse you. An attorney can interpret ambiguous language rather than you guessing and discovering later that you misunderstood the grantor’s intent.

Open a Dedicated Trust Bank Account

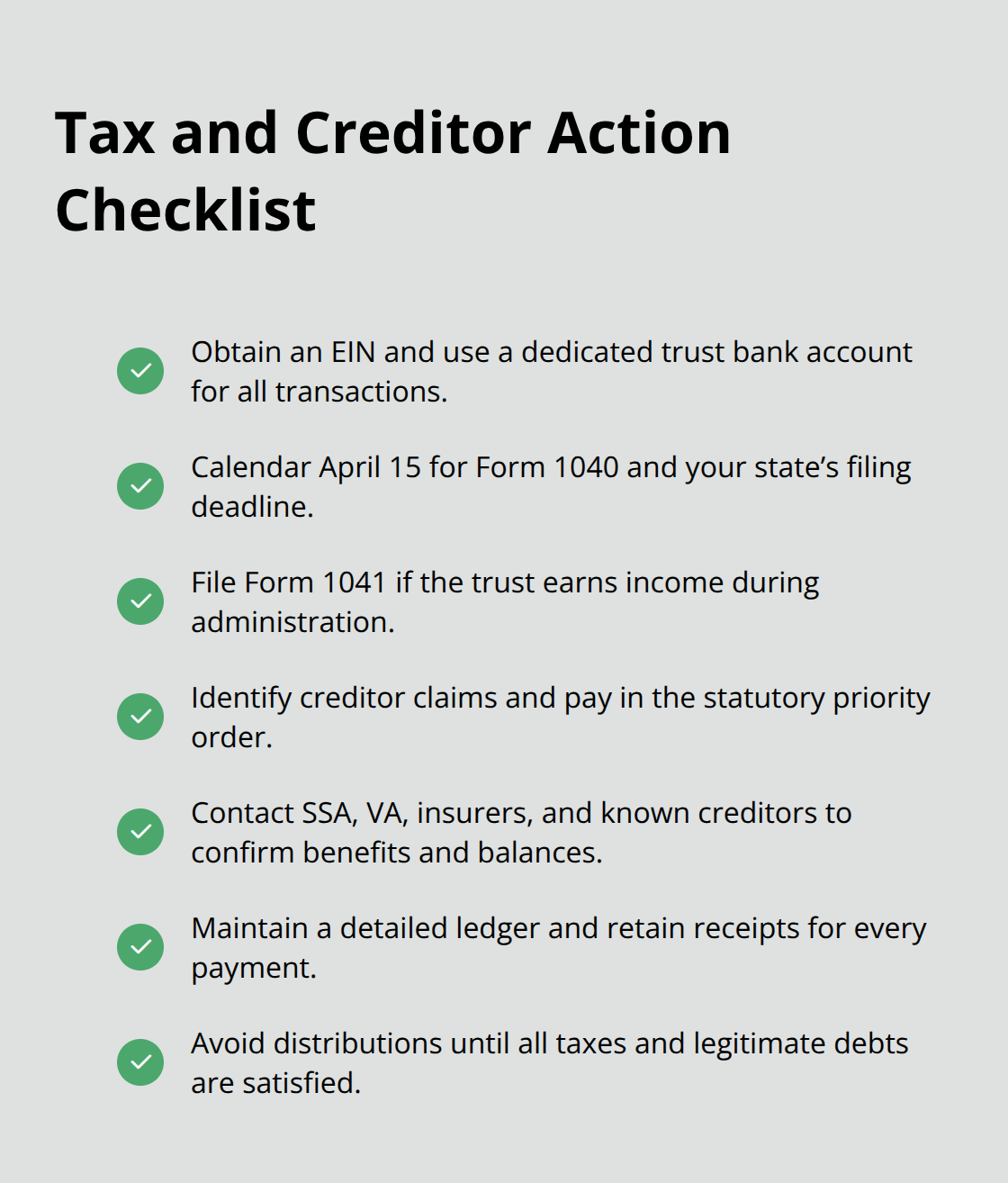

Open a dedicated bank account in the trust’s name immediately after the grantor’s death or succession, and obtain a federal Employer Identification Number (EIN) from the IRS-you cannot use the decedent’s Social Security number. This account becomes your command center for all trust transactions. Deposit any liquid assets, insurance proceeds, or income into this account. Keep meticulous records of every deposit and withdrawal. When you pay the grantor’s final medical bills, funeral expenses, or property taxes from this account, you have a clear paper trail that protects you if beneficiaries later question whether funds were spent appropriately. Many trustees postpone this step thinking they’ll handle it later, but every week of delay creates gaps in documentation and increases the risk that trust money gets mixed with personal funds.

Inventory Assets and Determine Their Values

Inventory all trust assets and determine their values as of the date of death or succession. For real estate, obtain a professional appraisal rather than relying on recent sale prices in the neighborhood. For investment accounts, use the closing price on the date of death or succession, which becomes the tax basis for capital gains calculations. For business interests, hire a business appraiser if the trust holds a significant stake. For personal property like jewelry, art, or vehicles, get written appraisals for items worth more than five thousand dollars. This upfront investment in accurate valuations prevents disputes later and ensures tax filings are correct.

File Tax Returns and Pay Creditors

File the grantor’s final federal income tax return by April 15 using Form 1040, and file any required state income tax return by your state’s deadline (typically May 1 in most states). If the trust generates income during administration, file a fiduciary return with the IRS using Form 1041. Missing these deadlines triggers penalties that compound monthly and reduce the estate’s value.

Pay creditor claims in the order state law requires. Contact the Social Security Administration, Department of Veterans Affairs, life insurance companies, and any creditors you identify through the grantor’s mail and financial statements. Document every payment with receipts and keep a ledger showing the date, creditor name, amount paid, and the reason for payment. This documentation is your defense if a beneficiary later questions whether you paid legitimate debts or misused trust funds.

Distribute Assets According to the Trust Document

Distribute assets according to the trust document’s terms, not according to your own timeline or preferences. If the trust directs immediate distribution to beneficiaries, make those distributions within a reasonable timeframe after you’ve paid all debts and taxes. If the trust directs that assets remain in the trust for a specified period or until beneficiaries reach a certain age, follow that instruction exactly. Obtain signed receipts from each beneficiary confirming they received their distribution. These receipts prove you completed your obligation and prevent beneficiaries from later claiming they never received their inheritance.

Final Thoughts

Trust administration requires precision, documentation, and adherence to legal obligations that protect both the trust and your personal liability. The three core responsibilities-securing assets, paying debts and taxes, and communicating transparently with beneficiaries-form the foundation of sound administration. Mistakes in any of these areas create cascading problems that become expensive and time-consuming to fix.

Your role as trustee or executor demands that you understand the trust document thoroughly, inventory assets accurately, file tax returns on time, and distribute assets according to the grantor’s written instructions. These steps protect you from personal liability and prevent beneficiaries from questioning your decisions later. The documentation you create during administration becomes your defense if disputes arise, and professional guidance early in the process prevents mistakes that are difficult and expensive to correct.

We at Law Offices of Roshni T. Desai provide personalized trust administration guidance across Southern California with over 25 years of experience. Our firm handles the legal and administrative details so you can focus on honoring the grantor’s wishes. Contact us for a free consultation to discuss your situation and next steps.