Trust Tax Planning California: Minimizing Tax While Protecting Assets

Trust tax planning in California requires more than generic strategies. Your assets face unique state and federal tax pressures that demand a tailored approach.

At Law Offices of Roshni T. Desai, we’ve seen families lose thousands to preventable tax mistakes. This guide shows you how trusts can protect your wealth while keeping taxes manageable.

How Trusts Shape Your California Tax Picture

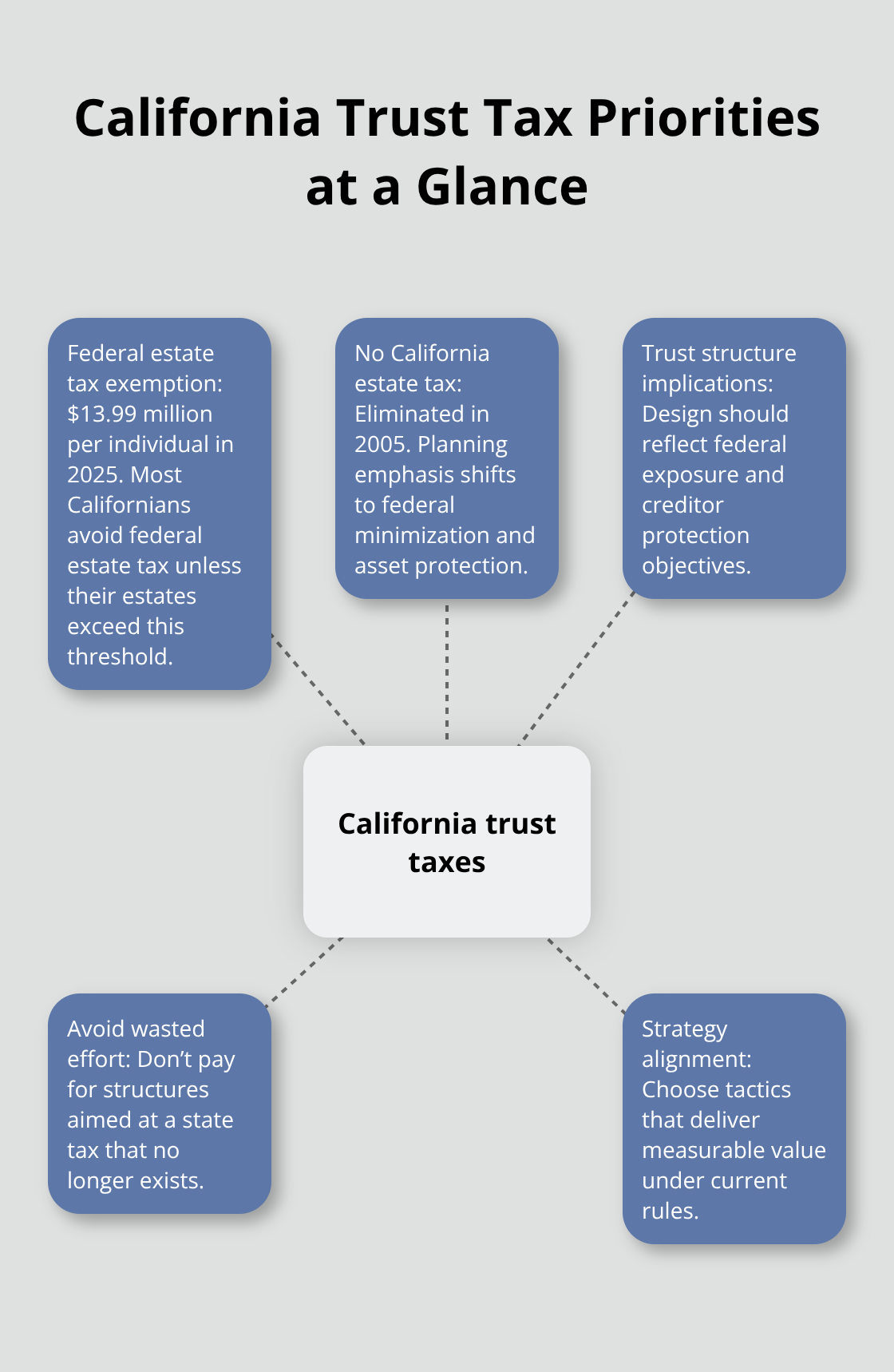

Trusts are not tax-elimination tools, but they are powerful tax-management vehicles when structured correctly. The federal estate tax exemption sits at $13.99 million per individual for 2025, according to the IRS, which means most California residents won’t face federal estate tax unless their estates exceed this threshold. California eliminated its state estate tax in 2005, so your planning focus shifts entirely to federal tax minimization and asset protection. This distinction matters because it changes how you should structure your trust and what strategies deliver real value. Many Californians waste money on trust structures designed to avoid a state tax that no longer exists, when they should address federal exposure and creditor protection instead.

Revocable trusts offer flexibility but deliver no tax savings

A revocable living trust lets you maintain complete control over your assets during your lifetime and avoid probate when you pass. The IRS treats revocable trusts as part of your personal estate for tax purposes, so they provide zero federal estate tax reduction. What they do provide is probate avoidance, which saves your heirs thousands in court fees and delays-probate in California typically costs 3-7% of estate value according to court records. If your estate is under $13.99 million, a revocable trust’s real benefit is streamlined administration and privacy, not tax savings. You can modify or revoke a revocable trust at any time, making it flexible but not protective against creditors or lawsuits.

Irrevocable trusts create tax advantages and asset protection

Irrevocable trusts work differently. Once you transfer assets into an irrevocable trust, you cannot take them back or change the terms without beneficiary consent or a court order. This permanent transfer removes the assets from your taxable estate, reducing your federal estate tax exposure dollar-for-dollar. If you have $15 million in assets and transfer $1 million to an irrevocable trust, your taxable estate drops to $14 million, staying under the exemption threshold. Irrevocable trusts also shield assets from creditors and lawsuits because you no longer own them legally. The trade-off is loss of control and flexibility. The trust files its own tax return and pays taxes on income it retains, or beneficiaries pay taxes on distributions they receive.

Why the right structure matters for your situation

This complexity demands professional guidance to avoid mistakes that cost far more than the planning itself. The specific trust type you need depends on your asset level, family situation, and goals. A trust that works for one family may create unnecessary complications for another. Understanding these structural differences positions you to make informed decisions about which strategies actually apply to your circumstances-and which ones you can safely skip.

Tax-Cutting Strategies With Trusts

The gap between understanding trusts and actually using them to reduce taxes is where most California families stumble. Three concrete strategies separate effective tax planning from wasted effort.

Annual gift tax exclusions compound over time

The annual gift tax exclusion is your most accessible tool. For 2025, you can give $19,000 per person per year without touching your federal exemption, according to the IRS. A married couple with three adult children can transfer $114,000 annually tax-free. Over a decade, that strategy moves $1.14 million out of your taxable estate without paperwork or complexity. Most families ignore this because the numbers seem small, but consistent annual gifting compounds significantly.

Direct payments for education or medical expenses bypass the exclusion entirely. You can pay a grandchild’s tuition directly to the school or cover a parent’s long-term care costs and remove those dollars from your estate at no tax cost. This strategy works best when you start early and execute it consistently each year.

Irrevocable Life Insurance Trusts eliminate death benefit taxation

Life insurance proceeds normally inflate your taxable estate, potentially creating a tax bill your heirs must pay from liquid assets. An ILIT owns the policy instead of you, removing the death benefit from estate taxes entirely. If you have a $2 million policy and your estate sits at $14 million, that policy pushes you $1 million over the exemption threshold, triggering federal taxes your beneficiaries must cover. Placing the policy in an ILIT eliminates that tax exposure while providing cash to pay estate costs or equalize inheritances among heirs.

The trade-off is irrevocability-you cannot access the policy or change beneficiaries without trustee consent. This permanent structure protects the proceeds but removes your flexibility to modify the arrangement later.

Qualified Personal Residence Trusts reduce gift tax on your home

QPRTs let you transfer your home at a reduced gift tax cost while keeping occupancy rights for a set period. You place the home into the trust today, but retain the right to live there for, say, ten years. The gift tax value drops because you’re only transferring a future interest, not immediate ownership. The IRS values that future interest using interest rates and life expectancy tables, typically reducing the taxable gift by 30-50% depending on the term length and rates.

After your occupancy period ends, the home passes to beneficiaries outside your estate, eliminating future appreciation from taxes. This approach works when you own a California home that has appreciated significantly and you’re comfortable eventually moving out.

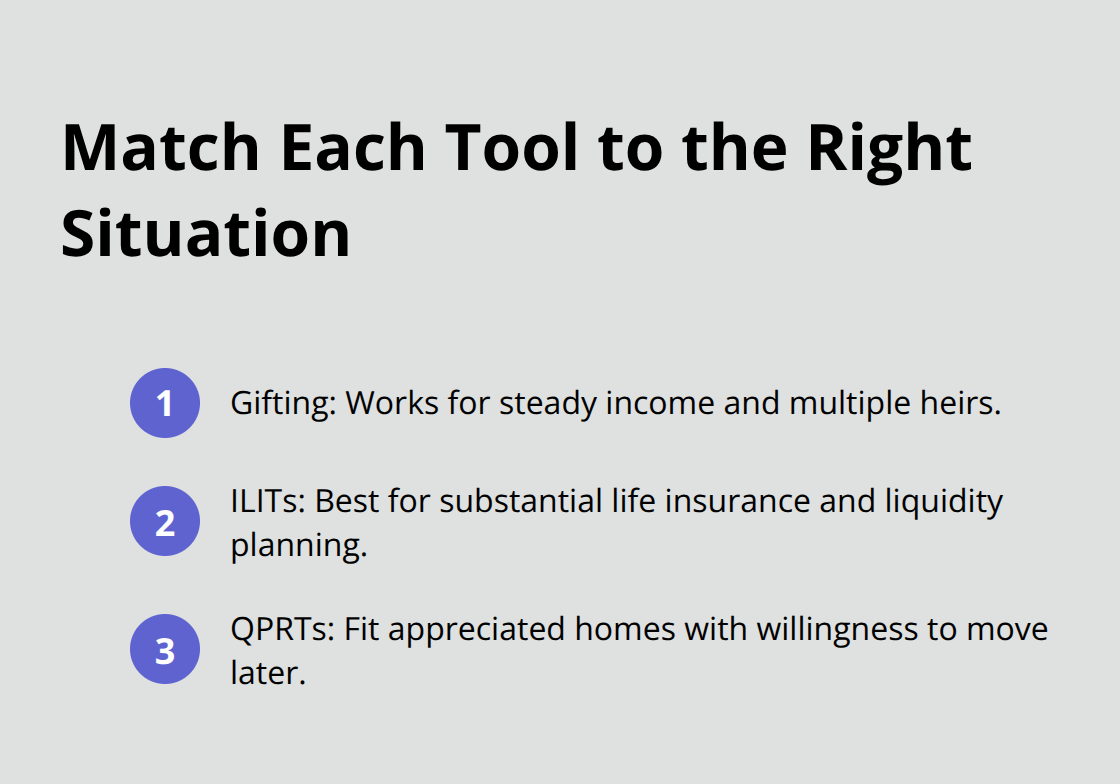

Matching strategies to your assets and family structure

Each strategy targets different assets and family situations. Gifting works for those with steady income and multiple heirs. ILITs suit those with substantial life insurance. QPRTs fit homeowners with appreciated property and a willingness to eventually relinquish occupancy.

The right choice depends on what you own, who you want to benefit, and how much control you need to keep. These three tools form the foundation of tax-efficient planning, but they only deliver results when you align them with your specific circumstances. The next section addresses the mistakes that undermine even well-intentioned planning efforts.

Where Trust Planning Goes Wrong

Outdated trusts create tax exposure and family conflict that active management prevents. Many Californians set up trusts and treat them as permanent fixtures that never require attention. A trust drafted ten years ago reflects your circumstances from a decade back, not your current situation. Marriage, divorce, the birth of grandchildren, significant asset growth, or changes in tax law all demand trust updates. California law requires trustees to notify beneficiaries of trust changes, and failing to do so creates legal exposure. The IRS allows you to modify certain irrevocable trusts through decanting, a process that transfers trust assets to a new trust with updated terms without triggering gift taxes. If your trust hasn’t received a review in more than three years, or if you’ve experienced major life events like remarriage or the death of a named beneficiary, the cost of a review appointment is trivial compared to the cost of outdated provisions that misalign with your actual goals.

Uncoordinated assets create tax inefficiencies and family disputes

Many families fail to coordinate their trusts with their wills and beneficiary designations on retirement accounts and insurance policies. A trust that names your oldest child as trustee contradicts a will naming your spouse as executor, which creates conflict and delays during administration. Retirement accounts like IRAs and 401(k)s pass by beneficiary designation, bypassing your trust entirely unless you name the trust as beneficiary-a choice that often triggers unfavorable tax treatment. Life insurance policies work the same way. If your trust holds your home and most assets but your $500,000 life insurance policy names your ex-spouse as beneficiary because you never updated it after divorce, your current family receives less than you intended. The solution requires documenting which assets flow through your trust, which pass through beneficiary designations, and which transfer through other mechanisms like joint ownership or transfer-on-death deeds. A comprehensive asset inventory prevents gaps and overlaps that create tax inefficiencies and family disputes.

Tax law changes demand regular trust reviews

State and federal tax rules shift constantly, and trusts that ignore these changes forfeit available savings. California’s elimination of state estate tax in 2005 means trusts structured to minimize state taxes no longer serve their intended purpose. Federal generation-skipping transfer tax rules changed in 2010 and again in 2025, affecting how generational wealth transfers work. The federal estate tax exemption fluctuates annually and is scheduled to drop from $13.99 million to roughly $7 million in 2026 unless Congress acts. A trust that worked perfectly in 2024 may create unexpected tax exposure in 2026 if it doesn’t account for exemption changes. Annual trust reviews assess whether your structure still aligns with current law and your circumstances. The cost of a review is far lower than the cost of undoing a poorly structured arrangement or paying excess taxes.

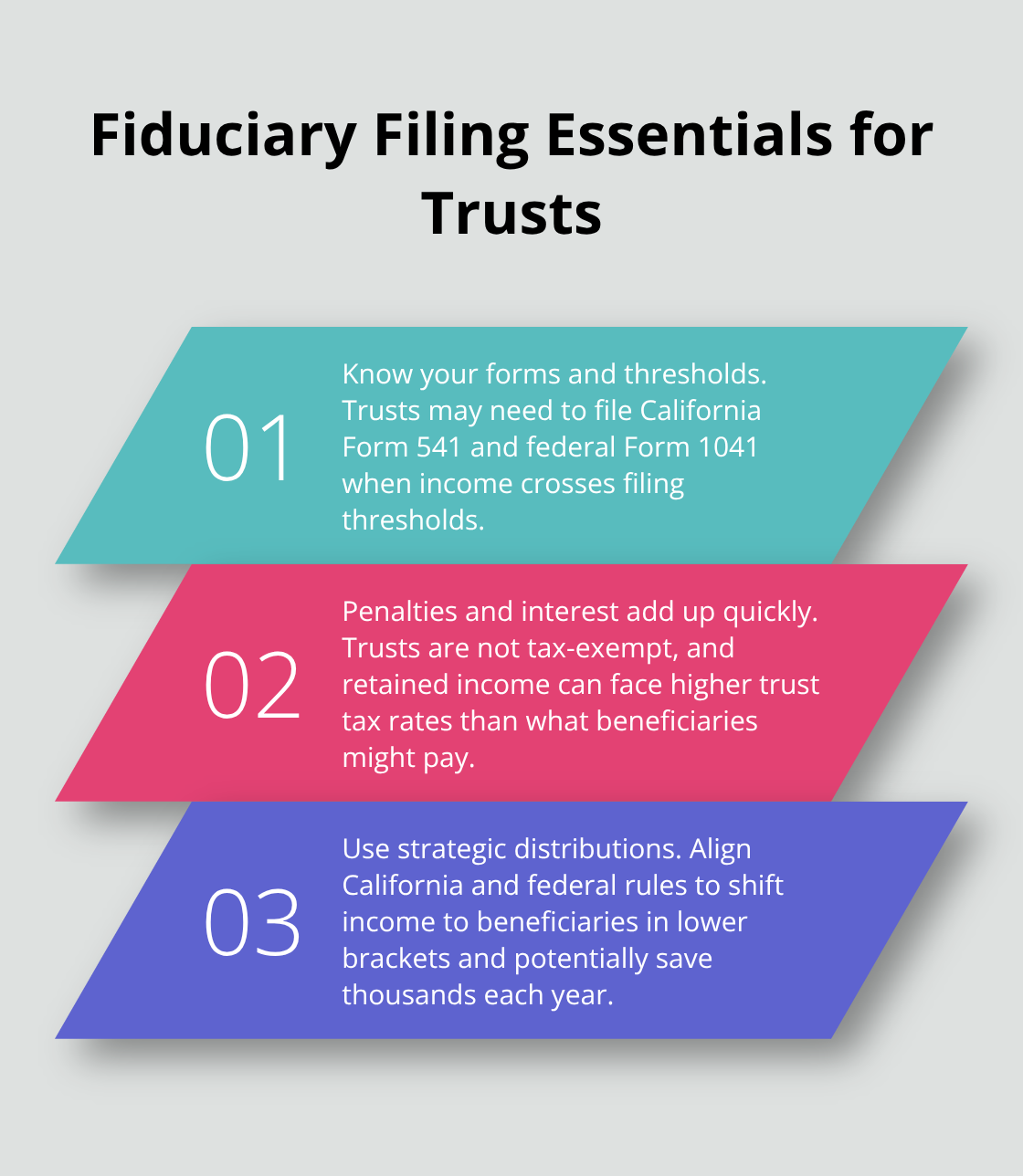

Fiduciary tax filing requirements carry real penalties

Fiduciaries must file Form 541 California Fiduciary Income Tax Returns and federal Form 1041 if the trust generates income above certain thresholds. Failure to file these returns triggers penalties and interest that accrue quickly. Many trustees assume trusts are tax-exempt, which they are not.

Income retained by the trust faces higher tax rates than distributions to beneficiaries in lower brackets. A simple strategic distribution decision can save thousands annually but requires understanding both California and federal rules. The combination of outdated documents, uncoordinated assets, and overlooked tax requirements transforms what should be a protective structure into a liability that burdens your heirs with preventable complications and costs.

Final Thoughts

Federal estate tax exemptions drop significantly in 2026 unless Congress extends current law, cutting your planning window from $13.99 million per person to roughly $7 million. Families who wait until 2026 to implement trust tax planning California strategies face compressed timelines and fewer options to move assets efficiently. Starting now allows you to execute gifting strategies, establish irrevocable trusts, and restructure life insurance before exemption changes force reactive decisions that limit your flexibility.

California’s elimination of state estate tax in 2005 shifted planning focus entirely to federal minimization and asset protection, which means your trust strategy should emphasize federal exemption management and creditor shielding rather than state tax avoidance. Many generic trust templates ignore this reality and cost families thousands in unnecessary complexity. Your California-specific situation demands planning that accounts for federal rules while leveraging state asset protection laws that other states don’t offer.

Trust tax planning requires coordinating multiple moving parts: trust structure, beneficiary designations, asset titling, annual gifting, and ongoing compliance with California and federal filing requirements. A single misalignment between your trust and your will, or an overlooked tax filing deadline, can undermine years of careful planning. We at Law Offices of Roshni T. Desai provide personalized estate planning and trust administration across Southern California, and we offer free consultations with flexible scheduling to discuss your situation without pressure or commitment.